- Nutraceuticals & Functional Foods

- RUTF & RUSF Market

RUTF & RUSF Market Size, Share, and Growth Forecast, 2025 - 2032

RUTF & RUSF Market By Product Type (RUTF, RUSF, Others), Formulation (Standard Peanut & Milk Recipes, Low-Milk Or Milk-Free Variants, Others), End-user and Regional Analysis for 2025 - 2032

RUTF & RUSF Market Size and Trends Analysis

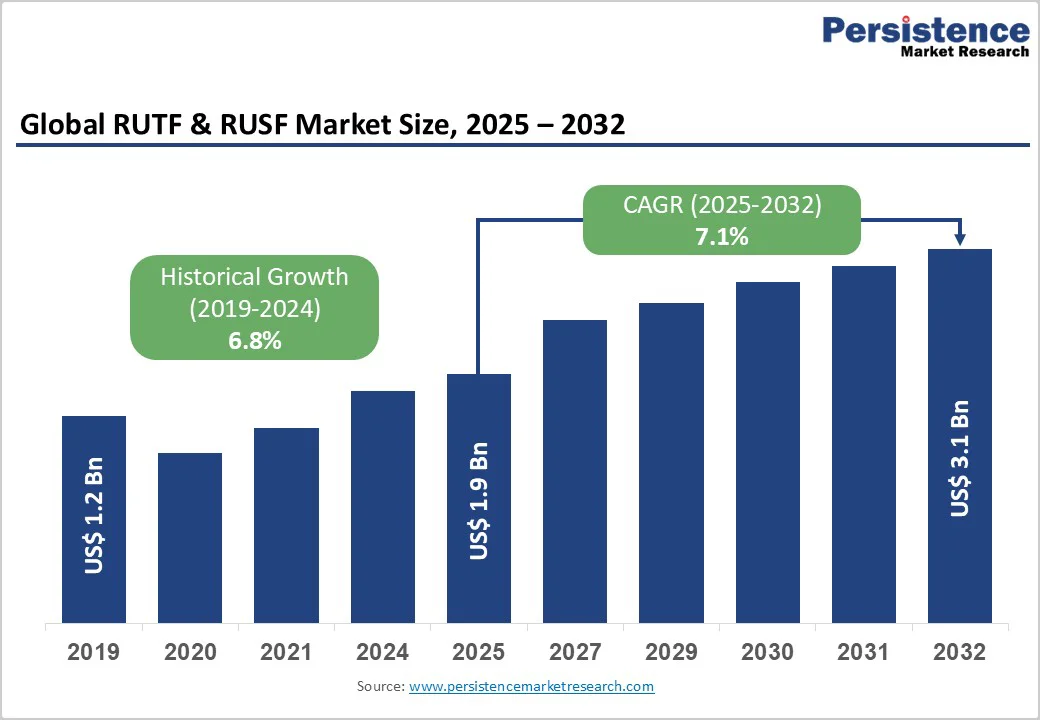

The global RUTF & RUSF market size is likely to be valued at US$1.9 billion in 2025. It is expected to reach US$3.1 billion by 2032, growing at a CAGR of approximately 7.1% during the forecast period from 2025 to 2032. Increasing donor funding volatility, a higher incidence of humanitarian crises, large procurement volumes, and expanding local manufacturing capacity are the primary growth drivers.

Supply-side constraints such as raw-material inflation, logistics challenges, and regulatory and quality-assurance requirements moderate growth. The market is mission-driven (humanitarian and public programs) and is increasingly commercializing and developing local industry.

Key Industry Highlights

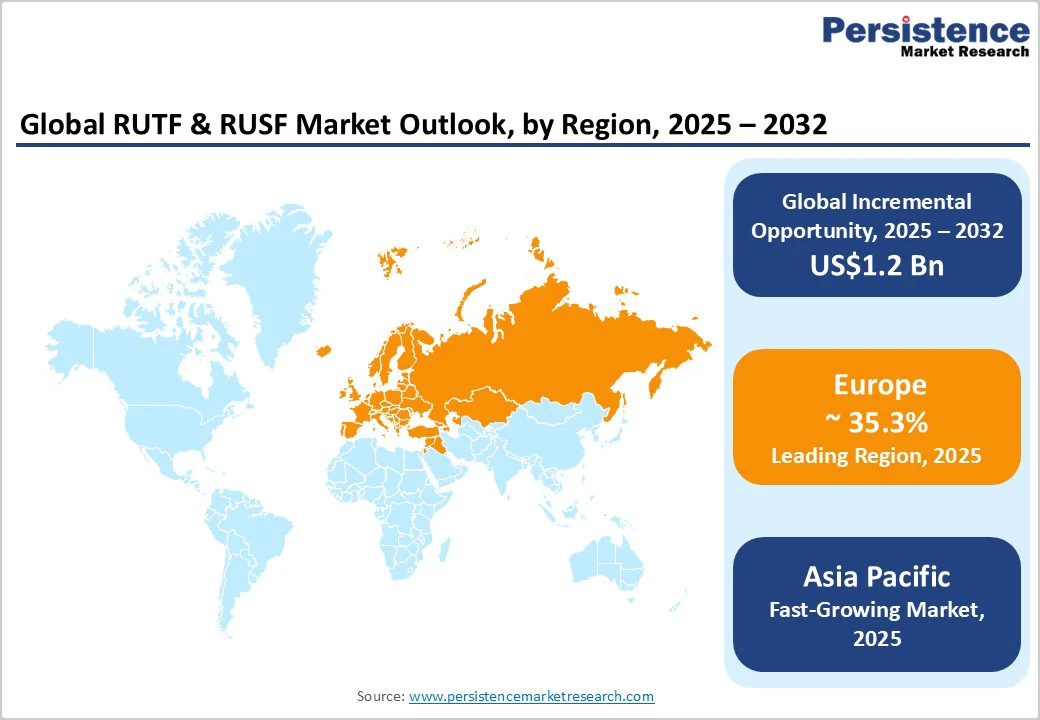

- Leading Region: Europe accounts for the largest share of global therapeutic food production, representing 35.3% of total output value, driven by established manufacturing capacity, stringent quality systems, and strong participation in institutional tenders.

- Fastest-growing Region: Asia Pacific is the fastest-expanding regional market, supported by new production facilities, competitive access to raw materials, and scaling government nutrition programs.

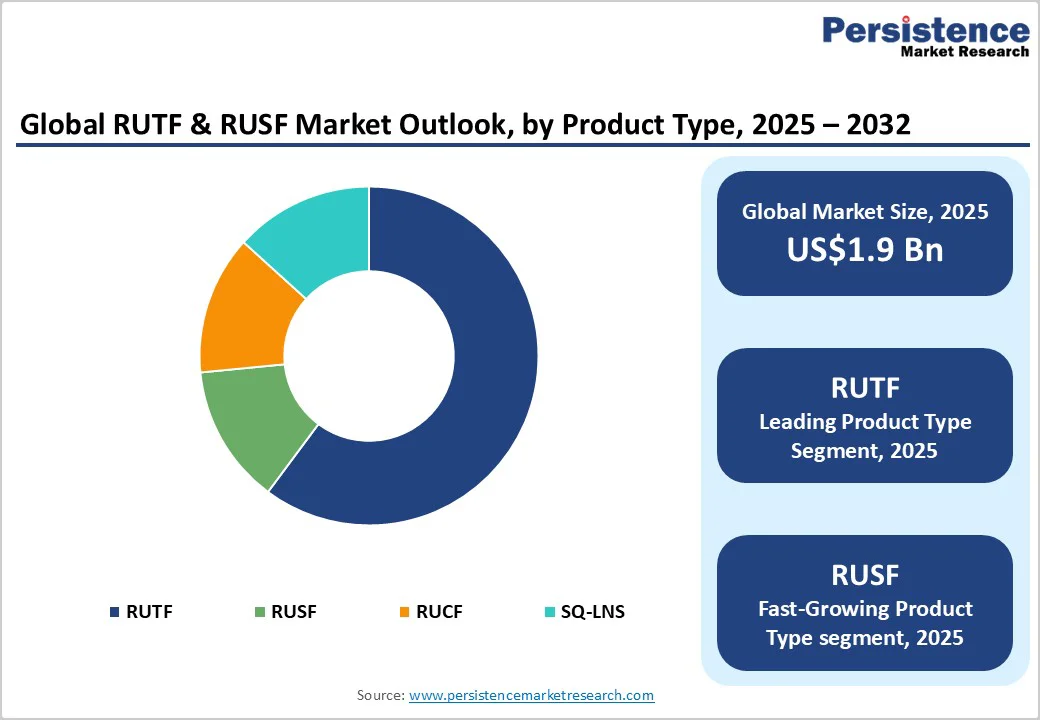

- Dominant Product Type: RUTF remains the dominant product category, contributing 67.6% of market share, supported by its central role in treating severe acute malnutrition and its prioritization in emergency and institutional pipelines.

- Leading Formulation: Peanut- and milk-based formulations account for 71.2% of total production, driven by established clinical validation, stable supply chains, and strong procurement confidence.

| Key Insights | Details |

|---|---|

|

RUTF & RUSF Market Size (2025E) |

US$1.9 Bn |

|

Market Value Forecast (2032F) |

US$3.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustained Humanitarian Demand and Rising Prevalence of Acute Malnutrition

Humanitarian agencies report funded demand and procurement spikes since 2020, with volumes increasing from roughly 50,000 MT per year to scenarios of 70,000–120,000 MT in 2023–2025. This volume escalation directly increases demand for Ready-to-Use Therapeutic Food (RUTF) and Ready-to-Use Supplementary Food (RUSF), prompting producers and donors to invest in materials and logistics. Community-based management of acute malnutrition maintains a robust baseline for therapeutic products. Large-agency procurement means policy shifts or funding changes have an outsized influence on market trajectories.

Donor and Government Funding plus Renewed Political Focus on Nutrition

Global nutrition initiatives and emergency allocations since 2022 have raised budget lines for therapeutic and supplementary nutrition. Major donors have directed funding to scale production in supplier countries, supporting capacity expansion and enabling price negotiations that reduce unit costs for large buyers. Recent grants and commitments have helped NGOs and social enterprises expand production across the U.S., Africa, and Asia.

Local Manufacturing and Product Innovation to Reduce Cost and Increase Reach

Manufacturers and nonprofit producers continue to expand local plants through franchise networks and targeted financing. Local production reduces landed cost, shortens lead time, and strengthens country-level resilience. Innovation in plant-based formulas and reduced-lactose recipes increases adaptability in regions with allergies, dietary restrictions, or supply constraints, opening new procurement pathways.

Barrier Analysis - Funding Volatility and Donor Concentration

The market is heavily donor-funded, with a small number of institutional buyers accounting for the majority of purchases. Funding freezes, policy shifts, or reprioritization can sharply reduce procurement volumes. Despite improved supply capacity, predictable long-term funding remains uncertain. Price and volume sensitivity are high because most RUTF funding originates from humanitarian budgets, which are affected by political cycles.

Raw Material and Logistics Cost Escalation

RUTF and RUSF production depends on peanuts, milk powder, vegetable oil, and micronutrient premixes. Commodity volatility and elevated logistics costs raise landed costs and compress producer margins. When donors fix unit prices in tenders, producers face either margin compression or reduced order volumes, limiting reinvestment in capital expenditure and innovation.

Opportunity Analysis - Product Diversification with Plant-Based and Allergy-Friendly Formulas

Plant-based RUTF formulations that reduce or replace milk content can lower unit cost and expand production in regions with locally abundant cereals. Pilot program data suggests potential cost reductions of 20–30% per treatment. If broadly approved, such innovations would enable programs to treat more children with the same funding envelope.

Regional Manufacturing Clusters and Franchise Scaling

Expanding regional manufacturing, supported by concessional financing and franchise networks, reduces landed costs and increases procurement responsiveness. Strategically located plants can serve both humanitarian markets and emerging preventive-nutrition programs, creating additional revenue streams.

Institutional Procurement and Blended Finance for Stocks

Blended finance solutions that combine donor guarantees with impact investment can unlock working capital for warehousing and buffer stocks. This improves emergency responsiveness and allows manufacturers to secure raw materials at volume discounts. Multi-year commitments for strategic stockpiles help de-risk operations for larger producers.

Category-Wise Analysis

Product Type Insights

RUTF continues to hold the largest share, 67.6%, as it addresses severe acute malnutrition, a condition classified as life-threatening and prioritized in national nutrition budgets. Large institutional buyers procure substantial volumes of RUTF annually, shaping long-term supplier capacity planning and influencing global production distribution. RUTF’s integration into community-based treatment protocols makes it a non-substitutable therapeutic product during emergencies. For example, several countries maintain dedicated RUTF reserves within emergency nutrition pipelines to ensure uninterrupted treatment, reinforcing its position as the dominant product category.

RUSF and small-quantity lipid-based nutrient supplements are expanding quickly due to their use in prevention programs, school feeding schemes, and maternal–child health initiatives. Many governments continue to scale up moderate acute malnutrition and stunting-reduction programs that rely on RUSF as a core input. Growth is supported by packaging innovations such as single-serve sachets and customized micronutrient mixes for different age groups. For example, some ministries of health have piloted RUSF-fortified school snacks to address seasonal malnutrition, resulting in higher year-on-year demand and positioning RUSF as the fastest-growing segment.

Formulation Insights

Peanut and milk-based RUTF remains the benchmark formulation category, accounting for 71.2% of market share, due to its long-standing clinical validation and predictable therapeutic outcomes. These products closely align with recommended nutrient profiles, and procurement agencies have high confidence in their stability, taste acceptability, and absorption characteristics. The supporting supply chains are mature, with established peanut paste processors, dairy suppliers, and quality-assurance systems already integrated into many manufacturing sites. For example, high-volume producers continue to rely on peanut-and-milk blends to maintain consistency across multiple production batches, reinforcing the category’s dominance.

Plant-based and reduced-milk formulations are gaining momentum due to their potential to lower costs, address lactose intolerance, and increase local ingredient utilization. Several manufacturers are piloting recipes using locally available grains, legumes, and oilseeds to meet therapeutic requirements while reducing dependence on imported dairy ingredients. Successful trials of chickpea-based or soybean-enriched formulations in select countries illustrate the growing feasibility of diversified recipes. As more national programs explore locally sourced alternatives to strengthen domestic value chains, plant-based formulations are positioned for rapid growth.

Regional Insights

North America RUTF & RUSF Market Trends - Strategic Production Hub with Strong R&D and Supply Resilience

North America is not the largest buyer by volume but plays a key strategic role in global production and R&D. U.S.-based producers supply both domestic stockpiles and export markets, supported by philanthropic funding streams and structured government procurement. The region contributes disproportionately to global production value due to specialized manufacturing capability, reliable raw-material sourcing, and advanced quality-assurance systems that enable consistent output.

The U.S. continues to serve as a central hub for nonprofit and social enterprise production, hosting extensive R&D focused on alternative recipes, packaging innovation, and shelf-life optimization. Strong regulatory oversight reinforces adherence to stringent food-safety standards and enhances supplier eligibility for institutional tenders in multiple regions. Investment activity in North America includes capacity expansions, warehouse upgrades, cold-chain improvements, and multi-year procurement agreements designed to stabilize production planning.

Recent developments illustrate this momentum, such as a U.S. manufacturer completing a production-line upgrade to increase emergency-response supply capability, a nonprofit producer forming a partnership with a logistics company to improve distribution reliability during climate-related disruptions, and a regional R&D center initiating pilot trials on reduced-milk and plant-forward formulations aimed at lowering production costs. Together, these initiatives reinforce North America’s strategic importance to global therapeutic food supply resilience.

Europe RUTF & RUSF Market Trends - Global Quality Leader Driving Innovation and Technical Transfer

Europe remains the leading market with a market share of 35.3%, product innovation, and global technology transfer, supported by long-established manufacturers and franchise networks. European suppliers maintain a strong influence in institutional tenders and frequently support regional producers through technical assistance, operational audits, and formulation training, strengthening manufacturing consistency in partner regions. France, the U.K., and Germany serve as important centers for R&D, donor coordination, and production infrastructure.

The EU’s stringent food-safety regulations enhance export credibility and reinforce trust in European-origin therapeutic foods, though they require sustained investment in compliance, traceability, and quality-management systems. Growth in the region is supported by advanced processing technologies, ongoing packaging development, and long-term donor commitments that help stabilize procurement cycles.

Recent activity reflects Europe’s continued leadership, including the commissioning of new mixing and filling lines by a large producer to meet rising demand, a technical-support initiative that provides equipment upgrades and training to franchise partners in Africa, and a packaging innovation project evaluating lightweight, lower-waste sachets that reduce transportation costs while maintaining product stability. These developments highlight Europe’s continued role in setting quality benchmarks, supporting regional capacity building, and driving innovation across the therapeutic food sector.

Asia Pacific RUTF & RUSF Market Trends - Rapidly Expanding Manufacturing Base with Cost-Competitive Growth

Asia Pacific is one of the fastest-growing manufacturing regions, supported by access to cost-competitive raw materials, expanding processing capacity, and a rising number of local producers entering the market. India and several ASEAN countries are building substantial production capabilities to serve expanding domestic programs targeting moderate acute malnutrition and maternal–child nutrition while also supplying regional export markets. Government procurement initiatives are increasing the demand pool for RUSF and RUCF, with local value addition and cost advantages supporting rapid market expansion.

Growth is also driven by ongoing investment in automated manufacturing systems, improved quality-control processes, and upgraded storage and logistics infrastructure. The region’s ability to harmonize with global nutrient profiles and food safety standards will shape future participation in international institutional tenders.

Recent developments point to accelerating momentum, including the completion of a new processing facility in India designed for dual domestic and export supply, a co-production agreement in Southeast Asia that enables a local manufacturer to improve quality-assurance capacity through partnership with an established regional food processor, and early-stage research efforts exploring chickpea- and mung-bean-based formulations aimed at reducing dependence on imported dairy ingredients. These initiatives reflect Asia Pacific’s expanding role in global production diversification and its growing contribution to supply-chain resilience.

Competitive Landscape

The global RUTF & RUSF market is moderately consolidated with a group of established branded manufacturers, nonprofit producers, and regional suppliers. A small number of qualified producers capture most institutional tender volumes, although supplier diversity is increasing due to franchising and local manufacturing initiatives.

Key strategies include securing multi-year institutional contracts, localizing production through franchise and joint-venture models, diversifying formulations, and mitigating supply risk through donor-backed finance for working capital and buffer stocks.

Key Industry Developments

- In November 2025, the Katsina State Government in Nigeria announced plans to build a local RUTF production factory and to employ more than 2,300 health workers as part of a larger strategy to tackle child malnutrition.

- In October 2024, UNICEF issued an urgent appeal for US$165 million to avoid widespread RUTF stockouts, warning that nearly two million severely malnourished children could be left without treatment.

Companies Covered in RUTF & RUSF Market

- Nutriset

- GC Rieber Compact

- Edesia Nutrition

- Valid Nutrition

- Hilina Enriched Foods

- Insta Products

- Nuflower Foods

- Mana Nutrition

- Tabuka Foods

- Amino Foods

- Samil Industrial

- Darfood

- InnoFaso

- NutriCare

- ATTA Nutrifood

- Huy Nutrition

- Mark Drugs

- Allripe International

- Medswana

- NutriVita Foods

Frequently Asked Questions

The global RUTF & RUSF market size in 2025 is US$1.9 Billion.

By 2032, the market is projected to reach US$3.1 Billion.

Key trends include rising adoption of community-based malnutrition treatment programs, increased procurement by humanitarian agencies, expansion of localized manufacturing units in Africa and South Asia, and the shift toward peanut-free and dairy-alternative formulations to improve allergen safety and cost efficiency.

Ready-to-Use Therapeutic Food (RUTF) remains the largest segment, driven by high global demand for severe acute malnutrition (SAM) management across emergency and non-emergency settings.

The market is expected to grow at a CAGR of 7.1% between 2025 and 2032, supported by expanding public health nutrition initiatives and strengthened supply chains in low-resource regions.