- Clothing, Footwear, & Accessories

- Swimwear and Beachwear Market

Swimwear and Beachwear Market Size, Share, and Growth Forecast 2026 - 2033

Swimwear and Beachwear Market by Product Type (Swimwear, and Beachwear), by End User (Men, Women, Kids, Boys, Girls, Toddlers), by Material (Nylon, Polyester, Spandex, Neoprene, Cotton, Others), by Sales Channel (Hypermarkets/Supermarkets, Departmental Stores, Specialty Stores, Independent Small Stores, Online Retailers), and Regional Analysis, 2026 - 2033

Swimwear and Beachwear Market Size and Trend Analysis

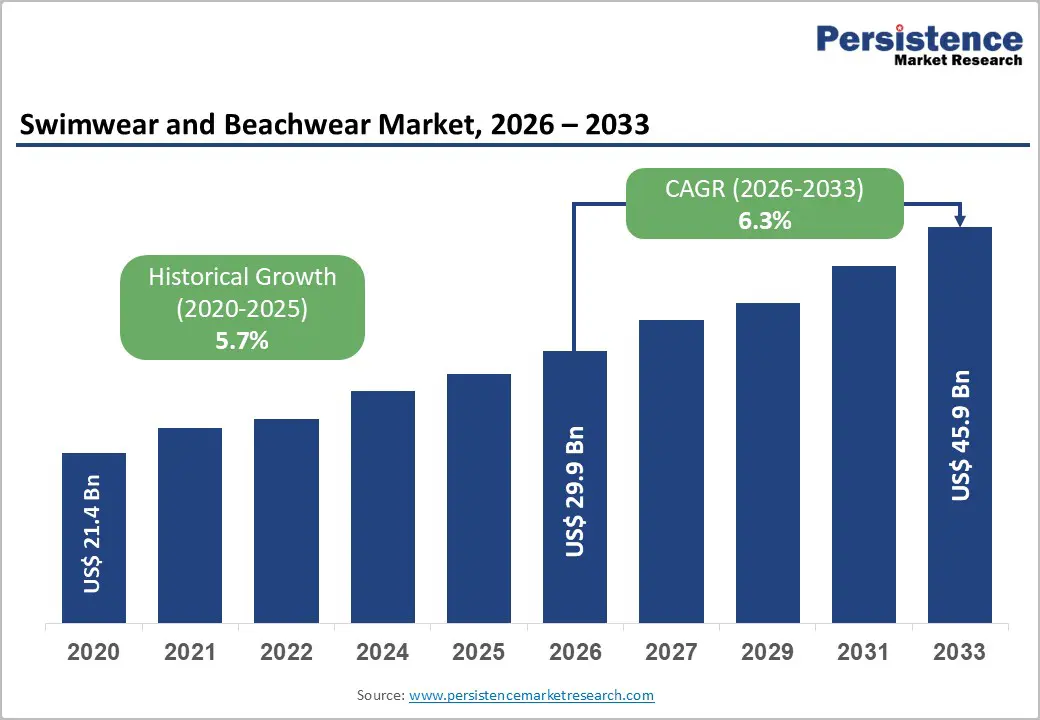

The global swimwear and beachwear market size is likely to be valued at US$ 29.9 billion in 2026 and is expected to reach US$ 45.9 billion by 2033, growing at a CAGR of 6.3% during the forecast period from 2026 to 2033. This steady expansion is driven by rising tourism, beach-oriented leisure activities, and fashion-driven consumer spending, particularly in urban and coastal markets.

Key Market Highlights

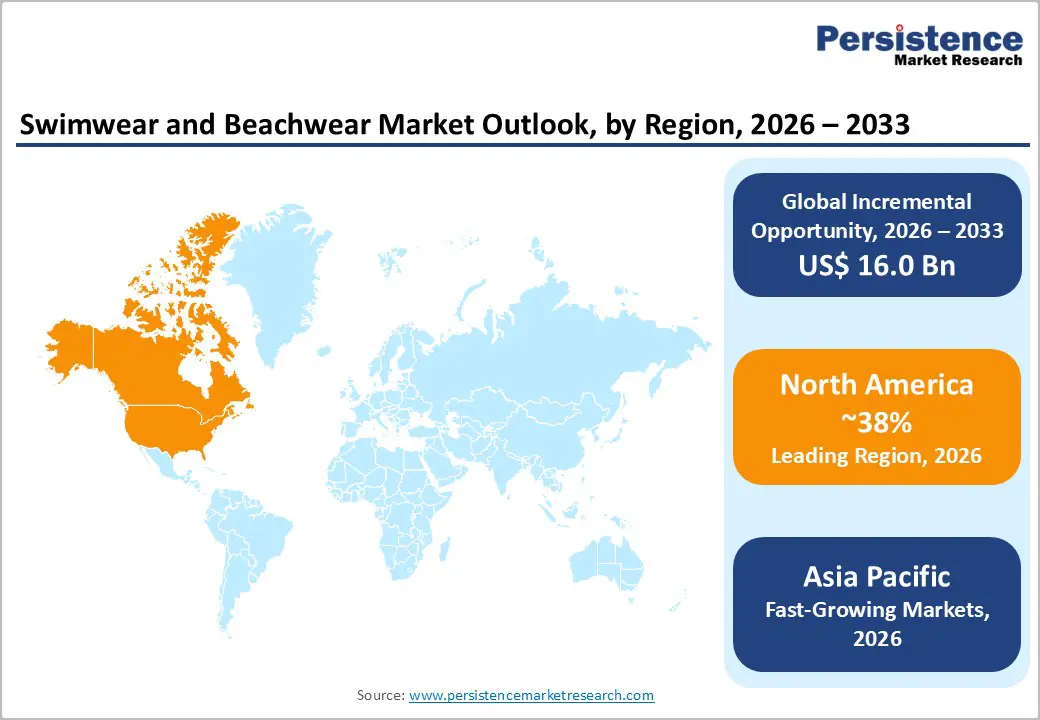

- Leading region: North America leads the swimwear and beachwear market, holding 38% share, due to strong consumer spending, high beach-tourism volumes, and well-developed retail infrastructure in the United States.

- Fastest-growing region: Asia Pacific is the fastest-growing region with rising CAGR of 7.8%, driven by rising disposable incomes, urbanization, and domestic tourism in China, Japan, India, and ASEAN countries.

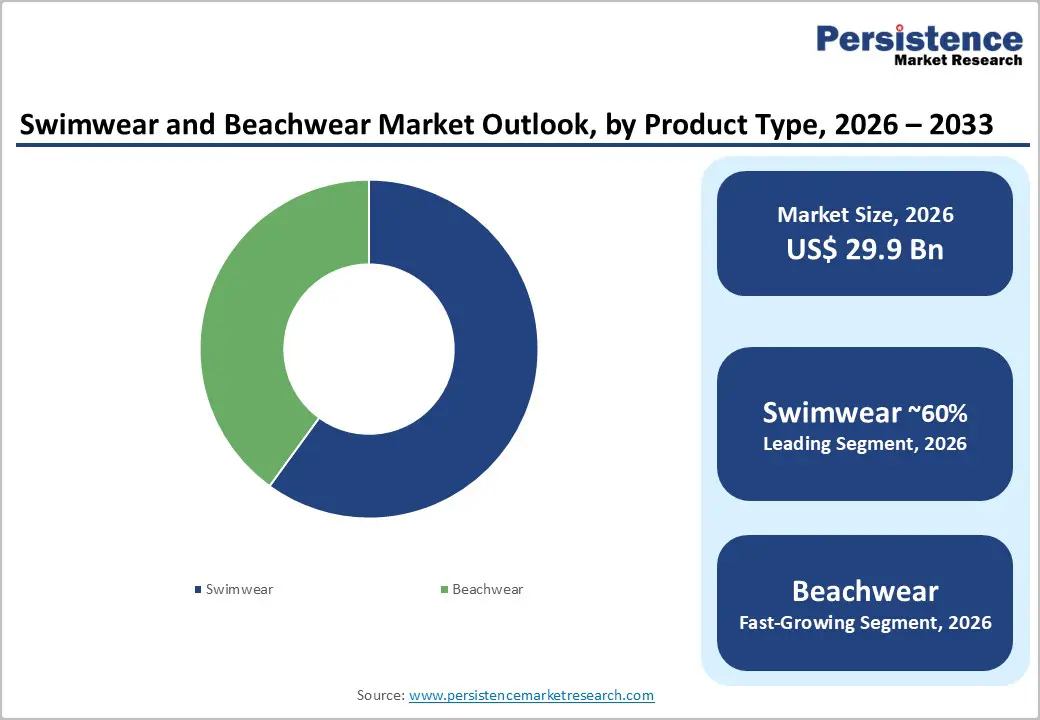

- Dominant segment: Swimwear is the dominant product type segment, capturing 60% of demand due to high fashion sensitivity and strong brand loyalty among female consumers.

- Fastest-growing segment: Online retail is one of the fastest-growing sales channels, expanding at a higher CAGR than brick-and-mortar channels as e-commerce, social commerce, and mobile-first shopping grow.

- Key market opportunity: The expansion of performance and functional swimwear, including rash guards, UV-protective suits, and competition swimwear, represents a high-value growth opportunity, particularly in North America and Europe.

| Key Insights | Details |

|---|---|

|

Swimwear and Beachwear Market Size (2026E) |

US$ 29.9 Billion |

|

Market Value Forecast (2033F) |

US$ 45.9 Billion |

|

Projected Growth CAGR (2026–2033) |

6.3% |

|

Historical Market Growth (2020–2025) |

5.7% CAGR |

Market Dynamics

Drivers - Global Tourism Recovery and Expanding Beach Leisure Culture is Driving Consistent Demand for Swimwear and Resort Fashion Worldwide

One of the main growth drivers of the swimwear and beachwear market is the steady rise in international tourism, domestic travel, and beach-focused leisure activities, which directly increase product demand. According to the World Tourism Organization (UNWTO), global tourist arrivals recovered to over 90% of pre-pandemic levels by 2025, with strong traffic toward coastal destinations such as Mediterranean Europe, Southeast Asia, and the Caribbean.

As travel and resort vacations become more frequent, consumers are purchasing multiple swimwear and beachwear items for different occasions, boosting overall sales volumes. Additionally, the growing popularity of staycations, cruises, water parks, and hotel pools is expanding swimwear usage beyond traditional holidays. This shift supports year-round demand in urban markets. Together, rising tourism activity and lifestyle-driven recreation are creating a consistent and expanding customer base for swimwear and beachwear globally.

Social Media Influence and Fast-fashion Cycles are Accelerating Trend-Driven Swimwear Purchases and Shortening Product Replacement Timelines

Fashion influence and social media engagement have become powerful drivers of consumer demand in the swimwear and beachwear market. Platforms such as Instagram, TikTok, and Pinterest promote beach looks, poolside styling, and influencer-led fashion trends, encouraging frequent wardrobe updates. Consumers now view swimwear as a style statement rather than only functional clothing.

Fast-fashion brands and digital retailers continuously launch new seasonal collections featuring bold colors, trendy cuts, and creative patterns, which shortens replacement cycles and increases purchase frequency. Industry reports indicate that swimwear and beachwear rank among the fastest-growing online apparel categories during summer seasons. This trend spans women, men, and children’s segments, supported by celebrity endorsements and viral fashion content. As trend-driven shopping becomes more common, fashion and social media continue to accelerate overall market growth and product turnover.

Restraints - Strong Dependence on Summer Seasons and Climate Conditions Creates Sales Volatility and Inventory Management Challenges for Brands

The swimwear and beachwear market faces a major challenge due to its strong dependence on seasonal weather patterns. Demand typically peaks during summer months and in warm coastal regions, while colder seasons experience sharp sales declines. In temperate climates, consumer purchasing behavior is closely linked to holiday schedules, temperature changes, and vacation periods, creating short selling windows. This seasonality often results in excess inventory, heavy discounting, and margin pressure for retailers and manufacturers.

Managing production volumes and stock levels becomes complex, increasing logistics costs and financial risk. In developing regions, limited retail infrastructure and unpredictable weather conditions further restrict consistent sales performance. Brands must rely on promotions, exports to warm regions, or diversified product lines to balance off-season slowdowns. Overall, the seasonal nature of swimwear demand continues to limit stable year-round revenue generation.

Rising Environmental Awareness is Pressuring Swimwear Brands to Adopt Eco-Friendly Materials and Sustainable Production Practices

Environmental impact has become a growing concern in the swimwear and beachwear market, particularly due to the heavy reliance on synthetic materials such as polyester, nylon, and spandex. These fabrics are petroleum-based and release microplastics during washing, contributing to ocean pollution and long-term environmental damage. Growing awareness among consumers, environmental organizations, and regulatory authorities is putting pressure on brands to improve sustainability practices.

Fast-fashion production cycles further intensify textile waste and resource consumption. Many shoppers are now actively seeking eco-friendly alternatives made from recycled fibers, biodegradable materials, or low-impact manufacturing processes. Brands that fail to adapt to sustainability expectations may experience reputational damage and declining consumer trust. Regulatory scrutiny around textile waste, chemical use, and emissions is also rising globally. These factors create operational challenges and cost pressures while reshaping product development strategies across the industry.

Opportunities - Increasing Participation in Water Sports and Fitness Activities is Boosting Demand for Premium Performance Swimwear And Technical Fabrics

A strong growth opportunity is emerging in performance-driven and functional swimwear designed for sports, fitness, and water-based activities. Demand is rising for products such as rash guards, compression suits, UV-protective swimwear, and high-speed competitive designs used in swimming, surfing, triathlons, and aquatic workouts. Leading brands, including Speedo International Limited, TYR Sport, Inc., Arena S.p.A., and ASICS Company, continue to invest in advanced fabric technologies, improved aerodynamics, and long-lasting materials. These products typically command premium prices and offer higher profit margins than standard swimwear. The growing global focus on fitness, outdoor recreation, and adventure sports is expanding this customer base. As more consumers seek comfort, durability, and professional-grade features, functional swimwear is expected to become one of the fastest-growing segments within the overall market.

Rapid Digital Retail Growth and Social-Commerce Adoption are Reshaping Swimwear Distribution and Global Brand Reach

The rapid expansion of online retail and direct-to-consumer (DTC) business models presents a major revenue opportunity for swimwear and beachwear brands. Digital platforms allow companies to reach global audiences, offer wider product assortments, and launch new styles quickly based on trend data. Advanced sizing tools, virtual try-ons, and personalized recommendations are improving customer confidence and reducing return rates.

Brands such as Nike, Inc., L Brands, Inc. (Victoria’s Secret), and Bali Swim Ltd are strengthening their digital storefronts and social-commerce channels to engage younger consumers. Growth is especially strong in Asia Pacific, Latin America, and the Middle East & Africa, where mobile-first shopping is accelerating. As cross-border e-commerce and influencer-led selling expand, online channels are expected to capture a larger share of total market revenue in the coming years.

Category wise Analysis

Product Type Insights

Swimwear remains the largest product segment in the swimwear and beachwear Market, accounting for approximately 60% of total market value. This leadership is driven by strong fashion sensitivity, higher spending per customer, and frequent product replacement cycles. One-piece swimsuits continue to attract buyers seeking comfort, support, and modest styling, while bikinis dominate vacation and resort purchases influenced by social-media trends.

Female consumers often purchase multiple styles for different occasions, increasing overall sales volumes. Leading brands such as Bali Swim Ltd, Liv Brasil, Seafolly US, and Gottex Company focus heavily on premium designs, bold prints, and sustainable materials to capture this segment. Their strong branding and seasonal launches reinforce women’s swimwear as the core revenue generator. Ongoing innovation in fit, style, and fabric technology continues to strengthen this segment’s dominant market position.

End-user Insights

Women represent the largest end-user segment in the swimwear and beachwear market, contributing approximately 50% of total demand. This dominance is linked to higher shopping frequency, strong engagement with fashion trends, and greater responsiveness to new designs and collections. Female consumers actively explore different cuts, colors, and brand offerings, often influenced by social-media content, influencers, and celebrity endorsements.

Women are also the primary buyers of bikinis, one-piece suits, tankinis, and beach dresses, driving volume across multiple product categories. Major retailers such as L Brands, Inc., Nike, Inc., and Sears Holdings Corporation consistently report women’s swimwear as one of their top seasonal performers. Promotional campaigns and trend-focused marketing further strengthen this segment’s importance. As lifestyle fashion becomes more integrated into daily leisure activities, women will continue to drive the majority of market growth globally.

Material Insights

Polyester and nylon together dominate the material landscape of the swimwear and beachwear market, accounting for an estimated 60% of total consumption. These synthetic fibers are preferred due to their durability, stretchability, quick-drying performance, and resistance to chlorine and saltwater exposure. Polyester is widely used in performance swimwear, rash guards, and board shorts, while nylon remains popular in form-fitting and high-comfort designs.

Leading manufacturers such as Speedo International Limited, TYR Sport, Inc., and Arena S.p.A. rely heavily on blended fabrics with spandex to achieve superior flexibility and shape retention. Additionally, recycled polyester and eco-friendly nylon options are gaining traction as sustainability concerns rise. These innovations allow brands to maintain product performance while reducing environmental impact. As technology improves, synthetic fabrics are expected to remain the primary material choice across premium and mass-market swimwear segments.

Sales Channel Insights

Online retail has become one of the fastest-growing distribution channels in the Swimwear and Beachwear Market, currently capturing around 25% of global demand. The growth is driven by rising smartphone usage, convenient home delivery, and social-commerce platforms that enable instant purchasing. E-commerce websites offer extensive product variety, size guidance tools, customer reviews, and personalized recommendations, which enhance buyer confidence.

Major platforms such as Amazon, Zalando, and Shein report strong seasonal spikes in swimwear sales, particularly during summer months. Younger consumers increasingly prefer digital shopping due to speed and access to global fashion trends. Emerging markets in the Asia-Pacific and Latin America are seeing rapid online adoption as logistics infrastructure improves. With ongoing innovation in virtual fitting and influencer marketing, online retail is projected to outpace physical stores in growth over the next decade.

Regional Insights

North America Swimwear and Beachwear Market Trends

North America represents a high-value and brand-driven market, led primarily by the United States. Strong consumer spending, developed retail infrastructure, and high participation in beach tourism support consistent demand across the region. Department stores, specialty swimwear chains, and robust e-commerce platforms provide wide product accessibility. Leading brands such as Bali Swim Ltd, L Brands, Inc., Nike, Inc., and Speedo International Limited maintain strong market presence through innovation, celebrity collaborations, and premium positioning.

At the same time, fast-fashion players offer affordable collections to attract budget-conscious buyers. Sustainability awareness is also increasing, with retailers introducing recycled fabrics and eco-friendly packaging. Regulatory standards governing product safety and chemical use encourage responsible sourcing practices. Overall, North America remains a mature yet profitable market, particularly for women’s swimwear, performance products, and digitally driven retail models.

Europe Swimwear and Beachwear Market Trends

Europe is characterized by strong fashion influence and a growing sustainability focus within the swimwear and beachwear sector. Countries such as Germany, the United Kingdom, France, and Spain serve as major consumption hubs, supported by both domestic tourism and international travel. Mediterranean nations, including Italy, Greece, and Turkey, generate heavy seasonal demand due to their popular beach destinations.

The region also hosts several premium and designer swimwear brands that emphasize style, quality, and eco-friendly materials. European Union policies under the Green Deal and Circular Economy Action Plan are encouraging recycled fabrics, transparent labeling, and waste reduction across the textile industry. Brands such as Arena S.p.A., Rip Curl Group Pty Ltd., and Gottex Company are responding with sustainable collections and innovative production techniques. With high fashion awareness and environmentally conscious consumers, Europe remains a stable growth region with strong premium market potential.

Asia Pacific Swimwear and Beachwear Market Trends

Asia-Pacific is the fastest-growing region in the Swimwear and Beachwear Market, driven by rising incomes, expanding middle-class populations, and increasing domestic tourism. China leads demand with increased resort travel, pool culture, and fashion awareness among urban consumers. Japan supports premium and technology-driven swimwear due to high-quality expectations and active beach tourism. India is witnessing strong mass-market growth as affordability improves and lifestyle trends evolve.

Southeast Asian countries such as Thailand, Indonesia, Vietnam, and the Philippines benefit from strong tourism inflows and coastal leisure culture. The region also serves as a major manufacturing hub, supported by low labor costs and established textile clusters. Growth in e-commerce, mobile shopping, and social-media-driven fashion is accelerating sales across both domestic and international markets, positioning Asia Pacific as the primary engine of global industry expansion.

Competitive Landscape

The swimwear and beachwear market is moderately fragmented, featuring global sportswear companies, specialized swimwear brands, and fast-fashion retailers competing across various price points and product categories. Major players such as Nike, Inc., Speedo International Limited, Arena S.p.A., L Brands, Inc., Bali Swim Ltd, and Rip Curl Group Pty Ltd hold strong positions through brand recognition, advanced fabric technology, and wide distribution networks. Fast-fashion and online-native brands are rapidly gaining market share by offering trend-driven designs at competitive prices with quick turnaround cycles.

Key competitive factors include product innovation, fit accuracy, sustainability initiatives, and omnichannel retail strategies. Emerging business models such as direct-to-consumer sales, customization, rental platforms, and resale markets are reshaping customer engagement. Overall, competition is shifting toward digitally focused, environmentally responsible, and customer-centric brands that prioritize speed, innovation, and lifestyle appeal.

Key Developments:

- July 2025: Nike introduced a new swimwear line using recycled polyester fabric focused on sustainability, UV protection, and chlorine resistance, reinforcing its commitment to eco-friendly performance apparel. This launch aligns with Nike’s broader recycled materials strategy and sustainability goals.

- March 2024: Speedo expanded its traditional performance swimwear portfolio to include beachwear items like cover-ups, kaftans, and beach dresses to broaden appeal among resort and lifestyle consumers, strengthening its presence beyond competitive swim segments and tapping lifestyle demand.

- September 2023: L Brands relaunched its swimwear portfolio with inclusive sizing, sustainable materials, and digital-first marketing efforts aimed at attracting younger, eco-conscious consumers while boosting women’s swimwear and online sales traction.

Companies Covered in Swimwear and Beachwear Market

- Bali Swim Ltd

- Liv Brasil

- King Trading Company

- Seafolly US

- Speedo International Limited

- L Brands, Inc.

- Nike, Inc.

- TYR Sport, Inc.

- Rip Curl Group Pty Ltd.

- Arena S.p.A.

- Gottex Company

- ASICS Company

- Wicked Weasel Pty. Ltd.

- Sears Holdings Corporation

- Others

Frequently Asked Questions

The global Swimwear and Beachwear Market is valued at US$ 29.9 Billion in 2026 and is projected to reach US$ 45.9 Billion by 2033, growing at a CAGR of 6.3% from 2026 to 2033, with a historical CAGR of 5.7% between 2020 and 2025.

Key demand drivers include rising tourism and beach‑oriented leisure activities, fashion and social‑media influence, and growth of e‑commerce, which drive consumption of designer swimwear, performance swimwear, and stylish beachwear across men, women, and kids.

The swimwear segment is the leading product type category, capturing 60% of demand due to high fashion sensitivity, strong brand loyalty, and larger per‑capita spending among female consumers.

North America is the largest regional market for swimwear and beachwear, accounting for roughly 38% of global value, driven by strong consumer spending, high beach‑tourism volumes, and well‑developed retail infrastructure in the United States.

A key opportunity lies in the expansion of performance and functional swimwear, including rash guards, UV‑protective suits, and competition swimwear, particularly in North America and Europe, where fitness culture and water‑sports participation are growing.