- Food Packaging

- Shelf Stable Packaging Market

Shelf Stable Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Shelf Stable Packaging Market by Product Type (Metal Cans, Bottles, Jars, Others), Packaging Format (Flexible, Rigid), Packaging Material (Plastic, Metal, Others), Application (Sauce & Condiment, Processed Fruit and Vegetable, Others), and Regional Analysis for 2026 – 2033

Shelf Stable Packaging Market Size and Trends Analysis

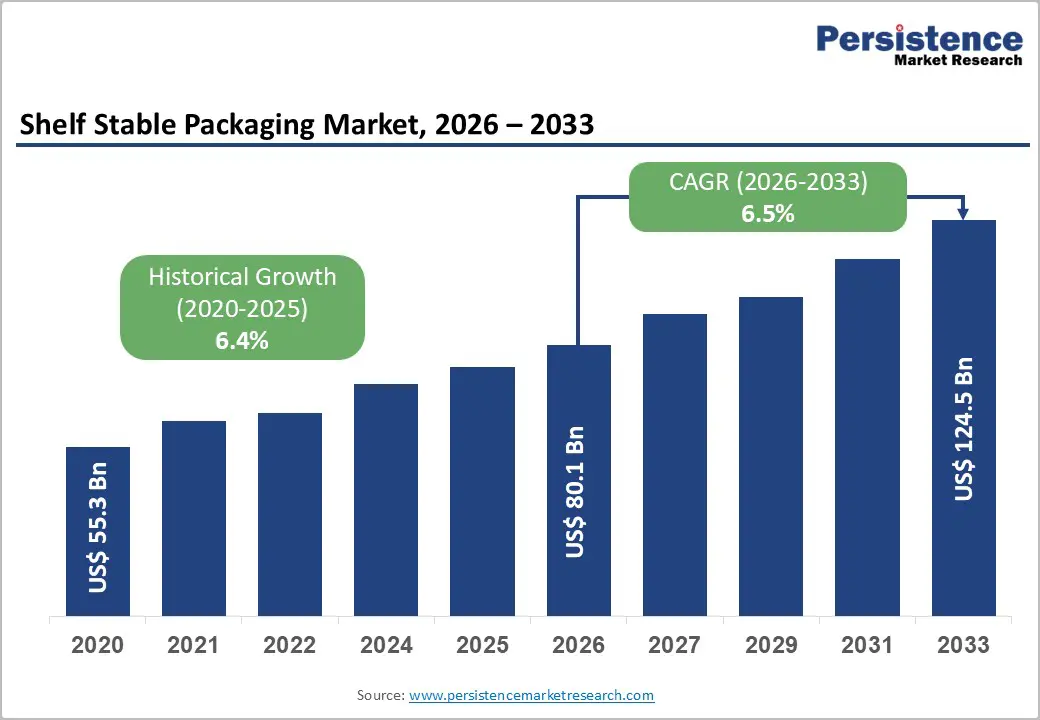

The global shelf stable packaging market size is likely to be valued at US$80.1 billion in 2026, and is expected to reach US$124.5 billion by 2033, growing at a CAGR of 6.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of convenience food consumption, rising demand for long-shelf-life packaged products, and growing adoption of flexible pouches and cartons in emerging markets.

The growing demand for sustainable, lightweight, shelf-stable packaging, especially pouches and cartons for sauces, juices, and dairy, is driving adoption among food processors. Advances in barrier films, recyclable mono-materials, and aseptic filling technologies are improving product protection and reducing environmental impact. Recognized for enhancing supply-chain resilience, reducing food waste, and expanding distribution reach, shelf-stable packaging is a key growth driver in modern retail and e-commerce markets.

Key Industry Highlights:

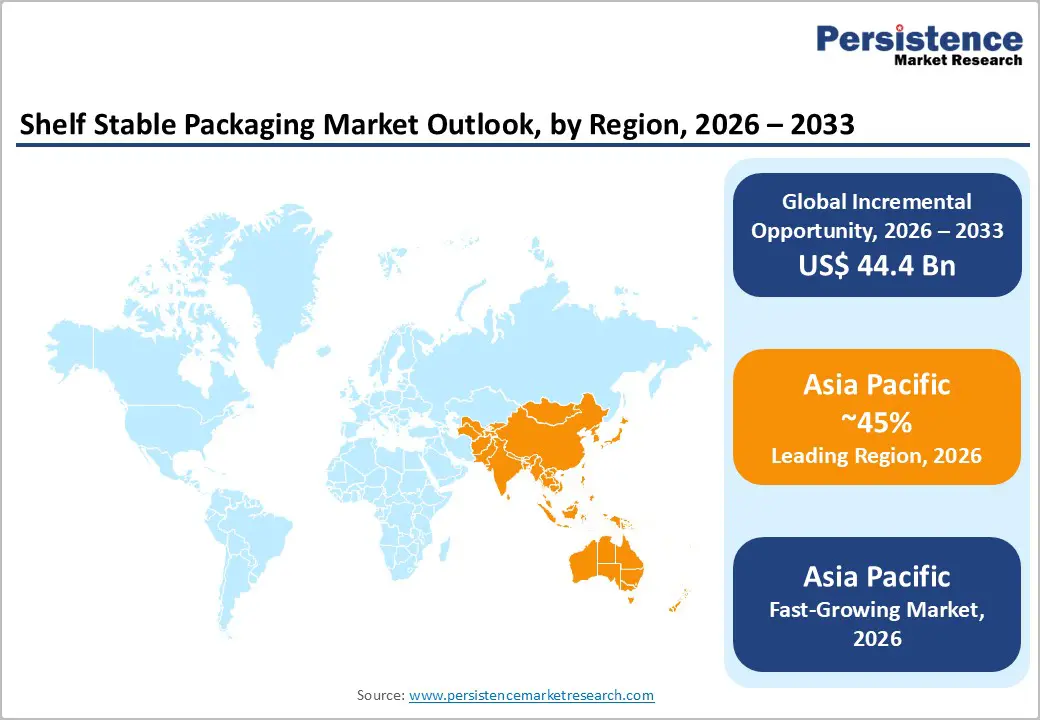

- Leading Region: Asia Pacific, to account for a 45% market share in 2026, driven by massive FMCG production, rapid urbanization, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by expanding middle-class consumption, increasing organized retail, and growing investments in aseptic packaging lines.

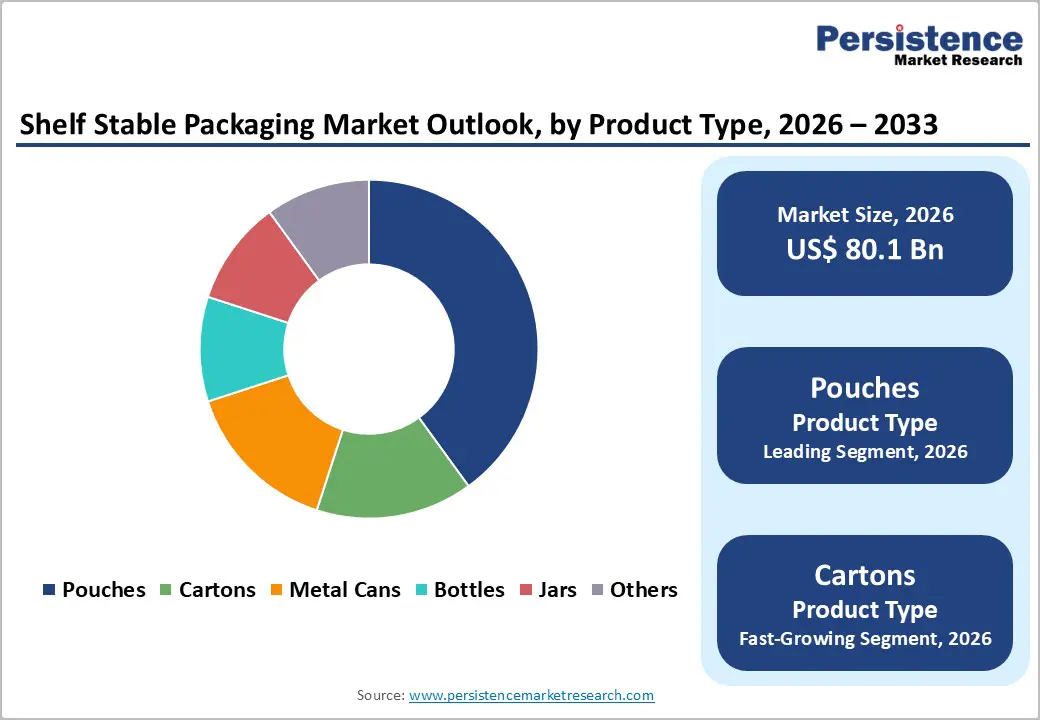

- Dominant Product Type: Pouches, to hold approximately 35% of the market share, as they remain the fastest-growing flexible format.

- Leading Packaging Format: Flexible, to contribute nearly 58% of the market revenue, due to cost and sustainability advantages.

- Global Packaging Waste & Recycling Reality: Only 14% of plastic packaging is collected for recycling worldwide, and food packaging (a core application for shelf-stable formats) faces particularly low recycling efficiency, emphasizing the challenge and opportunity for improved circular design.

| Key Insights | Details |

|---|---|

| Shelf Stable Packaging Market Size (2026E) | US$80.1 Bn |

| Market Value Forecast (2033F) | US$124.5 Bn |

| Projected Growth CAGR (2026-2033) | 6.5% |

| Historical Market Growth (2020-2025) | 6.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Convenience Food Consumption and Organized Retail Expansion

Consumer demand for convenience food, such as ready-to-eat and pre-prepared meal solutions, has grown materially as lifestyles become busier and urban households seek quick, low-effort meal options. In India, this trend is reflected in the rapid expansion of modern food retail channels, including supermarkets and online grocery platforms, which make a broader range of shelf-stable products readily accessible to more consumers. Government and industry data show that India’s retail food and grocery sector is expanding strongly, with modern organized formats expected to capture increasing market share as the overall retail market grows (organized retail’s share of India’s total retail is projected to rise above 35% by 2030) and the e-commerce grocery market growing at multi-year double-digit rates, highlighting the shift to structured, quality-assured retail distribution that favors packaged and shelf-stable goods.

The expansion of organized retail fundamentally supports shelf-stable packaging demand by increasing product visibility and consumption occasions across urban and semi-urban markets. Greater retail penetration brings convenience foods into mainstream consumer baskets in formats that rely on extended durability and secure packaging for distribution and storage. As retail infrastructures modernize and digital channels expand, shelf-stable packaged foods benefit from improved logistics and supply chains that enable longer shelf life without refrigeration, reducing waste and lowering distribution costs.

Increasing Focus on Food Waste Reduction and Supply-Chain Resilience

A growing emphasis on food waste reduction and strengthening supply-chain resilience is reshaping how food products are packaged and moved through value chains, creating a strong impetus for shelf-stable packaging. Governments and international agencies have highlighted the scale of the problem: about 19% of food available to consumers is wasted annually at retail, food service, and household levels, and an additional 13% is lost in supply chains before retail, underscoring systemic inefficiencies in harvesting, storage, and distribution. These losses translate into lost economic value, unnecessary greenhouse gas emissions, and heightened pressure on food systems to feed growing populations sustainably. By extending the usable life of food products and reducing dependence on cold-chain infrastructure, shelf-stable packaging helps limit spoilage and waste during transit and at points of sale, enhancing overall supply-chain robustness.

Supply-chain resilience has become a priority as disruptions ranging from logistical delays to infrastructure gaps expose vulnerabilities that can amplify waste and compromise food security. Reducing the volume of food that spoils before reaching end consumers preserves value and stabilizes supplies, which is essential for national food strategies and crisis preparedness. Shelf-stable packaging supports this resilience by enabling longer storage without refrigeration, simplifying logistics, and facilitating broader geographic distribution, mitigating risks from transport delays and fluctuating demand.

Barrier Analysis – Environmental Concerns and Plastic Waste Regulations

Rising regulatory and environmental pressures on plastic waste are constraining demand for traditional shelf-stable packaging formats that rely heavily on plastic materials. Government data shows that plastic packaging accounts for a significant portion of waste streams; in India, only about 9% of plastic waste was recycled in 2022, leaving the remainder to accumulate in landfills and unmanaged sites. This low recycling rate highlights the environmental cost of plastics in packaging and intensifies scrutiny on materials that contribute to waste and pollution. Globally, governments are tightening regulations on single-use plastics and imposing Extended Producer Responsibility (EPR) requirements that hold manufacturers accountable for end-of-life waste, increasing compliance complexity and costs for packaging producers.

These environmental concerns are prompting shifts toward sustainable alternatives and stricter policy frameworks that disadvantage conventional plastic-based shelf-stable packaging. Regulatory measures such as bans on single-use items and mandatory recycled content targets raise barriers for producers reliant on non-recyclable materials, pushing them toward investment in eco-friendly solutions with higher production costs. Policymakers are also enhancing monitoring and reporting systems to enforce waste management rules more effectively, further pressuring businesses to adapt.

Recycling and Circular Economy Challenges

Recycling and circular economy challenges pose significant restraints for the shelf-stable packaging market by limiting the efficient recovery and reuse of materials at the end of their lifecycle. Many shelf-stable packaging formats, such as multi-layer laminates combining plastics, aluminum foils, and barrier films, are engineered for performance, not recyclability. These composite structures are difficult to separate into constituent materials using existing recycling infrastructure, which leads to low recycling rates and increased waste sent to landfills or incinerators. The inability to process these formats effectively elevates disposal costs for waste managers and places pressure on manufacturers to redesign products for circularity.

The transition from linear “take-make-dispose” models to circular systems where packaging materials are continually reused or recycled into like-for-like applications requires technology investments, policy alignment, and stakeholder coordination across the value chain. Recycling facilities must upgrade sorting and reprocessing capabilities to handle complex packaging types, while brands must shift to designs that prioritize material homogeneity and recyclability. Policy frameworks in many regions are still evolving, creating uncertainty for investments in circular solutions. Consumer expectations for sustainable packaging add market pressure on producers, while the economics of recycling mixed materials remain challenging.

Opportunity Analysis – Innovation in Recyclable and Mono-Material Shelf-Stable Formats

Innovative recyclable and mono-material shelf-stable packaging formats present a significant market opportunity as businesses seek to align product design with circular economy goals and tightening regulatory frameworks. Government waste data from the UK shows that 64.1% of packaging waste was recycled in 2024, with paper & cardboard achieving the highest rates at 74.3%, demonstrating both the feasibility and commercial advantage of materials that fit existing recycling systems. Designing shelf-stable packaging using single polymers or highly recyclable substrates simplifies sorting and reprocessing, reducing downstream waste management costs for supply chains and enhancing material recovery rates. These innovations can improve resource efficiency while offering clear sustainability credentials to retail partners and end consumers looking for lower-impact products.

The shift toward recyclable and mono-material alternatives also helps manufacturers mitigate regulatory risk and capitalize on emerging policy incentives. Recyclable formats that integrate into established recycling streams reduce dependence on complex multi-layer materials that struggle to be recovered at scale. As government targets for recycled content and waste reduction tighten globally, companies that pioneer high-performance recyclable packaging can differentiate their offerings, future-proof supply chains, and potentially lower compliance costs.

Developments in E-commerce and Direct-to-Consumer Shelf-Stable Formats

Growth in e-commerce and direct-to-consumer (DTC) distribution is reshaping demand for shelf-stable packaging by creating new performance requirements and expanding market reach. Online grocery and packaged food sales eliminate many traditional retail constraints, requiring products to withstand longer transit times, varied handling conditions, and diverse storage environments before reaching the end customer’s doorstep. Shelf-stable packaging addresses these needs by ensuring product safety and quality without reliance on cold-chain logistics, which can be costly and complex to manage across broad geographic delivery zones. Improvements in packaging durability, barrier protection, and ease of shipment reduce the risk of damage and spoilage, supporting customer satisfaction and repeat purchases in competitive e-commerce ecosystems.

DTC models further amplify this opportunity by allowing brands to control packaging design and presentation directly, strengthening consumer engagement and enabling tailored formats. Customizable shelf-stable packages such as portioned, resealable, or subscription-ready formats enhance convenience and reinforce brand identity, which is critical when physical shelf presence is absent. E-commerce platforms also generate rich consumer data, enabling companies to optimize packaging based on purchase patterns, delivery feedback, and regional preferences, driving iterative improvements.

Category-wise Analysis

Product Type Insights

Pouches are anticipated to dominate the market, accounting for approximately 35% of the market share in 2026. Their dominance is driven by their cost efficiency, lightweight structure, and strong barrier performance. Flexible pouches reduce material usage compared to rigid packaging, lowering transportation and storage costs across supply chains. Their compatibility with retort and aseptic processing makes them suitable for ready-to-eat meals, sauces, pet food, and beverages. Consumer preference for convenient features such as resealability, easy pouring, and portability further strengthens adoption. Tasty Bite’s ready-to-eat meals are sealed in multi-layer retort pouches that can maintain product safety and quality for up to 18 months without refrigeration, illustrating how pouch formats extend shelf life and support broad distribution.

Cartons represent the fastest-growing product type, with their strong sustainability profile, efficient material use, and alignment with growing retailer and consumer emphasis on recyclability. Constructed primarily from paperboard, cartons offer excellent printability and branding opportunities while providing effective protection for liquids and dry goods without excessive weight. Their compatibility with aseptic processing enables long shelf life at ambient temperatures, reducing dependence on refrigeration and lowering distribution costs. Tetra Brik® Aseptic cartons are widely used by dairy and juice producers to keep products safe at room temperature for months without refrigeration, a capability that supports extended shelf life and broader distribution.

Packaging Material Insights

Plastic is expected to dominate the market, contributing nearly 52% of revenue in 2026, supported by its versatility, durability, and cost efficiency. Plastic materials such as PET, PP, and PE offer strong moisture and oxygen barrier properties, which are critical for extending product shelf life in ambient conditions. Their lightweight structure reduces transportation costs and improves supply chain efficiency compared to glass or metal alternatives. Plastics are compatible with retort and aseptic processing technologies, supporting high-volume food and beverage applications. Berry Global Group, Inc. is a major global producer of plastic packaging used in shelf-stable food and beverage products. The company manufactures a wide range of rigid and flexible plastic containers, bottles, and pouches that protect products from moisture and oxygen, ensuring long shelf life at ambient temperatures.

The paper & paperboard segment represents the fastest-growing packaging material, with strong alignment with sustainability and recyclability priorities across supply chains. These materials are derived from renewable sources and can be efficiently recycled within existing municipal systems, reducing environmental impact compared with some multi-layer plastic formats. Paperboard also offers excellent printability and structural strength, making it suitable for cartons, wraps, and rigid boxes that protect dry foods and beverages at ambient temperatures. Graphic Packaging International is a major global producer of fiber-based cartons and folding cartons for food and beverage brands. The company supplies paperboard packaging used for juices, milk alternatives, dry goods, and other ambient products, enabling protection and long shelf life with materials that fit into traditional recycling streams and consumer waste systems.

Regional Insights

North America Shelf Stable Packaging Market Trends

North America is propelled by the region’s advanced food processing, strong brand innovation, and high public awareness of convenience and sustainability benefits. Distribution systems in the U.S. and Canada provide extensive support for shelf stable packaging programs, ensuring wide accessibility across pouches, flexible, and food populations. Increasing demand for lightweight, convenient, and easy-to-recycle forms is further accelerating adoption, as these formats improve shelf life and reduce barriers associated with chilled distribution.

Innovation in shelf stable packaging technology, including stable, recyclable, improved aseptic delivery, and targeted beverage enhancement, is attracting significant investments from both public and private sectors. Government initiatives and FDA/USDA campaigns continue to promote use against waste risks, sustainability concerns, and emerging DTC threats, creating sustained market demand. The growing focus on carton grades and specialty uses, particularly for food and other products, is expanding the target applications for shelf stable packaging.

Europe Shelf Stable Packaging Market Trends

Europe is driven by increasing awareness of sustainability and convenience benefits, strong regulatory systems, and government-led circular economy programs. Countries such as Germany, France, the U.K., and Italy have well-established food and packaging frameworks that support routine shelf stable packaging use and encourage the adoption of innovative material delivery methods, including recyclable cartons and mono-material pouches. These high-compliance formulations are particularly appealing for food populations, regulation-conscious brand owners, and beverage users, improving shelf life and coverage rates.

Technological advancements in shelf stable packaging development, such as enhanced recyclability, application-targeted delivery, and improved aseptic grades, are further boosting market potential. European authorities are increasingly supporting research and trials for packaging against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, eco-friendly options is aligned with the region’s focus on preventive plastic reduction and food-waste minimization. Public awareness campaigns and promotion drives are expanding reach in both food & beverage and healthcare segments, while suppliers are investing in sustainable substrates and novel variants to increase efficacy.

Asia Pacific Shelf Stable Packaging Market Trends

Asia Pacific is expected to dominate and be the fastest-growing, capturing the 45% revenue in 2026, driven by rising convenience food awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Indonesia, and Thailand are actively promoting packaging campaigns to address packaged food growth and emerging sustainability needs. Shelf stable packaging is particularly attractive in these regions due to its cost-effective administration, ease of adoption, and suitability for large-scale food & beverage and beverage drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deploy shelf stable packaging, which can withstand challenging distribution conditions and minimize cold-chain dependence. These innovations are critical for reaching domestic brand owners and improving overall product coverage. Growing demand for pouches, flexible, and food applications is contributing to market expansion. Public-private partnerships, increased FMCG expenditure, and rising investment in packaging research and production capacity are further accelerating growth. The convenience of packaging delivery, combined with improved shelf life and reduced risk of spoilage, positions it as a preferred choice.

Competitive Landscape

The global shelf-stable packaging market is characterized by intense competition between multinational packaging leaders and emerging sustainability-focused innovators. In North America and Europe, companies such as Amcor Plc and Tetra Pak International S.A. maintain strong market positions through advanced research and development capabilities, integrated supply chains, and long-standing relationships with leading food and beverage brands. Their investments in high-barrier flexible pouches and aseptic carton technologies strengthen product performance while meeting evolving regulatory and environmental standards.

In the Asia Pacific region, regional manufacturers compete through cost-efficient production models and localized distribution networks, improving accessibility for growing food processing industries. Flexible packaging formats support lightweighting initiatives, reduce transportation costs, and enhance operational efficiency across large-scale food lines. Strategic partnerships, acquisitions, and technology collaborations are accelerating innovation cycles and portfolio expansion.

Key Industry Developments:

- In February 2026, Amcor announced the commercialization of its AmPrima® Plus recycle-ready packaging to help cheese processors meet sustainability mandates across North America. Agropur’s Grand Cheddar™ was transitioned from a paperboard overpack with flow wrap film to an all-flexible AmPrima® Plus format. Premium shelf appeal was maintained using Amplify® finishing technologies, including matte overlacquer and metallic inks, while improving recyclability and packaging efficiency.

- In February 2025, Tetra Pak announced the introduction of packaging material incorporating certified recycled polymers, becoming the first company in the food and beverage packaging industry in India to take this step. The carton packages integrating recycled polymers were certified under ISCC PLUS (International Sustainability & Carbon Certification), a globally recognized sustainability certification system. The packaging material was designed to include 5% certified recycled polymers, in compliance with the mandate issued by the Ministry of Environment, Forests & Climate Change under the Plastic Waste Management (Amendment) Rules 2022. The regulatory requirement was scheduled to come into effect on April 1, 2025.

Companies Covered in Shelf Stable Packaging Market

- Amcor Plc

- Tetra Pak International S.A.

- Crown Holdings Inc.

- Silgan Holdings Inc.

- Mondi Group

- Reynolds Group Holdings Ltd.

- Ardagh Group S.A.

- Sealed Air Corporation

- Printpack Inc.

- DuPont de Nemours Inc.

- Avient Corporation (formerly PolyOne)

- Bemis Company Inc. (now Amkor Flexibles)

- Spartech LLC

Frequently Asked Questions

The global shelf stable packaging market is projected to reach US$80.1 billion in 2026.

Increasing urbanization, busy lifestyles, and dual-income households are accelerating the consumption of ready-to-eat and processed food products that require extended shelf life and ambient storage capability.

The shelf stable packaging market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Expanding food processing industries and improving retail infrastructure in emerging economies are increasing demand for ambient, long-life packaged foods, opening new revenue streams for cost-effective and scalable shelf-stable packaging solutions.

Amcor Plc, Tetra Pak International S.A., Crown Holdings Inc., Mondi Group, and Silgan Holdings Inc. are the key players.