- Hardware & Software IT Services

- Recurring Payment Market

Recurring Payment Market Size, Share, and Growth Forecast, 2026 - 2033

Recurring Payment Market by Component Type (Services, Payment Platforms), Payment Type (Fixed, Variable), End-user (B2B, B2C), and Regional Analysis for 2026 - 2033

Recurring Payment Market Size and Trends Analysis

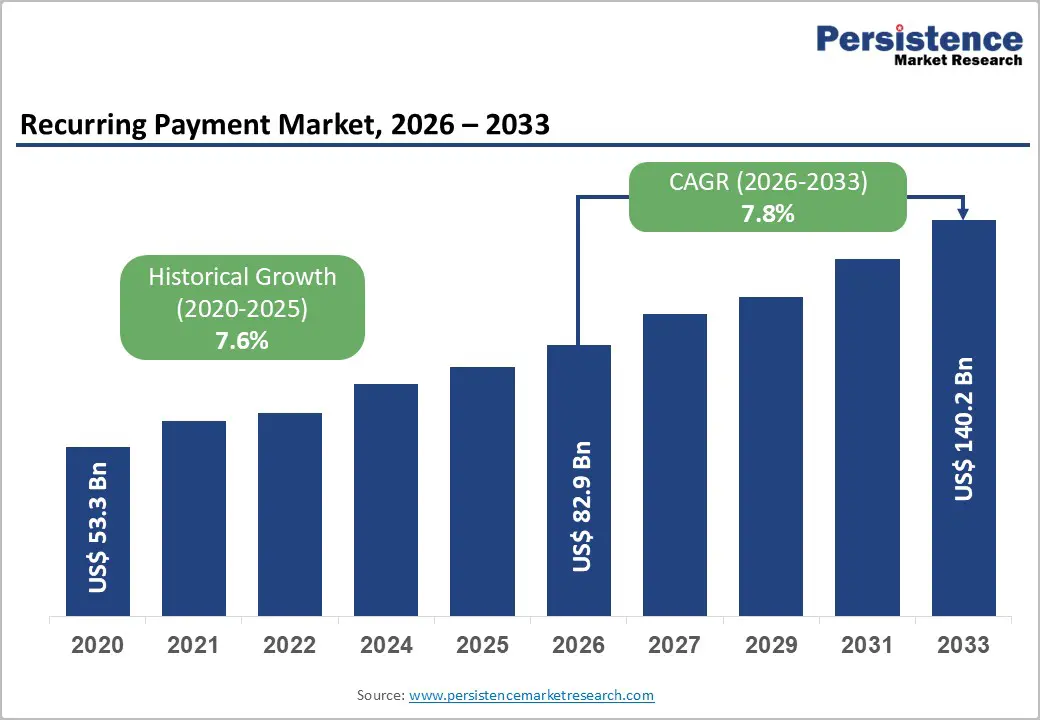

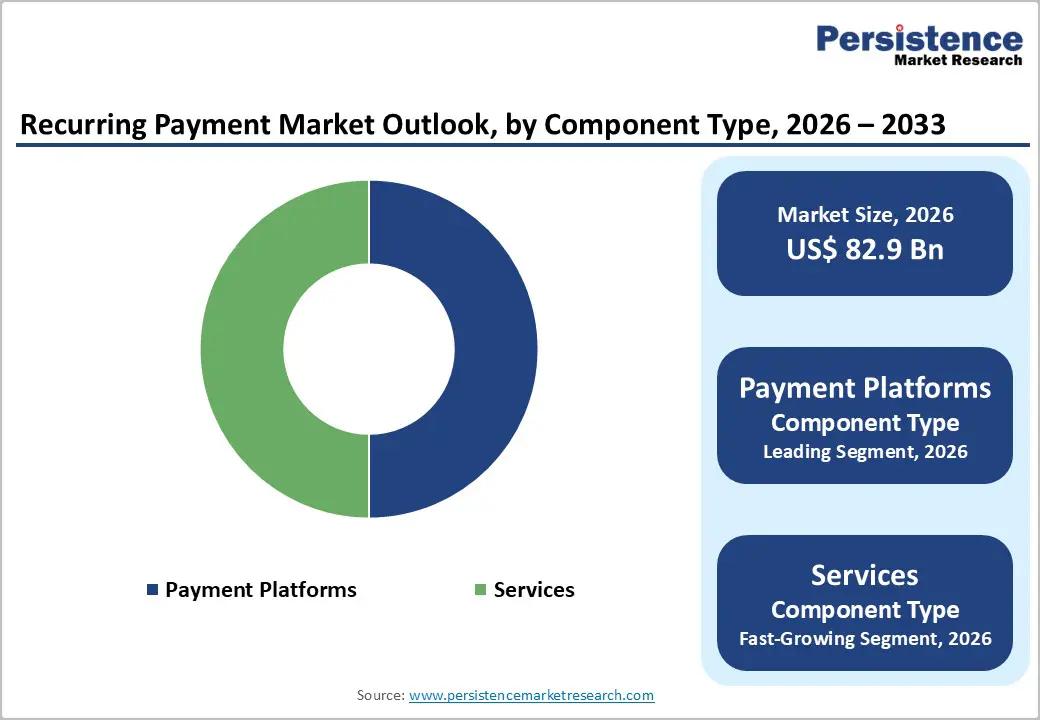

The global recurring payment market size is likely to be valued at US$82.9 billion in 2026, and is expected to reach US$140.2 billion by 2033, growing at a CAGR of 7.8% during the forecast period from 2026 to 2033, driven by the increasing prevalence of subscription-based business models, rising adoption of digital wallets and automated billing, and growing consumer preference for convenient, seamless recurring transactions across SaaS, streaming, e-commerce, and utilities.

The growing demand for recurring payment platforms, particularly in B2C subscriptions, is driving rapid adoption. Key advancements in tokenization, PCI-DSS compliant gateways, and smart retry logic are enhancing authorization rates and reducing churn. Recognized as essential for predictable revenue and customer retention, recurring payment solutions are fueling growth in the emerging subscription economy.

Key Industry Highlights:

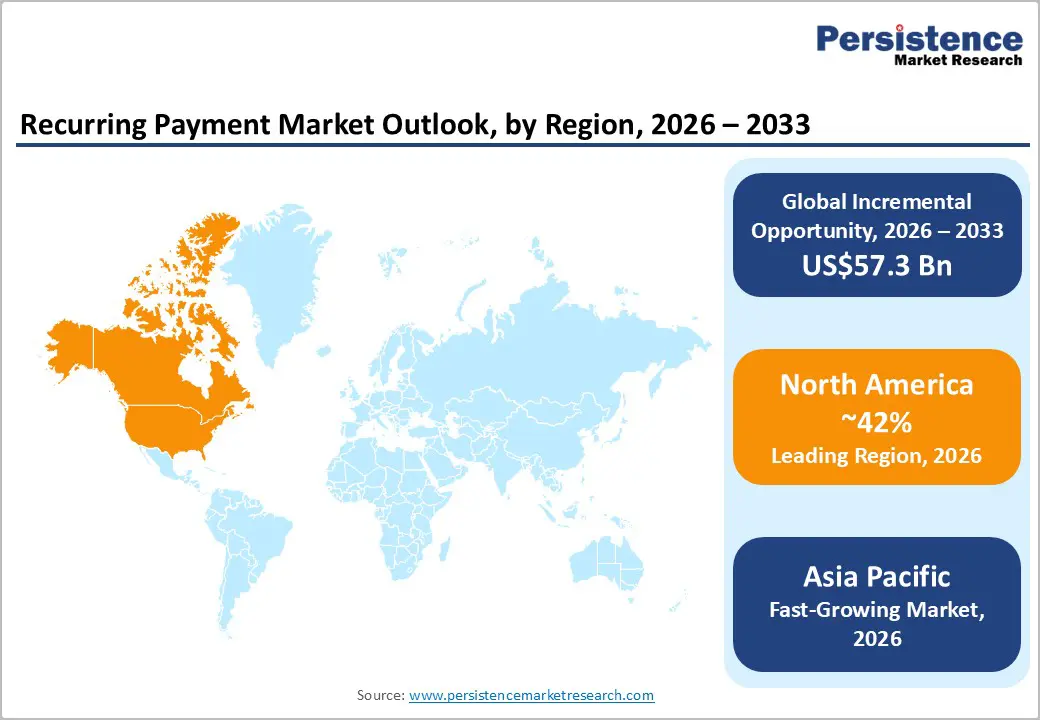

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by early subscription model adoption, strong SaaS presence, and high digital payment penetration in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by explosive growth in digital subscriptions, rapid e-commerce expansion, and increasing recurring billing acceptance in China and India.

- Dominant Component Type: Payment platforms, to hold approximately 58% of the market share, as they remain the core infrastructure for recurring billing.

- Leading Payment Type: Fixed, to contribute nearly 68% of the market revenue, due to dominance in SaaS, streaming, and membership models.

| Key Insights | Details |

|---|---|

|

Recurring Payments Market Size (2026E) |

US$82.9 Bn |

|

Market Value Forecast (2033F) |

US$140.2 Bn |

|

Projected Growth CAGR (2026-2033) |

7.8% |

|

Historical Market Growth (2020-2025) |

7.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis – Explosion of Subscription Economy and Digital Payment Adoption

Rapid adoption of digital payment infrastructure has significantly expanded the addressable market for automated billing and recurring transactions. India’s central bank data shows that digital methods now account for 99.8% of total transaction volume and 97.7% of total transaction value in the first half of 2025, illustrating near-universal use of cashless payments across the economy and widespread readiness for automated debits and credits tied to subscription services. Integrated real-time payment systems such as the Unified Payments Interface (UPI) handle a dominant share of these transactions, with UPI alone making up about 85% of all digital payment volumes, indicating both consumer comfort with digital mandates and the scalability of platforms that can support recurring charges without manual intervention.

This pervasive digital payment environment lowers barriers for consumers to sign up for subscription models from media and software services to utility billing and digital memberships by enabling seamless, secure, and instant payments at regular intervals. Government-backed initiatives and regulatory frameworks that promote interoperable and inclusive digital payments strengthen trust and participation in recurring payment ecosystems, encouraging businesses to adopt subscription pricing models and reducing churn through dependable automated collections.

B2B Recurring Models and Embedded Finance

B2B recurring models and embedded finance are transforming how businesses buy and sell services by shifting one-time transactions toward ongoing revenue streams and integrating financial services directly into business workflows. In a B2B context, companies increasingly prefer subscription-based access to software, platforms, and services such as cloud infrastructure, analytics, and supply-chain solutions. This model provides predictable revenue for sellers and predictable cost structures for buyers, simplifying budgeting and strengthening long-term client relationships. Because recurring billing aligns economic incentives across the customer lifecycle, rewarding customer success rather than one-off sales, companies are investing in systems that automate invoicing, collections, and renewals to support scalability.

Embedded finance further accelerates this shift by placing financial capabilities such as payments, credit, and reconciliation directly within business applications. For example, a procurement platform might offer integrated payment processing and financing terms at the point of purchase, eliminating the need for firms to cobble together separate systems or rely on external banks. This reduces friction, shortens sales cycles, and enhances liquidity management for both buyers and sellers. As embedded finance matures, B2B ecosystems increasingly offer tailored credit lines, dynamic settlement options, and real-time cash-flow tools that are native to core business processes.

Barrier Analysis - Regulatory Complexity and Compliance Costs

Growing regulatory complexity and the associated compliance costs have emerged as notable restraints on the recurring payments market, particularly for firms scaling subscription services across multiple jurisdictions. Operating in highly regulated environments such as financial services requires businesses to adhere to stringent rules around customer data protection, Anti-Money Laundering (AML), Know Your Customer (KYC) norms, and periodic reporting, which often necessitate investment in specialized personnel, systems, and audits. These obligations can divert time and resources away from product innovation and customer acquisition, slowing the pace at which recurring payment products can be developed and deployed.

Broad regulatory requirements also translate into financial burdens, especially for smaller providers. Official government data shows that compliance tasks in regulated sectors may consume close to 20% of total labor input for firms subjected to extensive oversight, reflecting significant internal resource allocation toward regulatory adherence. In complex markets such as India, small and medium enterprises confront hundreds of unique regulatory obligations annually, with total compliance costs reaching around ?13 lakh per unit each year, elevating operational expenses and reducing margins for companies managing recurring payment solutions.

Payment Failure Rates and Churn Risk

High payment failure rates present a meaningful challenge for the recurring payments market, directly influencing customer retention and revenue stability. In subscription-based and automated billing environments, transactions that fail due to expired cards, insufficient funds, or authentication issues can interrupt service delivery and create friction for customers. When a payment attempt is declined and not swiftly resolved, the customer’s access to the service may be suspended, which can trigger dissatisfaction and increase the likelihood that they choose to cancel the subscription altogether. For businesses, frequent payment interruptions translate into uncollected revenue and higher operational costs associated with retries, customer outreach, and debt recovery efforts.

Churn risk escalates when customers encounter repeated payment issues during the renewal process, especially if they must manually update payment credentials or re-authorize bank mandates. Even loyal users can disengage if they perceive the billing experience as cumbersome or unpredictable, undermining the lifetime value that recurring revenue models seek to capture. A key contributor to payment failure is the complex landscape of card networks and authentication standards, which can lead to inconsistent authorization outcomes across regions and customer segments. Reducing failure rates requires investments in intelligent retry logic, real-time payment notifications, and integrations with multiple payment methods to offer fallback options.

Opportunity Analysis - Growth in Intelligent Billing and Churn-Reduction Platforms

Rapid improvements in billing intelligence and churn-reduction platforms present a strong opportunity for the recurring payments market by enhancing customer experience and stabilizing revenue streams. Smart billing systems can automatically adjust payment attempts based on historical success rates, offer proactive reminders, and support multiple payment methods, making it easier for subscribers to keep their services active. Embedded within digital payment ecosystems, these tools reduce friction at renewal points and provide real-time insights that help businesses anticipate and address declines before they result in service interruption or cancellation. Such capabilities are especially valuable in high-volume digital environments where small lapses in payment processing can trigger outsized churn.

Government and central bank data demonstrate the scale and penetration of digital payments infrastructure that these intelligent systems can leverage. India’s digital payment transactions surged from INR 2,071 crore in FY 2017-18 to INR 18,592 crore in FY 2023-24, indicating vast user adoption of electronic transactions that can be harnessed for recurring billing models. The Unified Payments Interface (UPI) has been a key driver of this trend, growing from INR 92 crore in FY 2017-18 to INR 13,116 crore in FY 2023-24, providing a large base of users familiar with digital payment authorizations. Platforms that integrate machine learning to optimize authorization timing and offer seamless re-mandate workflows can significantly reduce the incidence of failed payments, bolster lifetime value, and reduce churn across subscription services, utilities, and other recurring revenue models.

Embedded Recurring Payments

Embedded recurring payments refer to the seamless integration of automated billing functionality directly into digital products, services, or business workflows. Rather than directing customers to an external checkout or payment portal, enterprises embed the capability to save payment credentials, schedule regular charges, and manage subscriptions within the platforms their customers already use. This integration simplifies the user experience, lowers friction at onboarding and renewal stages, and helps maintain consistent cash flow for sellers by reducing the steps required to authorize periodic payments.

For merchants and service providers, embedded recurring payments mean less dependency on manual billing processes and fewer payment disruptions. When recurring payment logic is native to a platform, such as within a software dashboard, mobile app, or business management system, updates to billing information, payment retries, and notifications can be automated and tailored to real-time user behavior. This reduces decline rates and supports proactive engagement with customers who might otherwise lapse due to outdated payment details or unclear renewal prompts. From the customer perspective, the convenience of embedded recurring payments fosters stronger long-term relationships. Subscribers can manage preferences, view billing histories, and update funding sources without leaving the core service environment, which boosts transparency and trust.

Category-wise Analysis

Component Type Insights

Payment platforms are anticipated to dominate the market, accounting for approximately 58% of the market share in 2026. Their dominance stems from their ability to provide end-to-end payment orchestration, including subscription management, automated invoicing, tokenization, fraud detection, and multi-currency processing within a single infrastructure. Businesses prefer integrated platforms that can support card payments, bank debits, digital wallets, and real-time payment systems while offering analytics and reporting tools. These platforms also ensure regulatory compliance and security standards, reducing operational complexity. Stripe, Inc., which offers Stripe Billing, a comprehensive subscription and recurring billing solution used by thousands of businesses worldwide. Stripe’s tools let companies integrate recurring invoices, automate renewal charges, manage failed payments, and support usage-based pricing all through a single API, simplifying both developer implementation and ongoing operations.

The services segment are represent the fastest-growing component type, owing to many businesses are shifting from one-time sales to ongoing digital offerings that deliver continuous value. Companies across sectors such as cloud computing, software as a service (SaaS), streaming media, digital education, and professional services increasingly sell access rather than ownership. These service models rely on recurring payments to ensure stable cash flow and predictability. Customers benefit from continuous updates, support, and flexibility in subscription tiers, while providers can deepen long-term engagement. Salesforce, Inc., a global leader in cloud-based CRM and enterprise software. In its fiscal year 2025, Salesforce reported US$35.7 billion in subscription and support revenue, which includes ongoing cloud services that customers pay for on a recurring basis, highlighting how service-oriented offerings dominate its business model.

Payment Type Insights

The fixed segment is expected to dominate the market, contributing nearly 68% of revenue in 2026, supported by their simplicity and predictability for both businesses and customers. Under a fixed model, subscribers pay a set amount at regular intervals monthly, quarterly, or annually regardless of usage levels. This structure simplifies budgeting, reduces billing disputes, and enhances transparency. For providers, fixed pricing ensures steady cash flow and easier revenue forecasting. It also lowers administrative complexity compared to usage-based models. Adobe Inc. and its Adobe Creative Cloud suite, where customers pay a set monthly or annual fee for access to design and productivity tools rather than purchasing one-off software licenses. This fixed subscription model has helped Adobe build stable recurring revenue and deepen customer loyalty by offering continuous access to updates and cloud services.

The variable segment represents the fastest-growing payment type, driven by the align pricing with actual usage or consumption, offering flexibility that customers increasingly prefer. Under variable models, charges adjust based on metrics such as hours used, data consumed, transactions processed, or levels of service accessed, making them attractive for both businesses and end users who want to pay proportionally to value received. These dynamic billing structures are especially suited to cloud computing, metered services, and APIs, where usage can fluctuate widely. Amazon Web Services (AWS), AWS bills its cloud services on a pay-as-you-go basis, meaning customers are charged only for computing, storage, and bandwidth resources they actually consume, without long-term contracts or upfront fees, this aligns costs with usage rather than a fixed subscription.

Regional Insights

North America Recurring Payment Market Trends

North America is projected to dominate, account for nearly 42% of the global recurring payment market in 2026, driven by the region’s early subscription model adoption, strong SaaS ecosystem, and high public awareness of seamless billing benefits. Distribution systems in the U.S. and Canada provide extensive support for recurring payment programs, ensuring wide accessibility across payment platforms, fixed, and B2C populations. Increasing demand for intelligent, convenient, and easy-to-integrate forms is further accelerating adoption, as these formats improve authorization rates and reduce barriers associated with failed payments.

Innovation in recurring payment technology, including stable churn-prediction, improved tokenization delivery, and targeted B2B enhancement, is attracting significant investment from both public and private sectors. Government initiatives and PCI Security Standards Council campaigns continue to promote use against fraud risks, revenue leakage concerns, and emerging subscription threats, creating sustained market demand. The growing focus on variable grades and specialty uses, particularly for B2C and others, is expanding the target applications for recurring payments.

Europe Recurring Payment Market Trends

Europe is seeing a rise in awareness of the advantages of the subscription economy, supported by robust regulatory frameworks and government-driven digital payment initiatives. Countries such as the U.K., Germany, France, and the Netherlands have well-established fintech frameworks that support routine recurring payment use and encourage adoption of innovative billing delivery methods, including open-banking PSD2 solutions. These high-compliance formulations are particularly appealing for B2C populations, regulation-conscious merchants, and SaaS users, improving retention and coverage rates.

Technological advancements in recurring payment development, such as enhanced open-banking, application-targeted delivery, and improved variable grades, are further boosting market potential. European authorities are increasingly supporting research and trials for payments against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, secure options is aligned with the region’s focus on preventive fraud reduction and digital economy expansion. Public awareness campaigns and promotion drives are expanding reach in both B2C and B2B segments, while platforms are investing in compliance and novel variants to increase efficacy.

Asia Pacific Recurring Payment Market Trends

Asia Pacific is likely to be the fastest-growing market for recurring payments in 2026, driven by rising subscription awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting recurring payment campaigns to address digital economy growth and emerging subscription needs. Recurring payments are particularly attractive in these regions due to their scalable administration, ease of integration, and suitability for large-scale B2C and SaaS drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deploy recurring payments, which can withstand challenging regulatory conditions and minimize failure dependence. These innovations are critical for reaching domestic merchants and improving overall subscription coverage. Growing demand for payment platforms, fixed, and B2C applications is contributing to market expansion. Public-private partnerships, increased digital expenditure, and rising investment in payment research and infrastructure are further accelerating growth. The convenience of recurring payment delivery, combined with improved retention and reduced risk of involuntary churn, positions it as a preferred choice.

Competitive Landscape

The global recurring payment market features competition between established payment giants and emerging billing specialists. In North America and Europe, Stripe and Adyen lead through strong R&D, distribution networks, and merchant ties, bolstered by innovative platforms and dunning programs. In Asia Pacific, local players advance with localized gateway solutions, enhancing accessibility. Payment platform delivery boosts authorization rates, cuts churn risks, and enables mass integrations across subscriptions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Variable formulations solve flexibility issues, aiding penetration in usage-based segments.

Key Industry Developments:

- In October 2025, Recurly, a leading subscription growth platform, launched its Fall Release, introducing Recurly Compass, an AI-powered subscription strategist. This release positioned Recurly as the industry’s first true subscription growth engine, helping brands scale and retain subscribers in the growing subscription economy.

- In July 2024, Finix, a full-stack payment processor, launched Recurring Billing on its dashboard. The new no-code solution allowed businesses to easily set up and manage recurring payments.

Companies Covered in Recurring Payment Market

- PayPal

- Stripe

- Square

- Adyen

- Braintree

- Authorize.Net

- Recurly

- Chargebee

- Zuora

Frequently Asked Questions

The global recurring payment market is projected to reach US$82.9 billion in 2026.

Increasing adoption of subscription models across industries such as SaaS, streaming media, digital education, fintech, and utilities is driving demand for automated recurring billing systems.

The recurring payment market is poised to witness a CAGR of 7.8% from 2026 to 2033.

The adoption of artificial intelligence in payment systems creates opportunities to reduce failed transactions, predict churn, and optimize retry strategies.