- Medical Devices

- Suture Anchor Devices Market

Suture Anchor Devices Market Size, Share, and Growth Forecast 2026 - 2033

Suture Anchor Devices Market by Product Type (Absorbable, Non-absorbable), by Material Type (Metallic Suture Anchor, Bio-absorbable Suture Anchor, PEEK Suture Anchor, Bio-composite Suture Anchor, All Suture Anchor), End-user (Hospitals, Emergency Medical Services, Clinics, Ambulatory Surgical Centres), and Regional Analysis, 2026 - 2033

Suture Anchor Devices Market Size and Trend Analysis

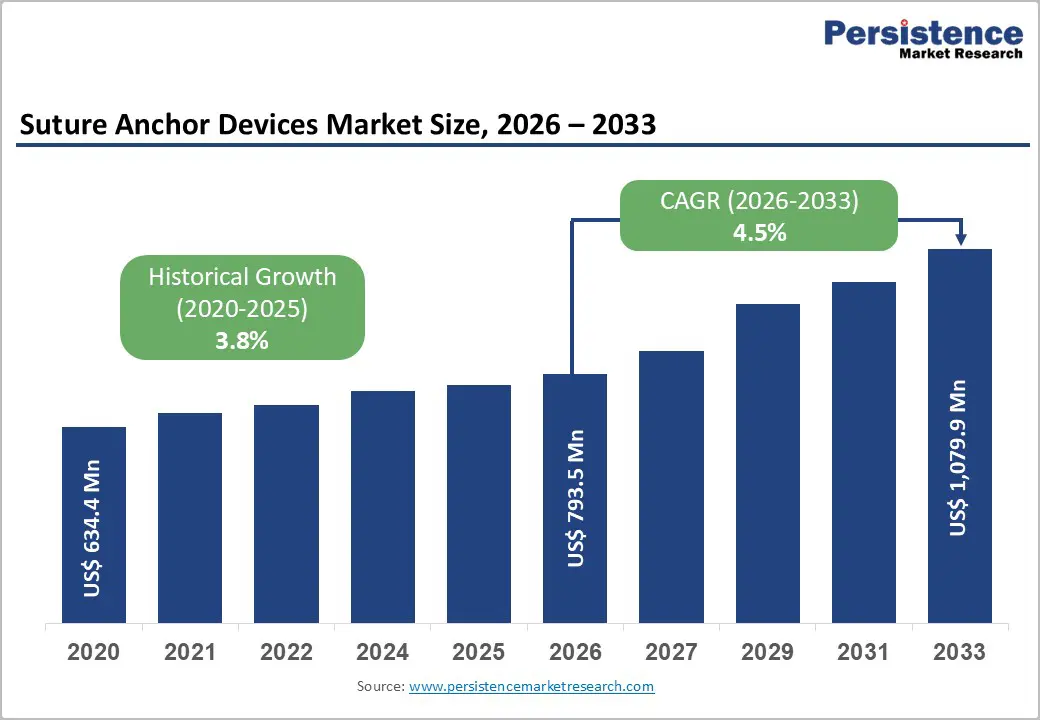

The global suture anchor devices market is expected to be valued at US$ 793.5 million in 2026 and projected to reach US$ 1,079.9 million by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

The market expansion is driven by the rise in prevalence of rotator cuff tears and musculoskeletal injuries, with aging populations demonstrating the highest incidence of orthopedic pathology requiring minimally invasive surgical intervention. The global shift toward arthroscopic surgical techniques utilizing advanced suture anchor technology has substantially increased procedural volumes, supported by technological innovations in bio-composite materials, all-suture anchor platforms, and drug-coated fixation systems that enhance healing outcomes and eliminate imaging artifacts associated with permanent metallic implants. Additionally, the expanding accessibility of ambulatory surgical center infrastructure and growing adoption of minimally invasive orthopedic procedures across developed and emerging healthcare systems continue to support robust market growth.

Key Industry Highlights:

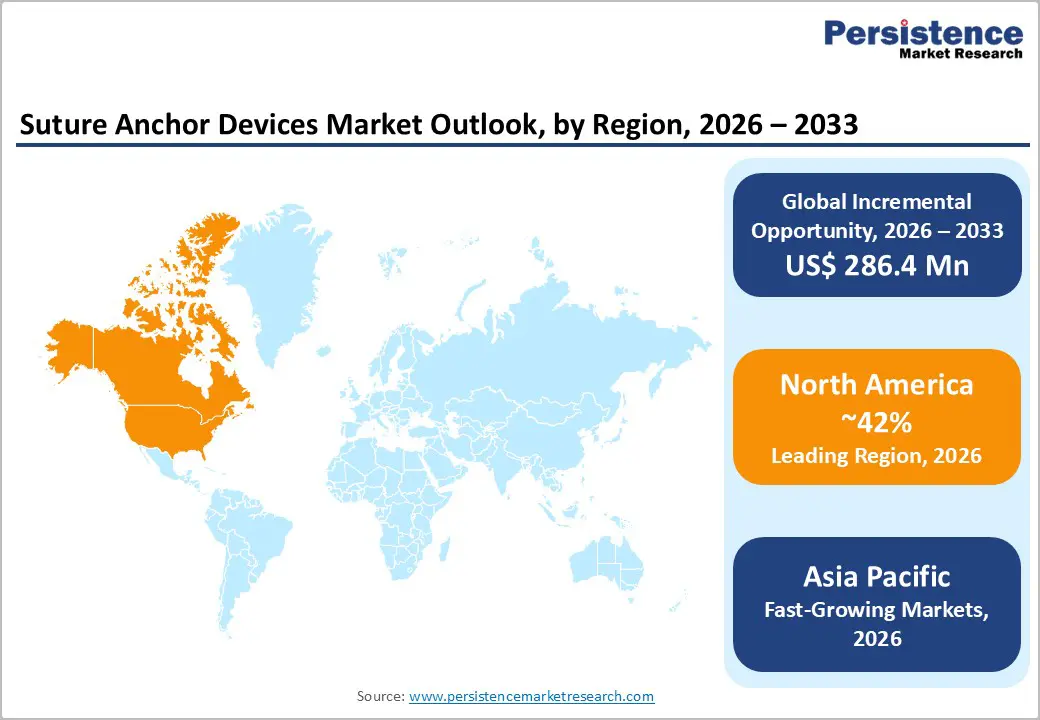

- North America maintains market dominance with 42% regional share, anchored by exceptional surgical procedure volumes exceeding tens of thousands of arthroscopic rotator cuff repairs annually, robust healthcare infrastructure, and premium device adoption patterns supporting sustained growth and innovation investment.

- Asia Pacific demonstrates the fastest regional growth trajectory through 2033, driven by China’s healthcare infrastructure modernization at 4.8% CAGR, India’s medical tourism expansion and government insurance initiatives at 5.0% CAGR, and Southeast Asia’s private hospital network development, establishing Asia Pacific as the highest-growth suture anchor market.

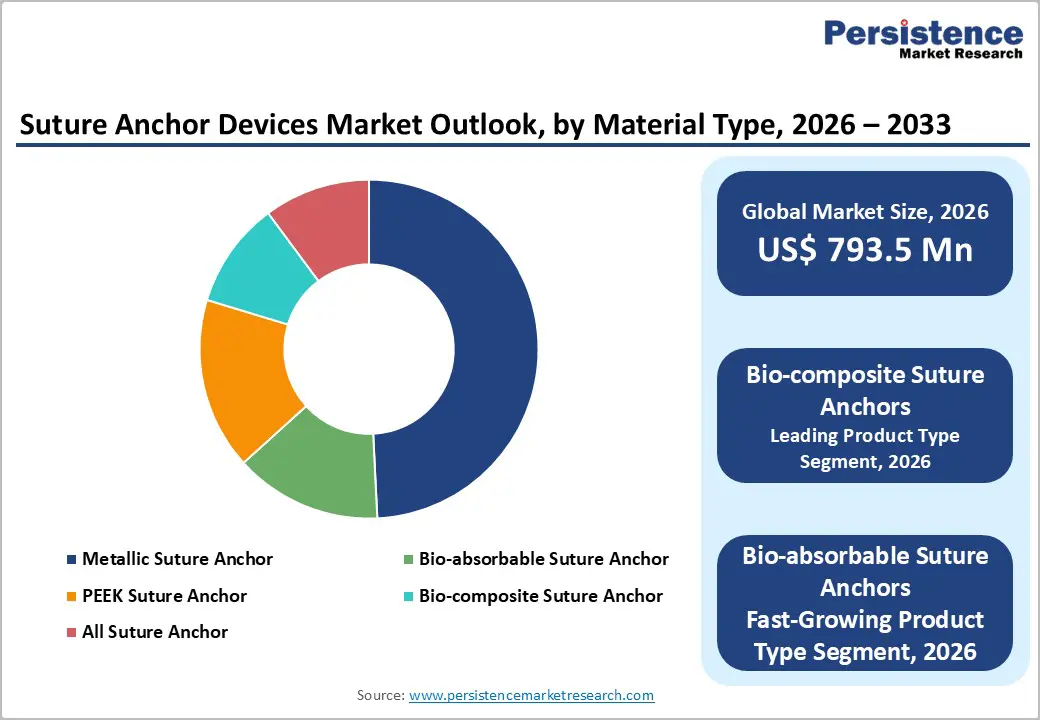

- Bio-composite Suture Anchors command 42% market dominance, combining PLGA polymers with β-tricalcium phosphate to deliver superior osteoconductivity, bone remodeling facilitation, and 90% absorption within 3 years, establishing biocomposites as the gold-standard fixation platform.

- All-Suture Anchor Platforms represent the fastest-growing segment, enabling dense medial-row fixation with minimal bone removal, demonstrating 95% healing rates, and eliminating cyst formation complications, with recent innovations including Smith+Nephew Q-FIX and OSSIO fiber systems.

- Bioabsorbable Materials command 50-79% revenue share, reflecting surgeon preference for systems eliminating permanent implant burden, facilitating revision surgery, improving postoperative imaging clarity, and reducing long-term complications compared to metallic alternatives.

| Key Insights | Details |

|---|---|

| Suture Anchor Devices Market Size (2026E) | US$ 793.5 million |

| Market Value Forecast (2033F) | US$ 1,079.9 million |

| Projected Growth CAGR (2026 - 2033) | 4.5% |

| Historical Market Growth (2020 - 2025) | 3.8% |

Market Dynamics

Drivers - Rising Incidence of Rotator Cuff Tears and Musculoskeletal Injuries in Aging Populations

The suture anchor devices market is experiencing substantial growth driven by exponential increases in rotator cuff tears and musculoskeletal injuries across global populations. The aging demographic trends across developed nations and rapidly aging emerging markets have substantially elevated rotator cuff tear incidence, with orthopedic literature demonstrating that rotator cuff pathology affects approximately 25-40% of individuals aged 60 years and older. Sports-related injuries and traumatic musculoskeletal conditions continue to rise, particularly among younger athletic populations and middle-aged individuals engaging in recreational activities. Additionally, the increasing prevalence of chronic conditions, including diabetes, hypertension, and obesity, correlates with elevated musculoskeletal disorder rates requiring surgical intervention. These demographic and epidemiological trends have created exceptional procedural demand for arthroscopic rotator cuff repair utilizing advanced suture anchor fixation systems.

Technological Advancement and Superiority of Arthroscopic Minimally Invasive Techniques

Technological innovation in suture anchor design and biomaterial science has fundamentally transformed orthopedic surgical practice, establishing arthroscopic techniques as the gold-standard approach for rotator cuff repair. Suture-bridging constructs have demonstrated biomechanical superiority compared to traditional transosseous repairs, with clinical studies demonstrating 95% healing rates in arthroscopic repair compared to substantially lower rates with open surgical techniques. The development of advanced materials including biocomposite anchors containing PLGA and β-tricalcium phosphate, all-suture anchor platforms, and drug-coated fixation systems, has enhanced procedural versatility and patient outcomes. The elimination of imaging artifacts associated with permanent metallic implants, combined with the elimination of revision surgery requirements for bioabsorbable systems, has substantially increased surgeon adoption and healthcare system procurement of advanced suture anchor platforms across hospital and ambulatory surgical center settings.

Restraints - High Device Costs and Steep Surgeon Learning Curve

The suture anchor devices market faces significant constraints from elevated device costs and substantial surgeon training requirements that limit market penetration in cost-sensitive healthcare settings. Advanced suture anchor systems incorporating biocomposite materials, drug-coated surfaces, and all-suture anchor technology command premium pricing that restricts accessibility in resource-constrained healthcare systems. The surgical application of modern suture anchors requires extensive surgeon training and procedural experience, with published literature documenting a substantial learning curve for optimal anchor positioning, secure knot construction, and appropriate fixation pattern selection. Healthcare institutions must invest substantially in surgeon education, surgical training equipment, and procedural protocol development, creating barriers to market expansion in emerging economies and rural healthcare settings.

Regulatory Complexity and Anchor Pullout Complications

The suture anchor devices market is constrained by stringent regulatory approval pathways across global markets and documented clinical complications, including anchor pullout and peri-anchor cyst formation. Anchor pullout incidence has been documented at 3.3% in cohorts utilizing screw-in bioabsorbable anchors, requiring intraoperative remediation and potentially compromising surgical outcomes. Peri-anchor cyst formation, associated with inflammatory responses to implant material, necessitates potential future revision surgery and long-term clinical surveillance. The regulatory environment requires comprehensive biocompatibility testing, biomechanical validation, and clinical evidence generation prior to market approval, extending product development timelines and increasing commercialization expenses.

Opportunities - Biocomposite Material Innovation and Drug-Coated Anchor Technology Development

Biocomposite and drug-coated suture anchor technology represents a substantial market opportunity addressing the clinical limitations of traditional fixation systems and enhancing tissue healing outcomes. Modern biocomposite anchors combining PLGA polymers with β-tricalcium phosphate demonstrate superior osteoconductivity, with 90% of systems absorbing within 3 years while facilitating bone remodeling and eliminating permanent implant burden. Recent advancements in drug-coated balloon technology with growth factor integration and PEEK anchors with bioactive coatings have demonstrated enhanced tissue integration and accelerated healing timelines. Companies developing next-generation biocomposite systems with optimized degradation kinetics and improved pull-out strength are positioned to capture substantial market share as healthcare systems prioritize materials that reduce inflammatory complications and enhance patient outcomes.

Category-wise Analysis

Product Type Insights

Bio-composite Suture Anchors represent the dominant segment in the suture anchor devices market, commanding approximately 42% market share in 2025, reflecting superior clinical outcomes and enhanced biocompatibility compared to alternative fixation modalities. Biocomposite anchors composed of PLGA polymers combined with β-tricalcium phosphate demonstrate exceptional osteoconductivity, with the β-TCP component providing a biological scaffold for bone ingrowth while the PLGA copolymer provides structural support during the critical healing period. Clinical validation demonstrates that biocomposite systems facilitate 90% absorption within 3 years while promoting new bone formation with significantly lower inflammatory responses compared to pure polymer systems. The Zimmer Biomet ComposiTCP™ anchor, incorporating 30% β-TCP and 70% PLDL demonstrates 267N pull-out strength in preclinical testing, establishing biocomposites as the gold-standard fixation platform. The elimination of permanent implant burden, combined with predictable degradation kinetics and enhanced imaging clarity postoperatively, establishes biocomposite anchors as the market-leading segment with sustained growth potential through 2033.

End-user Insights

Hospitals represent the leading segment in the suture anchor devices market due to their high surgical volumes and comprehensive orthopedic care capabilities. Most complex procedures such as rotator cuff repair, shoulder stabilization, and hip and knee ligament reconstruction are performed in hospital settings, where advanced infrastructure and skilled orthopedic surgeons are readily available. Hospitals are also better equipped with specialized operating rooms, imaging facilities, and post-operative care units, enabling safe and efficient use of suture anchor devices. Additionally, hospitals handle a higher number of trauma and sports injury cases, which significantly increases the demand for suture anchors. Favorable reimbursement policies, availability of multidisciplinary surgical teams, and access to a wide range of advanced implant options further strengthen hospital dominance. As centers of training and innovation, hospitals are often early adopters of new suture anchor technologies, reinforcing their leading position in the market.

Regional Insights

North America Suture Anchor Devices Market Trends

North America Suture Anchor Devices Market Trends reflect the region’s strong leadership in the global market, driven by advanced healthcare infrastructure, high procedural volumes in orthopedic and sports medicine, and strong adoption of innovative implant technologies. The United States, in particular, exhibits a robust demand for suture anchors due to increasing incidence of orthopedic injuries, a growing aging population prone to degenerative joint conditions, and widespread availability of minimally invasive arthroscopic procedures. Technological advancements, such as bio-absorbable and bio-composite anchors, are rapidly integrated into clinical practice, enhancing patient outcomes and expanding indications. Comprehensive insurance coverage and favorable reimbursement frameworks also support higher utilization rates. Furthermore, strong presence of key medical device manufacturers and extensive clinical research foster product development and early market entry of cutting-edge solutions. These factors collectively sustain North America’s leading position, making it the largest and most mature market for suture anchor devices globally.

Asia Pacific Suture Anchor Devices Market Trends

Asia Pacific Suture Anchor Devices Market Trends show the region emerging rapidly due to expanding healthcare access, rising incidence of sports injuries, and improved orthopedic care infrastructure. Growing awareness of minimally invasive arthroscopic procedures in countries like China, India, Japan, and South Korea is boosting demand for suture anchor devices. Investments in hospital modernization, increased healthcare spending, and a rising middle-class population with greater ability to afford advanced treatment are key growth drivers. Additionally, expanding medical tourism in the region attracts patients seeking high-quality yet cost-effective orthopedic surgeries, further increasing procedural volumes. Local manufacturing and the entry of international device makers with region-specific solutions are enhancing product availability and affordability. Government initiatives to strengthen healthcare systems, combined with training programs for orthopedic specialists, contribute to the wider adoption of suture anchors. Overall, the Asia Pacific is poised for strong growth and represents significant untapped potential in the global suture anchor devices market.

Competitive Landscape

The competitive landscape of the suture anchor devices market is marked by intense rivalry as manufacturers strive to differentiate through innovation, product quality, and expanded distribution. Key players focus on launching advanced anchors, including bio-absorbable, bio-composite, and all-suture options, to meet diverse surgical needs. Strategic initiatives such as partnerships, acquisitions, and collaborations help companies broaden their geographic reach and strengthen clinical adoption. Emphasis on research and development enhances design features like improved fixation strength and biocompatibility, addressing surgeon preferences and patient outcomes.

Key Market Developments

- In July 2025, OSSIO Inc. launched OSSIOfiber® 2.5 mm suture anchors, which were designed to improve several surgical procedures, including Brostrom repair for lateral ankle instability.

- In July 2025, Smith+Nephew released its Q-FIX KNOTLESS All-Suture Anchor for soft tissue-to-bone fixation across multiple joint spaces, including Shoulder, Hip, and Foot & Ankle.

Companies Covered in Suture Anchor Devices Market

- Smith & Nephew Plc.

- Zimmer Biomet Holdings Inc.

- ConMed Corporation

- Arthrex Inc.

- Johnson and Johnson (DePuy Synthes Inc.)

- Medtronic Plc

- Stryker Corporation

- Parcus Medical LLC

- Wright Medical Group N.V.

- Teknimed SA

- MedShape Inc.

- South America Implants S.A.

- Anstem Medical

Frequently Asked Questions

The global market is expected to reach US$ 793.5 million in 2026.

Growth is driven by rising rotator cuff tears, sports injuries, technological advancements, and increased adoption of minimally invasive procedures.

North America leads the market, while the Asia Pacific is the fastest-growing region.

Opportunities exist in biocomposite, drug-coated, and all-suture anchors, as well as expansion in emerging Asia Pacific markets.

Smith & Nephew Plc., Zimmer Biomet Holdings Inc., ConMed Corporation, and Arthrex Inc. are leading companies that hold dominant positions in the market.