- Advanced Materials

- Special Effect Pigments Market

Special Effect Pigments Market Size, Share, and Growth Forecast 2026 - 2033

Special Effect Pigments Market by Product Type (Metallic Pigment, Pearlescent Pigment, Fluorescent Pigment, Other), Application (Paints and Coatings, Plastics, Cosmetics, Printing Inks, Others), End-use Industry (Automotive, Personal Care, Packaging, Electronics, Construction, Other), and Regional Analysis for 2026 - 2033

Special Effect Pigments Market Size and Trend Analysis

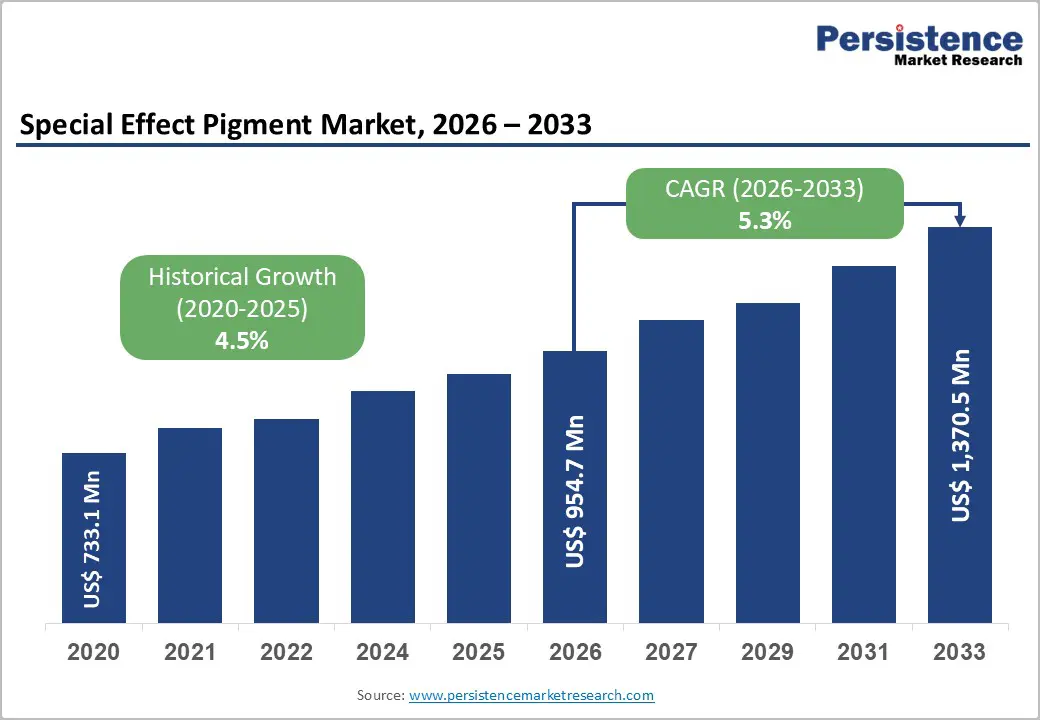

The global special effect pigments market size is estimated to be valued at US$ 0.95 billion in 2026 and is projected to reach US$ 1.37 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

The growth is propelled by accelerating demand for premium-finish automotive coatings, a flourishing global cosmetics and personal care industry, and growing adoption of sustainable packaging solutions across consumer goods verticals. Global vehicle production data reported by the International Organization of Motor Vehicle Manufacturers (OICA) confirms sustained automotive activity as a structural demand driver for high-performance effect pigments. Simultaneously, premiumization trends in beauty and personal care, supported by rising disposable incomes in the Asia Pacific, continue to expand the addressable market for pearlescent, metallic, and fluorescent pigment variants globally.

Key Highlights:

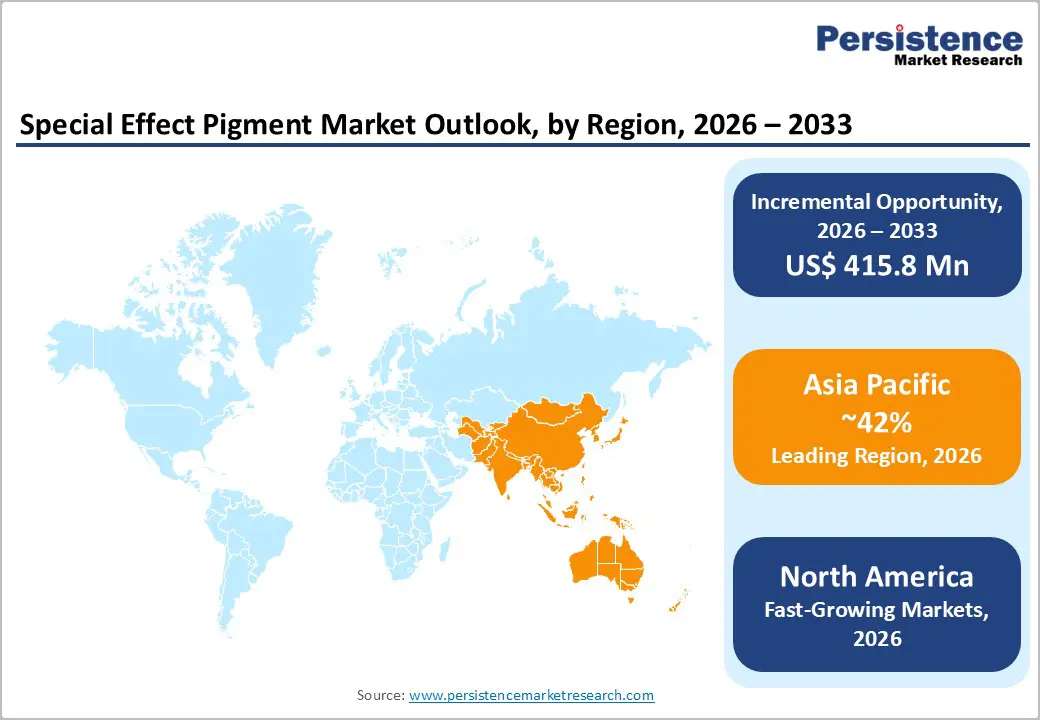

- Leading Region: Asia Pacific leads the global Special Effect Pigments market with approximately 42% revenue share, driven by large-scale automotive manufacturing in China, Japan, and India, rapid cosmetics industry expansion, and growing demand for premium packaging solutions.

- Fastest Growing Region: North America is projected to register the highest CAGR through 2033, fueled by rising demand for eco-friendly effect pigments, advanced automotive coatings, and clean-label cosmetic formulations aligned with U.S. FDA and EPA compliance standards.

- Dominant Segment: Metallic pigments represent the leading product type with approximately 53% market share, driven by widespread adoption in automotive OEM coatings, flexible packaging, and industrial applications, offering cost-effectiveness, metallic luster, and UV durability.

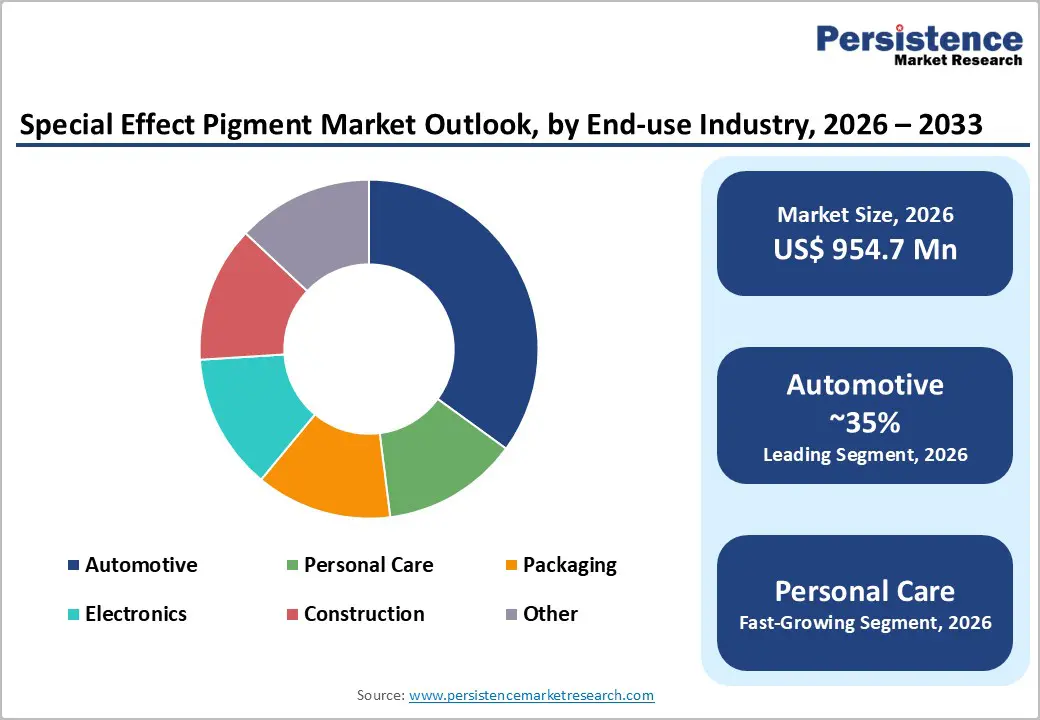

- Fastest Growing Segment: The personal care end-use segment is the fastest growing category, propelled by global beauty industry premiumization, rising demand for clean-label formulations, and social-media-driven consumer interest in high-impact shimmer, iridescent, and fluorescent effects.

- Key Opportunity: Development of sustainable, heavy-metal-free, and bio-derived special effect pigments presents the most significant near-term growth opportunity, as cosmetics, packaging, and automotive industries align procurement with global ESG compliance mandates and environmental regulations.

| Key Insights | Details |

|---|---|

| Special Effect Pigments Market Size (2026E) | US$ 954.7 Mn |

| Market Value Forecast (2033F) | US$ 1,370.5 Mn |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.5% |

DRO Analysis

Drivers - Rising Automotive Production and Demand for Premium Exterior Coating

The global automotive industry represents the largest end-use segment for special effect pigments, driven by a sustained emphasis on visual differentiation through advanced exterior coating technologies. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached approximately 93.5 million units in 2023, underscoring the sector’s scale as a high-volume and consistent consumer of effect pigments. Original equipment manufacturers and refinish providers increasingly utilize metallic, pearlescent, and chromatic-shift pigments to enhance brand identity and aesthetic appeal.

The accelerating transition toward electric vehicles further strengthens this demand, with EV manufacturers prioritizing bespoke, premium finishes as a key product differentiator. Additionally, ongoing investments in waterborne-compatible pigment formulations, driven by regulatory requirements under U.S. EPA and EU REACH frameworks, are expanding opportunities for next-generation automotive effect pigments.

Expanding Global Cosmetics Industry Sustaining Pearlescent Pigment Demand

The personal care and cosmetics industry constitutes a major and rapidly expanding demand driver for special effect pigments, particularly pearlescent and fluorescent variants that impart iridescent, shimmer, and metallic visual effects. Consumer preferences are increasingly oriented toward high-impact, visually striking finishes, influenced by the widespread dissemination of beauty content across digital and social media platforms.

Concurrently, stringent regulatory frameworks, including the EU Cosmetics Regulation (EC) No.?1223/2009 and U.S. Food and Drug Administration guidelines, are compelling manufacturers to develop heavy-metal-free, bio-derived, and sustainably sourced pigment chemistries. Leading suppliers such as Merck KGaA and Clariant AG have consequently expanded their cosmetic-grade, eco-compliant effect pigment portfolios to address this high-value, regulation-intensive segment.

Restraints - Volatility in Raw Material Prices and Ethical Sourcing Challenges

The production economics of special effect pigments are significantly exposed to raw material price volatility, particularly for mica, aluminum, and titanium dioxide, core substrates for pearlescent and metallic pigment variants. India and Madagascar collectively supply over 60% of global sheet mica, and ongoing regulatory crackdowns on informal mining operations introduce recurring supply disruptions. Aluminum prices, intrinsically linked to global energy costs and trade tariff dynamics, directly impact metallic pigment manufacturing costs.

These input cost pressures erode manufacturer margins and can translate into price increases that dampen demand in cost-sensitive industrial applications, particularly in emerging markets where price competitiveness is a primary procurement criterion for buyers across packaging and printing ink segments.

Stringent Environmental Regulations Requiring Costly Reformulation Investments

Environmental compliance represents a structurally increasing cost burden for special effect pigment manufacturers across global markets. The European Union's REACH Regulation (EC No. 1907/2006) restricts heavy metals including lead, cadmium, and hexavalent chromium historically used in certain pigment formulations, mandating costly product reformulation programs. The U.S. Environmental Protection Agency (EPA) enforces VOC emission standards for coating systems, driving transitions to waterborne formulations that demand specially engineered pigment compatibilities.

Smaller and medium-sized manufacturers, particularly those in developing economies, face disproportionate compliance costs relative to their resource base, limiting their ability to compete effectively in North American and European premium markets and constraining overall industry innovation diversity.

Opportunities - Electric Vehicle Expansion Creating a New Frontier for Functional Effect Pigments

The global surge in electric vehicle (EV) adoption is creating a new demand for advanced special-effect pigments that offer aesthetic appeal and compatibility with next-generation vehicle systems. In 2023, the International Energy Agency (IEA) reported 17 million EV sales, accounting for around 20% of total vehicle sales, with continued growth expected due to government incentives in the EU, China, and the U.S. EV manufacturers are using distinctive exterior finishes as key brand differentiators.

Furthermore, the rise of LiDAR-compatible and infrared-reflective pigments, essential for advanced driver-assistance systems (ADAS), marks a premium application niche. The American Coatings Association (ACA) emphasizes the significance of integrating functional pigments in automotive surfaces, with suppliers collaborating with OEMs to secure preferred-supplier status in the expanding EV coatings market.

Sustainable and Bio-based Pigment Innovation Responding to Global ESG Mandates

Escalating regulatory scrutiny and strengthening corporate sustainability commitments across the cosmetics, packaging, and automotive sectors are generating significant growth opportunities for manufacturers of eco-certified, bio-derived, and heavy metal free special effect pigments. Policy initiatives such as the European Green Deal and related sustainable product design legislation are accelerating industry-wide reformulation toward circular and bio-based chemistries within the European Union’s extensive industrial base.

Separately, ethical sourcing initiatives led by organizations such as the Responsible Mica Initiative are increasingly integrated into multinational companies’ supply chain due diligence requirements. Recent innovations underscore this trend, including the introduction of biodegradable, plant based effect pigments by CQV Co., Ltd. and the launch of responsibly sourced pearlescent pigments by Merck KGaA.

Category-wise Analysis

Product Type Insights

Metallic pigments represent the leading product type within the Special Effect Pigments market, accounting for approximately 53% of total global revenue. This dominance is underpinned by their broad application versatility, established manufacturing scalability, and superior performance characteristics. Aluminum-based metallic pigments are the most extensively utilized, particularly in automotive OEM exterior coatings, industrial surface treatments, and flexible packaging applications, where they provide pronounced metallic brilliance, high opacity, and durable ultraviolet resistance.

Zinc-, bronze-, and copper-based variants further expand the portfolio, supporting demand in specialty printing inks and decorative architectural coatings. According to the American Coatings Association, paints and coatings constitute the largest downstream market for pigments globally, reinforcing sustained consumption of metallic pigments.

Application Insights

Paints and coatings constitute the largest application segment for special effect pigments, accounting for approximately 38% of total market revenue. This leadership is driven by extensive usage across automotive OEM and refinish coatings, architectural decorative finishes, and industrial protective applications, all of which represent high-volume demand segments requiring both visual appeal and functional durability. The effect pigments used in these applications deliver essential performance attributes beyond aesthetics, including ultraviolet stability, thermal resistance, and corrosion protection, which are particularly critical for automotive exteriors and infrastructure coatings.

The global paints and coatings market continues to expand, supported by urbanization-driven construction activity in the Asia Pacific region and sustained infrastructure investments across North America and Europe. In parallel, the industry-wide transition from solvent-borne to waterborne coating systems, driven by VOC emission regulations enforced by the U.S. Environmental Protection Agency and the European Chemicals Agency, is increasing demand for advanced waterborne-compatible effect pigment formulations developed by specialized suppliers.

Industry Insights

The automotive industry is the largest segment for special effect pigments, accounting for about 35% of global demand. OEMs use layered paint systems with metallic, pearlescent, and color-shift pigments to enhance vehicle finishes and brand identity. In 2023, global motor vehicle production reached approximately 93.5 million units, reflecting a steady need for specialized pigments. The trend towards premium vehicles, especially electric models, is increasing pigment specifications per vehicle.

The automotive refinish sector in mature markets like North America, Germany, and Japan also drives ongoing demand for effect pigments. Leading suppliers such as Merck KGaA and BASF SE are investing in automotive-grade, waterborne-compatible pigment portfolios, underscoring the importance of this market segment.

Regional Insights

North America Special Effect Pigments Trends

North America is a strategically significant, innovation?driven market for special effect pigments, underpinned by its strong automotive manufacturing base, mature cosmetics industry, and stringent regulatory environment. The United States hosts several leading automotive coatings manufacturers, including PPG Industries and Sherwin?Williams, which are major consumers of advanced metallic and pearlescent pigments. Early adoption of low?VOC and waterborne coating systems, in compliance with U.S. Environmental Protection Agency regulations, continues to sustain demand across automotive, architectural, and industrial applications.

Although geopolitical developments, including trade sanction dynamics related to U.S.-Iran tensions, have intermittently disrupted titanium dioxide and specialty mineral supply chains, the region’s robust innovation ecosystem, comprehensive regulatory frameworks, and rising demand for sustainable, clean?label cosmetic pigments support a resilient growth outlook through the 2026-2033 forecast period.

Europe Special Effect Pigments Trends

Europe holds a prominent position in the global special-effect pigments market, supported by its advanced automotive manufacturing base, a highly developed chemicals industry, and a stringent regulatory framework. Germany serves as the core of regional market activity, hosting leading pigment producers such as ALTANA AG and Merck KGaA, alongside premium automotive OEMs, including BMW, Volkswagen Group, and Mercedes?Benz, that specify advanced effect pigments for high?end exterior finishes. France and the United Kingdom contribute substantial cosmetics?driven demand, while Spain represents a growing market for architectural decorative coatings.

Ongoing geopolitical tensions affecting Middle Eastern trade routes have challenged raw material supply chains, prompting European manufacturers to pursue backward integration and regional sourcing strategies. Simultaneously, the European Green Deal and EU Circular Economy Action Plan are accelerating the transition toward bio?based and recyclable pigment substrates, reinforcing Europe’s leadership in sustainable effect pigment innovation.

Asia Pacific Special Effect Pigments Trends

Asia Pacific represents the largest regional market for special effect pigments, accounting for approximately 42% of global revenue, supported by its extensive automotive manufacturing base, rapidly expanding cosmetics and personal care industries, and cost?competitive production capabilities. China leads regional demand, underpinned by its vast industrial infrastructure and government?supported initiatives promoting advanced materials manufacturing.

Japan and South Korea contribute significant premium demand from automotive and electronics applications, while India is emerging as a key manufacturing hub, evidenced by recent capacity expansions by domestic producers. Geopolitical tensions affecting Middle Eastern trade routes have encouraged regional manufacturers to diversify raw material sourcing and strengthen intra?regional supply chains. The ASEAN sub?region, particularly Vietnam, Thailand, and Indonesia, is the fastest?growing market, driven by rising disposable incomes, accelerating urbanization, and expanding cosmetics and flexible packaging sectors.

Competitive Landscape

The global Special Effect Pigments market exhibits a moderately consolidated competitive structure, with Merck KGaA, ALTANA AG (ECKART division), and BASF SE collectively accounting for an estimated 40% of total global market revenue. These dominant players differentiate through proprietary effect pigment technologies, broad product portfolios, and deep application expertise across automotive, cosmetics, and industrial end markets. Key growth strategies employed by market leaders include geographic expansion into Asia Pacific manufacturing hubs, co-development partnerships with automotive OEMs, backward integration to secure mica and aluminum supply chains, and sustained R&D investment in eco-friendly, waterborne-compatible formulations. Regional producers from China and India are intensifying price competition, compelling established multinationals to further differentiate through performance, sustainability credentials, and value-added technical service quality.

Key Developments:

- July 2025: ALTANA AG, through its ECKART division, received the ALTANA Innovation Award for developing a new formulation of UV-curing printing inks incorporating advanced effect pigments. The innovation utilizes PVD-based METALURE® pigments and alcohol-based silver dollar pigments to deliver high-gloss, chrome-like finishes with improved printability and adhesion.

- March 2025: DIC Corporation, through its subsidiary Sun Chemical, announced its participation in the in-cosmetics Global 2025 exhibition, where it introduced new high-performance pigments targeted at the cosmetics and beauty segment.

- January 2024: ALTANA agreed to acquire Silberline, a key producer of aluminum-based effect pigments used in coatings, inks, plastics, and consumer goods. This move expands ALTANA’s ECKART GmbH division by adding advanced research and production capabilities, particularly in North America and Asia.

Top Companies in the Special Effect Pigments Market

- Merck KGaA (Darmstadt, Germany) is a global pioneer in effect pigment technology, operating through its Performance Materials division. The company's Iriodin®, Colorstream®, and Xirona® product families span automotive, cosmetics, and industrial coating applications globally. Sustained R&D investment in sustainably sourced, mica-based pigments and next-generation color-shifting technologies reinforces Merck's market leadership, premium pricing position, and preferred supplier status among multinational automotive and cosmetic brand customers.

- ALTANA AG / ECKART (Wesel, Germany) operates one of the world's leading metallic and pearlescent pigment businesses through its ECKART division. The product portfolio encompasses aluminum, zinc, and copper-based metallic pigments alongside mica-based pearlescent variants, serving automotive, printing, plastics, and cosmetics end markets globally. Expansion into 3D printing-grade pigments and sustainable formulations demonstrates ECKART's commitment to addressing emerging application requirements and evolving environmental compliance standards.

- BASF SE (Ludwigshafen, Germany) delivers one of the industry's most comprehensive effect pigment portfolios through its BASF Colors & Effects division, including the Laripure® and Sicopearl® product ranges. The company's global manufacturing footprint, deep chemical formulation expertise, and focus on eco-compliant, waterborne-compatible pigment systems position it as a preferred supplier to automotive OEMs, coatings manufacturers, and cosmetic brands across North America, Europe, and the Asia Pacific.

Companies Covered in Special Effect Pigments Market

- ALTANA AG

- DIC Corporation

- Merck KGaA

- NIHON KOKEN KOGYO CO., LTD

- BASF SE

- Sudarshan Chemical Industries Ltd.

- Schlenk Metallic Pigments GmbH

- CQV Co., Ltd.

- The Shepherd Color Company

- VIAVI Solutions Inc.

Frequently Asked Questions

The global Special Effect Pigments market is estimated to be valued at US$ 954.7 Mn in 2026 and is projected to reach US$ 1,370.5 Mn by 2033, expanding at a CAGR of 5.3% during the 2026-2033 forecast period, supported by accelerating demand from the automotive, cosmetics, and sustainable packaging industries.

The key demand drivers include rising global automotive production, with the OICA recording approximately 93.5 million vehicle units produced in 2023, growing premiumization of personal care and cosmetics products globally, the accelerating adoption of EVs with bespoke designer exterior finishes, and expanding sustainable packaging requirements across consumer goods industries worldwide.

Metallic pigments hold the leading product type share, accounting for approximately 53% of the total global market share. Their dominance is attributed to extensive adoption in automotive OEM coatings, industrial finishes, and flexible packaging, offering superior metallic luster, UV resistance, and broad compatibility with evolving waterborne coating formulation requirements under EPA and REACH regulations.

Asia Pacific is the dominant regional market, accounting for approximately 42% of total global revenue. China, Japan, South Korea, and India are the primary contributors, driven by large-scale automotive manufacturing, rapidly expanding cosmetics exports, growing electronics industry activity, and rising middle-class consumer spending on premium packaged goods.

The most significant near-term opportunities lie in developing sustainable, bio-based, and heavy-metal-free effect pigments to address stringent ESG and regulatory requirements across cosmetics, packaging, and automotive procurement chains. Additionally, the emergence of EV-specific functional pigments, including LiDAR-compatible and infrared-reflective coatings for ADAS-equipped vehicles, presents a high-value, technology-intensive growth niche for innovation-led manufacturers.

The leading players in the global Special Effect Pigments market include Merck KGaA, ALTANA AG (ECKART division), BASF SE (BASF Colors & Effects), DIC Corporation, Sudarshan Chemical Industries Ltd., Schlenk Metallic Pigments GmbH, CQV Co., Ltd., NIHON KOKEN KOGYO CO., LTD, The Shepherd Color Company, and VIAVI Solutions Inc.