- Pharmaceuticals

- Targeted Cancer Therapies Market

Targeted Cancer Therapies Market Size, Share, and Growth Forecast, 2026 - 2033

Targeted Cancer Therapies Market by Therapy Type (Monoclonal Antibodies, Signal Transduction Inhibitors, Hormone Therapies, Small Molecule Inhibitors), Disease Indication (Lung Cancer, Breast Cancer, Colorectal Cancer, Gastrointestinal), End-User (Hospitals, Cancer and Radiation Therapy Centers, Clinics), and Regional Analysis for 2026-2033

Targeted Cancer Therapies Market Share and Trends Analysis

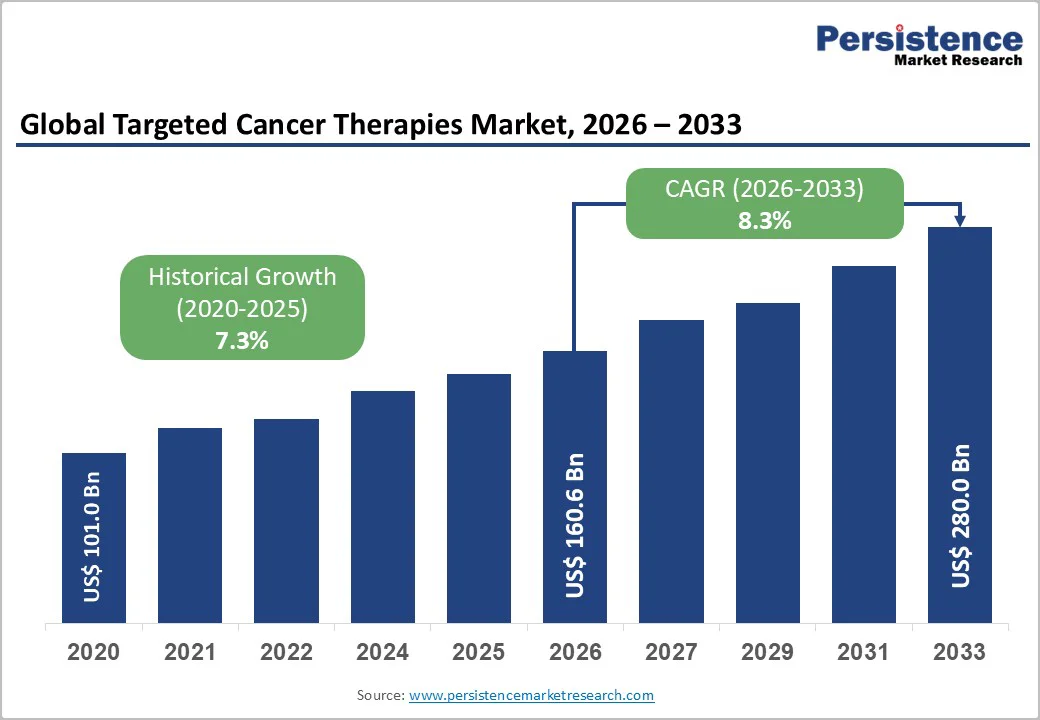

The global targeted cancer therapies market size is likely to be valued at US$ 160.6 billion in 2026 and is estimated to reach US$ 280.0 billion by 2033, growing at a CAGR of 8.3% during the forecast period 2026−2033. Growing global cancer burden, as well as broader adoption of biomarker-driven treatment approaches that allow for more precise and personalized care, is a prime factor fueling market growth. This shift is reinforced by consistent regulatory approval of new targeted medications for both solid tumors and blood cancers, helping integrate these therapies into standard clinical practice. Targeted therapies now play a central role in oncology, gradually replacing conventional chemotherapy as the preferred first-line treatment in many cases. The transition is driven by their ability to focus on specific cancer cell mechanisms, often resulting in better outcomes and fewer adverse effects.

Key Industry Highlights

- Dominant Region: North America is expected to command about a 40% market share in 2026, supported by financial strength and a culture of rapid innovation.

- Fastest-growing Market: Asia Pacific is slated to emerge as the fastest-growing regional market through 2033, due to ageing populations and rapidly improving health systems.

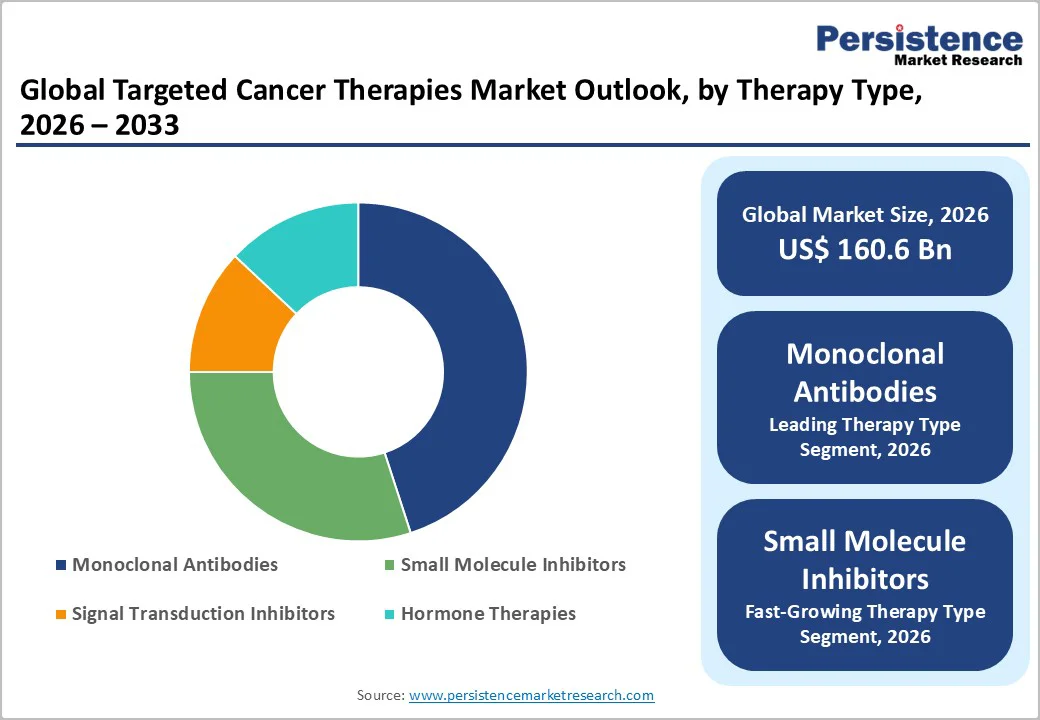

- Leading & Fastest-growing Therapy Type: Monoclonal antibodies is set to command around 45% of the revenue share in 2026, whereas small molecule inhibitors are likely to grow the fastest from 2026 to 2033.

- Leading & Fastest-growing Disease Indication: Lung cancer is slated to dominate with an estimated 29% market revenue share in 2026, while breast cancer is expected to be the fastest-growing segment between 2026 and 2033.

- Market Driver: Increasing number of cancer cases globally, accentuated by aging populations and sedentary lifestyles, is heightening the need for advanced tumor screening solutions.

- Market Opportunities: Growing incidence of cancer in developing economies can produce enormous opportunities on account of the presence of massively underserved patient populations.

| Key Insights | Details |

|---|---|

| Targeted Cancer Therapies Market Size (2026E) | US$ 160.6 Bn |

| Market Value Forecast (2033F) | US$ 280.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3% |

| Historical Market Growth (CAGR 2020 to 2024) | 7.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Cancer Incidence and Aging Population

Global cancer cases are rising as populations grow older, lifestyles become more sedentary, and more people are identified through improved screening programs. According to the International Agency for Research on Cancer (IARC), the global cancer burden is increasing rapidly, with an estimated 20 million new cases and 9.7 million deaths in 2022 and a projected rise of about three?quarters to more than 35 million new cases by 2050. This means more patients are being diagnosed at stages where advanced treatments are needed, which naturally increases demand for targeted oncology drugs that can be matched to specific tumor characteristics.

Lung, breast, and colorectal cancers are among the most frequently diagnosed worldwide, and each has well?established targeted treatment options, so growth in these cancers directly reinforces uptake of targeted therapies. Projections from international cancer registries indicate that the number of new cancer cases will continue to climb over the coming decades, making these high-incidence tumors a central focus of precision?medicine strategies.

High Therapy Costs and Access Inequities

High therapy costs and unequal access to treatment remain a fundamental structural restraint in the cancer therapies market growth path, particularly for advanced targeted agents, immunotherapies and multi-drug combination regimens. Targeted cancer therapy costs in the USA can range from about US$ 10,000 to over US$ 30,000 per month, and for some newly launched agents, the average monthly price is now well above US$ 25,000, putting sustained treatment far beyond the reach of many patients without robust coverage.

Even where national or private insurance is available, patient co?payments, benefit caps, and non-covered services can generate substantial out-of-pocket expenses, driving delayed treatment initiation, dose reductions, therapy interruptions and significant financial burdens for patients. The impact is especially pronounced in low? and middle?income countries, where per?capita health spending is far lower and public oncology budgets are constrained. In these markets, the annual cost of a single targeted therapy or immunotherapy course can exceed several multiples of average income, making widespread reimbursement infeasible and leaving many patients reliant on out?of?pocket payment, charity programs or international aid.

Expanding Cancer Care to Unlock Demand for Advanced Oncology Therapies in Emerging Markets

Rapid growth in oncology services across emerging economies is reshaping where patients receive care and how they access sophisticated treatments. Health systems in Asia Pacific APAC, Latin America, and the Middle East & Africa are investing in dedicated cancer centers, radiation therapy units, and multidisciplinary clinics, which strengthens local diagnostic and treatment capabilities. These investments shorten care pathways, reduce the need for outbound medical travel, and enable earlier intervention for tumor types that are prevalent in these regions, such as lung, breast, and gastrointestinal cancers. For industry stakeholders, this shift creates a window to partner with providers on clinical protocols, training, and technology transfer that align new infrastructure with international standards of oncology practice.

At the same time, improvements in healthcare financing are translating capacity into real, addressable demand. Governments and private insurers are broadening coverage for oncology services and reimbursable drugs, including higher-cost modalities such as targeted therapies and immuno-oncology agents. Rising incomes and rapid urbanization in countries such as China, India, and members of the ASEAN have increased patients’ ability and willingness to seek timely care in formal health systems. This combination of upgraded facilities and more supportive funding models expands the effective market for modern cancer therapies and diagnostics.

Category-wise Analysis

Therapy Type Insights

Monoclonal antibodies is anticipated to be the leading segment holding approximately 45% of the cancer therapies market revenue share in 2026. Monoclonal antibodies are specifically designed to recognize and attach to distinct markers on cancer cells. This targeted action allows oncologists to treat a wide range of solid tumors and blood cancers while limiting damage to healthy tissue, which makes these drugs a routine choice in many modern treatment protocols. Their role spans major cancers such as breast, lung and colorectal disease, as well as conditions such as multiple myeloma and lymphomas, and they are, therefore, used repeatedly across lines of therapy and over long treatment courses, creating stable and recurring demand.

Small molecule inhibitors are likely to be the fastest-growing segment from 2026 to 2033. Small molecule inhibitors work inside the cancer cell, blocking specific signaling pathways that drive tumor growth and survival. By acting on defined molecular targets, they can slow or stop cancer cell proliferation while often causing fewer systemic side effects than traditional chemotherapy, which makes them attractive options for both patients and clinicians.

Disease Indication Insights

Lung cancer is slated to dominate with an estimated 29% of market revenue share in 2026. This disease combines a high number of patients with a lesser chance of survival, which pushes clinicians to use intensive and often multi?line treatment strategies. A large number of people are still diagnosed at a stage where the disease has spread or is difficult to remove surgically, so oncologists rely heavily on systemic therapies to control the cancer and extend survival. This clinical reality keeps lung cancer at the center of treatment guidelines and drug?development efforts across the industry.

Breast cancer is expected to fastest-growing segment between 2026 and 2033, because a growing number of patients are being detected earlier and living longer, which naturally lengthens the period over which treatment is required. As screening programs expand and follow?up care improves, more women move through multiple phases of therapy, including surgery, radiation, systemic drugs and ongoing maintenance, so the overall demand for breast cancer medicines continues to rise.

End-User Insights

Hospitals are poised to secure an approximate 55% market share in 2026, as these facilities are best equipped to handle the most complex parts of treatment. They initiate most systemic regimens, manage high?risk infusions and deliver combination protocols that require close monitoring, emergency support and rapid access to diagnostic services. These hospital-based oncology centers are also where many advanced therapies are introduced first, including monoclonal antibodies, signal transduction inhibitors and intensive supportive?care regimes that must follow strict safety procedures.

Cancer and radiation therapy centers is anticipated to be the fastest-growing segment during the 2026-2033 forecast period. Dedicated cancer and radiation therapy centers are emerging as one of the most dynamic end?user groups in oncology because they focus exclusively on cancer care and are designed around outpatient workflows. Health systems are deliberately shifting part of oncology activity away from large general hospitals into these specialized centers to reduce pressure on inpatient services, shorten waiting times and offer a more streamlined experience for patients.

Regional Insights

North America Targeted Cancer Therapies Market Trends

North America is likely command a significant portion of the targeted cancer therapies market share at approximately 40% in 2026, on the back of financial strength and a culture of rapid innovation. The region’s substantial healthcare budgets and broad insurance access mean that more patients can be diagnosed early and treated with the latest approaches including the newest targeted and immune-based therapies. The United States plays an especially prominent role, because of its intense concentration of leading pharmaceutical companies, academic research centers, and pioneering biotech firms, all of which continuously roll out new drugs and technologies.

Regulatory agencies such as the U.S. Food and Drug Administration (FDA) have streamlined the approval of innovative drugs through special designations and fast-track programs, allowing promising treatments to reach patients sooner. Competition is sharp, with established industry giants constantly challenged by agile biotechs, fueling a busy pipeline of partnerships, developments, and new product launches. Continued high levels of investment flow into research areas like immuno-oncology, cell and gene therapy, and precision medicine, ensuring that North America remains a leading and influential market in setting global standards and driving future breakthroughs in cancer treatment.

Europe Targeted Cancer Therapies Market Trends

Europe is the second?largest hub for cancer therapies, anchored by major markets such as Germany, the U.K., France, and Spain. The region’s strength comes from broad public healthcare coverage, well-developed cancer registries and national cancer control plans that support earlier detection and structured, guideline-based treatment pathways. Since most patients in the European Union (EU) are treated within universal or social insurance systems, access to essential oncology care is relatively broad, although the speed at which the newest drugs are adopted can differ from one country to another.

The competitive landscape combines global pharmaceutical leaders with strong regional players, creating an environment where innovation and cost effectiveness both matter. Europe is also a frontrunner in the use of biosimilars, especially for monoclonal antibodies, which helps health systems free up budget for newer treatments. In terms of regional investments, the focus of market players needs to be on developing precision oncology solutions, upgrading radiotherapy infrastructure, and engineering digital tools that improve care coordination and data sharing.

Asia Pacific Targeted Cancer Therapies Market Trends

Asia Pacific is positioned to become the fastest-growing regional market for targeted cancer therapies through 2033, owing to the large, ageing populations and rapidly improving health systems across the region. An increasing number of cancer cases are being diagnosed in China, India and ASEAN member states, while governments and private providers are investing heavily in hospitals, cancer centers and modern equipment. As this infrastructure expands, it will become easier to deliver advanced treatments, eventually leading to an increase in the demand for both established regimens and newer targeted and immune?based therapies across the region.

China and Japan have emerged as leaders, supported by strong local scientific expertise and targeted policy initiatives that improve patient access to the latest medicines. On the other hand, countries such as India and those in Southeast Asia are working quickly to scale up cancer infrastructure, opening new oncology centers and radiation therapy clinics that boost the use of advanced therapies in communities that previously relied mainly on older treatments.

Competitive Landscape

The global cancer therapies market structure is moderately consolidated. Key players such as Pfizer Inc., Merck & Co., Inc., F. Hoffmann?La Roche AG, and Novartis AG are dominating the market, collectively capturing nearly 50% of the market share. Global pharma leaders dominate high?value segments such as monoclonal antibodies, small?molecule targeted agents and immunotherapies, leveraging extensive pipelines, strong brands and broad commercial footprints across major regions. These companies typically control access to the widest range of indications and combination regimens, reinforcing their influence on clinical practice and payer negotiations. This has resulted in a market structure where a relatively small number of global companies capture a substantial share of revenue, while a long tail of emerging and regional players contributes to innovation, specialization and geographic reach.

Key Industry Developments

- In July 2025, Akari Therapeutics advanced research on its novel PH1 payload, a spliceosome modulator used in antibody-drug conjugates (ADCs) that induces cancer cell death and stimulates immune response by altering RNA splicing in targeted cancer cells.

- In May 2025, Avammune Therapeutics, a biopharma startup based in Philadelphia and Bengaluru, has raised US$ 12 million in Series A funding to advance its small-molecule immunotherapies that activate the innate immune system for cancer and autoimmune diseases.

- In January 2025, Mayo Clinic researchers have developed a strategy that combines antibody-drug conjugates with proteolysis-targeting chimeras to enhance the delivery of cancer drugs into tumor cells. This method improved therapy absorption by up to 1.9 times in breast cancer models and shows promise for treating aggressive cancers with targets such as HER2, EGFR, and MET.

Frequently Asked Questions

The global targeted cancer therapies market is projected to reach US$ 137.2 billion in 2026.

Surging cancer incidence worldwide, growing demand for precision medicine, and continuous advances in genomics, biomarkers, and drug‑development technologies are driving the market.

The market is poised to witness a CAGR of 8.3% from 2026 to 2033.

Expanding therapeutic combinations, enhancing cancer care capacity in emerging economies, widening companion‑diagnostic use, and next‑generation targeted and biosimilar launches are the key market opportunities.

Pfizer Inc., Merck & Co., Inc., F. Hoffmann‑La Roche AG, and Novartis AG are some of the key players in the market.