- Food and Beverages

- Pretzel Salts Market

Pretzel Salts Market Size, Share, and Growth Forecast, 2026 - 2033

Pretzel Salts Market by Product Type (Natural, Iodized), Application (Baked Goods, Cereals, Dry Blends, Seasonings, Meat, Poultry, Fishy), Distribution Channel (Indirect Sales (B2C), Direct Sales (B2B), Hypermarkets/Supermarkets, Online Stores, Specialty Stores), and Regional Analysis for 2026 - 2033

Pretzel Salts Market Share and Trends Analysis

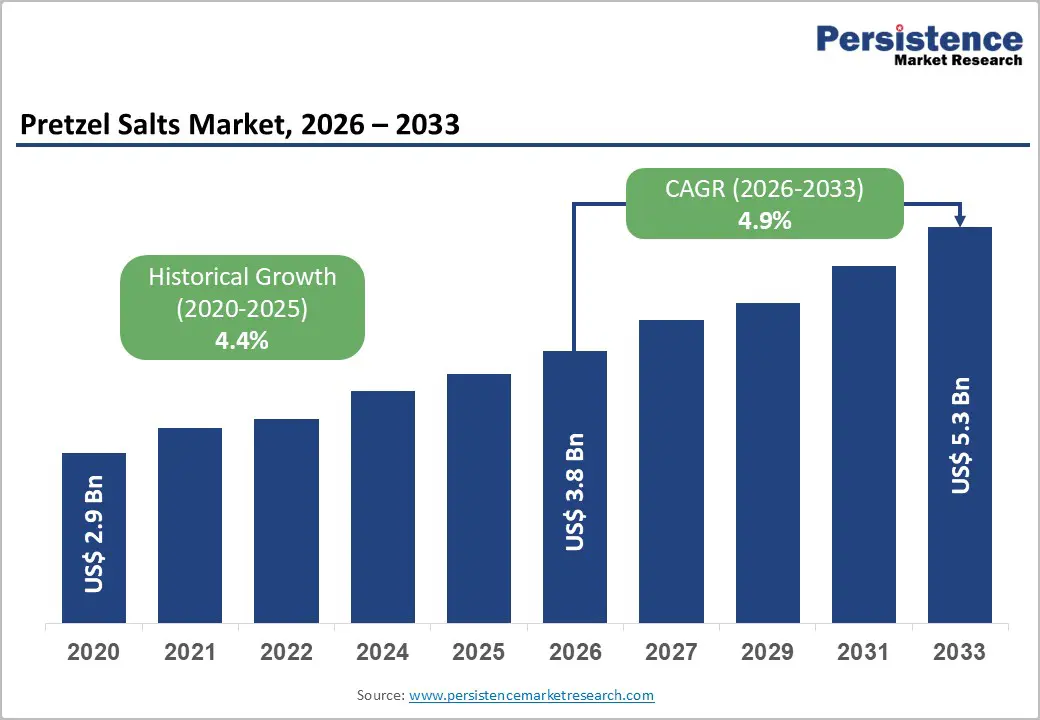

The global pretzel salts market size is likely to be valued at US$ 3.8 billion in 2026, and is projected to reach US$ 5.3 billion by 2033, growing at a CAGR of 4.9% during the forecast period 2026−2033. Demand for pretzel salts is expanding due to rising consumption of baked snacks and processed foods, reflecting increasing urbanization, rising disposable income, and evolving consumer taste preferences. Urban population growth and changing demographics are stimulating snack consumption, particularly in developed and emerging economies, which drives demand for standardized seasoning ingredients such as pretzel salts.

Technological integration in food processing is enabling consistent salt particle size, controlled moisture content, and improved shelf-life, enhancing product acceptance among manufacturers. Regulatory frameworks for food safety and hygiene are increasingly stringent, prompting manufacturers to adopt standardized salts, which fosters market growth. Distribution network modernization, including e-commerce platforms and hypermarket penetration, improves accessibility to both small- and large-scale food producers.

Key Industry Highlights

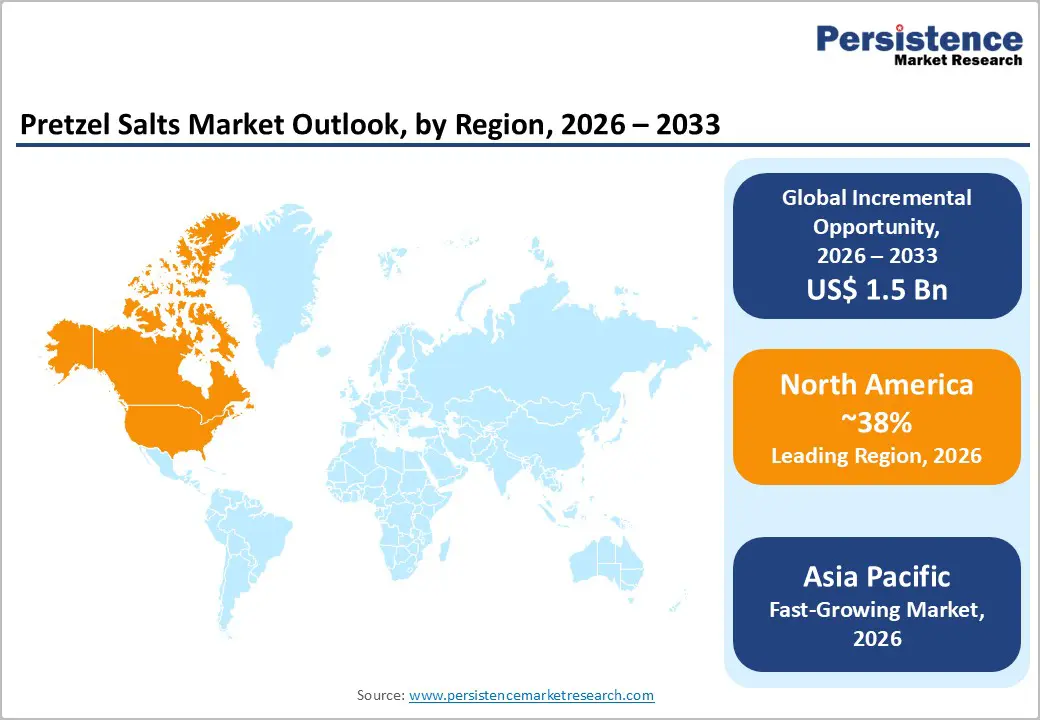

- Dominant Region: North America is projected to lead with 38% market share in 2026, driven by strong snacking demand and retail reach.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by rising snack demand and urbanization.

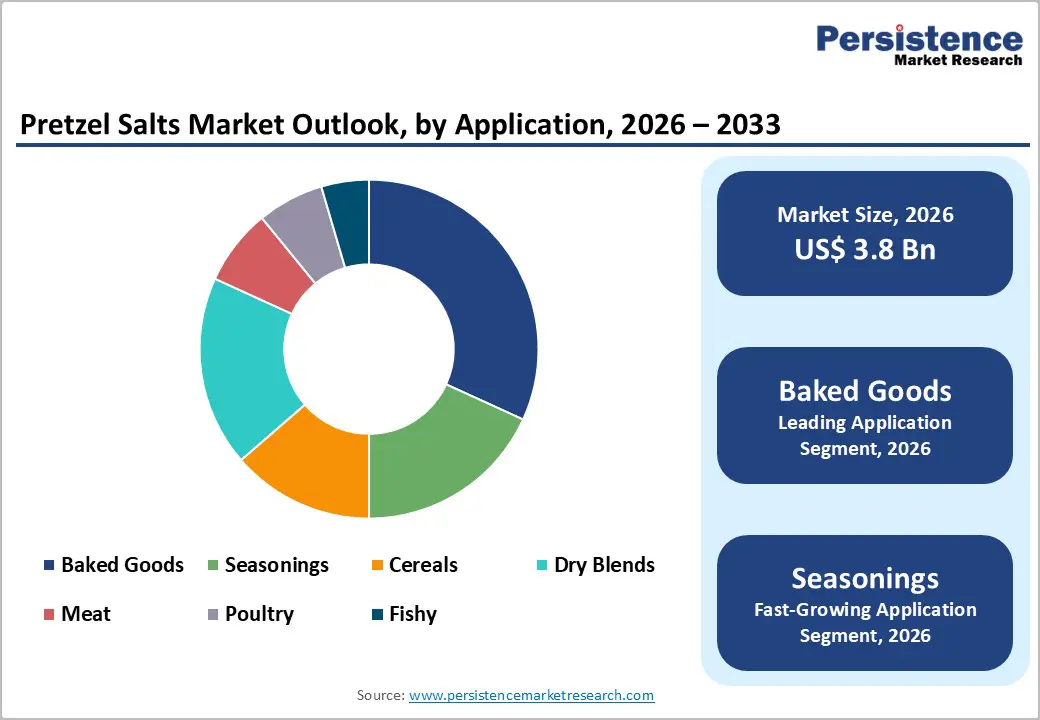

- Leading Application: Baked goods are set to lead with over 35% market share in 2026, supported by flavor, texture, and shelf-life benefits.

- Fastest-growing Application: Seasonings are expected to be the fastest-growing segment from 2026 to 2033, fueled by customizable flavors and fortified salts.

| Key Insights | Details |

|---|---|

|

Pretzel Salts Market Size (2026E) |

US$ 3.8 Bn |

|

Market Value Forecast (2033F) |

US$ 5.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Demand from Snack and Baked Goods Industries

Strong consumer expenditure patterns in 2025 illustrate persistent demand for food products sold through retail and food services channels, with U.S. Census Bureau data showing total retail and food services sales up 3.7% year over year in 2025. Frequent purchase occasions for snacks and baked goods contribute materially to this sustained sales momentum, expanding shelf-stable and fresh categories that require ingredient inputs at scale. Manufacturers across food processing operations adjust formulations to maintain consistent taste, quality, and texture, resulting in higher utilization rates of seasoning and functional components. Salt selection and application influence key sensory attributes and shelf profile of finished products, influencing production decisions in high-volume snack and bakery lines targeted at both grocery and food service distribution networks.

Consumption patterns shaped by lifestyle shifts favor convenience, portability and diversified flavor experiences, prompting food producers to broaden their offerings. These structural shifts in consumer behavior are reflected in broad retail sales performance, with food services and related product categories contributing to overall growth in consumer spending. In response to heightened competition and margin pressure, producers refine operational processes to balance cost, product quality and ingredient performance, reinforcing the strategic emphasis on ingredient sourcing.

Growth in Premium and Gourmet Pretzel Products, Increasing Specialty Salt Use

Premium and gourmet snack products cater to evolving consumer preferences for quality, taste differentiation, and experiential eating occasions, which increases the application of unique and artisanal salt varieties in seasoning and finishing processes. Higher income consumers often equate premium ingredients with superior sensory appeal and dining value, shifting purchase decisions toward products that provide distinctive textures and flavors. Manufacturers and chefs incorporate salts with specific mineral compositions, colors, or flavor infusions into premium snacks to align with these trends, ensuring products stand out in crowded retail and foodservice channels. This trend supports pricing strategies that justify higher margins and reinforce brand positioning around quality, craftsmanship, and gastronomic appeal.

The demand for differentiated sensory experiences has reshaped product development in finished goods, leading producers to adopt specialty salts that enhance crunch, flavor layering, and visual appeal for premium snacks. In professional kitchens and upscale foodservice, chefs select artisanal salt types to elevate presentation and tailor taste profiles, driving adoption upstream in supplier networks. Parallel shifts in consumer search behavior and retail assortment show increasing interest in gourmet and international snack categories, underscoring sustained consumer engagement with premium foods.

Fluctuations in Raw Material Prices and Supply Chain Vulnerabilities

Cost instability for key inputs and fragile distribution networks are a major restraint because they directly reduce operational predictability and inflate procurement budgets. Salt extraction and processing are energy-intensive activities with input costs linked to fuel, electricity, and labor. When fuel or energy prices shift rapidly, processing expenses can move in tandem, forcing producers to adjust selling prices to maintain margins. For example, authoritative data from the U.S. Geological Survey (USGS) show the average unit value of salt products in the United States changed across different types in 2025, indicating price movements even for basic commodities such as solar and rock salt in that year.

Logistics constraints further exacerbate cost volatility through dependencies on transport networks that are sensitive to external shocks, including weather events, strikes or geopolitical disruptions. Transit bottlenecks increase lead times and inventory carrying costs, eroding service levels for retailers and manufacturers alike. In global supply chains, reliance on a limited number of major producers for bulk shipments means that interruptions at production sites quickly propagate to downstream buyers, compressing availability and pushing spot prices upward. Tightening transportation capacity and fluctuating freight rates also elevate the total cost of bringing salt from production hubs to processing centers and end markets.

Competition from Alternative Seasoning Options

Limited consumer preference for traditional salt seasonings stems from a broader shift in eating behavior that is reshaping flavor choices at a category level. By 2025, average sodium intake in the U.S. remains at about 3,400 mg per day compared with the recommended 2,300 mg per day, according to draft voluntary sodium reduction goals published by a national food regulatory agency, a clear indicator that consumers and policymakers are actively targeting sodium reduction in processed foods. This focus has driven snack brands to diversify seasonings and promote alternatives such as herbs, spices, salt substitutes and flavor blends that offer satisfying taste profiles with perceived health benefits, reducing reliance on coarse salt alone.

Eating occasions and competitive product formats further divert share from conventional salts. Snack categories such as baked vegetable crisps, seasoned nuts, and nutrient-fortified chips offer complex seasonings that resonate with health and taste priorities, diluting the appeal of single-note salt toppings. Consumers drawn to novel spice combinations or perceived healthier seasoning alternatives allocate discretionary snack spend toward these emerging choices, diminishing repeat consumption of classic salt applications. This behavioral shift intensifies marketplace competition, compelling producers to recalibrate product portfolios and invest in seasoning innovation that aligns with evolving taste preferences and regulatory sodium reduction trends, placing pressure on legacy salt formulations to maintain relevance in a crowded snacking ecosystem.

Collaborations with Bakery and Snack Manufacturers to Offer Customized Salt Blends

Strategic partnerships between snack producers and seasoning innovators enable development of tailored seasoning solutions that directly address specific product profiles and regional taste preferences. Retail buyers and foodservice chains increasingly seek distinct flavor experiences that differentiate offerings on shelf and drive premium pricing. Co-creation with bakery and snack manufacturers supports development of innovative grain sizes, infusion techniques, and flavor combinations that resonate with evolving consumer palates while allowing for customized seasoning solutions that enhance product appeal.

Working closely with processed food manufacturers accelerates product innovation cycles and reduces time to market for new seasoning blends tailored to emerging trends. Government initiatives promoting healthier food options encourage formulation of seasoning profiles that maintain taste appeal while supporting nutritional guidance. Such alignment with public policy can enhance brand reputation and open channels with health-focused retailers and foodservice operators.

Increasing Focus on Organic and Natural Salts as Part of Clean-Label Products

Consumer demand for organic and natural ingredients drives innovation in clean-label offerings, reflecting a shift toward transparency and minimal processing in food production. Clean-label positioning communicates simplicity, familiarity, and quality, strengthening brand credibility in health-conscious segments. Certified organic salts appeal to consumers seeking products free from artificial additives, creating a perceived premium and health benefit. Regulatory frameworks supporting organic certification ensure consistency and reliability of ingredient sourcing, reinforcing consumer trust and compliance with industry standards. Companies adopting these inputs can differentiate offerings while meeting evolving regulatory expectations for labeling and product composition.

Sustainability considerations reinforce demand, as organically produced salts reduce environmental impact compared to conventional sources. Traceability from certified farms allows companies to communicate origin and production practices effectively, appealing to urban and premium-oriented shoppers. Integration of natural salts enables premium positioning, supports reformulation initiatives targeting health-conscious consumers, and aligns with lifestyle trends emphasizing functional, clean-label snacks.

Category-wise Analysis

Product Type Insights

Natural salts are likely to be the leading segment with an estimated 55% of the pretzel salts market revenue share in 2026, driven by strong adoption across baked goods, seasonings, and meat processing applications. Its widespread acceptance is supported by consumer preference for minimally processed ingredients and regulatory approval for food-grade applications. Manufacturers favor natural salt for consistent taste, reliability in formulations, and compatibility with existing production equipment. Accessibility through established supply chains ensures availability for both industrial and retail applications. Technological improvements in refining and packaging enhance purity and shelf life, further reinforcing its dominance.

Iodized salts are expected to witness the fastest growth between 2026 and 2033, as regulatory encouragement for iodine fortification increases and health-conscious consumer preferences expand. Food processors increasingly incorporate iodized salt to comply with nutritional regulations and cater to health-conscious consumers. Technological advancements allow precise iodization, maintaining taste and stability in baked products, cereals, and seasonings. Accessibility through both B2B and retail distribution channels supports scaling, while fortification programs provide regulatory alignment. Innovation in value-added iodized blends enables tailored applications for meat, poultry, and dry seasoning mixes. Adoption is further enhanced by growing digital commerce channels, which expand consumer reach and facilitate direct engagement with health-focused product lines.

Application Insights

Baked goods are poised to lead with an estimated 35% of the pretzel salts market share in 2026, owing to the widespread use of pretzel salts for flavor enhancement, texture consistency, and shelf-life stabilization. Bakeries and large-scale food manufacturers prefer standardized salts to maintain uniform taste across production batches. Regulatory approval for food-grade salts in baked goods ensures compliance with safety standards while supporting mass adoption. Consumer trust in fortified and high-quality ingredients strengthens demand, particularly in products such as pretzels, crackers, and specialty breads. Distribution through modern retail, online channels, and foodservice networks ensures broad accessibility and consistent supply. Technological integration in baking processes, including precise mixing and dosing systems, enhances efficiency and product quality.

Seasonings are anticipated to be the fastest-growing segment between 2026 and 2033, driven by increasing adoption of value-added culinary products and customizable flavor blends. Pretzel salts are incorporated into dry spice mixes, snack coatings, and processed meat seasonings to enhance taste and provide fortification benefits. Consumer interest in ready-to-use culinary solutions and digital commerce channels enables rapid scaling across retail and foodservice sectors. Regulatory alignment for fortified salts facilitates innovation in seasoning blends while ensuring compliance. Manufacturers benefit from flexible integration of pretzel salts into diverse seasoning formats, improving product differentiation and market appeal. Adoption is further supported by supply-chain advancements that ensure timely delivery and product quality.

Regional Insights

North America Pretzel Salts Market Trends

North America is expected to lead with an estimated 38% of the pretzel salts market value in 2026, supported by advanced food processing infrastructure, strong regulatory frameworks, and high consumer awareness. The United States and Canada drive this dominance with well-established snacking cultures that consistently fuel demand for baked and seasoned products. Extensive retail networks, including supermarkets, convenience stores, and e-commerce platforms, ensure widespread availability and visibility for a wide range of seasoning variants. Long-standing brand portfolios and continuous flavor innovation enable rapid adoption of premium salt formulations that enhance texture, appearance, and taste, generating strong consumer loyalty and recurring purchase cycles.

Ingredient innovation represents a critical differentiator supporting leadership. Companies in the United States and Canada invest in research and development to create gourmet blends, specialty salts, and textural variants tailored for premium positioning, optimizing flavor release and sensory experience in baked goods. Integration across foodservice channels, including quick-service outlets, casual dining, and experiential restaurants, amplifies demand for consistent, high-performance seasoning solutions. Strategic retail promotions aligned with seasonal events, sports, and cultural occasions further stimulate sales.

Europe Pretzel Salts Market Trends

Europe maintains a significant position in the pretzel salts market, supported by established snacking habits, high per-capita consumption of baked products, and mature retail infrastructure. Countries such as Germany, France, and the United Kingdom drive demand through widespread adoption of seasoned baked goods across supermarkets, convenience formats, and online channels. Innovation in flavor and texture profiles, including gourmet and specialty salts, enhances product differentiation and stimulates premiumization. Well-developed logistics and cold chain networks ensure consistent product availability and quality, enabling rapid market response to seasonal trends and consumer preferences.

Sustainability initiatives and regulatory compliance frameworks play a critical role in market dynamics, with strict food safety standards and quality certifications shaping ingredient sourcing and manufacturing practices. Investment in research and development allows producers to experiment with reduced-sodium formulations, natural salts, and functional blends that cater to health-conscious consumers. Partnerships with bakeries, quick-service outlets, and gourmet snack providers create downstream demand for specialized salts and provide platforms for premium ingredient integration. Increasing interest in traceability and clean-label attributes further encourages adoption of certified and natural salt variants, aligning with evolving consumer expectations.

Asia Pacific Pretzel Salts Market Trends

Asia Pacific is forecasted to be the fastest-growing market for pretzel salts between 2026 and 2033, stimulated by rising processed food consumption, increasing retail modernization, and regulatory encouragement for fortified salts. China, India, and Japan are leading this growth trajectory due to evolving consumption patterns and rapid urbanization that drive demand for convenient, on-the-go snacking options. Exposure to global flavors and Western-style products is catalyzing the adoption of seasoned and textured ingredients, while modern retail formats, including large grocery chains and e-commerce platforms, enhance product accessibility and accelerate time-to-market for innovative salt variants. Food manufacturers are strategically reformulating portfolios to include premium seasoning elements that elevate sensory appeal while aligning with local taste preferences, supported by investments in pilot production lines and application laboratories.

Policy frameworks and regulatory support for food quality and fortification standards are critical structural drivers of market expansion. Simplified import procedures and certification harmonization reduce entry barriers for specialty salts, enabling premium ingredient penetration. Rising disposable incomes are shifting expenditure toward value-added and premium snack categories, allowing manufacturers to price innovative seasoning solutions at higher margins. Collaborative initiatives between global suppliers and domestic processors accelerate capability transfer, enabling faster uptake of textural and flavor innovations previously limited to mature markets.

Competitive Landscape

The global pretzel salts market structure is moderately consolidated, with leading suppliers such as Cargill, Morton Salt, SaltWorks, Windsor Salt, Kensalt, and American International Foods collectively controlling an estimated 55% of total market share. These players dominate through extensive distribution networks, established relationships with industrial and artisanal bakers, and consistent adherence to food safety and quality standards. Smaller regional manufacturers contribute to the remaining share, serving local bakeries, specialty snack producers, and niche segments. Product portfolios in the market include standardized, value-added, and fortified salts, enabling differentiation across flavor, texture, and functional attributes.

Competitive strategies emphasize reliability, product quality, and compliance with regulatory frameworks, allowing leading suppliers to maintain strong positioning in both industrial and artisanal channels. Investment in research and development facilitates introduction of gourmet blends, specialty salts, and textural variants that enhance sensory experience, supporting premiumization and brand differentiation. Partnerships with bakeries, foodservice providers, and distributors ensure consistent market penetration, while operational efficiency and logistics capabilities create cost advantages over smaller competitors.

Key Industry Developments

- In August 2025, Pretzelized introduced Sea Salt Pretzel Snackers, a light, crisp twist on classic pretzels now sold nationwide in single-serve multipacks that combine a crunchy pretzel exterior with a cracker-like interior and are free from common allergens such as nuts, sesame, soy, and dairy.

- In April 2025, Oreo launched a limited-time Chocolate Covered Pretzel flavor nationwide, featuring pretzel-flavored cookies topped with salt and a chocolate-flavored crème filling in a first-ever sweet-and-savory cookie offering.

- In March 2025, Kellanova introduced Rice Krispies Treats Bliss bars, a new sweet-and-salty snack featuring marshmallow and crispy rice topped with chocolate or caramel and candied sea salt pretzels that will roll out nationwide in April.

Companies Covered in Pretzel Salts Market

- Cargill, Incorporated.

- Morton Salt, Inc.

- SaltWorks

- Windsor Salt Ltd.

- Kensalt Ltd

- American International Foods, Inc.

- SAN FRANCISCO SALT CO

- Hoosier Hill Farm.

- Jacobsen Salt Co.

Frequently Asked Questions

The global pretzel salts market is projected to reach US$ 3.8 billion in 2026.

Rising demand for seasoned and flavored snacks, premiumization, and expanding retail and foodservice channels are driving the market.

The market is poised to witness a CAGR of 4.9% from 2026 to 2033.

Innovation in gourmet, organic, and fortified salts, along with clean-label trends and expanding emerging markets, represent key opportunities.

Some of the key market players include Cargill, Incorporated, Morton Salt, Inc., SaltWorks, Windsor Salt Ltd., Kensalt Ltd, and American International Foods, Inc.