- Smart Packaging

- Resealable Films Market

Resealable Films Market Size, Share, and Growth Forecast, 2026 - 2033

Resealable Films by Material Type (Polyethylene, PET, Others), Product Form (Pouches, Lidding Films, Others), Closing Mechanism (Zipper, Adhesive/Pressure Sensitive), Application (Food & Beverage, Personal Care, Others), and Regional Analysis 2026 - 2033

Resealable Films Market Size and Trends Analysis

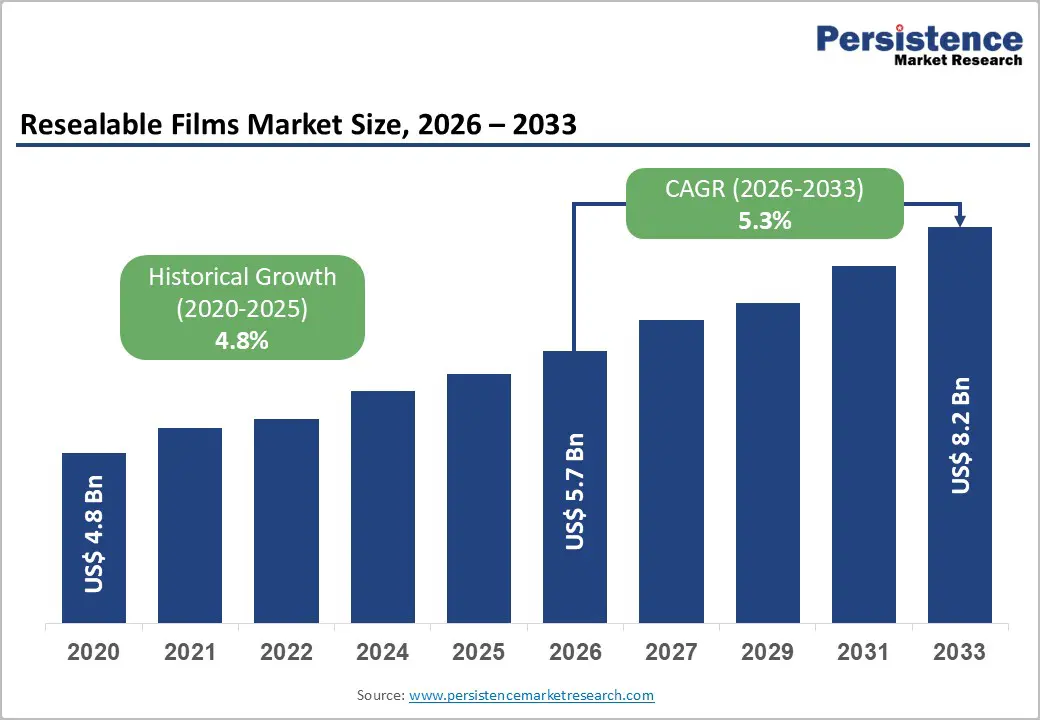

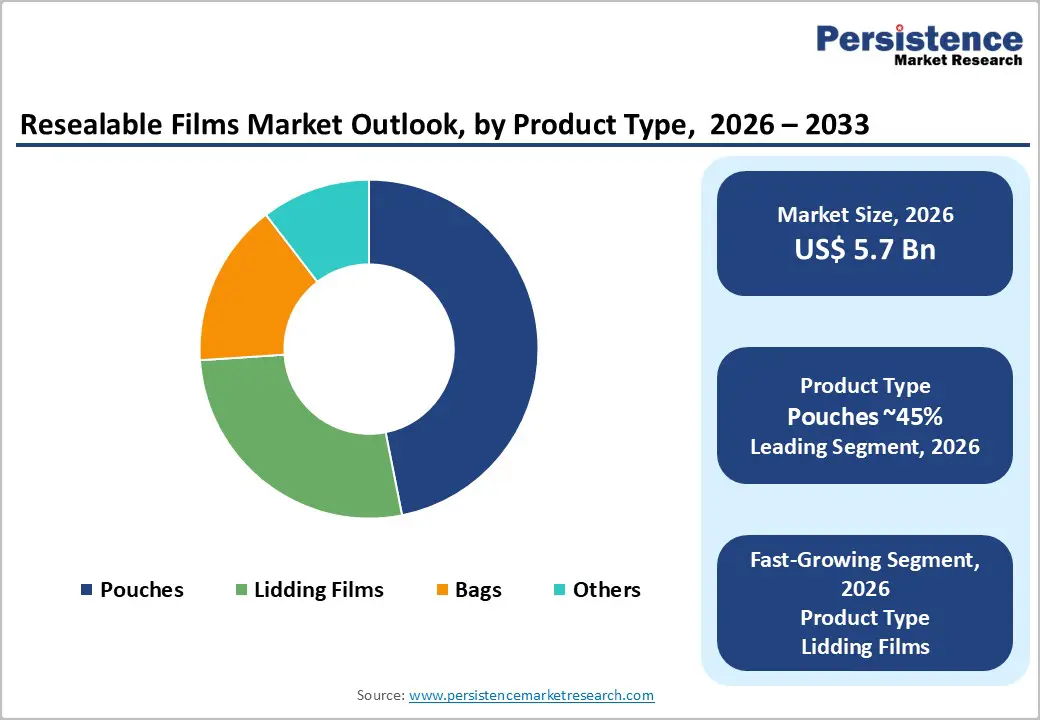

The global resealable films market size is likely to be valued at US$5.7 billion in 2026 and is expected to reach US$ 8.2billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by the global prioritization of food waste reduction and the "Design for Recycling" (DfR) mandates enforced by regulatory bodies such as the European Union.

As consumer demographics shift toward smaller households requiring portion control, resealable films are becoming the standard for shelf-life extension in the food & beverage and healthcare sectors. This trajectory indicates a market maturation where convenience features are no longer premium add-ons but essential requirements for competitive packaging.

Key Industry Highlights:

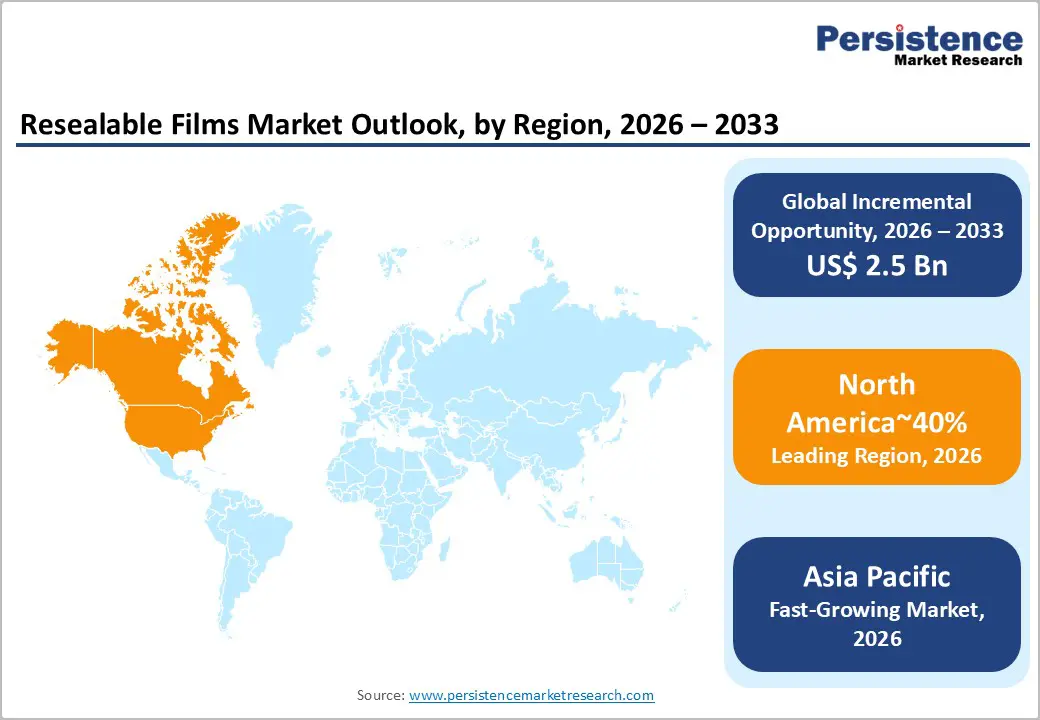

- Leading Region: North America is projected to lead due to high F&B and healthcare consumption, advanced packaging infrastructure, and strong regulatory frameworks, accounting for approximately 40% share.

- Fastest-growing Region: Asia Pacific, due to rapid industrialization, expanding F&B and pharmaceutical sectors, and rising urbanization.

- Leading Material Segment: Polyethylene, accounting for approximately 42%, driven by cost-efficiency, flexibility, and compatibility across high-volume packaging applications.

- Leading Product Form Segment: Pouches are expected to lead through versatility, cost-efficiency, and suitability across retail, frozen, and ready-to-eat formats, with approximately 45%.

| Key Insights | Details |

|---|---|

|

Resealable Films Market Size (2026E) |

US$5.7 Bn |

|

Market Value Forecast (2033F) |

US$8.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis – Demand for Convenient Packaging

Rising demand for convenient packaging is structurally strengthening the adoption of resealable films across packaged food value chains. Urbanization and time-constrained consumption patterns are increasing dependence on ready-to-store and multi-use product formats. Resealable films support extended product usability after initial opening, which improves household storage efficiency and reduces premature disposal. Shelf life enhancement capabilities reinforce retailer inventory management by lowering spoilage exposure and stabilizing replenishment cycles. Portion control functionality aligns with broader waste minimization frameworks embedded within retail and food service systems. These combined attributes position resealable formats as integral components of modern flexible packaging architecture.

Flexible resealable substrates are progressively displacing rigid packaging in high turnover categories. Pouch-based configurations improve material efficiency while optimizing transportation and shelf space utilization. Enhanced pack functionality strengthens consumer retention through consistent post-purchase performance rather than promotional influence. Retailers benefit from improved stock rotation and reduced return rates linked to compromised freshness. For converters and film producers, value creation shifts toward barrier engineering, seal integrity, and adhesive innovation. Resealable films are becoming embedded within cost-efficient and sustainability-driven packaging strategies.

Sustainability Mandates and Food Waste Reduction Initiatives

Escalating sustainability mandates are structurally accelerating demand for resealable film technologies across food packaging systems. Food waste contributes meaningfully to global greenhouse gas emissions, intensifying regulatory scrutiny and policy intervention. Resealable films mitigate post-opening spoilage by enabling controlled resealing of perishable products. This functional attribute aligns packaging performance with waste reduction and carbon mitigation objectives. Legislative frameworks, including the Packaging and Packaging Waste Regulation within the EU, reinforce prevention-oriented packaging standards. Compliance requirements are also reshaping material specifications and procurement criteria across retail supply chains.

Retailers are prioritizing packaging formats that reduce shrinkage and inventory losses. High barrier resealable films enhance moisture and oxygen control, strengthening product stability during distribution and storage. Regulatory alignment is shifting demand toward advanced multilayer substrates and precision sealing technologies. Film converters are reallocating investment toward barrier coatings, recyclable structures, and performance validation systems. Cost structures increasingly reflect lifecycle efficiency rather than upfront material pricing alone. These dynamics embed resealable films within broader decarbonization and waste minimization strategies across packaged food ecosystems.

Barrier Analysis – High Technical Complexity and Manufacturing Costs

A key structural restraint in the resealable films market is the elevated technical complexity associated with integrating resealable features into high-speed packaging environments. Implementation frequently requires retrofitting vertical form fill seal systems with zipper applicators and precision alignment modules. These modifications increase capital intensity and extend commissioning timelines across production facilities. Resealable structures also depend on multilayer laminates and pressure-sensitive adhesive systems that raise raw material procurement costs. For small and medium-sized enterprises, the resulting capital expenditure burden constrains adoption capacity. The combined equipment and material requirements embed higher entry barriers relative to conventional heat-seal film formats.

Operationally, complex resealable constructions can reduce line efficiency compared with standard film configurations. Additional sealing stages and alignment tolerances introduce variability that affects throughput stability. High-volume manufacturers, therefore, assess format conversion through strict return on investment thresholds. Downtime risk during changeover and operator retraining further influences decision frameworks. At the value chain level, converters must balance performance enhancement with cost containment pressures from brand owners. These dynamics moderate market penetration by linking technical sophistication directly to capital allocation discipline.

Recyclability Challenges of Multi-Material Film Structures

Despite their contribution to food waste reduction, resealable films face structural end-of-life constraints linked to material composition. Many legacy solutions depend on multilayer laminates combining dissimilar polymers to achieve barrier integrity and seal performance. These composite structures are incompatible with standard mechanical recycling systems and are frequently categorized as mixed plastics. As a result, recovery pathways are limited, increasing reliance on incineration or landfill disposal. This technical incompatibility creates tension between packaging functionality and circular economy objectives. Emerging mono-material mandates across regulated markets are intensifying scrutiny of non-recyclable flexible packaging formats.

Recyclability requirements are reshaping material innovation and procurement standards. Brand owners and retailers aligned with circular economy commitments are prioritizing polyethylene-based mono-material alternatives. Failure to transition toward compatible structures exposes manufacturers to regulatory levies and potential product delisting. Converters must therefore reengineer barrier performance within single polymer architectures while preserving seal reliability. This transition elevates research expenditure and reformulation complexity across flexible packaging portfolios. Recyclability constraints represent a structural restraint embedded within regulatory compliance and material science limitations.

Opportunity Analysis – Development of Mono Material Recyclable Resealable Film Architectures

The transition toward mono-material polyethylene and polypropylene resealable films represents a structurally significant innovation pathway within flexible packaging markets. Regulatory recyclability mandates and corporate sustainability commitments are accelerating demand for solutions compatible with established mechanical recycling streams. Engineering high-barrier performance within single polymer architectures addresses the core limitation of legacy multilayer laminates. Integration of resealable functionality into recyclable substrates enhances lifecycle efficiency without compromising consumer convenience. As sustainability targets approach implementation deadlines, procurement strategies increasingly prioritize verified recyclability credentials. This convergence of regulatory pressure and brand accountability expands the addressable market for compliant resealable film technologies.

Intellectual property around barrier coatings, seal integrity, and polymer modification becomes a primary competitive differentiator. Suppliers capable of scaling mono material solutions that match legacy performance standards gain preferential access to large consumer goods portfolios. Compatibility with existing collection systems reduces infrastructure dependency and lowers systemic transition friction. Capital allocation is therefore shifting toward polymer science innovation and extrusion optimization platforms. These dynamics position recyclable resealable films within broader circular economy investment cycles.

Expansion into Pharmaceutical and Medical Flexible Packaging

The healthcare sector represents a structurally attractive diversification pathway for resealable film manufacturers beyond food applications. Demand for senior-compliant and child-resistant packaging formats is increasing in parallel with demographic aging and chronic disease management trends. Resealable high-barrier films enable secure storage of transdermal systems, wound care materials, and selected medical devices between uses. Preservation of sterility and contamination control aligns directly with pharmaceutical quality assurance protocols and regulatory validation standards. Technologies originally engineered for food safety, including moisture and oxygen barrier optimization, can be adapted to meet medical packaging specifications. This functional convergence expands the application scope of advanced resealable substrates within regulated healthcare environments.

Entry into pharmaceutical packaging shifts competitive dynamics toward certification capability and compliance infrastructure. Regulatory approval processes, material traceability, and validation testing elevate technical thresholds relative to food markets. However, these barriers also reduce exposure to commoditization pressures typical of high-volume consumer goods packaging. Margin structures in medical applications generally reflect performance assurance and risk mitigation requirements. Resealable film suppliers capable of meeting pharmaceutical standards can reposition portfolios toward higher value, regulation-insulated demand streams.

Category-wise Analysis

Material Insights

Polyethylene is expected to lead, with approximately 42% share in 2026, supported by its entrenched role across high-volume food packaging workflows. Its low seal initiation temperature and compatibility with zipper and slider systems anchor widespread adoption in frozen foods, fresh produce, and retail pouches. Variants such as LDPE (Low-Density Polyethylene), LLDPE (Linear Low-Density Polyethylene), and HDPE (High-Density Polyethylene) enable tailored mechanical performance across flexible and heavy-duty applications. The shift toward mono-material architectures reinforces polyethylene as the default recyclable substrate within organized retail supply chains. Industry participants, including Amcor, Berry Global, Mondi, and Dow, integrate advanced PE resins and recyclable laminates to embed enterprise-scale deployment. Continuous innovation in BOPE structures, anti-fog coatings, and tactile reseal mechanisms sustains replacement cycles and utilization intensity across structured packaging ecosystems.

PET (Polyethylene Terephthalate) is expected to be the fastest-growing segment, driven by rising demand for high-clarity, high-performance packaging across premium food, medical, and ready-meal applications. Superior optical clarity, stiffness, and thermal stability position PET as the preferred substrate for lidding films and visible display packaging. Advancements in biaxially oriented PET technologies and mono-PET sealing solutions enhance barrier integrity while improving recyclability alignment. Expansion of recycled PET capacities and chemical recycling infrastructure supports scalable, sustainable adoption. Companies such as Toray Plastics, DuPont Teijin Films, Uflex, and Mitsubishi Chemical Group are advancing high-barrier PET platforms with precision surface treatments and automation compatibility. These factors collectively accelerate PET penetration in performance-driven and brand-sensitive packaging environments.

Product Insights

Pouches are expected to lead, accounting for approximately 45% share in 2026, supported by their entrenched adoption across snacks, confectionery, and pet food applications. Stand-up pouch architectures displace rigid containers by reducing material intensity while improving portability and shelf efficiency. Their lightweight structure enhances logistics optimization and lowers extended producer responsibility exposure across high-volume retail channels. Advanced zipper integrations and heat-stable reseal systems reinforce multi-serve convenience and product preservation. Companies such as Amcor, Mondi, and Berry Global continue expanding mono-material pouch platforms to align with recyclability and cost efficiency objectives. Ongoing innovation in gusset reinforcement, smart dispensing spouts, and high-barrier clear windows sustains utilization across organized retail and e-commerce supply chains.

Lidding films are expected to be the fastest-growing segment, driven by accelerating demand for tray-based fresh, chilled, and ready-meal formats. Retailers are replacing rigid snap-on lids with thinner resealable top-web films to reduce material usage and improve pallet efficiency. Peel-reseal technologies enhance tamper evidence, portion control, and modified atmosphere retention in protein and produce categories. Advancements in mono-PET sealing, wash-off adhesives, and laser micro-perforation strengthen recyclability and functional performance. Sealed Air, Amcor, KM Packaging, and Plastopil are expanding high-barrier lidding portfolios to meet fresh-to-go retail requirements. These developments position resealable top-seal films as a performance-driven upgrade within modern supermarket packaging systems.

Regional Insights

North America Resealable Films Market Trends

North America is expected to lead with 40% share, supported by structural demand fundamentals and regulatory alignment in 2026. The U.S. remains the central growth engine, underpinned by a mature, organized retail ecosystem and strong consumer preference for convenience-oriented packaging. High penetration of warehouse club formats such as Costco and Sam’s Club reinforces demand for large-format flexible packaging incorporating zippers and slider closures to preserve freshness across extended usage cycles. Product performance, seal integrity, and ease of reclosing remain central procurement criteria across food, personal care, and household applications.

Regulatory momentum further strengthens regional leadership. State-level mandates, including California Senate Bill 54, are accelerating the transition toward recyclable and reuse-aligned flexible structures. Industry investment is concentrated on store drop-off recyclable films compatible with the How2Recycle labeling framework, currently the most commercially viable recycling pathway for flexible packaging. Concurrently, manufacturers leverage the region’s innovation ecosystem to advance smart packaging integrations and certified child-resistant resealable formats, consolidating competitive advantage. Competitive intensity remains concentrated among established converters leveraging advanced R&D ecosystems to introduce smart packaging, child-resistant solutions, and high-barrier performance films.

Europe Resealable Films Market Trends

Europe is expected to remain a structurally mature and regulation-driven market, positioned as the benchmark region for sustainable packaging compliance and material circularity standards. The regional market is anticipated to be shaped by regulatory harmonization under the Packaging and Packaging Waste Regulation (PPWR) and broader European Green Deal objectives, which are expected to accelerate the transition from complex multi-layer laminates toward mono-material polyolefin structures. Demand is projected to be anchored in food applications requiring resealable lidding films and pressure-sensitive closure systems. Technological development is likely to concentrate on high-barrier coatings compatible with mechanical and chemical recycling streams, reinforcing the region’s institutional alignment between policy mandates and packaging innovation.

Germany is expected to function as the primary anchor shaping regional momentum, supported by high consumer sensitivity to plastic waste reduction and strict enforcement of packaging compliance frameworks. Industrial converters and film producers in Germany are projected to accelerate investment in recyclable mono-PO resealable systems, solvent-free lamination technologies, and advanced coating platforms that maintain oxygen and moisture barrier performance without compromising recyclability thresholds. As PPWR implementation timelines advance, Europe is expected to maintain its role as the regulatory reference market, shaping specification standards and innovation priorities across the global resealable films industry.

Asia Pacific Resealable Films Market Trends

Asia Pacific is expected to register the fastest growth trajectory in the global resealable films market, supported by structural expansion in packaged food consumption and large-scale flexible packaging manufacturing capacity. Rapid urbanization across major metropolitan corridors is anticipated to accelerate the transition from informal retail formats toward organized supermarkets and e-commerce platforms, where resealable packaging is positioned as a hygiene, shelf-life, and convenience necessity. The region’s cost-competitive extrusion, lamination, and pouch-conversion infrastructure is expected to strengthen its role as both a high-volume domestic consumption base and an export-oriented manufacturing hub. Regulatory frameworks are likely to evolve progressively, with increasing alignment toward recyclable mono-material structures as governments tighten oversight on non-recyclable multi-layer films.

China is expected to function as the principal anchor shaping regional acceleration, driven by scale advantages in polymer production, vertically integrated packaging conversion, and expanding modern retail penetration. Domestic converters are projected to enhance automation and barrier coating technologies to serve both internal demand and export markets. As regulatory scrutiny increases and brand owners standardize sustainability commitments, vendor strategies in China are expected to shift toward compliant resealable lidding films and recyclable zipper pouches, positioning the country as the structural engine of Asia Pacific’s fastest-growing resealable films ecosystem.

Competitive Landscape

The global resealable films market is moderately consolidated, with leadership concentrated among multinational flexible packaging groups such as Amcor, Berry Global, Mondi, Sealed Air, and Coveris. The upper tier is defined by vertically integrated operators with in-house polymer science, extrusion, lamination, and closure-system engineering capabilities, enabling development of proprietary zipper formats, peel-reseal technologies, and high-barrier mono-material structures. Beyond scale, their relevance is anchored in regulatory fluency and the ability to certify structures under recycling validation schemes such as Cyclos-HTP and the Association of Plastic Recyclers Design Guide, reinforcing on-pack sustainability claims and compliance assurance. The remaining competitive landscape is fragmented among regional converters specializing in application-specific formats, including bakery pouches, fresh produce lidding films, and niche pressure-sensitive reseal labels.

Competitive positioning is expected to revolve increasingly around sustainability integration and material platform standardization rather than price-led competition. Industry behavior is anticipated to reflect incremental consolidation, technology-focused acquisitions, and expanded collaboration with chemical recyclers and resin producers to secure compliant feedstock streams. Platform-based innovation, lifecycle assessment transparency, and alignment with extended producer responsibility frameworks are expected to define competitive advantage, shaping a market structure where technical depth, certification credibility, and global manufacturing integration determine strategic positioning.

Key Industry Highlights:

- In February 2026, Amcor integrated Berry Global's PE shrink portfolio into its North American service model. The move offers customers a single point of access for "best-in-class" recycle-ready bundling films, simplifying the transition to circular supply chains.

- In January 2026, Mondi received nine World Star Awards for innovations, including recyclable, high-performance flexible packaging solutions. The award-winning designs replace less sustainable multi-material structures with high-barrier paper and mono-plastic alternatives that maintain product freshness while ensuring end-of-life recyclability.

- In November 2025, Mondi launched an extended food packaging portfolio featuring solid board and digital printing for stand-out shelf presence. The expansion enables food manufacturers to pair resealable flexible lids with premium, digitally printed solid board trays for a cohesive, sustainable, and high-impact retail appearance.

- In March 2025, Amcor and Berry Global received final U.S. antitrust clearance for their USD 8.43 billion merger. This merger creates a global leader in flexible films and closures, consolidating the two largest buyers of plastic resins to dominate the food and healthcare packaging sectors.

Companies Covered in Resealable Films Market

- Amcor plc

- Berry Global Group, Inc.

- Mondi Group

- Sealed Air Corporation

- Coveris

- Constantia Flexibles

- Huhtamäki Oyj

- Sonoco Products Company

- ProAmpac

- Winpak Ltd.

- UFlex Ltd.

- Cosmo Films

- Printpack

- Toray Plastics

- Treofan

- Innovia Films

Frequently Asked Questions

The global resealable films market is projected to be valued at US$5.7 billion in 2026 and is expected to reach US$8.2 billion by 2033, driven by global food waste reduction priorities, "Design for Recycling" (DfR) mandates, and consumer demand for convenient, portion-controlled packaging.

Resealable films directly mitigate post-opening spoilage, a major contributor to food waste and its associated greenhouse gas emissions. By enabling controlled resealing and extending product usability, these films align packaging performance with regulatory waste reduction targets (e.g., the EU's PPWR) and retailer goals for minimizing inventory shrinkage.

The resealable films market is forecast to grow at a CAGR of 5.3% from 2026 to 2033, reflecting steady demand from the food & beverage sector and the maturation of resealable features from premium add-ons to essential packaging requirements.

North America is the leading regional market, accounting for approximately 40% share, supported by high F&B consumption, advanced packaging infrastructure, and strong regulatory frameworks. Asia Pacific is the fastest-growing region, driven by rapid industrialization, urbanization, and the expansion of organized retail and e-commerce.

The market is moderately consolidated, led by multinational flexible packaging groups such as Amcor, Berry Global, Mondi, and Sealed Air. These players compete through vertical integration, proprietary closure technologies, and the ability to certify structures for recyclability. Regional specialists such as Uflex Ltd. and ProAmpac are significant in specific geographies and application niches.