- Processed Food

- Seitan Market

Seitan Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Seitan Market is segmented by Product Type (Flavored Seitan and Plain Seitan), by Form (Fresh, Frozen, Canned, and Dried), Sales Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online retail, and Others), and Regional Analysis, 2026 - 2033

Seitan Market Share and Trends Analysis

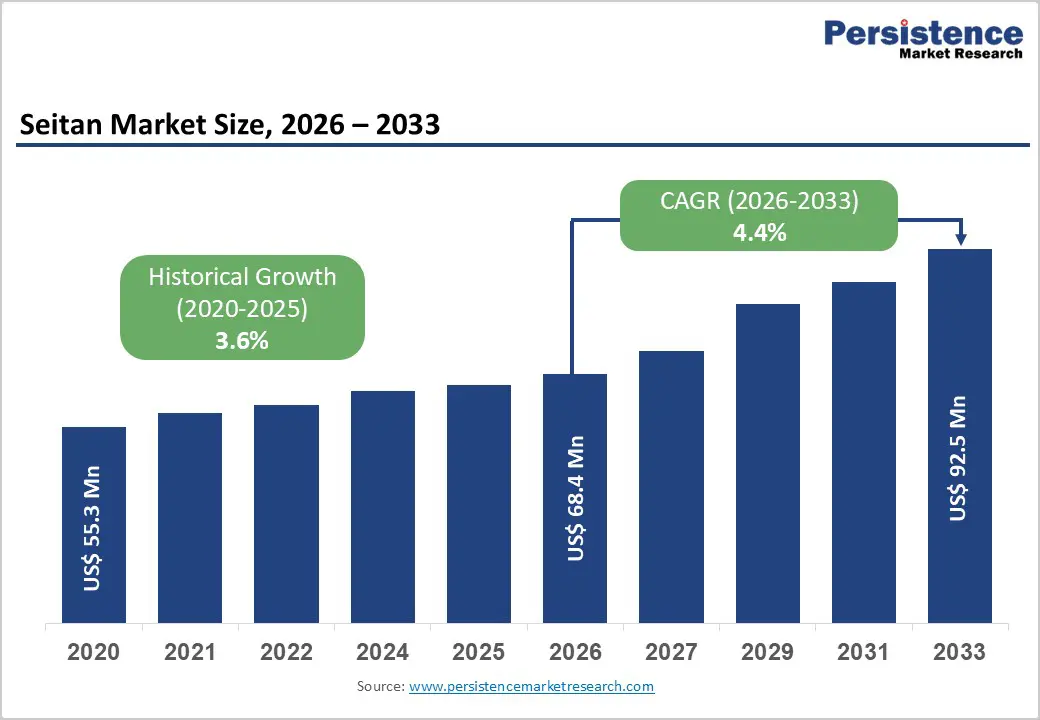

The global seitan market size is expected to be valued at US$ 68.4 million in 2026 and projected to reach US$ 92.5 million by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

The market is predominantly driven by the surging global transition toward plant-based diets and the increasing consumer preference for soy-free meat alternatives. As a wheat-gluten-based protein, seitan offers a unique fibrous texture that closely mimics traditional meat, making it a preferred choice for flexitarians and vegans alike. Furthermore, the market's historical growth of 3.6% between 2020 and 2025 indicates steady maturation, supported by the expansion of organized retail and a rising emphasis on high-protein, low-fat nutritional profiles in Western and Asian cuisines.

Key Industry Highlights:

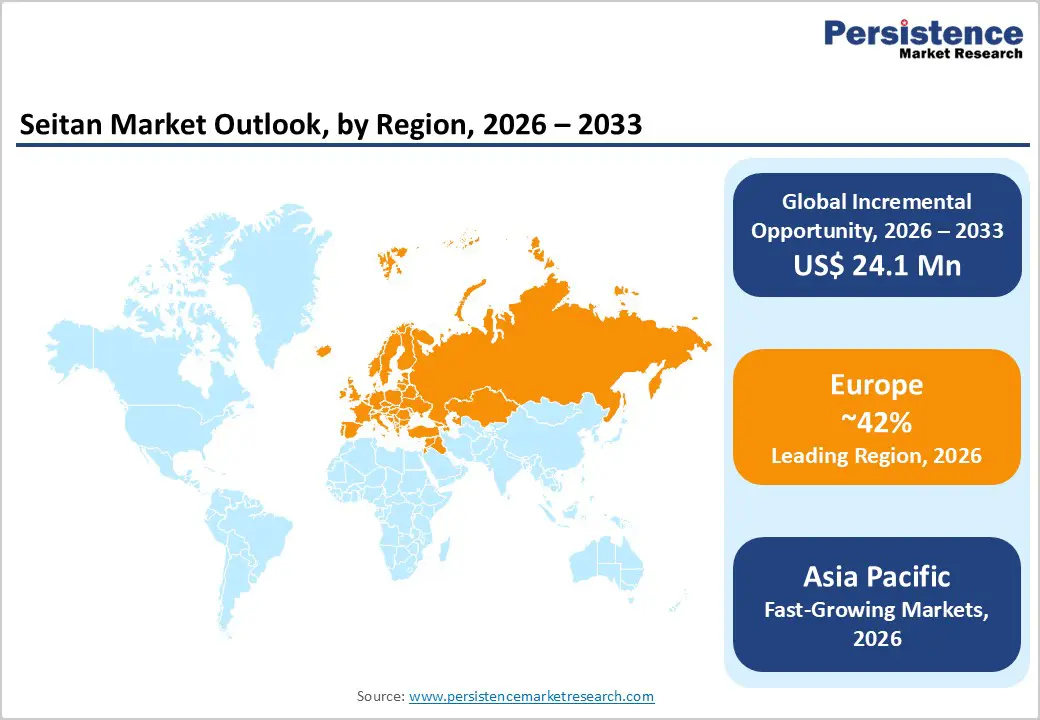

- Leading Region: Europe accounted for a 42% market share in 2025, driven by a mature vegan ecosystem and the long-standing cultural acceptance of wheat gluten in Germany and the U.K.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, fueled by the modernization of traditional wheat gluten dishes and rising demand in China and India.

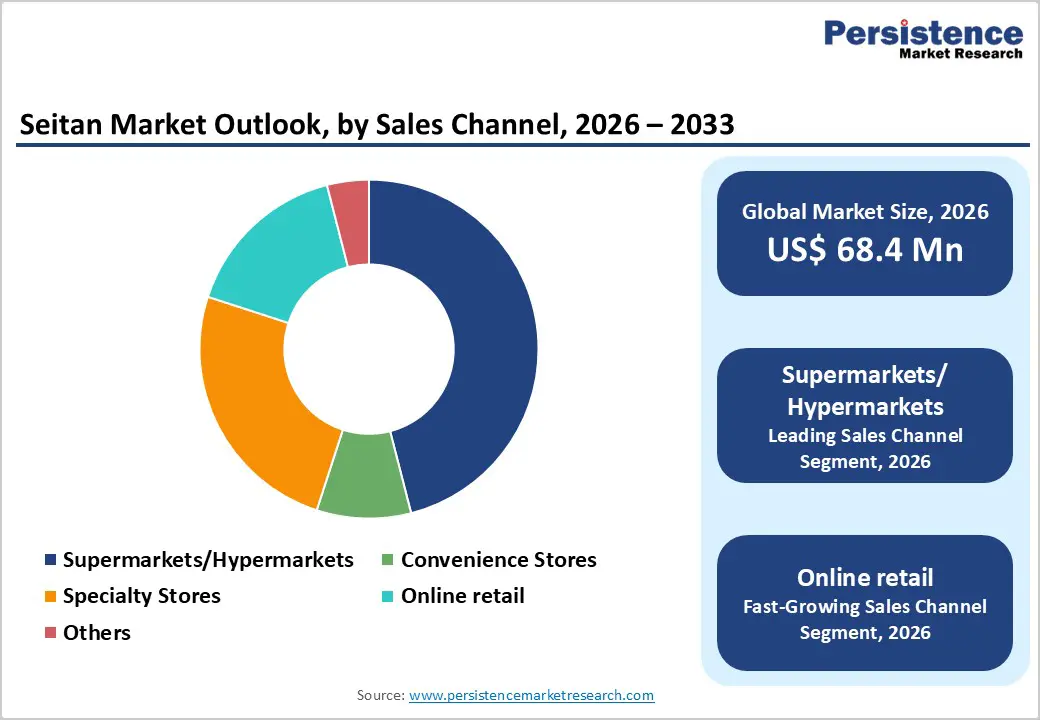

- Dominant Segment: Supermarkets/Hypermarkets remained the leading distribution channel with a 46% share in 2025, providing the essential cold-chain visibility for seitan products.

- Fastest Growing Segment: Online retail is the fastest-growing sales channel, as digital platforms offer consumers access to a wider variety of artisanal and specialty seitan brands.

- Key Market Opportunity: The Foodservice sector presents a high-value opportunity for seitan brands to partner with restaurants and QSR chains to drive menu innovation.

| Key Insights | Details |

|---|---|

|

Seitan Market Size (2026E) |

US$ 68.4 Mn |

|

Market Value Forecast (2033F) |

US$ 92.5 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.6% |

Market Dynamics

Driver - Rising Consumer Preference for Soy-Free Protein Alternatives

A significant catalyst for the Seitan Market is the growing population of consumers who are sensitive or allergic to soy-based products like tofu and tempeh. While soy has historically dominated the plant-based protein landscape, seitan, derived from hydrated wheat gluten, offers a nutritionally dense alternative with a distinct, chewy texture that many find more satisfying than legumes. In 2025, health organizations and nutrition journals highlighted the benefits of diversifying plant-protein sources to avoid overreliance on a single crop. This trend is particularly prevalent in North America and Europe, where soy-free claims are increasingly featured on packaging to attract allergen-conscious shoppers. The versatility of seitan in absorbing seasonings makes it a staple in clean-label meat substitutes.

Restraints - High Prevalence of Gluten Sensitivity and Celiac Disease

The primary barrier to the widespread adoption of seitan is its fundamental composition: it is almost entirely made of wheat gluten. This makes the product strictly off-limits for the growing number of individuals diagnosed with celiac disease or non-celiac gluten sensitivity. According to the Celiac Disease Foundation, nearly 1% of the global population is affected by celiac disease, and a larger percentage avoids gluten due to perceived digestive benefits. This physiological constraint limits seitan's total addressable market relative to other plant-based proteins, such as pea and mycoprotein, which are naturally gluten-free. As gluten-free diets continue to trend as a lifestyle choice, seitan manufacturers face a ceiling on consumer penetration in health-conscious segments.

Opportunity - Expansion into the Foodservice and Quick-Service Restaurant (QSR) Sector

There is a significant opportunity for seitan manufacturers to enter the global foodservice industry, where demand for plant-based menu items is at an all-time high. Because seitan holds its structure well under various cooking methods, including grilling, frying, and braising, it is an ideal ingredient for restaurant chefs. In 2024, notable developments included Blackbird Foods launching seitan-based wings in major retail and restaurant chains, signaling a move toward mainstream adoption. Partnerships with global QSR chains for seitan-based sandwiches or tacos can significantly increase brand visibility and consumer trial, especially as restaurants seek cost-effective alternatives to expensive lab-grown or highly processed vegan meats.

Category-wise Analysis

Form Insights

The frozen seitan segment currently accounts for a substantial share of the market, as it offers a longer shelf life and easier storage for both retail consumers and foodservice operators. Frozen seitan products are particularly popular for bulk purchases and as a backup protein source for household meal planning. Conversely, the Fresh (refrigerated) segment is gaining momentum, often perceived as a "premium" and "cleaner" option by health-conscious shoppers in specialty organic stores. Dried seitan, such as wheat gluten flakes or powder, is widely used in industrial applications and by home cooks who make seitan from scratch, representing a smaller but stable niche in the overall market.

Sales Channel Insights

Supermarkets/Hypermarkets dominated the distribution landscape in 2025, accounting for 46% of the market. These large-format stores provide the necessary cold-shelf visibility and variety that drive bulk of the volume sales. Major chains like Walmart, Tesco, and Carrefour have significantly expanded their private-label plant-based offerings to include seitan-based items. Meanwhile, Online retail is the fastest-growing channel. The shift in consumer behavior toward digital grocery shopping, accelerated by the post-pandemic digital infrastructure, allows for a wider assortment of artisanal and imported seitan brands that may not be available in local brick-and-mortar stores, providing a crucial growth lever for the forecast period.

Regional Insights

Europe Seitan Market Trends and Insights

Europe held the leading global market share of 42% in 2025, with Germany, the U.K., and France acting as the primary consumption centers. The region has a long history of utilizing wheat protein in traditional dishes, which has made seitan more culturally acceptable than in other Western regions. In 2023, the Dublin-based brand Thanks Plants successfully rolled out its seitan meat alternatives across all 157 ALDI outlets in Ireland, demonstrating the scale of retail penetration. Germany remains the most significant single-country market, supported by a high percentage of vegans and vegetarians and a robust organic food movement.

European regulations, including EU food labeling laws and recent debates over the use of "meat-like" terms for plant products, significantly affect the market. Manufacturers in the region often prioritize Organic certification, with brands like Biona Organic and The Bridge leading the premium segment. The expansion of plant-based options in traditional European foodservice, from schnitzels to stews, has further cemented seitan's role as a versatile protein backbone in the continent’s evolving food system.

Asia Pacific Seitan Market Trends and Insights

Asia-Pacific region is the fastest-growing market, projected to expand at a high CAGR through 2032. This growth is underpinned by the deep culinary roots of wheat gluten in China, Japan, and Vietnam, where seitan has been consumed for centuries as a Buddhist temple food. In 2025, the modernization of this traditional ingredient into Western formats such as burgers and nuggets is driving a new wave of demand among younger urban populations. India and China represent massive potential markets due to their large vegetarian populations and rising middle-class disposable incomes.

Manufacturing advantages in Asia, particularly the high domestic production of wheat, allow for cost-effective scaling of the seitan industry. In Japan, the demand for functional and healthy aging foods has led to the marketing of seitan for its low-fat and high-mineral content. The rapid proliferation of e-commerce and mobile-grocery platforms in Southeast Asia is further lowering the barriers to entry for global brands. As regional governments promote sustainable food systems and alternative proteins to ensure food security, the Asia Pacific seitan industry is poised for significant structural expansion.

Competitive Landscape

The global seitan market is characterized by a moderately fragmented structure, where specialized plant-based companies coexist with large-scale food conglomerates. Strategic mergers and acquisitions are common as global firms seek to diversify their protein portfolios; for instance, Nestlé S.A. acquired Sweet Earth Foods to gain a foothold in the North American seitan and plant-based space. Key differentiators in the market include flavor innovation, textural quality, and clean-label certifications such as Organic, Non-GMO, and Kosher.

Emerging business models are increasingly focused on the "experience economy," with brands opening vegan butcher shops or partnering with high-profile chefs to showcase seitan in fine-dining settings. Research and development are currently focused on improving the "juiciness" and "bite" of seitan to better compete with pea-protein-based substitutes. Furthermore, companies are investing in sustainable packaging to align with the overall eco-conscious values of their core consumer base.

Companies Covered in Seitan Market

- Upton's Natural

- Companion Foods

- Sweet Earth Foods

- Tofoo

- Franklin Farms

- Biona Organic

- The Bridge

- TerraSana

- Others