- Medical Devices

- Silent Scan Technology Market

Silent Scan Technology Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Silent Scan Technology Market by Product Type (1.5T MRI Scanners, 3T MRI Scanners), End User (Hospitals, Diagnostic Imaging Centers, Ambulatory Surgical Centers), and Regional Analysis from 2026 - 2033

Silent Scan Technology Market Share and Trends Analysis

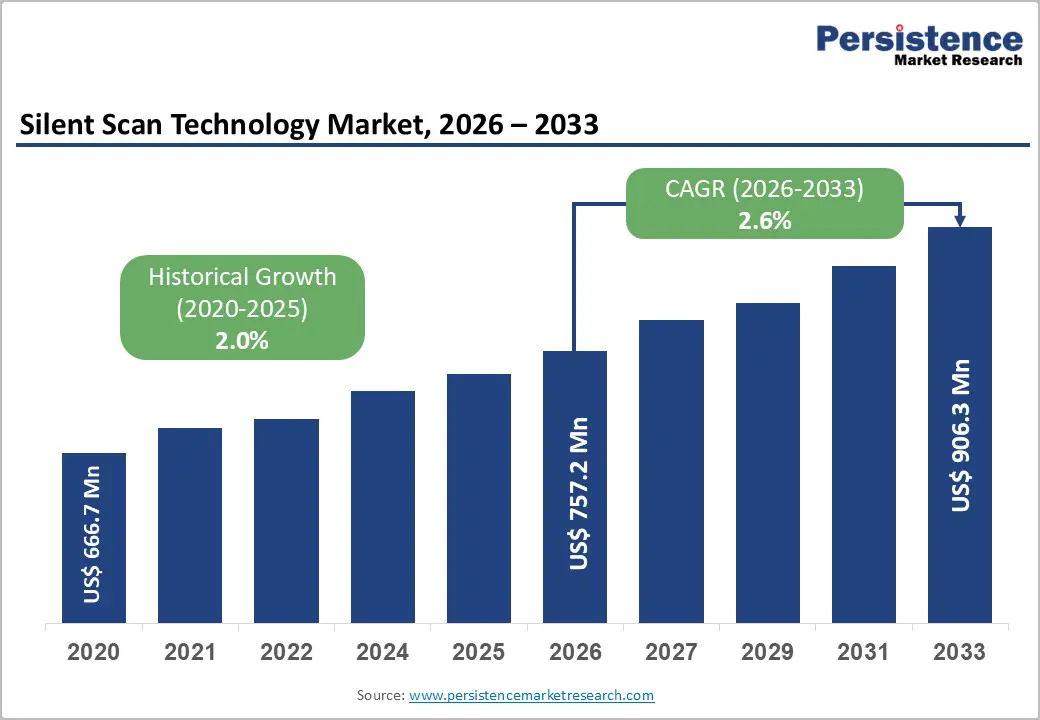

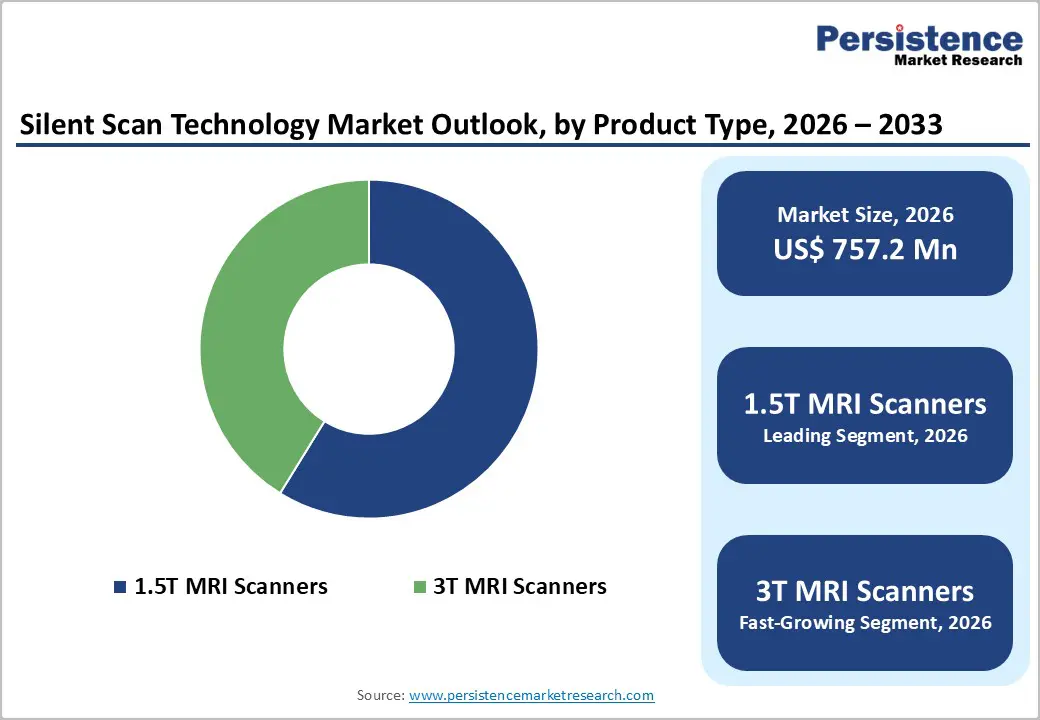

The global silent scan technology market is projected to reach US$ 757.2 million in 2026 and US$906.3 million by 2033, growing at a CAGR of 2.6% over the forecast period.

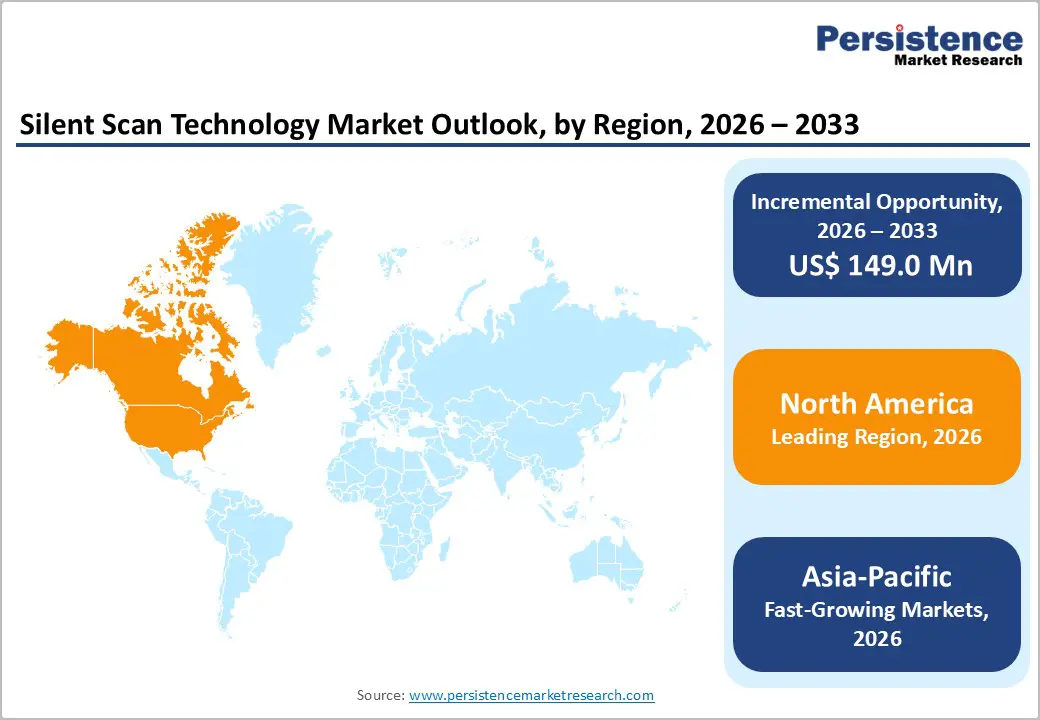

The market is expanding rapidly, driven by aging populations, rising rates of chronic disease, and increasing demand for remote patient monitoring. North America leads, driven by advanced healthcare infrastructure and FDA oversight. The Asia-Pacific region is the fastest-growing region, driven by smartphone penetration, supportive digitization policies, local manufacturing, and rising investments in AI-powered healthcare solutions.

Key Industry Highlights:

- Dominant Segment: 1.5T MRI scanners account for 58.8% of the market in 2025, driven by their optimal balance of image quality, scan speed, wide clinical applicability, patient comfort, and cost-effectiveness for hospitals and diagnostic centers.

- Dominant Region: North America leads in 2025 with 37.4% share, supported by a mature healthcare infrastructure, high adoption of advanced imaging technologies, and a patient-centric regulatory focus. The Asia-Pacific region is the fastest-growing region, driven by rising healthcare investments, expanding diagnostic networks, increasing prevalence of chronic diseases, and a growing emphasis on access to advanced imaging in emerging markets.

- Growth Drivers: Growth is driven by the rising burden of chronic and neurological diseases, increasing demand for patient-friendly MRI procedures, adoption of AI-assisted imaging protocols, technological advancements in gradient coils and noise reduction, and hospitals’ focus on improving patient experience and compliance.

- Opportunity: Key opportunities include expansion in emerging markets, integration with telemedicine and remote diagnostics, development of portable and low-cost silent scan MRI units, AI-enabled imaging enhancements for workflow efficiency, and increasing adoption in patient-focused, value-based healthcare models.

| Key Insights | Details |

|---|---|

|

Silent Scan Technology Market Size (2026E) |

US$ 757.2 Mn |

|

Market Value Forecast (2033F) |

US$ 906.3 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

2.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.0% |

Market Dynamics

Driver: Rising demand for patient-friendly MRI procedures

The global utilization of MRI continues to grow rapidly as clinicians increasingly rely on it for non-invasive diagnosis of neurological, musculoskeletal, and soft-tissue conditions. According to OECD data, MRI exams per 1,000 population in countries like France and Germany range between 120 and 150 annually, reflecting high diagnostic throughput in advanced healthcare systems. Roughly 100–150 million MRI scans occur worldwide each year, with the United States alone performing about 40 million scans annually. This volume underscores the widespread dependence on MRI for accurate diagnostics and monitoring.

Traditional MRI machines generate high noise levels, sometimes up to 120 dB(A), comparable to a rock concert or jackhammer, contributing to patient anxiety, motion artifacts, and incomplete scans. Silent scan technology, which reduces noise significantly (often to below 70–80 dB), directly addresses this issue by improving patient comfort and cooperation, especially among pediatric, geriatric, or claustrophobic patients, leading to better scan completion rates and diagnostic quality. As patients become more health-literate and outcomes-focused, demand for quieter, more comfortable imaging experiences increases, driving adoption of silent scan systems within MRI suites globally.

RESTRAINT: Integration challenges with existing imaging infrastructure

The integration of advanced imaging technologies, such as silent scan MRI, into existing healthcare infrastructure presents significant challenges, particularly for facilities with legacy systems. Healthcare providers often operate diverse equipment portfolios comprising MRI machines of varying generations and IT systems. Achieving seamless interoperability across imaging equipment, hospital IT systems, and electronic health records requires extensive standardization efforts, adherence to DICOM/HL7 protocols, and custom middleware solutions tasks that demand significant time and resources. Healthcare IT analyses show fragmented legacy systems and vendor-specific implementations frequently delay or inflate integration projects.

These technical hurdles are compounded in lower-resource settings where infrastructure deficits, such as unreliable power supply, limited facility space, and underdeveloped networking capabilities, can further constrain the deployment of silent scan MRI systems. The World Bank reports that many developing countries allocate less than 2% of GDP to healthcare, leaving facilities underfunded for advanced diagnostics, such as MRI upgrades. Moreover, the maintenance and calibration of sensitive magnet and gradient systems require specialized staff and technical support, which many community hospitals lack. These integration and infrastructure challenges slow uptake and widen disparities in access to patient-friendly imaging technologies.

Opportunity: Expansion into emerging markets with growing healthcare infrastructure

Emerging markets offer substantial growth opportunities for silent scan technology as healthcare systems in Asia, Latin America, and Africa invest in diagnostic infrastructure to meet rising demand for high-quality care. Global health transition trends reveal significant healthcare expansion needs, with major investments underway to strengthen universal health coverage and access to essential services. For example, the World Bank has emphasised the need for increased health system financing to reach more than 1.5 billion people with quality services by 2030, highlighting persistent infrastructure gaps across low-income countries. and middle-income countries.

MRI access in these regions remains limited: low and middle-income countries average only ~1.1 MRI units per million people, compared with high-income country densities exceeding 30 units per million, indicating a large unmet need for advanced imaging. As healthcare budgets expand and diagnostic imaging capacity strengthens, supported by both government spending and private investment, there’s a growing opportunity to deploy silent scan MRI systems that offer enhanced patient experience and clinical differentiation. Additionally, the strong correlation between the availability of imaging technology and overall healthcare infrastructure capacity suggests that targeted investments in advanced diagnostic modalities, such as silent scan MRI, could yield substantial improvements in care delivery and utilization.

Category-wise Analysis

By Product Type Insights

1.5T MRI scanners lead with a 58.8% share in 2025, as they balance diagnostic capability, affordability, and broad clinical application. In large MRI inventories, roughly 66–82% of systems are 1.5 Tesla units, making them far more common than higher-field scanners in routine practice. For instance, in a recent clinical inventory survey, 81.8% of MRI units were 1.5 T, compared with 17.5% at 3 T, indicating strong installed-base dominance.

Clinicians favour 1.5T for general neurological, musculoskeletal, and abdominal imaging due to well-established protocols and flexibility across indications. They also have lower acquisition and operating costs than 3T systems, making them accessible to mid- and high-volume centres alike. This wide installed base creates a larger addressable market for silent scan upgrades and technology integration.

By End-user Insights

Hospitals lead adoption of MRI and silent scan technology because they are primary hubs for advanced diagnostic imaging. Globally, hospitals account for ~50–60% of all MRI procedures and installations, reflecting their central role in diagnostic workflows for acute care, chronic disease management, and multidisciplinary specialties.

Hospitals have higher patient volumes, broader service requirements, and larger capital budgets than standalone diagnostics centres, enabling them to invest in high-cost equipment such as MRI with silent-scan capabilities. They also integrate imaging across departments, neurology, oncology, orthopaedics, driving continual demand for versatile, patient-centric MRI systems. Furthermore, government funding programs and large-scale healthcare investments often prioritise hospital imaging infrastructure, reinforcing their position as dominant end users of advanced MRI technology.

Regional Insights

North America Silent Scan Technology Market Trends

North America dominates because it has the highest MRI utilization and installed base globally, creating a large addressable market for silent scan technology. The region has more than 12,000 MRI systems performing 40+ million scans annually, far exceeding those of other regions; the United States alone accounts for more than 11,000 units and ~44 million scans per year. The abundance of advanced healthcare facilities, extensive insurance coverage, and supportive reimbursement policies encourage the adoption of patient comfort innovations, such as silent-scan MRI systems. Additionally, North America’s sophisticated healthcare infrastructure, high per-capita health expenditure, and rapid integration of digital and AI imaging technologies further accelerate the uptake of cutting-edge MRI enhancements.

Europe Silent Scan Technology Market Trends

Europe is a key region due to its substantial MRI fleet and emphasis on preventive healthcare, which supports demand for advanced imaging technologies like silent scan systems. The continent operates approximately 10,000 MRI units, collectively delivering over 35 million scans annually across public and private hospitals. Countries such as Germany, the UK, and France lead in MRI adoption, with Western European health systems emphasizing early disease detection through imaging. Government-backed healthcare models and strong regulatory frameworks also facilitate technology upgrades in hospital networks, enhancing patient care quality. Furthermore, initiatives to improve imaging accessibility in rural and underserved areas are driving incremental investments in MRI capacity, making Europe a consistent contributor to global silent scan technology demand.

Asia Pacific Silent Scan Technology Market Trends

Asia-Pacific is the fastest-growing region due to the rapid expansion of healthcare infrastructure, rising diagnostic volumes, and government investments. The region now features over 8,000 MRI systems, performing more than 20 million scans annually, reflecting surging demand in populous countries such as China, Japan, and India. Government initiatives to improve healthcare access and insurance coverage are increasing hospital imaging capacity, while private diagnostic networks are expanding into tier 2 and tier 3 cities. Additionally, strong economic growth and rising prevalence of chronic diseases compel healthcare providers to upgrade imaging capabilities to meet diagnostic needs efficiently. Combined with increasing adoption of digital health solutions and localized manufacturing, these factors drive accelerated adoption of silent scan MRI technology, surpassing growth rates in Western markets.

Competitive Landscape

The silent scan technology market is highly competitive, led by MRI system manufacturers like Siemens Healthineers, GE Healthcare, Philips Healthcare, Canon Medical, and Hitachi. Companies compete through product innovation, silent scan integration, AI enhancements, and hospital partnerships, focusing on patient comfort, image quality, and expanding presence in emerging markets.

Key Industry Developments:

- In January 2026, the U.S. Food and Drug Administration (FDA) cleared the Biograph One PET/MRI system from Siemens Healthineers, marking a major regulatory milestone for advanced hybrid imaging technology. The clearance covered the second-generation positron emission tomography/magnetic resonance (PET/MR) scanner, which combines detailed anatomical and functional imaging in a single platform.

- In March 2025, Philips accelerated precise imaging by integrating unique artificial intelligence technologies into its MRI systems, enhancing diagnostic performance and workflow efficiency. The company introduced its Smart Speed-Precise solution with dual-AI engines and updated MR Workspace software at the European Congress of Radiology in Vienna.

Companies Covered in Silent Scan Technology Market

- General Electric (GE) Healthcare

- Siemens Healthineers

- Philips Healthcare

- Hitachi Healthcare

- Canon Medical Systems Corporation

- Konica Minolta Healthcare

- Neusoft Medical Systems

- United Imaging Healthcare (UIH)

- Aspect Imaging

- Hyperfine Research

- Others

Frequently Asked Questions

The global silent scan technology market is projected to be valued at US$ 757.2 Mn in 2026.

Rising patient demand for comfort, chronic disease prevalence, AI advancements, and hospital imaging upgrades drive growth.

The global silent scan technology market is poised to witness a CAGR of 2.6% between 2026 and 2033.

Expansion in emerging markets, portable MRI units, telemedicine integration, AI imaging enhancements, and patient-focused care.

General Electric (GE) Healthcare, Siemens Healthineers, Philips Healthcare, Hitachi Healthcare, Canon Medical Systems Corporation, Konica Minolta Healthcare.