- Processed Food

- Tilapia Market

Tilapia Market Size, Share, and Growth Forecast, 2025 - 2032

Tilapia market by Species (Nile Tilapia, Blue Tilapia, Mozambique Tilapia, Wami Tilapia), Application (Food Industry, Pharmaceutical Industry, Animal Feed, Pet Food, Food Service, Retail), and Regional Analysis for 2025 - 2032

Tilapia Market Size and Trends Analysis

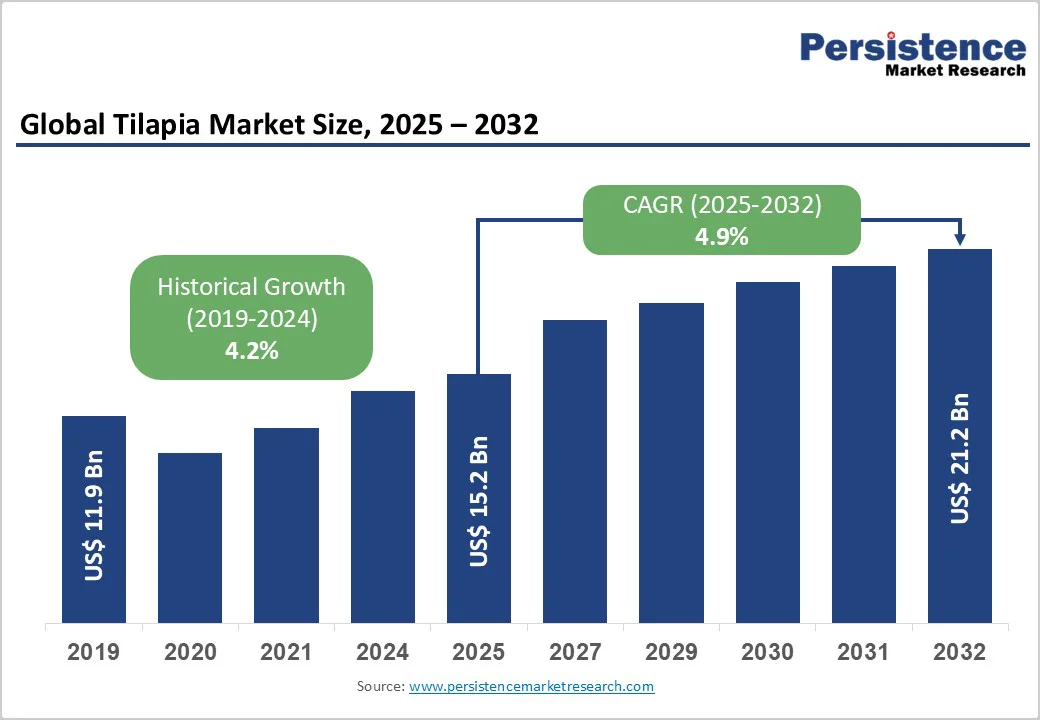

The global tilapia market size is likely to be valued US$ 15.2 Bn in 2025, projected to reach US$ 21.2 Bn by 2032 growing at a CAGR of 4.9% during the forecast period from 2025 to 2032.

The market is experiencing robust growth driven by increasing demand for affordable, high-protein seafood, rising adoption of sustainable aquaculture practices, and advancements in fish farming technologies.

The market is further propelled by innovations in disease-resistant tilapia breeds and eco-friendly farming methods, catering to consumer preferences for sustainable seafood. The growing acceptance of tilapia as a versatile, cost-effective protein source in processed foods and nutraceuticals is a key growth factor.

Key Industry Highlights:

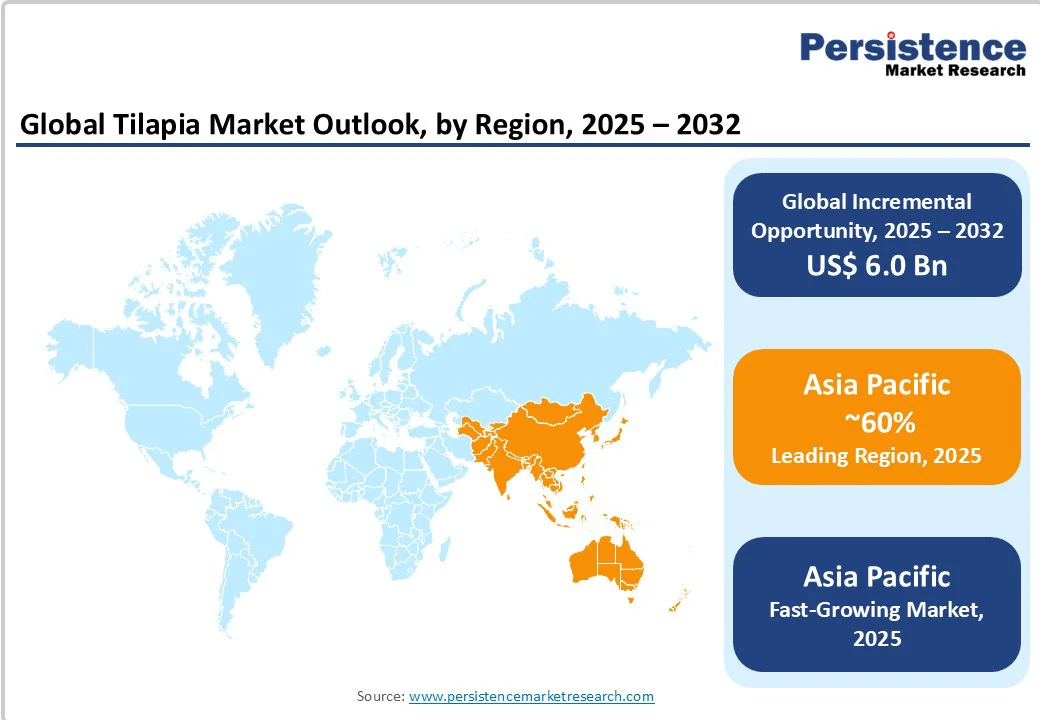

- Leading Region: Asia Pacific, commanding a 60% market share in 2025, driven by dominant production in China and expanding aquaculture in India.

- Fastest-growing Region: Asia Pacific, fueled by population growth and rising seafood consumption in emerging economies.

- Dominant Species: Nile Tilapia, holding approximately 70% of the market share, due to its fast growth and adaptability to diverse farming systems.

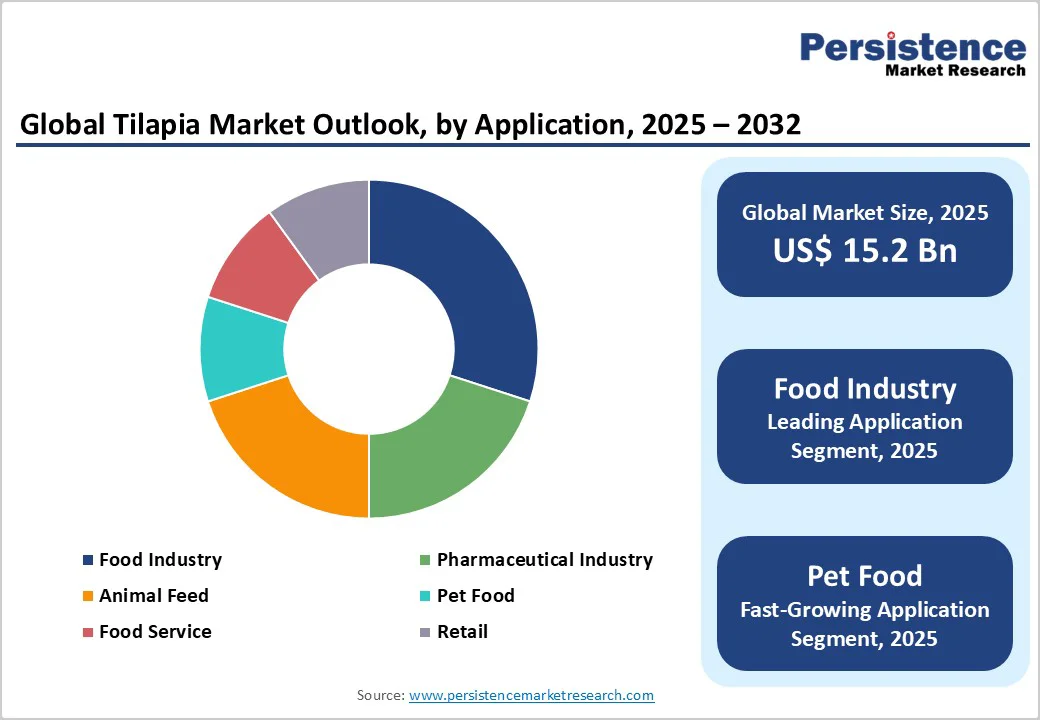

- Leading End-use: Food Industry, accounting for over 60% of market revenue, driven by demand for fresh and processed freshwater fish products.

- Key Market Driver: Tilapia is a cost-effective, lean, and protein-rich fish, making it popular among consumers seeking nutritious yet affordable food options.

- Growth Opportunity: Expansion in aquaculture fish-derived omega-3 supplements for pharmaceuticals and high-protein pet food formulations.

| Key Insights | Details |

|---|---|

| Tilapia Market Size (2025E) | US$ 15.2 Bn |

| Market Value Forecast (2032F) | US$ 21.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.2% |

Market Dynamics

Driver-Rising demand for affordable protein and sustainable aquaculture

Rising demand for affordable protein and sustainable aquaculture is a key driver of growth in the global tilapia market. Tilapia is recognized as a cost-effective, lean, and protein-rich fish, making it an accessible source of nutrition for a growing global population, particularly in developing regions where protein security is a concern. Its mild flavour and versatility in culinary applications further enhance its appeal to consumers, restaurants, and foodservice providers.

Focusing on sustainable aquaculture practices is reshaping production strategies. Environmental concerns, regulatory frameworks, and consumer preferences are encouraging producers to adopt eco-friendly techniques, such as recirculating aquaculture systems (RAS), integrated multi-trophic aquaculture, and the use of sustainable, low-impact feeds. These practices not only reduce ecological footprints but also improve operational efficiency and product quality.

Restraint - Disease outbreaks and environmental concerns

Disease outbreaks and environmental concerns are major challenges affecting the global tilapia market. Aquaculture systems, particularly intensive pond and cage farming, are vulnerable to bacterial, viral, and parasitic infections, which can cause significant mortality and economic losses.

Common diseases, such as Streptococcus infections, tilapia lake virus (TiLV), and bacterial gill disease, not only reduce productivity but also increase operational costs due to the need for medications, vaccines, and biosecurity measures. Inadequate disease management can lead to contamination risks, affecting both domestic consumption and export quality standards.

Environmental concerns further compound these challenges. Intensive tilapia farming can result in water pollution from uneaten feed, faecal waste, and chemical residues, disrupting local ecosystems and reducing water quality. Habitat degradation, particularly in coastal and inland water systems, can affect biodiversity and trigger regulatory scrutiny. Climate change, including rising water temperatures and extreme weather events, also impacts growth rates, feed efficiency, and disease susceptibility.

Opportunity - Expansion in value-added products and nutraceuticals

Increasingly expanding into value-added products and nutraceutical applications, creating new growth avenues beyond traditional fresh and frozen fish sales. Value-added freshwater fish products, such as ready-to-cook fillets, marinated portions, and frozen convenience meals, cater to the growing demand for convenience and premium-quality seafood in the retail and foodservice sectors.

These products allow companies to achieve higher margins, differentiate their offerings, and appeal to health-conscious and time-sensitive consumers.

Nutraceutical applications, including omega-rich extracts and aquaculture fish oil, are gaining traction due to their health benefits, including support for heart, joint, and cognitive health. Aquaculture fish oil, for instance, has been explored for its bioactive compounds and high omega-3 content, aligning with the global trend toward functional foods and dietary supplements.

Category-wise Analysis

Species Insights

Nile Tilapia dominates the market, account 70% of the share in 2025. Its strong position stems from rapid growth rates, high disease resistance, and adaptability to diverse farming systems such as ponds and cages. These traits make it a preferred species for large-scale, cost-effective aquaculture production across Asia, Africa, and Latin America.

Blue Tilapia is the fastest-growing segment, driven by rising demand for hybrid breeds offering superior fillet yield, faster growth, and adaptability to controlled aquaculture environments. Its resilience to varying water conditions and suitability for urban and recirculating aquaculture systems make it a preferred choice for sustainable and high-efficiency fish farming operations worldwide.

End-use Insights

Food Industry leads with over 60% share, driven by growing demand for fresh fillets, frozen portions, and processed products across retail and food service channels. Rising seafood consumption, coupled with freshwater fish’s affordability, mild flavour, and nutritional benefits, continues to strengthen its position as a preferred protein source globally.

Pet Food is the fastest-growing, fueled by rising demand for high-protein, nutrient-rich formulations that support premium pet nutrition. Freshwater fish’s digestibility, lean protein content, and low allergen potential make it an ideal ingredient in specialized pet diets, especially for health-focused and premium product categories targeting companion animal wellness.

Regional Insights

North America Tilapia Market Trends

North America accounts for 20% in 2025, driven by strong consumer demand in the United States and Canada. The region’s dependence on imports mainly from China, Indonesia, and Latin America continues to shape its market dynamics, as local production remains limited due to high operating costs and regulatory constraints. Increasing health awareness and the growing popularity of lean, protein-rich, and sustainable seafood have made freshwater fish a staple in North American diets.

Retailers and food service providers are emphasizing responsibly sourced and certified freshwater fish to align with consumer preferences for environmentally friendly products. In parallel, the U.K. market, though part of Europe, reflects similar consumption patterns. Guided by the Food Standards Agency (FSA), the U.K. is witnessing a steady rise in freshwater fish imports to meet demand for affordable, omega-3-rich seafood within health-conscious and flexitarian diets.

Europe Tilapia Market Trends

Europe holds about 15% market share, led by Germany and France emerging as key contributors to regional growth. The market’s expansion is supported by the European Union’s aquaculture subsidies, which encourage sustainable fish farming practices, technological innovation, and local production to reduce reliance on imports. Germany’s strong retail sector and increasing consumer preference for affordable, protein-rich seafood have driven the popularity of aquaculture fish, particularly in frozen and ready-to-cook formats.

France, on the other hand, benefits from growing demand for ethically sourced and eco-labeled seafood, aligning with the EU’s “Blue Growth” strategy promoting sustainable aquaculture. Additionally, partnerships between European distributors and Asian producers ensure a consistent supply of high-quality, traceable freshwater fish products. Retail chains and food service providers are expanding their offerings of responsibly farmed aquaculture fish to meet consumer expectations for sustainability and value.

Asia Pacific Tilapia Market Trends

Asia Pacific commands around 60% share and is the fastest-growing region. This leadership is largely driven by China, which produces over 1.8 Mn tons of freshwater fish annually, supported by well-established aquaculture infrastructure, advanced breeding programs, and strong export-oriented production. China remains a key global supplier, exporting to major markets such as the United States and Europe.

India is emerging as a significant growth hub, with expanding pond-based and cage aquaculture systems across states such as Andhra Pradesh, Odisha, and West Bengal. Government initiatives promoting sustainable aquaculture, coupled with increasing private investments, are accelerating production efficiency and quality standards. Other Southeast Asian countries, including Indonesia, Thailand, and the Philippines, are also strengthening their aquaculture fish industries through technology adoption and international partnerships.

Competitive Landscape

The global tilapia market is highly competitive, driven by growing consumer demand for affordable, protein-rich seafood and increasing awareness of sustainable aquaculture practices.

Major players such as Baiyang Investment Group, Blue Ridge Aquaculture, and Nireus Aquaculture are investing heavily in innovative and eco-friendly farming methods, including recirculating aquaculture systems (RAS) and integrated multi-trophic aquaculture, to ensure year-round production while minimizing environmental impact.

Companies are also emphasizing value-added processing offering frozen fillets, seasoned portions, and ready-to-eat products to appeal to health-conscious and convenience-driven consumers worldwide.

In addition, strong global distribution networks and strategic partnerships with retailers, food service providers, and exporters are helping these producers expand their market reach across North America, Europe, and Asia Pacific. The competition is further intensified by technological advancements in feed efficiency, genetics, and traceability systems that improve quality and sustainability.

Key Developments

- In October 2024: A state agency in Chennai is culling invasive tilapia in Adyar Creek to protect native species. Tilapia spread quickly due to its adaptability and high reproductive rate, with the introduction of Genetically Improved Farmed Tilapia (GIFT) worsening the issue. The Chennai River Restoration Trust (CRRT) has launched a culling operation to remove adult tilapia and safeguard local biodiversity.

- In July 2024: Aller Aqua and IDH launched a partnership to support out-grower tilapia farming in Kenya’s Homabay and Migori counties. The project aims to improve smallholder aquaculture by providing quality inputs, training, and market access. With over 250 farmers at the launch, the initiative promotes sustainable, inclusive aquaculture practices, offering farmers two production cycles annually and fostering entrepreneurship and gender equality.

Companies Covered in Tilapia Market

- Nireus Aquaculture

- Blue Ridge Aquaculture

- China Fishery Group

- Hainan Xiangtai Fishery

- Baiyang Investment Group

- Nile Aqua

- American Pride Seafoods

- Wada Farms

- Aquamaof Aquaculture Technologies

- Northern Tilapia

- Golden Prize Caviar

- Fischer Seafoods.

- Others

Frequently Asked Questions

The global tilapia market is projected to reach US$ 15.2 Bn in 2025, driven by demand for affordable protein and sustainable aquaculture.

Adoption of eco-friendly farming techniques, including recirculating aquaculture systems (RAS) and sustainable feed, reduces environmental impact while improving productivity.

The market is poised to witness a CAGR of 4.9% from 2025 to 2032, supported by eco-friendly farming innovations.

Expansion in omega-3 nutraceuticals and pet food offers opportunities for freshwater fish-derived value-added products.

China Fishery Group, Nireus Aquaculture, Blue Ridge Aquaculture, and American Pride Seafoods lead through sustainable tilapia production.