- Communication Infrastructure & Services

- RF-over-Fiber (RFoF) Solutions Market

RF-over-Fiber (RFoF) Solutions Market Size, Share, and Growth Forecast, 2026 - 2033

RF-over-Fiber (RFoF) Solutions Market by Component (Products [RFoF Links, RFoF Transceivers Modules, RFoF Subsystems], Services [Installation Services, Repair and Maintenance Services, Support Services]), Frequency Band (Up to 3 GHz, 3 GHz - 8 GHz, 8 GHz - 18 GHz, More than 18 GHz), Application, and Regional Analysis for 2026 - 2033

RF-over-Fiber (RFoF) Solutions Market Size and Trends

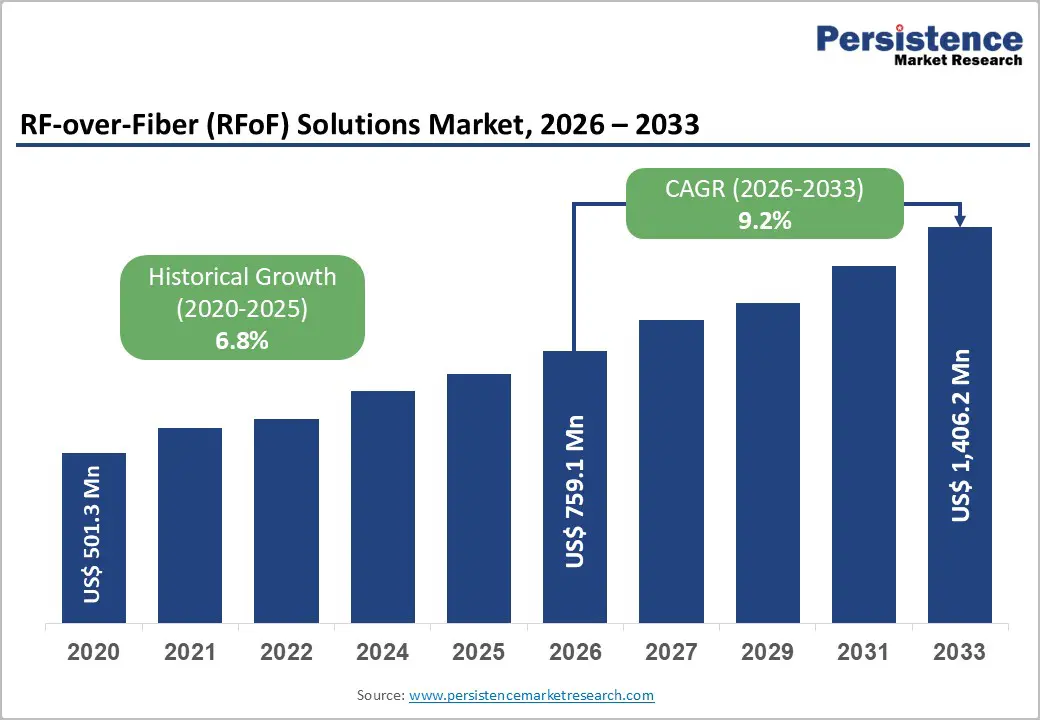

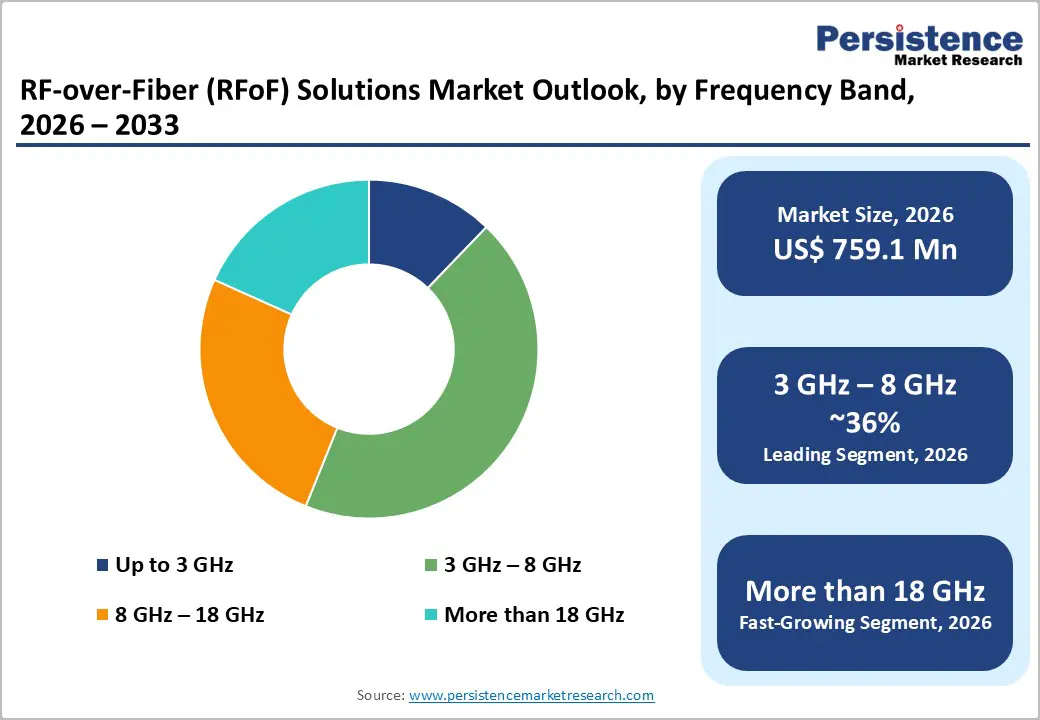

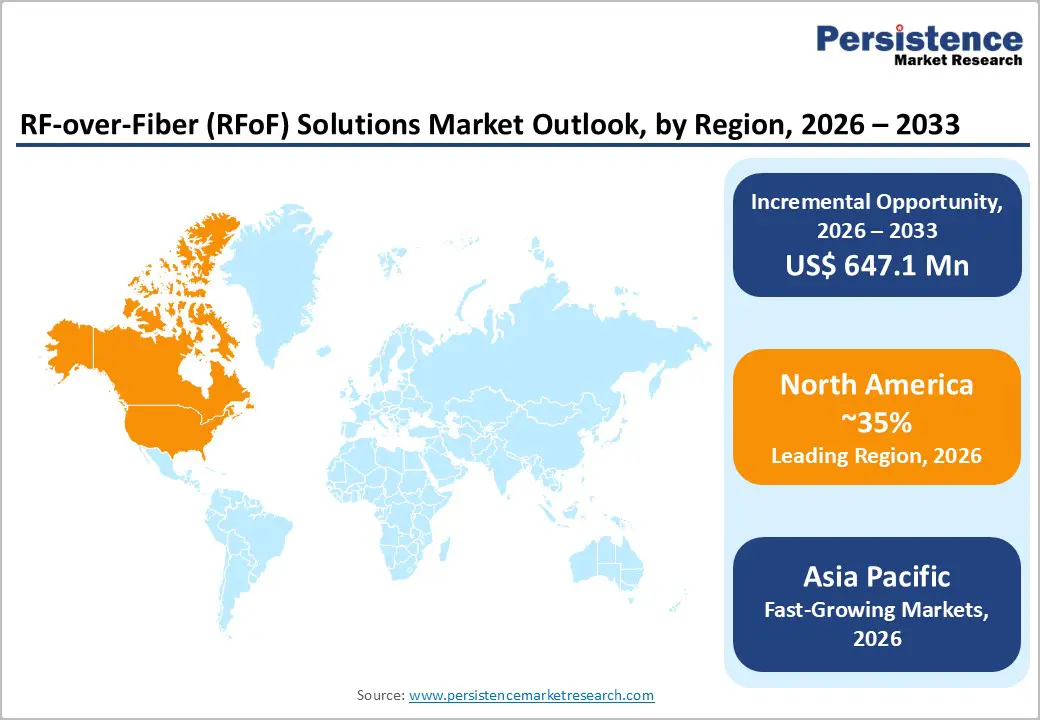

The global RF-over-fiber (RFoF) solutions market size is projected to rise from US$ 759.1 Mn in 2026 to US$ 1,406.2 Mn by 2033. It is anticipated that the market will grow at a CAGR of 9.2% from 2026 to 2033, driven by the accelerating deployment of 5G and emerging 6G telecommunications infrastructure, which demand high-frequency, low-latency signal transmission over extended distances.

As traditional coaxial cable solutions reach their technical limits in supporting millimeter-wave frequencies and distributed antenna systems, RF-over-fiber technology has emerged as the preferred alternative to copper-based transmission media. The strategic focus on secure, electromagnetic interference-resistant communications in defense and aerospace sectors is substantially accelerating market adoption across geographies.

Key Industry Highlights:

- Leading Component: RFoF transceiver modules dominate the product segment, capturing more than 46% market share in 2026, driven by their ability to integrate optical and RF functions, reduce equipment count, and support high-bandwidth, long-distance RF transmission. RFoF links are the fastest-growing component due to rising demand for long-reach, low-loss signal transport in telecom, satellite, and defense applications.

- Leading Frequency Band: 3 GHz - 8 GHz dominates with over 36% market share in 2026, supported by 5G mid-band deployments and radar applications that require high bandwidth and low latency. More than 18 GHz is the fastest-growing band with a CAGR of 14.7%, driven by emerging high-frequency satellite communications and advanced defense systems demanding ultra-wide bandwidth.

- Leading Application: Cellular fronthaul/backhaul holds the largest share at over 32% in 2026, due to telecom operators upgrading networks to support massive 4G/5G data traffic and C-RAN architectures. Commercial satellite ground stations are the fastest-growing application, driven by LEO constellation expansion, multi-beam antennas, and increased use of higher frequency bands.

- Leading Region: North America leads with over 35% market share in 2026, driven by large-scale 5G fronthaul deployment, high telecom CAPEX, and strong defense & aerospace demand. Asia Pacific is the fastest-growing region with a CAGR of 14.8%, supported by dense 5G rollouts, growing defense and satellite communication needs, and major fiber expansion programs.

| Global Market Attribute | Key Insights |

|---|---|

| RF-over-Fiber (RFoF) Solutions Market Size (2026E) | US$ 759.1 Mn |

| Market Value Forecast (2033F) | US$ 1,406.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 9.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.8% |

Market Dynamics

Driver

Higher Bandwidth & Capacity and EMI Immunity Driving RFoF Adoption

The demand for higher bandwidth and capacity is pushing RF-over-Fiber (RFoF) solutions due to traditional coaxial cables struggling to support the increasing data rates and long-distance signal transmission. As networks evolve toward 5G/6G, satellite communications, and advanced radar systems, the need for high-capacity links becomes critical, making RFoF a preferred choice. Electromagnetic interference (EMI) immunity is becoming a major requirement in congested RF environments, such as military operations, dense urban telecom hubs, and industrial settings. Optical fiber is inherently immune to EMI, ensuring stable and reliable signal integrity even in harsh conditions. The dual demand for higher bandwidth and EMI immunity is driving strong adoption.

Defense, Aerospace, and Satellite Communication Modernization

RFoF’s inherent electromagnetic hardening ensures reliable signal integrity in hostile environments, making it ideal for military communications and electronic warfare scenarios. Satellite ground stations, especially those supporting expanding LEO constellations, use RFoF to transmit telemetry and command signals from distributed antenna arrays to centralized control centers without loss or latency. Increased defense and aerospace modernization efforts are creating sustained demand for RFoF solutions across airborne platforms, naval vessels, and ground-based command centers. Investments in next-generation satellite communications and advanced sensing systems further expand demand for high-performance RFoF components across multiple frequency bands.

Restraint

High Infrastructure Deployment Costs and Capital Intensity

The high initial capital expenditure required to deploy comprehensive fiber-optic infrastructure, especially in rural and geographically isolated areas, remains a major restraint, limiting adoption by smaller telecom operators and regional service providers. RFoF system integration demands specialized installation expertise and extensive compatibility testing with existing network architectures, leading to deployment timelines of 6-18 months and mid-scale implementation costs ranging from US$ 500,000 to US$ 2 million. Many small and medium-sized enterprises delay RFoF deployment and continue using legacy copper systems despite their lower performance. Integration complexity in heterogeneous networks where equipment from multiple manufacturers must interoperate adds certification and testing burdens, further increasing costs and timelines.

Technical Integration Complexity and Signal Degradation Challenges

RF-over-fiber (RFoF) systems face significant technical challenges due to environmental factors, including chromatic dispersion, temperature-driven phase shifts, and modal coupling in multimode fibers, which degrade signal integrity. Ensuring phase-matching across multi-channel RFoF links for phased-array radar and coordinated antenna systems requires specialized optical delay lines and advanced signal conditioning, increasing component costs well beyond standard single-link deployments. Integration with legacy 3G/4G infrastructure often exposes incompatibility in connectors, impedance matching, and control protocols, necessitating custom engineering and slowing rollout. A limited pool of skilled RFoF designers and technicians restricts deployment capacity, especially in emerging markets.

Opportunity

Cloud Computing Infrastructure Expansion and AI Data Center Proliferation

The rapid rise in AI workload processing and machine learning training is driving massive expansion in global data center capacity, with hyperscale cloud providers building high-density, AI-optimized facilities that demand extensive low-latency, high-bandwidth interconnects. This surge fuels demand for RFoF solutions, which enable efficient, long-reach transmission of high-frequency signals required for distributed antenna systems and remote base station architectures. As edge computing grows, especially alongside 5G fronthaul deployments, RFoF becomes critical for connecting geographically dispersed compute nodes with minimal latency, supporting real-time AI inference. Asia-Pacific is emerging as a key growth region, with major investments in Singapore, Tokyo, Sydney, and India driving colocation and hyperscale build-outs.

Centralized Radio Access Network (C-RAN) Architecture Implementation and Remote Radio Head Deployment

Telecommunications operators are increasingly shifting from traditional distributed RAN setups to centralized RAN (C-RAN) architectures, where baseband processing is consolidated in large data centers and connected to remote radio units via fiber fronthaul links enabled by RF-over-Fiber technology. This transition supports advanced features like coordinated multi-point transmission, dynamic load balancing, and improved spectrum efficiency, driving significant operational and network performance gains. North America has already deployed C-RAN for 5G across more than 50 metropolitan areas, while Asia-Pacific, especially China and Japan, is rapidly expanding adoption. The Open RAN initiative further accelerates this shift by standardizing RFoF-compatible fronthaul specifications, promoting interoperability and reducing component costs.

Category-wise Analysis

Component Analysis

RFoF transceivers modules dominate the product segment, capturing more than 46% market share in 2026 as they directly address the need for high-bandwidth, low-loss transmission of RF signals over long distances critical for modern telecom and wireless infrastructure. They simplify system design by integrating optical and RF functions, reducing equipment count and improving reliability. Growing demand for 5G, distributed antenna systems (DAS), and seamless connectivity in dense urban environments further drives their adoption. Transceiver modules offer scalable and flexible deployment options that align with network upgrade cycles.

RFoF links demonstrate significant growth as they offer a highly efficient way to transport RF signals over long distances with minimal loss, which is critical for modern wireless networks and distributed antenna systems. As telecom operators expand 5G and begin preparing for 6G, the need for low-latency, high-capacity signal distribution is increasing. RFoF links are preferred in harsh environments where traditional coaxial cabling is impractical due to weight, interference, and maintenance issues. Their ability to support high-frequency signals and wide bandwidths makes them ideal for advanced radar, satellite, and high-speed communication applications, driving rapid adoption.

Frequency Band Analysis

3 GHz - 8 GHz dominate the market, capturing over 36% market share in 2026 with a value exceeding US$ 273.3 Mn, as this range aligns with key communication and radar applications that demand high bandwidth and low latency. It supports 5G mid-band services, essential for broad coverage and capacity in wireless networks. Many military and aerospace systems also operate in this band, driving demand for high-fidelity RF transmission over fiber to maintain signal integrity. This spectrum efficiently balances range and performance, making it ideal for dense urban and indoor deployments where RFoF minimizes interference and loss.

More than 18 GHz demonstrate highest growth with a CAGR of 14.7% due to modern wireless systems and defense applications increasingly requiring ultra-wide bandwidth and high-frequency transmission. As satellite communications expand, operators need RF transport solutions that support higher carrier frequencies with minimal loss and latency. Military and aerospace systems demand compact, lightweight, and rugged RF distribution, pushing the adoption of RFoF for frequencies above 18 GHz.

Application Analysis

Cellular fronthaul/backhaul holds over 32% of the market share in 2026, with a value exceeding US$ 242.9 Mn, due to mobile networks' demand for high-capacity, low-latency links to support massive data traffic from 4G/5G services. Fiber enables transparent, high-fidelity RF transmission over long distances, which is essential for densified cell sites and centralized RAN architectures. It also reduces interference and signal degradation compared with traditional coaxial links. Operators are upgrading backhaul to fiber to handle higher bandwidth and future-proof capacity needs as user data consumption grows.

Commercial satellite ground stations are expected to grow at the highest rate due to the surge in low-Earth orbit (LEO) and geostationary satellite deployments is driving massive demand for high-bandwidth, low-latency connectivity. Ground stations need reliable long-distance RF signal transmission between antennas and processing equipment, and RFoF offers superior signal integrity compared to coaxial cabling, especially over extended distances. The shift toward multi-beam antennas, phased arrays, and higher frequency bands (Ka/Ku) also increases the need for low-loss RF transport solutions.

Regional Insights

North America RF-over-Fiber (RFoF) Solutions Market Trends

North America accounts for over 35% of the RF-over-Fiber (RFoF) Solutions market share in 2026, reaching approximately US$ 265.7 Mn, driven by large-scale 5G fronthaul deployments, high telecom capital expenditure, and strong aerospace and defense demand. RFoF-enabled remote radio head architectures reached critical scale across 50+ metropolitan areas, including New York, Los Angeles, Chicago, Dallas, and Toronto, supported by major investments from Verizon, AT&T, and Rogers exceeding US$1 billion during 2023-2025. The FCC’s 5G Fund for Rural America, Dec 2024, prioritizes fiber-based backhaul, indirectly accelerating adoption for long-distance antenna deployments. Defense and space programs led by Lockheed Martin, Raytheon, Boeing, and NASA’s SCaN Testbed continue to validate RFoF performance, reinforcing adoption across military and civilian communication systems.

Asia Pacific RF-over-Fiber (RFoF) Solutions Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 14.8%, due to dense 5G fronthaul deployments and rising defense and satellite communication requirements. China’s large-scale 5G rollout, supported by strong government policy and operator capital expenditure, has accelerated adoption across cellular fronthaul, satellite ground infrastructure, and defense networks, while localization efforts by Huawei and domestic vendors have increased supply availability and pricing competition. India represents the highest growth potential within the region, underpinned by the BharatNet program connecting over 214,000 gram panchayats and rapid nationwide optical fiber expansion exceeding 3.7 million route kilometers, with fiber deployment intensity increasing significantly during the 5G era. Japan and South Korea maintain steady RFoF growth momentum through advanced 5G networks, early-stage 6G research, and strong domestic optical component ecosystems led by companies including Samsung and LG.

Europe RF-over-Fiber (RFoF) Solutions Market Trends

Europe is expected to hold more than 20% share by 2026, driven by the rapid deployment of next-generation telecommunications networks, high-bandwidth RF transport over long distances, and regulatory harmonization favoring fiber-based architectures. Leading markets Germany, the UK, and France show strong adoption, with operators like Telekom Deutschland and Vodafone Germany deploying C-RAN 5G networks that boost demand from suppliers. Defense, aerospace, and space communication programs further support growth, as NATO standardization, the UK Space Agency, and Arianespace increasingly require RFoF for secure, low-EMI communications. Environmental and electromagnetic compliance regulations reinforce RFoF preference over conventional RF media across Europe.

Competitive Landscape

The RF-over-Fiber (RFoF) solutions market is moderately fragmented, with a mix of specialized technology providers and a few established photonics players. Companies compete by focusing on high-performance, low-latency, and low-loss systems tailored for applications. Differentiate their product through customization, ruggedized designs, wide frequency support, and seamless integration with existing RF and optical infrastructure. Companies also emphasize long-term contracts, application-specific solutions, and close customer collaboration to build switching costs and sustain competitive advantage.

Key Industry Developments

- In April 2025, Hytech Associates entered into a strategic sales partnership with RFOptic to expand the reach of RFOptic’s RF-over-Fiber and Optical Delay Line solutions. Through this agreement, Hytech will market RFOptic’s low-loss, EMI-immune RFoF systems, enabling secure, long-distance, and high-performance signal transmission across diverse industrial and telecom applications.

- In December 2024, RFOptic launched its new RFoF Ultra product series targeting electronic warfare and advanced wireless testing applications, offering coax replacement from 100 MHz up to 12 GHz and 18 GHz in a compact form factor. The solution delivers high dynamic range with improved ACLR and EVM, supports dense 1U/2U system integration, and is optimized for 5G and emerging 6G deployments.

Companies Covered in RF-over-Fiber (RFoF) Solutions Market

- Huber+Suhner AG

- Optical Zonu Corporation

- DEV Systemtechnik GmbH

- ViaLite Communications

- RFOptic Ltd.

- Global Foxcom

- Emcore Corporation

- Finisar Corporation

- Syntonics LLC

- Octane Wireless

- APIC Corporation

- Glenair, Inc.

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 759.1 Mn in 2026.

The need to transmit high-frequency RF signals over long distances with minimal loss, low latency, and strong immunity to electromagnetic interference is a key driver of the market.

The market is expected to witness a CAGR of 9.2% from 2026 to 2033.

The expansion of 5G/6G networks, satellite ground stations, and defense modernization programs that require low-loss, secure RF signal transport and remote sensing applications create strong market expansion potential.

Huber+Suhner AG, Optical Zonu Corporation, DEV Systemtechnik GmbH, ViaLite Communications, RFOptic Ltd., Global Foxcom, Emcore Corporation are among the leading key players.