- Sporting Goods & Equipment

- Scuba Gloves Market

Scuba Gloves Market Size, Share, and Growth Forecast 2026 - 2033

Scuba Gloves Market by Thickness (1 Millimeter, 2 Millimeter, 3 Millimeter, 5 Millimeter, 6 Millimeter and Above), Size (Small, Medium, Large, Extra Large, Extra Extra Large), Closure Type (Full Wrist Strap, No Wrist Strap, Velcro Closure, Zippered Wrist), End-user (Male, Female, Kids), and Regional Analysis, 2026 - 2033

Scuba Gloves Market Size and Trend Analysis

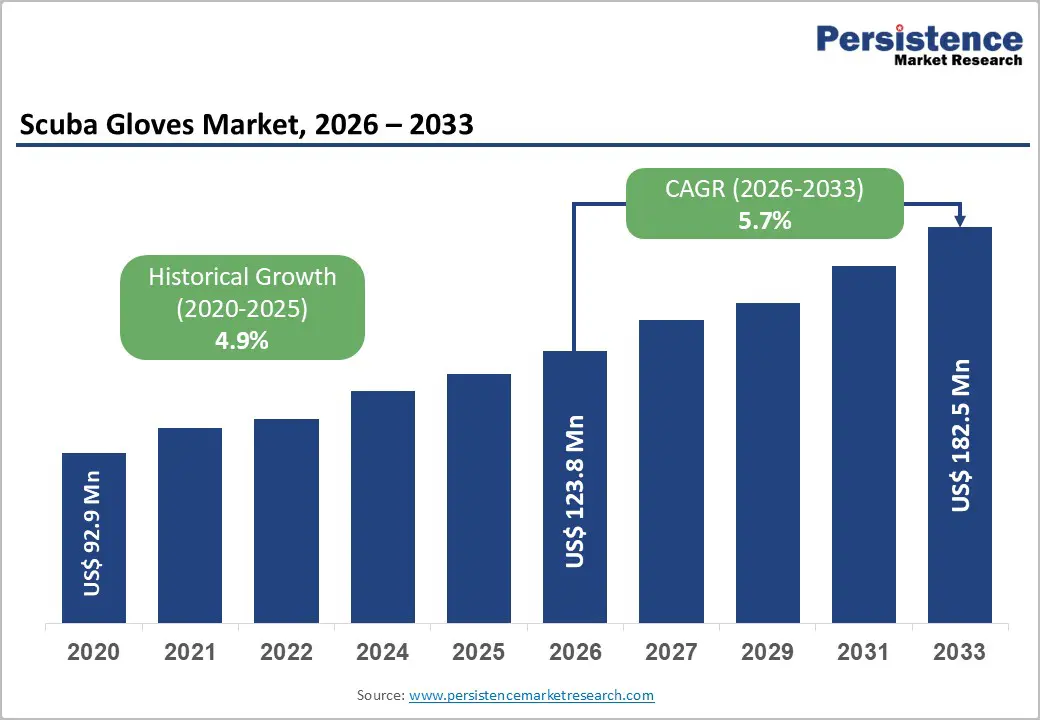

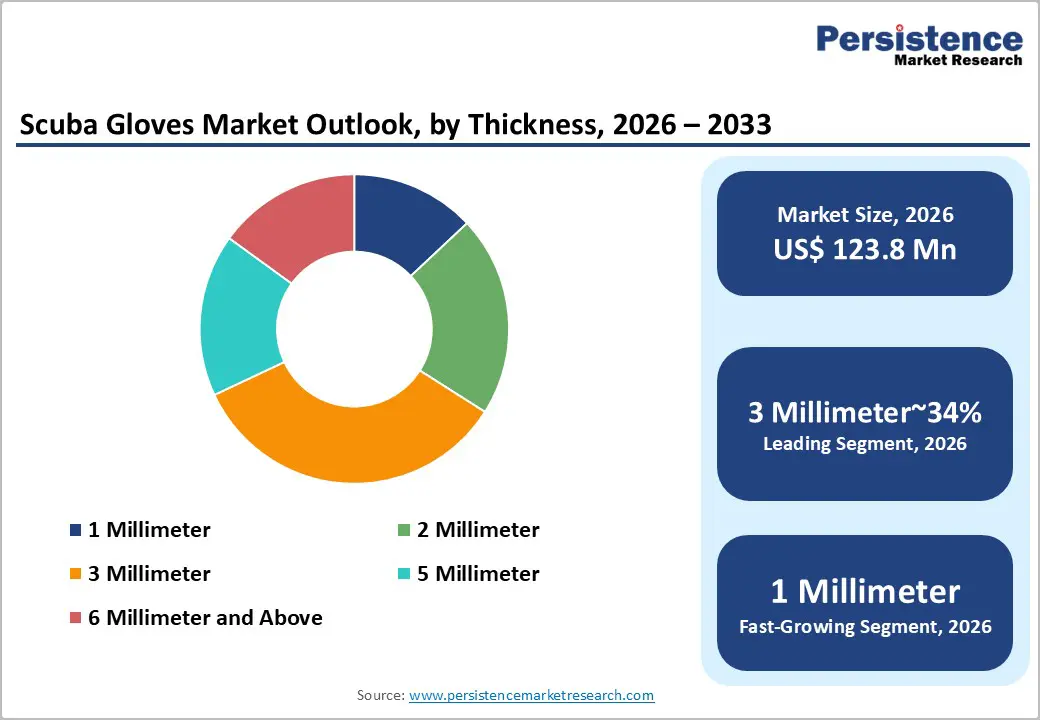

The global Scuba Gloves market size is likely to be valued at US$ 123.8 million in 2026 and is expected to reach US$ 182.5 million by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033. The market's steady growth is anchored in the global expansion of recreational scuba diving participation, rising adventure tourism spending, and continuous innovation in neoprene material technologies that improve thermal protection, flexibility, and durability.

Key Industry Highlights:

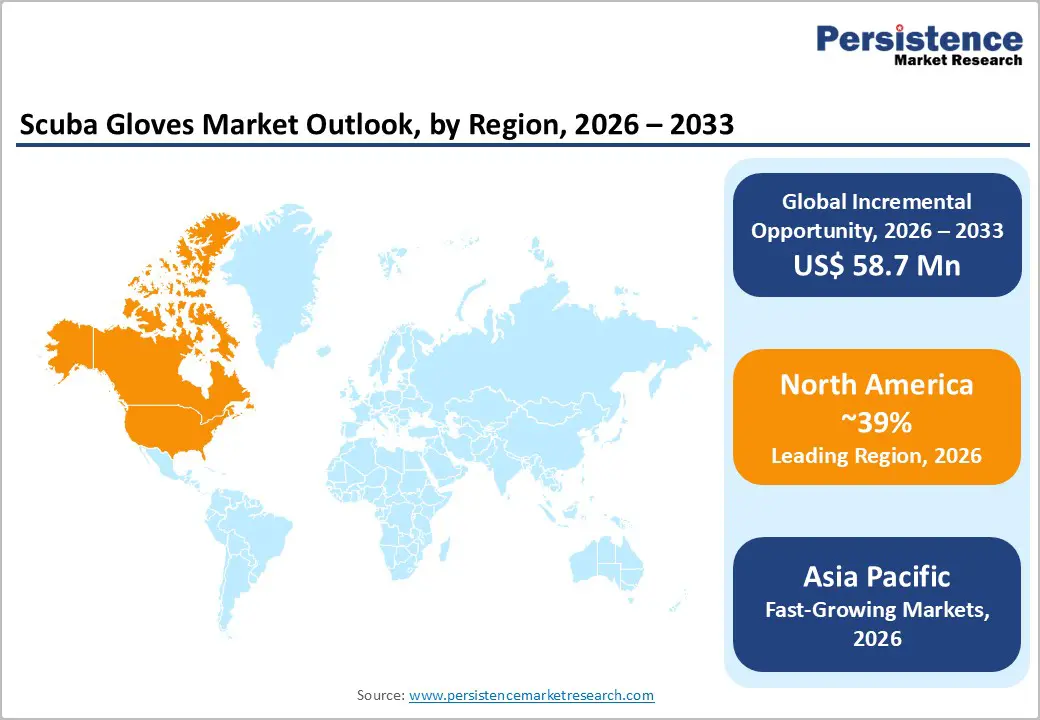

- Leading Region: North America leads the global Scuba Gloves market holding 39%, high per-capita equipment spending, a mature retail infrastructure, and the presence of leading global brands including Aqua Lung International, Henderson Aquatics, and XS Scuba.

- Fastest Growing Region: Asia Pacific is the fastest growing region with rising CAGR of 8.7%, driven by booming dive tourism, rapidly expanding middle-class participation in adventure sports, and the region's dual role as both the largest manufacturing base and one of the fastest-growing consumer markets for scuba equipment.

- Dominant Segment: The 3 Millimeter thickness segment dominates the Scuba Gloves market with approximately 34% revenue share, owing to its versatile thermal performance across the widest range of global dive water temperatures, making it the preferred default glove choice for recreational divers worldwide.

- Fastest Growing Segment: The Female end-user segment is the fastest growing category, supported by PADI's Women's Dive Day global campaign, targeted female certification programs across 6,600+ dive centers, and a rising female share in casual and recreational diving globally.

- Key Market Opportunity: The eco-diving tourism boom and growing demand for sustainable scuba gloves represent the most actionable market opportunity, with Gen Z divers willing to spend 10% more with sustainable operators, and brands such as Mares already launching recycled-rubber glove lines to capitalize on this accelerating consumer preference shift.

| Key Insights | Details |

|---|---|

|

Scuba Gloves Market Size (2026E) |

US$ 123.8 Million |

|

Market Value Forecast (2033F) |

US$ 182.5 Million |

|

Projected Growth CAGR (2026–2033) |

5.7% |

|

Historical Market Growth (2020–2025) |

4.9% |

Market Dynamics

Drivers - Global Expansion of Scuba Diving Participation and Certification Activity

The steadily growing global base of certified scuba divers remains the most fundamental and long-term demand driver for scuba gloves. Professional Association of Diving Instructors (PADI), the world’s largest diving certification agency, has issued more than 30 million certifications worldwide as of 2025 through its network of 128,000 professionals and 6,600 dive centers and resorts operating across 186 countries. A 2025 study conducted by Boston Consulting Group and commissioned by PADI found that PADI-exclusive dive shops achieved stronger year-over-year revenue growth, reflecting healthy commercial activity across the diving equipment ecosystem. Divers aged 30–40 account for the largest participation share at 39.7%, while the 20–30 age group is projected to grow at an 11.5% CAGR. This steady pipeline of newly certified divers, each requiring protective hand gear for training and recreational dives, creates consistent and recurring global demand for scuba gloves across all thickness categories.

Rising Demand for Cold-Water and Technical Diving Driving Premium Glove Adoption

Beyond beginner-level recreational diving, the rapid rise of cold-water, technical, wreck, and cave diving is driving strong demand for premium, high-thickness scuba gloves that provide superior thermal protection and enhanced grip. Cold-water environments, typically defined as temperatures below 15°C (59°F), require gloves made with 5mm or 6mm neoprene to ensure diver safety and performance. The global scuba diving equipment market was valued at approximately US$ 2.2 billion in 2025, with wetsuits and thermal protection gear contributing 42.6% of total equipment revenue. Leading brands such as Aqua Lung International and Cressi have expanded their premium glove portfolios to address this demand. Aqua Lung’s Thermocline range, for example, features triple-glued and blind-stitched seams in 3mm and 5mm neoprene options for enhanced insulation. This premiumization trend supports higher average selling prices and stronger margins for manufacturers globally.

Restraints - Seasonal and Geography-Dependent Demand Patterns Limiting Market Scalability

Demand for scuba gloves, particularly thicker 3mm, 5mm, and above variants, is highly seasonal and geographically concentrated, which limits consistent year-round revenue generation for manufacturers and distributors. Many tropical dive destinations require only 1mm or 2mm gloves, and in some cases, no gloves at all, reducing demand for higher-margin cold-water products. According to Diving Equipment & Marketing Association (DEMA), dive gear sales in the United States follow strong seasonal patterns tied to weather conditions and travel cycles, with most purchases concentrated in spring and summer. This seasonality creates inventory management challenges and increases working capital requirements, particularly for smaller distributors operating in single-climate markets. The uneven demand cycle also limits production planning efficiency and reduces economies of scale, making it more difficult for suppliers to maintain stable cash flows throughout the year across multiple geographic regions.

High Entry Cost of Scuba Diving as a Sport Limits New Participant Growth

The relatively high cost of entering scuba diving as a recreational activity restricts the pace of new participant growth, thereby limiting expansion of the addressable market for entry-level scuba gloves. Certification fees, equipment purchases, and travel expenses collectively create a significant financial barrier. According to DEMA industry data, average U.S. dive centers issued only 128 entry-level certifications in 2023, down from 154 in 2022, with 32% of agencies reporting declines.

Basic open-water certification through agencies such as the Professional Association of Diving Instructors typically costs between US$ 300 and US$ 600, excluding equipment expenses. This upfront investment disproportionately affects younger consumers and individuals in emerging markets. As a result, the slower pace of new diver acquisition moderates long-term growth in demand for beginner-level gloves and related entry-tier equipment across global markets.

Opportunity - Growing Female and Youth Diver Segments as Untapped Demand Pools

The rising participation of women and youth in scuba diving presents a significant and underpenetrated growth opportunity for scuba glove manufacturers. Historically, male divers have represented 60–65% of certified divers; however, women now account for approximately 40% of casual divers compared to 35% within the core diver base. The Professional Association of Diving Instructors has actively promoted inclusion through initiatives such as Women’s Dive Day, conducted across its 6,600+ dive centers worldwide.

Between 2015 and 2020, PADI’s male-to-female membership ratio averaged 63% to 37%, with female participation steadily increasing. Manufacturers that introduce ergonomically designed gloves tailored for women, along with youth-specific sizing and features, can capture incremental demand from these growing segments. As younger divers and female participants expand across global markets, targeted product innovation and inclusive branding strategies can unlock sustainable long-term growth opportunities for glove suppliers.

Eco-Diving Tourism Boom and Sustainable Product Innovation Creating New Market Differentiation

The global rise of eco-diving tourism and marine conservation-focused travel is creating a premium growth opportunity for scuba glove manufacturers investing in sustainable materials and environmentally responsible production. Condé Nast Traveller identified eco-diving with the Professional Association of Diving Instructors as one of the top travel trends for 2024. PADI reports that Gen Z divers are willing to pay up to 10% more to dive with verified sustainable operators, and this preference extends to equipment purchases.

In January 2024, Mares announced a partnership with a sustainable materials supplier to develop scuba gloves made from recycled rubber compounds. Companies adopting bio-based neoprene alternatives, recyclable packaging, and transparent supply chain certifications can differentiate in the premium segment and command higher price points among environmentally conscious consumers driving certification growth.

Category-wise Analysis

By Thickness Insights

Among all thickness categories, the 3 millimeter neoprene scuba glove segment holds the largest share in the global Scuba Gloves market, accounting for approximately 34% of total revenue. The 3mm thickness sits in the ideal mid-range of the product spectrum, offering a strong balance between thermal insulation for water temperatures of 10°C to 18°C (50°F to 65°F) and the flexibility required to handle dive equipment comfortably underwater. This balance makes it the preferred option for most recreational divers worldwide.

It performs effectively across temperate dive regions such as the Mediterranean, Pacific, and Atlantic, which together represent a substantial portion of global dive activity. Product portfolios from leading brands such as Aqua Lung International and Cressi show that 3mm and 5mm gloves form the core of their offerings, with 3mm models typically generating the highest unit volumes and SKU diversity. Its adaptability for both tropical and mild cold-water conditions makes it especially attractive for traveling divers seeking one reliable, all-purpose glove.

By Size Insights

The large size segment leads the global scuba gloves market by size category, capturing approximately 30% of total revenue. This leadership closely reflects the demographic structure of the global diving population. Adult males aged 30 to 40 represent the largest share of active divers, accounting for nearly 39.7% of the diver base, and most divers in this group require medium to large glove sizes.

As a result, manufacturers prioritize production of Large sizes, enabling higher production volumes, stronger economies of scale, and wider retail availability compared to more specialized sizes such as Small or Extra Extra Large. Major brands, including Aqua Lung, Henderson Aquatics, and XS Scuba, typically introduce their most advanced features, such as reinforced palms and upgraded closure systems, first in the Large size range. While Large remains dominant, demand for Extra Large and Extra Extra Large gloves is rising steadily as male diver demographics continue to expand across global markets.

By Closure Type Insights

The Full Wrist Strap closure segment represents the leading category in the Scuba Gloves market, accounting for approximately 38% of total revenue. This closure design is widely preferred because it significantly reduces water entry by creating a firm and adjustable seal around the wrist. Minimizing water flush-through is especially important in cold-water diving, where heat retention directly affects diver comfort and safety. Leading manufacturers, including Aqua Lung International, incorporate adjustable full wrist strap systems into their premium glove models to enhance insulation performance during extended dives. The design also allows seamless integration with wetsuit and drysuit cuffs, which is a critical requirement for technical and commercial divers. Product development trends from brands such as Cressi and Henderson Neosport show that full wrist straps are increasingly combined with ergonomic, pre-curved finger construction to reduce hand fatigue. This combination of performance, comfort, and adaptability reinforces the segment’s premium positioning and market leadership.

By End User Insights

The male end-user segment is the clear market leader in the global Scuba Gloves industry, accounting for approximately 58% of total revenue. Male divers represent between 60% and 65% of the global certified recreational diver population and generally demonstrate higher spending on specialized and technical diving equipment. They are more actively involved in demanding disciplines such as wreck diving, cave diving, commercial diving, and underwater research, where high-performance gloves in 5mm and 6mm+ thickness categories are commonly required.

Studies commissioned by leading industry organizations confirm that male divers continue to dominate scuba equipment purchasing decisions worldwide. However, the Female segment is emerging as the fastest-growing end-user category. Initiatives such as Women’s Dive Day and targeted certification campaigns are successfully encouraging female participation across various age groups. This shift is gradually expanding the customer base and creating new opportunities for brands to design more inclusive product lines.

Regional Insights

North America Scuba Gloves Market Trends

The United States leads the North American Scuba Gloves market, supported by the world’s largest concentrated base of certified recreational divers. The country has approximately 2.6 million active scuba divers, and annual diving-related spending is substantial, with California alone generating between US$ 161 million and US$ 323 million in dive expenditures. The broader U.S. marine economy contributes significantly to national GDP, highlighting the economic importance of marine recreation activities such as scuba diving.

Regulatory oversight from ASTM International and the U.S. Consumer Product Safety Commission ensures product safety and quality standards for dive equipment manufacturers. Innovation remains a defining feature of the region, with brands like Aqua Lung International, Henderson Aquatics, and XS Scuba investing in advanced neoprene materials, ergonomic designs, and sustainable packaging. Canada further supports regional demand, particularly for 5mm and 6mm+ gloves suited for colder Pacific and Atlantic coastal waters.

Europe Scuba Gloves Market Trends

Europe represents a mature and well-established market for scuba gloves, with strong demand across Spain, France, Italy, the United Kingdom, and Germany. Mediterranean destinations such as Spain and France attract significant domestic and international dive tourism, supporting consistent equipment sales. In contrast, the United Kingdom drives demand for thicker 5mm and 6mm+ gloves due to colder diving conditions in the North Sea and Atlantic waters. Market surveys across Western Europe indicate positive revenue expectations among dive instructors, signaling steady regional growth in dive gear sales.

The regulatory framework under the European Union, including CE marking requirements and REACH chemical compliance standards, shapes material selection and manufacturing processes for neoprene gloves. Certification agencies such as SSI are expanding across the region, increasing diver certifications and equipment demand. Additionally, sustainability-focused consumers in Germany and Scandinavia are encouraging brands to introduce eco-friendly and recycled-material glove lines.

Asia Pacific Scuba Gloves Market Trends

Asia Pacific is the fastest-growing regional market for scuba gloves, driven by expanding dive tourism across Indonesia, Thailand, the Philippines, Malaysia, and Australia. These countries host some of the world’s most recognized dive destinations, attracting international divers and supporting strong equipment sales. Certification programs are widely accepted across Southeast Asia, enabling smooth travel and repeat dive participation.

China is emerging as both a manufacturing powerhouse and a growing consumer market, supported by rising middle-class interest in adventure tourism. Japan maintains steady domestic demand through established diving communities in Okinawa and other coastal regions. The region also serves as the primary production hub for competitively priced scuba gloves, with manufacturers in Taiwan, China, and South Korea supplying global markets. India is developing as an emerging growth market, supported by expanding dive tourism in the Andaman and Nicobar Islands and Lakshadweep, positioning Asia Pacific for sustained growth.

Competitive Landscape

The global scuba gloves market demonstrates a moderately concentrated competitive structure, with leading players such as Aqua Lung International, Cressi, Henderson Aquatics, Mares, and ScubaPro collectively accounting for over 60% of total market revenue. Competition is driven by technological differentiation, including advanced neoprene formulations, glued-and-blind-stitched seams, liquid-sealed construction, ergonomic pre-curved designs, and integrated wrist closure systems. These features directly impact product durability, comfort, and thermal efficiency, which are key purchasing factors for divers.

Established brands are increasingly focusing on sustainable sourcing practices and eco-friendly product lines to meet evolving consumer expectations. At the same time, emerging Asia Pacific manufacturers are intensifying competition in the mid-range and value segments through cost-efficient production models. The growing adoption of direct-to-consumer digital sales channels is also reshaping the market, enabling brands to enhance margins, strengthen customer engagement, and build loyal diving communities worldwide.

Key Developments:

- In January 2024, Mares formed a strategic collaboration with a major sustainable materials supplier to create an eco-friendly scuba glove range made from recycled rubber, aiming to capture interest from environmentally conscious divers and strengthen its sustainability credentials in the dive gear category.

- In March 2024: Fourth Element introduced its “X-Flex” neoprene glove series, delivering 50% more stretch and enhanced thermal insulation for extreme cold-water diving, expanding its technical glove portfolio and appealing to professional and adventure divers seeking high-performance gear.

- In August 2023: Henderson Aquatics reported a 10% year-over-year increase in premium business-application dive glove sales, driven by stronger demand from commercial diving, marine research, and underwater industrial sectors - highlighting robust B2B growth alongside recreational market expansion.

Companies Covered in Scuba Gloves Market

- Aqua Lung International

- Baresports Company

- UTD International, Inc.

- Waterproof USA

- Henderson Aquatics Inc.

- AKONA

- Henderson Neosport

- XS Scuba

- Cressi

- AROPEC SPORTS CORP.

- Divtop

- Possess Sea Industrial Co., Ltd.

- Scuba Gear Canada

- UNIQUE SAFETY SERVICES

- Planet Scuba India

- Mares (Head Sport GmbH)

- ScubaPro (Johnson Outdoors)

- Fourth Element

- Hollis

- Beuchat

Frequently Asked Questions

The global Scuba Gloves Market is valued at US$ 123.8 Million in 2026 and is projected to reach US$ 182.5 Million by 2033, expanding at a CAGR of 5.7% during the forecast period. The market recorded a historical CAGR of 4.9% between 2020 and 2025, reflecting steady growth supported by expanding global diver participation and product innovation.

The primary demand drivers include the continuous global expansion of certified scuba divers, with PADI having issued over 30 million certifications across 186 countries, rising cold-water and technical diving activity driving premium glove adoption, and growing eco-diving tourism trends. Material innovations in neoprene formulations offering improved flexibility, thermal retention, and grip performance further support market growth.

The 3 Millimeter thickness segment leads the Scuba Gloves market with approximately 34% of total revenue, owing to its optimal balance between thermal insulation for water temperatures of 10°C to 18°C and dexterity for operating dive equipment. Its versatility across the broadest range of global dive conditions makes it the default choice for recreational divers worldwide.

North America, led by the United States, is the dominant region in the global Scuba Gloves market, supported by approximately 2.6 million active scuba divers, high consumer spending on dive equipment, and the presence of leading brands such as Aqua Lung International and Henderson Aquatics. The U.S. marine economy contributed US$ 432 Billion to national GDP in 2021, reflecting the market's deep commercial foundation.

The most significant emerging opportunity lies at the intersection of eco-diving tourism and sustainable product innovation. With Gen Z divers willing to pay 10% more for environmentally responsible diving products and Condé Nast Traveller naming eco-diving the travel trend for 2024, manufacturers that develop eco-certified scuba gloves, as Mares is doing with its recycled-rubber product line, can command premium pricing and capture disproportionate share of the fastest-growing diver demographic.