- Food Ingredients & Additives

- Saffron Market

Saffron Market Size, Share, and Growth Forecast 2026 - 2033

Saffron Market by Grade (Grade I, Grade II, Grade III, Grade IV), Form (Stigma, Powder, Liquid, Petals, Stamen), Application (Food & Beverages, Pharmaceuticals, Cosmetics & Personal Care), Distribution Channel (B2B, B2C), and Regional Analysis, 2026 - 2033

Saffron Market Size and Trend Analysis

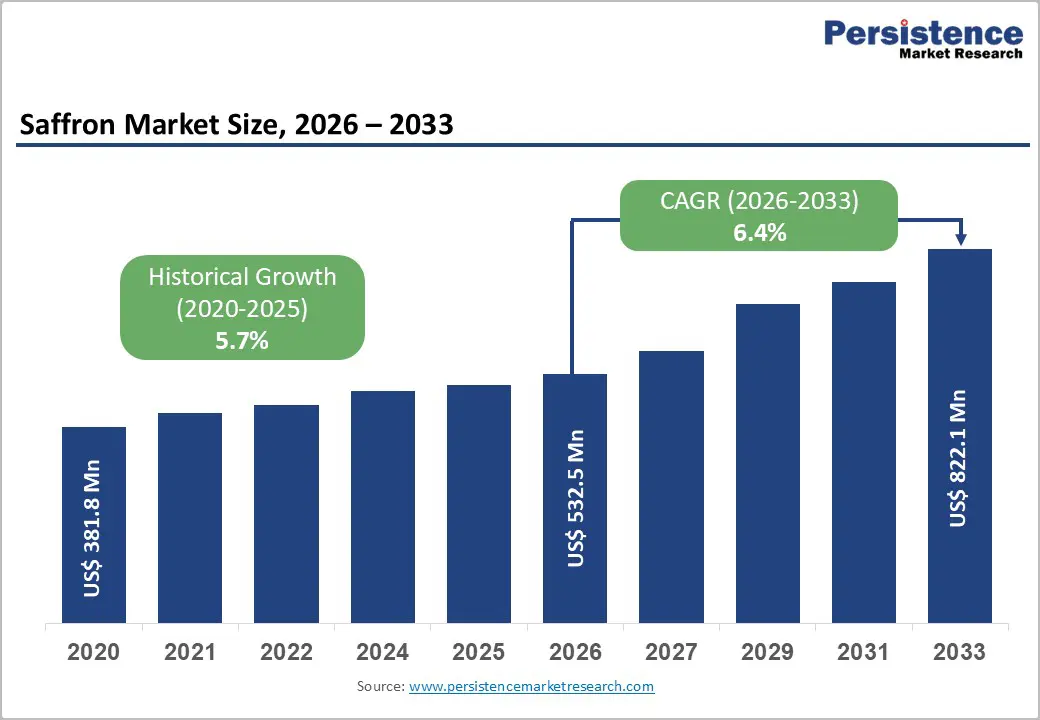

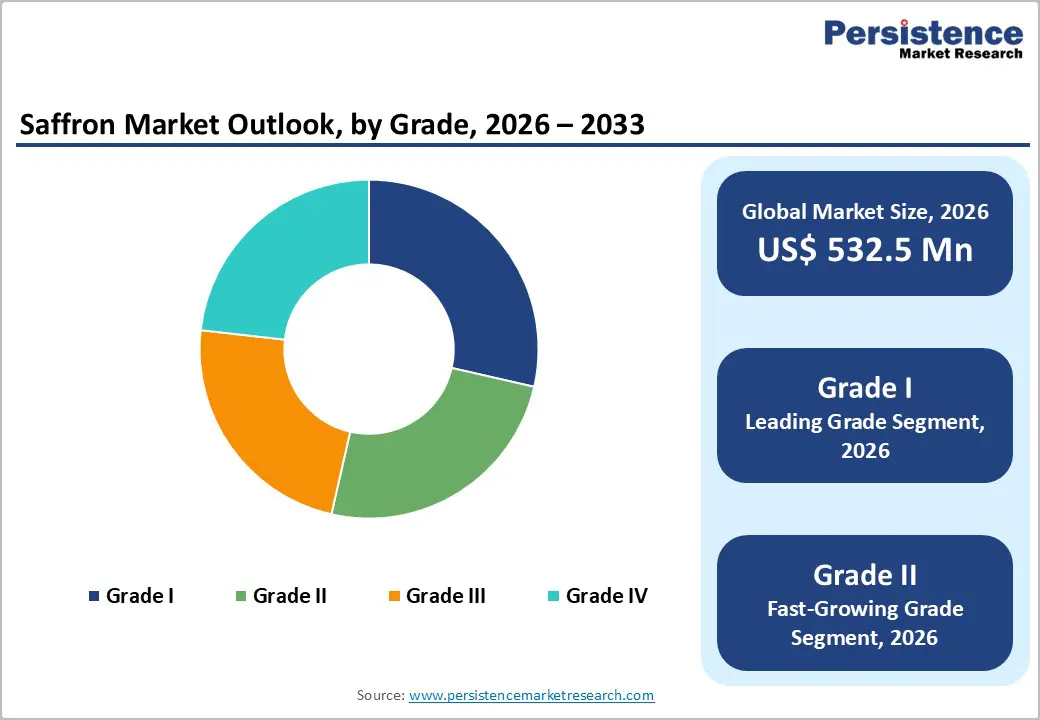

The global saffron market size is likely to value at US$ 532.50 million in 2026 and is projected to reach US$ 822.07 million by 2033 at a CAGR of 6.4% in the forecast period advancing on a steady commercial trajectory, propelled by rising demand across food, pharmaceutical, and premium beauty applications. This expansion reflects growing consumer awareness of saffron's functional health benefits, accelerating premiumization in global culinary culture, and the deepening integration of saffron-derived compounds into nutraceutical and cosmeceutical formulations.

Key Industry Highlights:

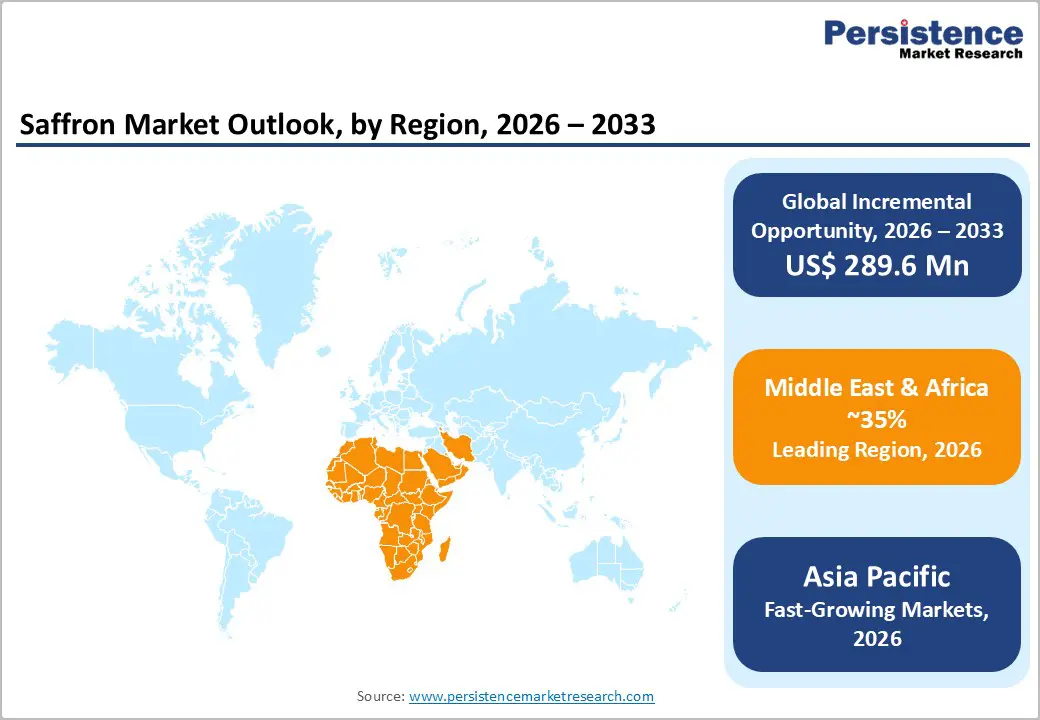

- Leading Region: Middle East & Africa leads the saffron market with 35% share, driven by strong cultural, culinary, and hospitality-driven demand across GCC countries.

- Fast-Growing Market: Asia Pacific is the fastest-growing market expanding at a CAGR of 8.3% due to the growing demand for food, cosmetics, and pharmaceuticals.

- Leading Category: Grade I saffron dominates with 52% share, supported by strong preference for high-purity, ISO 3632-certified products across food, pharmaceutical, and export markets.

- Fastest Growing Application Category: Cosmetics & personal care is the fastest growing segment, fueled by rising demand for saffron-based bioactive ingredients in skincare and beauty formulations.

- Key Opportunity: Expansion of pharmaceutical-grade saffron extracts in cognitive health nutraceuticals presents the most promising growth opportunity through 2033.

Market Dynamics

Drivers - Rising Consumer Demand for Natural, Functional Ingredients Across Food and Health Categories

The most powerful force shaping the saffron sector today is the global pivot toward natural, bioactive ingredients that deliver both sensory and therapeutic value. Consumers across North America, Europe, and Asia Pacific are actively selecting food products, dietary supplements, and personal care items formulated with botanicals carrying documented health credentials. Saffron, with its clinically studied antioxidant, anti-depressant, and anti-inflammatory properties, fits this profile precisely and has emerged as a premium compliant alternative across multiple categories.

Regulatory bodies in the European Union and the United States have progressively tightened restrictions on synthetic colorants and flavour enhancers, reinforcing saffron's commercial relevance for food manufacturers. The clean-label movement has accelerated procurement of natural spice-based ingredients by an estimated 18% between 2022 and 2025 across major food and beverage manufacturers globally, anchoring long-term demand visibility for the saffron market.

Expanding Pharmaceutical and Nutraceutical Applications of Saffron-Derived Compounds

The pharmaceutical sector's growing recognition of saffron's active constituent, crocin, as a clinically relevant compound for cognitive health and mood regulation has materially expanded the saffron market's addressable demand base. Peer-reviewed clinical trials have demonstrated saffron extract's efficacy in managing mild-to-moderate depression, anxiety, and age-related cognitive decline, prompting nutraceutical brands to accelerate product launches featuring standardised saffron extract formulations across regulated markets.

The global nutraceuticals market surpassed US$ 400 Billion in value by 2024, and saffron-based functional formulations represent one of its fastest-integrating natural inputs. This pharmaceutical pull effect diversifies the saffron demand base well beyond traditional culinary channels, embedding the ingredient within high-margin therapeutic and wellness portfolios and supporting sustained saffron market growth throughout the 2026 - 2033 forecast period.

Restraints - Supply Concentration and Climate Vulnerability of Saffron-Producing Regions

The most structurally significant constraint on saffron market growth is the extreme geographic concentration of production, with Iran alone accounting for approximately 80-90% of global saffron output. This dependence on a narrow cultivation base exposes the entire saffron supply chain to disruption from climate variability, including the erratic rainfall patterns and temperature fluctuations increasingly documented across the Iran-Afghanistan cultivation belt over the past several harvest cycles.

When seasonal yield declines occur as observed notably in 2021 and 2023 wholesale prices spike sharply, squeezing downstream manufacturers' margins and disrupting long-term procurement contracts. The inability to rapidly scale cultivation in alternative geographies, combined with saffron's labour-intensive harvesting requirements, implies this supply-side vulnerability will continue to act as a persistent ceiling on volume growth and price predictability.

Prevalence of Adulteration and Counterfeiting Eroding Consumer Confidence

Saffron is among the world's most adulterated spices, and the persistent presence of fraudulent or diluted product in global supply chains constitutes a material restraint on saffron market share expansion, particularly in retail and e-commerce channels. A significant proportion potentially exceeding 30% of commercially available saffron products in some markets contain adulterants such as safflower, turmeric, or synthetic dyes, undermining buyer confidence and depressing willingness-to-pay premiums.

Regulatory enforcement remains inconsistent across key importing markets, and the analytical cost of ISO-grade authentication deters smaller buyers from robust verification practices. This quality assurance gap creates reputational risk for the broader saffron industry and constrains the market's ability to convert casual buyers into loyal, high-value repeat purchasers, particularly within fast-growing e-commerce and direct-to-consumer retail formats.

Opportunities - Premiumization of Saffron in the Luxury Food Service and Fine Dining Segment

The fine dining and luxury food service sector presents a high-value, structurally underserved opportunity for saffron suppliers and branded product developers to capture margin-rich revenue. As Michelin-starred restaurants and premium hospitality groups across Europe, the Gulf Cooperation Council, and urban Asia intensify their sourcing of traceable, origin-certified specialty ingredients, saffron particularly Grade I PDO-certified varieties occupies a uniquely defensible premium position within the chef-driven procurement landscape.

Producers should prioritise investment in origin authentication technology and direct-to-chef distribution models to eliminate intermediary margin dilution and build direct brand equity. The luxury food service market is expanding at approximately 9% annually in key urban markets, and saffron suppliers who establish verifiable provenance credentials today are positioned to lock in exclusive supplier relationships before the competitive window narrows, with the window before 2027 being particularly time-sensitive.

Saffron Extract Integration in Cosmetics and High-Performance Skincare Formulations

The cosmetics and personal care industry's rapid pivot toward bioactive, botanical actives creates a compelling and time-sensitive growth channel for saffron extract suppliers. Saffron's documented brightening, antioxidant, and anti-inflammatory skin benefits align directly with the dominant "skinification" trend reshaping premium skincare globally, prompting major cosmetics houses in South Korea, France, and the United Arab Emirates to actively source standardised saffron extracts for serums, masks, and complexion-targeting treatments.

The global active cosmetics ingredient market is expanding at a CAGR exceeding 7%, and saffron-derived compounds remain meaningfully underpenetrated relative to their functional profile. Suppliers who can deliver consistent extract standardisation, regulatory compliance documentation, and scale capacity are best positioned to capture long-term offtake agreements with tier-one cosmetics manufacturers, with cosmetics-grade saffron extract commanding significant value premiums over culinary-grade product.

Category-wise Analysis

Grade Insights

Grade I commands the dominant position in the saffron market, holding approximately 52% of total market share, reflecting the premium end-user preference for highest-purity, ISO 3632-certified saffron across food service, pharmaceutical, and export-grade applications. This structural dominance persists because institutional buyers, including nutraceutical manufacturers, luxury food producers, and pharmaceutical formulators, consistently specify Grade I in procurement contracts to meet regulatory and quality benchmarks set across regulated import markets.

The fastest growing segment is Grade II, as mid-market food manufacturers and emerging-market retailers seek the functional and sensory benefits of saffron at accessible price points without the premium associated with top-tier certification. The Grade II segment's expansion also reflects growing saffron market demand from quick-service restaurants and packaged food producers scaling saffron-flavoured SKUs across Asia and the Middle East.

Form Insights

Stigma the whole dried threads of the saffron crocus holds the leading position in the saffron market by form, capturing approximately 38% of market share, driven by its strong association with authentic premium quality and its dominance across culinary, pharmaceutical, and specialty retail channels. Whole stigma commands the highest unit price and remains the preferred form for professional food service buyers and premium consumers who use visual thread quality as a proxy for purity and potency.

The fastest growing form segment is Stamen, which is gaining commercial traction as an economical ingredient input for extract manufacturers, cosmetics formulators, and functional beverage producers requiring consistent bioactive concentration rather than aesthetic thread presentation. Powder and liquid forms continue to grow steadily within food processing and nutraceutical applications, while petals historically a lower-value byproduct are attracting interest from herbal tea and wellness product developers.

Application Insights

Food & beverages retains the largest application share in the saffron market at approximately 41%, underpinned by saffron's centuries-deep integration into culinary traditions across the Middle East, South Asia, Europe, and North Africa, alongside its growing adoption in premium packaged foods, artisan dairy, and specialty beverages. The application's dominance is reinforced by the structural weight of the global food processing industry and the continuing expansion of ethnic cuisine consumption across Western markets.

The fastest growing application segment is cosmetics & personal care, where saffron's multi-functional bioactive profile encompassing skin brightening, antioxidant protection, and anti-inflammatory action is driving accelerating formulation activity among leading beauty brands. The pharmaceuticals segment is also advancing steadily, supported by clinical evidence for saffron extract's neurological and metabolic health applications, confirming that application diversification remains a key structural strength reducing revenue concentration risk.

Distribution Channel Insights

The B2B distribution channel overwhelmingly dominates saffron market revenue, accounting for approximately 87% of total market share, reflecting the bulk procurement model that characterises the saffron supply chain from producing regions to food manufacturers, pharmaceutical companies, and cosmetics formulators. B2B relationships in the saffron sector are characterised by long-term contract structures, quality certification requirements, and volume-based pricing, which collectively concentrate revenue within this channel.

The fastest growing channel is B2C, accelerated by the expansion of direct-to-consumer e-commerce platforms, branded saffron retail packaging, and subscription wellness services introducing premium saffron directly to end consumers. As consumer awareness of saffron's health benefits grows particularly in North America and Europe the B2C channel is structurally positioned to gain share through the forecast period, with digital commerce removing traditional geographic barriers to premium retail access.

Regional Insights

Middle East & Africa Saffron Market Trends and Insights

Middle East & Africa leads the global saffron market, holding approximately 35% of total market share, a position underpinned by deep cultural, culinary, and religious saffron traditions across the Arabian Peninsula, North Africa, and the Iranian cultural sphere. GCC countries particularly Saudi Arabia and the UAE drive premium consumption, while the region also functions as a major transit and re-export hub for Iranian and Afghan saffron entering global markets.

- Iran Saffron Market Size

Iran is the global epicentre of saffron production, accounting for approximately 80-90% of worldwide saffron output, with cultivation concentrated in the Khorasan provinces. Domestically, saffron carries deep culinary, medicinal, and cultural significance, sustaining robust internal consumption across traditional cuisine, herbal medicine, and ceremonial use. Iran's saffron market is structurally export-oriented, with state-supported trade infrastructure and emerging value-added processing capacity reinforcing its dominant position in the coming years.

- Saudi Arabia Saffron Market Size

Saudi Arabia commands approximately 33% of Middle East & Africa saffron market revenue, making it the region's single largest national market. Deep culinary tradition where saffron is essential in iconic dishes such as kabsa and saffron-infused coffee and a high-income urban population sustain structurally strong demand. Vision 2030's food sector development agenda and premium retail expansion across Riyadh and Jeddah will reinforce growth through 2033.

- UAE Saffron Market Size

The UAE accounts for approximately 20% of Middle East & Africa saffron market revenue and occupies a strategically distinctive position as both a high-income retail centre and a major international saffron trading and re-export hub. Dubai's entrepôt role places the UAE at the intersection of domestic consumption and global commodity flows, while luxury hospitality and health-conscious urban consumers sustain premium demand growth above the regional average through 2033.

Asia Pacific Saffron Market Trends and Insights

Asia Pacific is poised as the fast growing in the global saffron market, projected to expand at a CAGR of 8.3% through 2033. Growth is propelled by an expanding middle-class base, deep traditional saffron use in Ayurvedic and Persian-origin cuisines, and explosive premium beauty market growth across China, Japan, and South Korea. India's emerging cultivation activity in Kashmir adds a strategically significant supply-side dimension to the region's importance.

- India Saffron Market Size

India accounts for an estimated 35-40% of Asia Pacific saffron market revenue, holding a dual role as the world's second-largest producer centred in Jammu & Kashmir's Pampore region and a major domestic consumer driven by Ayurvedic, religious, and culinary use. Government initiatives, including GI tagging of Kashmir saffron and the National Saffron Mission, are strengthening production standards and export positioning meaningfully above the regional average.

- China Saffron Market Size

China accounts for approximately 20-25% of Asia Pacific saffron market revenue and is emerging as one of the most strategically significant growth markets globally. Traditional Chinese Medicine has long incorporated saffron for circulatory and mood applications, providing a culturally embedded demand foundation. China's rapidly growing premium beauty sector is integrating saffron extract into luxury skincare lines at accelerating pace, supported by rising import volumes from Iran and Spain.

North America Saffron Market Trends and Insights

North America represents a structurally growing saffron market, propelled by rising consumer interest in ethnic cuisines, premium natural ingredients, and functional wellness products. Demographic diversification across South Asian, Middle Eastern, and Mediterranean diaspora communities sustains baseline demand, while mainstream premiumisation drives incremental volume. The North American saffron market is positioned to expand above the global average rate through 2033 as clean-label and functional ingredient trends deepen.

- United States Saffron Market Size

The United States captures approximately 75-78% of total North American saffron market revenue, making it the region's dominant demand centre by a significant margin. Demand is fuelled by both culinary adoption in premium food service and rapid growth in dietary supplements featuring saffron extract for mood and cognitive wellness. The country's well-developed natural products retail and e-commerce infrastructure provides efficient distribution pathways through 2033.

Competitive Landscape

The global saffron market exhibits a moderately fragmented competitive landscape, characterized by the presence of origin-based cultivators, specialty exporters, and integrated agri-processors. Competition is primarily driven by quality assurance standards, certification compliance, and traceability across the supply chain, as buyers increasingly prioritize authenticity, purity, and consistent grading in procurement decisions.

Geographic origin branding and premium certifications such as ISO and organic labeling remain key differentiators for market participants. Strategic consolidation is gradually emerging as players seek stronger control over sourcing networks. Meanwhile, the rise of digital retail channels is intensifying competition by enabling niche brands while increasing price transparency across global markets.

Key Market Developments

- In March 2024, Rumi Spice expanded its direct-sourcing network in Afghanistan's Herat Province, deepening partnerships with smallholder saffron farming cooperatives to scale certified-premium supply capacity and strengthen its ethical sourcing narrative for North American and European B2B buyers.

- In September 2024, Saharkhiz Saffron launched a new line of pharmaceutical-grade saffron extract products targeting European nutraceutical manufacturers, positioning the company to capitalise on growing clinical demand for standardised crocin-content extracts in the cognitive health supplement segment.

- In January 2025, Kashmir Box accelerated its B2C e-commerce strategy by introducing a GI-certified Kashmir Saffron subscription service targeting premium household consumers in the United States and United Kingdom, leveraging the Kashmir saffron GI tag as a key differentiator in an increasingly quality-conscious retail market.

Companies Covered in Saffron Market

- Gohar Saffron

- Tarvand Saffron

- Saharkhiz Saffron

- Rowhani Saffron

- Royal Saffron Company

- Rumi Spice

- Kashmir Box

- Baby Brand Saffron

- Mehr Saffron

- Esfedan Saffron

- Novin Saffron

- Azafranes Jiloca

- La Mancha Foods

- Zamouri Spices

- Saffron Business Co

- Kesar King

- Taj Mahal Saffron

- Golden Saffron (US)

- Saffron King Business Co

- Iran Saffron Company

Frequently Asked Questions

The Saffron market is valued at US$ 532.50 Million in 2026 and is projected to reach US$ 822.07 Million by 2033, growing at a CAGR of 6.4% driven by rising demand for natural, bioactive ingredients.

Market growth is driven by increasing clean-label demand and expanding clinical validation of saffron’s cognitive and health benefits boosting pharma and nutraceutical adoption.

Grade I saffron leads with 52% share due to strict quality requirements in pharmaceutical, food service, and export markets ensuring consistent demand.

Middle East & Africa dominates with 35% share due to strong cultural usage and its role as a key global trading and re-export hub.

The biggest opportunity lies in pharmaceutical-grade saffron extracts for cognitive health nutraceuticals amid rising global demand and evolving regulations.

The leading companies in saffron include Saharkhiz Saffron, Gohar Saffron, Rumi Spice, Rowhani Saffron, Royal Saffron Company, Kashmir Box, Azafranes Jiloca, and La Mancha Foods.