- Industrial Machinery

- Shiplifts Transfer Systems Market

Shiplifts Transfer Systems Market Size, Share, and Growth Forecast 2026 - 2033

Shiplifts Transfer Systems Market by System Type (Winched Shiplifts, Hydraulic Shiplifts, Floating Shiplifts, Rail-Based Transfer Systems, Others), Capacity (Below 5,000 Tons, 5,000–15,000 Tons, Above 15,000 Tons), Application (Shipbuilding, Ship Repair & Maintenance, Docking & Launching, Offshore Vessel Handling, Leisure & Yacht Handling), End-user, and Regional Analysis, 20262033

Shiplifts Transfer Systems Market Size and Trend Analysis

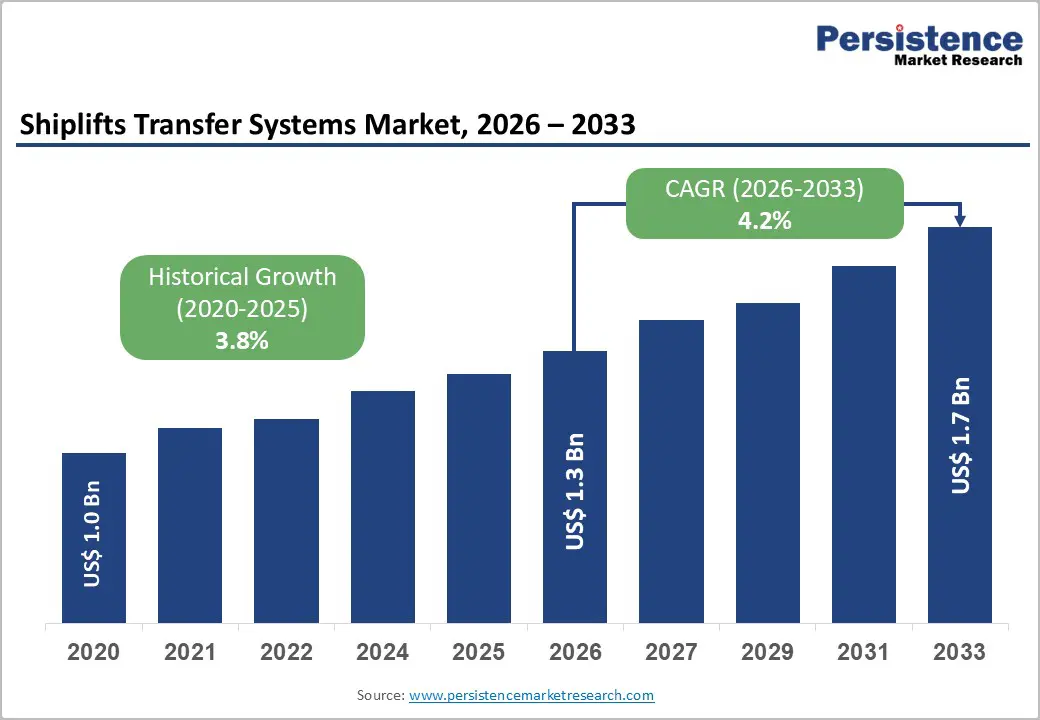

The global shiplifts transfer systems market size is likely to be valued at US$ 1.3 billion in 2026 and is expected to reach US$ 1.7 billion by 2033, growing at a CAGR of 4.2% during the forecast period from 2026 to 2033.

The market expansion is fundamentally driven by three converging demand pressures. First, accelerated naval modernization across major economies, particularly the United States, China, and India, necessitates advanced marine infrastructure to support fleet expansions and lifecycle management.

Key Industry Highlights:

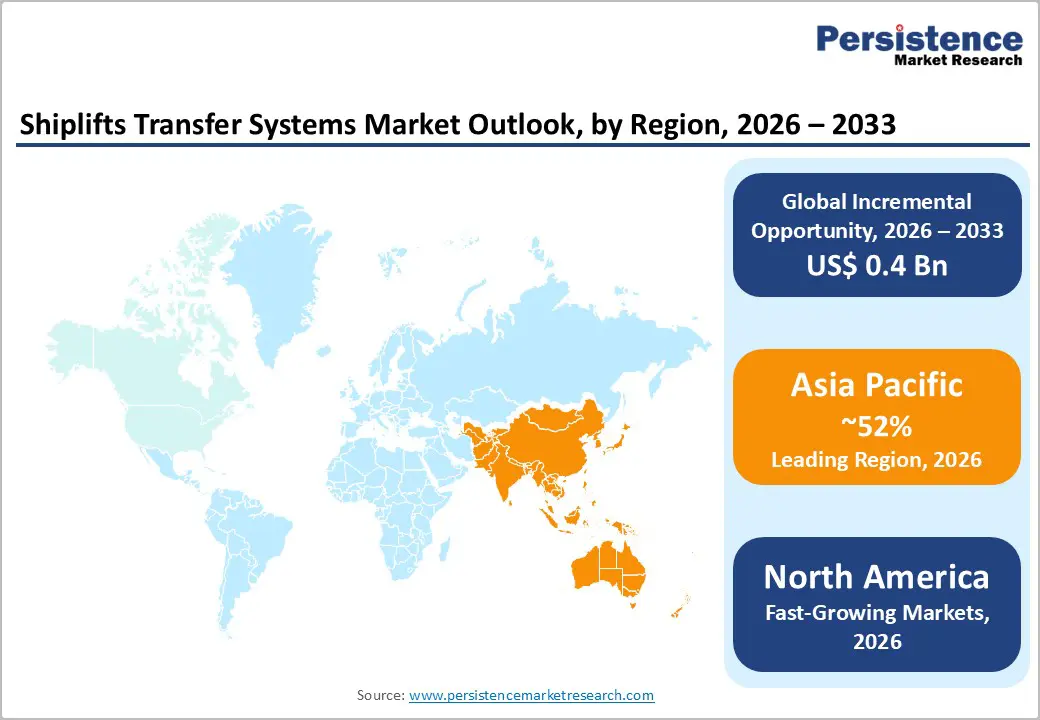

- Leading Region: Asia-Pacific holds about 52% of the global shiplifts market, driven by China’s shipbuilding leadership, India’s INR75,000 crore expansion, and growing Southeast Asian maritime infrastructure.

- Fastest Growing Region: North America is the fastest-growing region, expanding at 6.7% CAGR, supported by rising U.S. Navy budgets, large-capacity shiplift projects, and advanced naval construction programs.

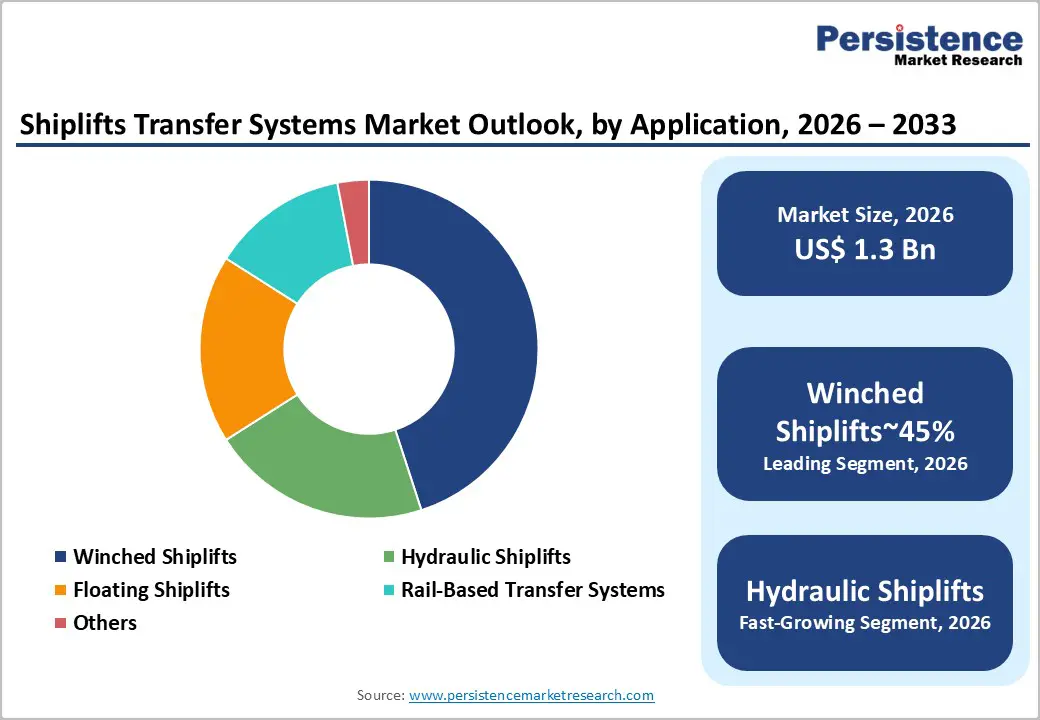

- Leading Segment: Winched shiplifts lead with 45% market share due to reliability and cost efficiency, while hydraulic systems grow fastest at 5.2% CAGR, driven by higher precision requirements.

- Fastest Growing Segment: Ship repair and maintenance is the fastest-growing application at 5.8% CAGR, supported by expanding global service demand and regulatory-driven retrofitting requirements.

- Key Opportunity: Naval modernization remains the strongest growth driver, fueled by large-scale fleet expansion plans, rising defense spending, and a 7.4% CAGR in defense vessel MRO activities.

| Key Insights | Details |

|---|---|

| Shiplifts Transfer Systems Market Size (2026E) | US$ 1.3 Billion |

| Market Value Forecast (2033F) | US$ 1.7 Billion |

| Projected Growth CAGR (2026-2033) | 4.2% |

| Historical Market Growth (2020-2025) | 3.8% |

Market Dynamics

Drivers - Global naval fleet expansion and modernization drive increased demand for advanced shiplift systems across commercial and military shipyards worldwide

Naval forces worldwide are undertaking large-scale modernization programs, which are significantly increasing demand for advanced shiplift and transfer systems. The Indian Navy is following an aggressive expansion strategy, aiming to operate 175–200 warships by 2035, with 68 vessels already under construction at an estimated value of INR2 lakh crore. Similarly, the U.S. Navy allocated US$ 230.8 billion in fiscal year 2024, including US$ 180.5 billion for Navy operations and US$ 50.3 billion for the Marine Corps, supporting its long-term goal of a 355-ship fleet by 2034.

Global defense spending reached US$ 2.443 trillion in 2023, reflecting continued government commitment to strengthening maritime capabilities. In parallel, naval vessel Maintenance, Repair, and Overhaul (MRO) markets are expanding at a 7.4% CAGR through 2029, directly increasing the need for efficient shiplift utilization across both commercial and military shipyards worldwide.

Government-led port upgrades and shipyard expansions in emerging markets stimulate demand for modern shiplift and vessel transfer systems

Governments across emerging economies are investing heavily in port modernization and shipyard expansion, creating strong demand for modern shiplift systems. India’s Maritime Development Fund, valued at INR25,000 crore, supports ship acquisition and comprehensive port upgrades, while an additional INR19,989 crore under the Shipbuilding Development Scheme targets an annual capacity increase of 4.5 million Gross Tonnage.

At the same time, Southeast Asian nations and China are expanding both brownfield and greenfield shipyards, with China accounting for nearly 60% of global merchant vessel orders. India’s Sagarmala 2.0 initiative further strengthens market momentum by allocating INR40,000 crore to catalyze total maritime investments of INR12,00,000 crore between 2025 and 2035. These large-scale infrastructure programs directly drive demand for advanced docking, lifting, and vessel transfer systems across regional shipyards.

Restraints - High investment costs and complex international supply chains limit adoption of large-capacity shiplift systems in global shipyards

Shiplift installations require substantial upfront capital investment, which remains a key restraint for market growth. Large-capacity systems exceeding 15,000 tons often demand investments ranging from US$ 100 million to over US$ 500 million, including civil works, hydraulic systems, automation controls, and commissioning costs. In addition to high capital intensity, the market faces persistent supply chain challenges due to the limited number of global suppliers for specialized hydraulic components, structural steel, and advanced control technologies.

Delays in sourcing critical systems, such as Bosch Rexroth AG hydraulics and specialized electrical components, frequently extend project timelines. Shipyards must coordinate procurement across multiple international vendors while managing tariffs, logistics disruptions, and geopolitical trade risks. These factors increase overall project costs, complicate execution, and discourage smaller shipyards from adopting modern shiplift solutions.

Shortage of trained technicians and complex system maintenance restricts shiplift market growth in developing and retrofit shipyards

The global marine services industry continues to face a shortage of skilled labor, particularly trained shiplift technicians and advanced control system engineers. Specialized expertise is essential for operating and maintaining modern synchronized lifting and hydraulic systems, yet qualified professionals remain limited worldwide. Currently, only about 16 shipyards globally possess retrofit-capable facilities, creating service bottlenecks and longer maintenance cycles. High system complexity also increases long-term operating costs, as routine maintenance and troubleshooting require specialized technical knowledge.

Many smaller and mid-sized shipyards lack access to adequate training programs and technical infrastructure, limiting their ability to adopt advanced shiplift technologies. As workforce development efforts struggle to keep pace with rapid market expansion, labor shortages remain a structural constraint, particularly in developing regions, reducing operational efficiency and slowing broader market penetration.

Opportunity - Expansion of offshore wind farms and specialized vessels creates new growth opportunities for modular and high-capacity shiplift systems

The rapid expansion of offshore renewable energy, particularly floating offshore wind farms, presents strong growth opportunities for advanced shiplift systems. These projects require specialized installation, maintenance, and support vessels, increasing demand for shiplifts capable of handling large and complex vessel designs. Bardex Corporation’s £1,000,000 award from The Crown Estate’s Supply Chain Accelerator program highlights this opportunity, supporting the development of modular shiplift infrastructure tailored for floating wind manufacturing.

Demand is also rising for vessels supporting deepwater operations, such as Anchor Handling Tug Supply (AHTS) ships and offshore wind service platforms, typically requiring systems with 10,000–40,000 ton capacities. Global offshore wind capacity is expected to grow steadily through 2035, driving higher vessel utilization rates. As specialized vessel day rates rise by 25–35% annually, shipyards are increasingly justified in investing in high-capacity, high-margin shiplift systems.

Naval construction initiatives and strategic shipyard development drive long-term demand for modern shiplift and automated handling solutions

Government-led naval construction initiatives are creating long-term opportunities for the shiplift transfer systems market. India’s three-cluster greenfield shipbuilding program, with a targeted investment of INR 75,000 crore across Tamil Nadu, Gujarat, and Odisha, is directly driving demand for modern shipyard infrastructure, including shiplifts and automated transfer systems.

Internationally, Pearlson Shiplift Corporation has secured contracts across Taiwan, the Qatar Free Zone Authority, and the U.S. Gulf Coast, with combined project values exceeding US$ 200–500 million. Strategic partnerships further support market growth, such as HD Hyundai’s INR10,000 crore joint venture with Cochin Shipyard for container ship construction. These programs emphasize advanced docking infrastructure to support large naval and commercial vessels, reinforcing sustained demand across South Asia, the Middle East, and Southeast Asia.

Category-wise Analysis

System Type Insights

Winched shiplift systems continue to dominate the market, accounting for approximately 45% share due to their proven reliability, cost efficiency, and operational simplicity. These systems use synchronized electric or hydraulic winches and cable mechanisms to lift and lower vessels, allowing precise control across varied hull shapes and weight distributions. Their straightforward design reduces maintenance complexity and operating costs when compared to hydraulic or floating dock alternatives.

Winched systems are particularly well-suited for mid-capacity applications ranging from 5,000 to 15,000 tons, which represent the most common requirement among global shipyards. Their flexibility and customization capabilities make them ideal for facilities with space or infrastructure constraints, especially retrofit projects. As shipyards increasingly focus on cost-effective upgrades rather than full replacements, winched shiplift systems remain the preferred and most widely adopted solution.

Capacity Insights

The 5,000–15,000 ton capacity segment leads the global shiplift market with approximately 52% share, reflecting its strong alignment with commercial vessel repair and mid-sized naval operations. This capacity range supports a wide variety of vessel types, including container ships, multipurpose vessels, and general cargo ships, which dominate global fleet composition.

From an investment perspective, systems in this range require moderate capital expenditure, typically between US$ 30 million and US$ 80 million, making them accessible to a broader range of commercial shipyards. Industry data indicates that vessels within this tonnage category account for nearly 60% of global dry-dock demand, directly supporting segment leadership. The balance between operational versatility, cost efficiency, and strong utilization rates positions the 5,000–15,000 ton segment as the primary growth driver in the near to medium term.

Application Insights

Ship repair and maintenance represent the fastest-growing application segment, expanding at a 5.8% CAGR through 2033. This growth is driven by the aging global fleet and increasingly stringent environmental and safety regulations. The global ship repair and maintenance services market is projected to grow from US$ 33.47 billion in 2025 to US$ 54.40 billion by 2033, reinforcing demand for efficient shiplift infrastructure.

Regulatory requirements such as IMO FuelEU rules, effective from 2025 and stricter emission standards are forcing operators to undertake frequent retrofitting and compliance upgrades. Additionally, approximately 86 aging LNG carriers with over 20 years of service require extensive maintenance or decommissioning. These factors are increasing shiplift utilization rates across commercial and naval yards, making repair and maintenance the most consistently expanding application segment.

End-user Insights

Commercial shipyards account for approximately 48% of total shiplift system demand, supported by a recovery in global shipbuilding and rising container vessel construction. The global shipbuilding market reached US$ 164.47 billion in 2026 and is expected to grow to US$ 206.24 billion by 2031 at a 4.6% CAGR, with Asia-Pacific holding a 38.3% share.

China alone accounts for nearly 60% of global merchant vessel orders, reinforcing commercial demand. Naval and defense shipyards represent the fastest-growing end-user segment due to accelerated fleet modernization and rising defense budgets across the U.S., NATO countries, China, and India. Defense vessel MRO activities are expanding at a 7.4% CAGR through 2029, driving sustained investments in advanced shiplift infrastructure tailored for military-grade operations.

Regional Insights

North America Shiplifts Transfer Systems Market Trends

North America is witnessing accelerated growth in the shiplift market, driven primarily by U.S. Navy modernization initiatives and expanding offshore energy projects. A major milestone includes Irving Shipbuilding awarding Bardex Corporation a contract for a 165-meter shiplift with over 27,000 metric tons capacity, the largest in the Americas, with production starting in October 2025. Fincantieri Marinette Marine has also commissioned advanced shiplift infrastructure to support U.S. Navy submarine and surface combatant programs.

These investments align with a 12.5% annual increase in U.S. Navy shipbuilding budgets between 2020 and 2024. Additionally, the U.S. naval vessel MRO market is growing at an 8.12% CAGR through 2025, reinforcing long-term demand for high-capacity, technologically advanced shiplift systems across the region.

Europe Shiplifts Transfer Systems Market Trends

European shipyards maintain strong technological leadership through advanced automation and specialization in high-value vessels. Germany accounts for approximately 26.5% of Europe’s ship repair and maintenance market, with major shipbuilding hubs in Hamburg and Bremen generating steady infrastructure demand. The region’s strong focus on green shipping, LNG propulsion, and emission reduction technologies requires modern shiplift systems capable of supporting complex retrofitting and precision assembly.

EU-wide regulatory frameworks such as the Green Deal are accelerating investments in energy-efficient vessels, driving further demand for advanced docking solutions. European shipyards are also adopting digital twin technologies and automation to improve operational efficiency. This focus on specialized vessels, including LNG carriers, offshore support ships, and naval platforms, supports premium-margin opportunities for advanced shiplift providers across the region.

Asia Pacific Shiplifts Transfer Systems Market Trends

Asia Pacific dominates the global shiplift transfer systems market with approximately 52% regional share, supported by China’s overwhelming leadership in shipbuilding. China accounts for nearly 60% of global merchant vessel orders and produces around 75% of bulk carriers, generating sustained demand for repair and transfer infrastructure. India is also emerging as a major growth market, with INR75,000 crore targeted investment across greenfield and brownfield shipyard clusters.

Japan and South Korea continue to lead in specialized vessels such as LNG carriers and advanced naval platforms, requiring precision-focused shiplift solutions. Pearlson Shiplift’s commissioning for PENTA-Ocean Construction in Japan highlights regional technological advancement. Meanwhile, rapid shipyard development in Southeast Asia, particularly Vietnam and Indonesia, is accelerating demand for modern shiplift systems supporting both commercial and naval expansion.

Competitive Landscape

The global shiplifts transfer systems market shows moderate consolidation, with technological leadership concentrated among the major players. Pearlson Shiplift Corporation, TTS Group ASA, Bardex Corporation, Damen Shipyards Group, and Bosch Rexroth AG collectively hold around 60% market share. High entry barriers limit new competition, as the market requires significant capital investment, advanced engineering expertise, and specialized installation capabilities developed over decades.

Competitive differentiation is driven by system capacity, innovation, and integrated service offerings. Bardex focuses on proprietary OmniLift chain jack technology, while TTS Group leverages its Syncrolift systems and global aftermarket support. Damen integrates shiplifts into turnkey shipyard solutions. Emerging trends include digital controls and AI-based load optimization, with strategic alliances expanding global reach and strengthening long-term competitiveness.

Key Market Developments

- In July 2025, Syncrolift AS, a subsidiary of Nekkar ASA, secured a significant contract to deliver two ship transfer systems to Dubai Maritime City, strengthening its presence in the Middle East and expanding transfer capacity for a key commercial maritime hub.

- In August 2025, Bardex Corporation extended its maintenance contract with the Republic of Korea Navy for Force Multiplier OmniLift systems, underscoring continued naval modernization spending and ongoing demand for lifecycle support of critical naval infrastructure in the Asia-Pacific.

In October 2025, Bardex announced the commencement of mechanical equipment production for the Irving OmniLift shiplift, the largest in North America, with over 27,000 metric tons of capacity, highlighting major progress in naval infrastructure investment and key shipyard development

Companies Covered in Shiplifts Transfer Systems Market

- Bosch Rexroth AG

- Damen Shipyards Group

- GANTREX

- Larsen & Toubro Limited

- Maschinenfabrik Bröhl GmbH

- MTi Co., Ltd.

- Pearlson Shiplift Corporation

- Ra In Ho Co. Ltd.

- Rolls-Royce Holdings PLC

- Royal HaskoningDHV

- TPK Systems Pte Ltd

- TTS Group ASA

Frequently Asked Questions

The global Shiplifts Transfer Systems market is expected to reach US$ 1.7 billion by 2033, growing at a 4.2% CAGR from 2026.

Demand is driven by naval fleet modernization, expansion of global ship repair services, and large-scale port and shipyard infrastructure investments worldwide.

Winched shiplift systems and the 5,000–15,000 ton capacity segment lead the market due to cost efficiency and wide commercial applicability.

Asia-Pacific leads the global market, supported by China’s shipbuilding dominance, India’s shipyard expansion, and Southeast Asia’s port development.

Major opportunities arise from offshore renewable energy vessels and government-backed naval construction and shipyard development programs globally.

The market is dominated by Pearlson Shiplift, TTS Group ASA, Bardex, Damen Shipyards, and Bosch Rexroth, with emerging competition from L&T and Rolls-Royce.