- Specialty & Fine Chemicals

- Pivaloyl Chloride Market

Pivaloyl Chloride Market Size, Share, and Growth Forecast, 2026 - 2033

Pivaloyl Chloride Market by Purity Grade (High Purity, Standard Purity), Application (Pharmaceutical, Agrochemicals, Others), End-user Industry (Chemical, Pharmaceutical, Agriculture, and Others), and Regional Analysis 2026 - 2033

Pivaloyl Chloride Market Size and Trends Analysis

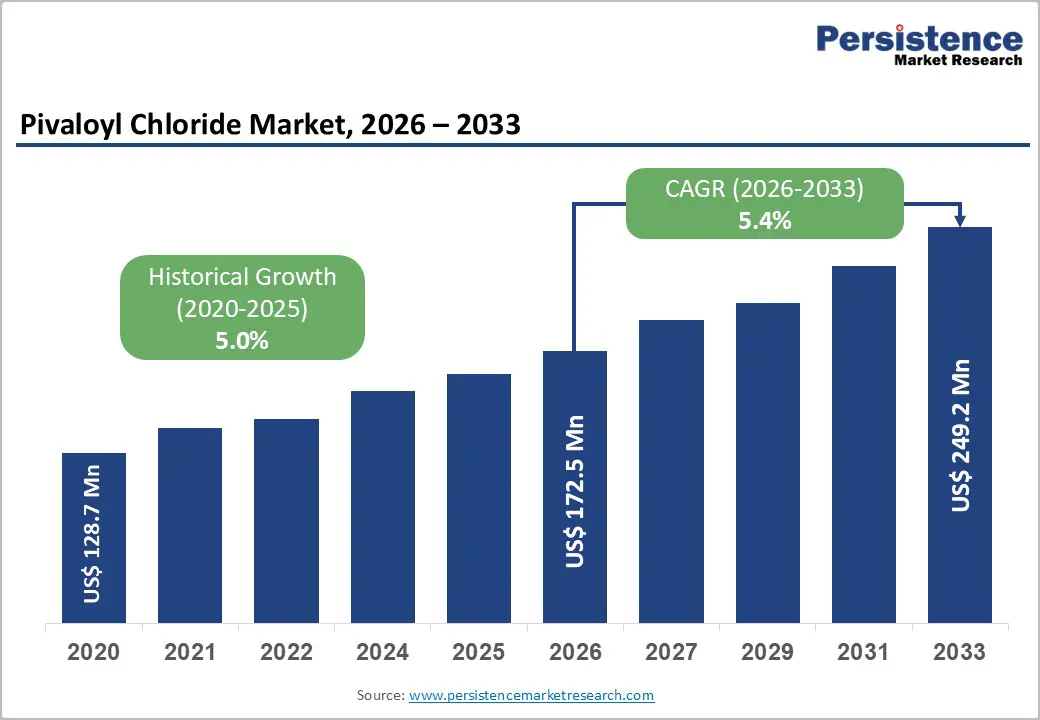

The global pivaloyl chloride market size is likely to be valued at US$172.5 million in 2026 and is expected to reach US$249.2 million by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033, driven by the rising demand in pharmaceuticals and agrochemicals, where it serves as a key acylation agent.

The market expansion is primarily fueled by the escalating demand for high-purity chemical intermediates in the pharmaceutical and agrochemical sectors. Pivaloyl chloride (also known as trimethylacetyl chloride) serves as a critical building block for a variety of Active Pharmaceutical Ingredients (APIs) and herbicides. The transition toward advanced synthesis methods in the Asia-Pacific region, coupled with the increasing prevalence of chronic diseases requiring specialized treatments, has solidified the compound's role in global supply chains.

Key Industry Highlights:

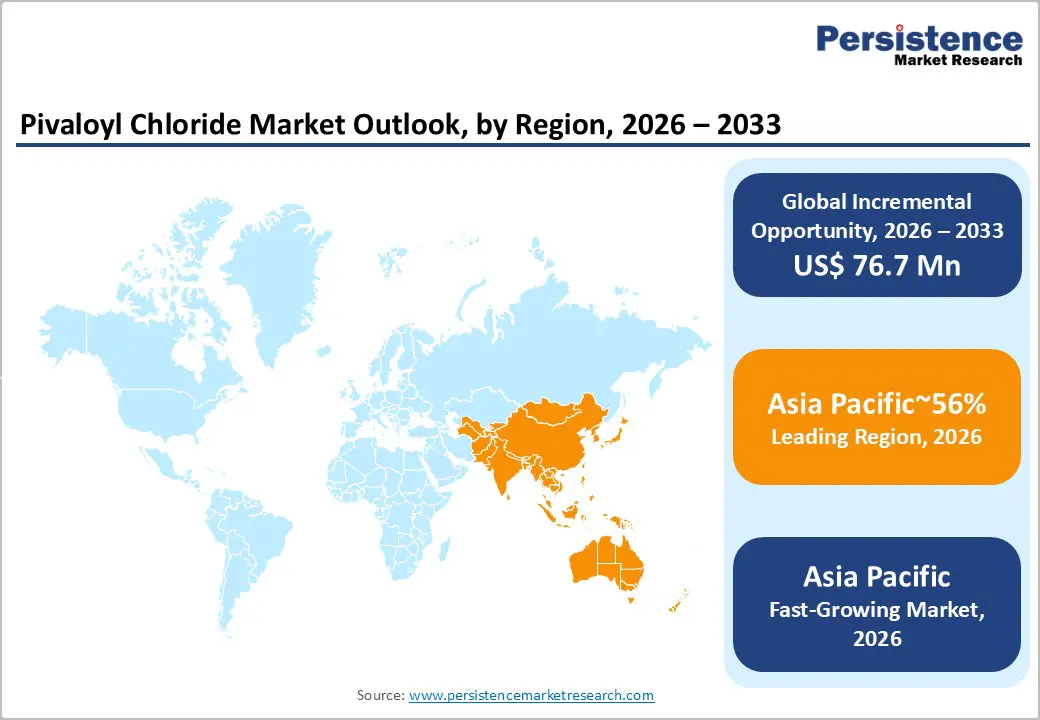

- Leading Region: Asia Pacific is projected to lead due to its unparalleled concentration of pharmaceutical and agrochemical manufacturing capacity, accounting for approximately 56% share in 2026, supported by high-purity distillation technologies, digitalized plant monitoring systems, and vertically integrated production networks.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest due to rapid industrial scaling, policy-driven investment incentives such as SEZ and chemical park expansions, and adoption across pharmaceutical and agrochemical sectors, enabling flexible high-purity intermediate production and export-oriented synthesis.

- Leading Purity Grade: The high purity segment is expected to lead, accounting for approximately 73% share in 2026 through entrenched pharmaceutical adoption, stringent reaction selectivity requirements, process consistency, and compatibility with high-value active pharmaceutical ingredient synthesis workflows.

- Leading End-user Industry: The chemical segment is projected to dominate for operational efficiency, functional versatility, industrial throughput, and cost-effective adoption across agrochemical and pharmaceutical production, holding approximately 49% share in 2026.

| Key Insights | Details |

|---|---|

|

Pivaloyl Chloride Market Size (2026E) |

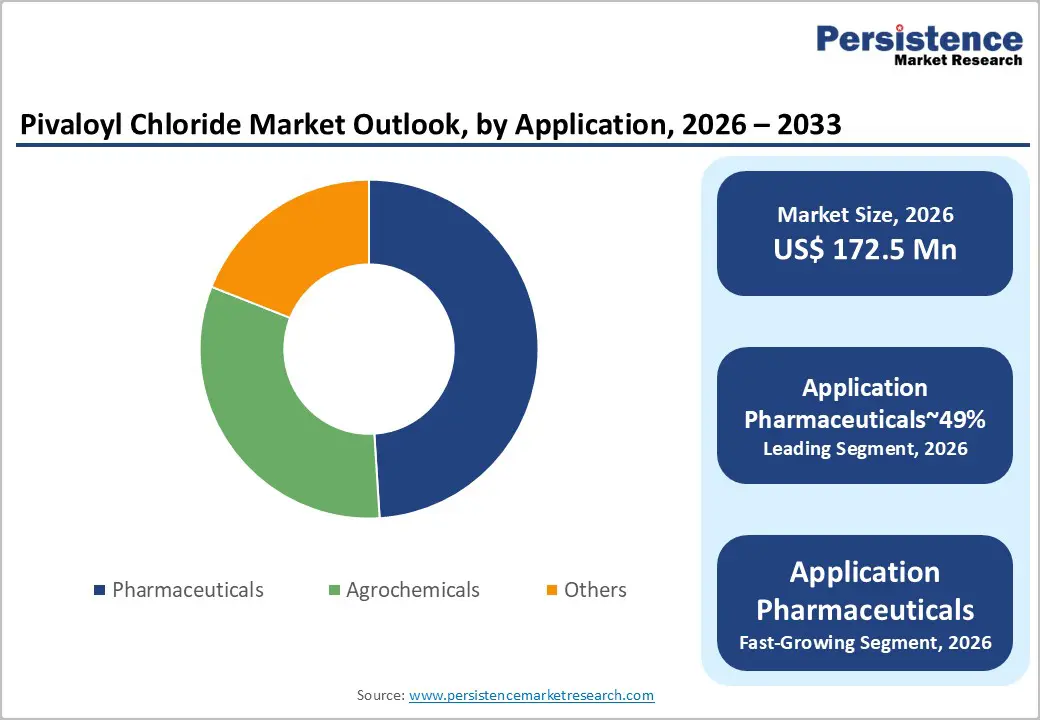

US$172.5 Mn |

|

Market Value Forecast (2033F) |

US$249.2 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expanding Pharmaceutical Active Ingredient Synthesis Supporting Demand for Pivaloyl Chloride

Rising pharmaceutical synthesis activity significantly strengthens demand for pivaloyl chloride across regulated drug manufacturing ecosystems globally. The compound functions as a critical acylating reagent within complex antibiotic and osteoporosis therapy synthesis pathways. Its steric hindrance characteristics stabilize reactive intermediates during multistep reactions requiring precise selectivity and yield optimization. Pharmaceutical producers rely on such reagents to protect functional groups during active ingredient synthesis. Expanding therapeutic demand for bone density treatments reflects demographic aging across developed and emerging healthcare markets. This structural healthcare transition increases production volumes for osteoporosis drugs requiring specialized chemical intermediates. Consequently, pivaloyl chloride consumption rises alongside pharmaceutical manufacturing expansion and therapeutic pipeline diversification.

Manufacturing models increasingly incorporate contract development and manufacturing organizations specializing in complex pharmaceutical intermediate synthesis. These facilities depend on high-purity reagents capable of supporting consistent reaction performance and regulatory-compliant drug production. Process efficiency considerations further elevate demand for intermediates, enabling predictable yields and reduced purification complexity. Pharmaceutical quality regulations require controlled synthesis pathways, reinforcing reliance on well-characterized specialty reagents such as pivaloyl chloride. Technological improvements in catalytic chemistry also expand feasible reaction routes utilizing sterically protective intermediates. These developments structurally embed pivaloyl chloride within pharmaceutical synthesis workflows, supporting antibiotics and bone-density treatments. Consequently, pharmaceutical sector expansion establishes a sustained demand foundation for the pivaloyl chloride market.

Transition toward Green Chemistry and Sustainable Chemical Manufacturing

The chemical manufacturing sector increasingly prioritizes environmentally responsible synthesis pathways to satisfy evolving regulatory frameworks. Green chemistry principles encourage the adoption of catalyst-driven reactions that maximize yield while minimizing hazardous byproduct generation. Such process innovations improve reaction efficiency during acylation and intermediate production, particularly when specialty reagents are used. Environmental compliance pressures are particularly strong across advanced chemical manufacturing economies, underscoring the need for sustainable industrial practices. Producers therefore redesign reaction pathways to reduce waste streams and improve solvent utilization during synthesis. These improvements support operational stability while aligning chemical production practices with broader environmental governance expectations. Consequently, demand strengthens for reagents compatible with high efficiency and environmentally optimized manufacturing routes.

Sustainable synthesis technologies also reshape production economics across specialty chemicals and pharmaceutical intermediates manufacturing segments. Catalyst-assisted processes enhance reaction selectivity, improving purity outcomes and reducing downstream purification requirements. Lower waste formation decreases treatment costs and simplifies compliance with environmental discharge standards governing chemical facilities. These efficiency gains strengthen cost competitiveness for producers operating within high-purity intermediate manufacturing environments. Market participants, therefore, increasingly integrate cleaner synthesis technologies to preserve margins while maintaining regulatory alignment. Continuous process optimization further supports scalability across fine chemical production without compromising product quality consistency. Such structural manufacturing shifts reinforce demand for reagents compatible with sustainable and precision-controlled synthesis.

Barrier Analysis - Moisture Sensitivity and Hydrolysis Risks Increasing Handling Complexity

Pivaloyl chloride is highly reactive with moisture, posing operational hazards during storage, transport, and processing. Contact with water initiates rapid hydrolysis, generating corrosive hydrogen chloride gas and significant heat release. These reaction characteristics impose strict requirements for moisture-controlled handling environments across chemical manufacturing facilities. Production units must maintain anhydrous conditions through sealed systems, inert atmospheres, and controlled humidity infrastructure. Such safety requirements increase the complexity of facility design and operational monitoring across intermediate chemical processing workflows. Regulatory compliance frameworks governing hazardous chemical management further intensify procedural oversight and workplace safety obligations. Consequently, operational risk management becomes a structural constraint that impedes broader adoption in certain manufacturing environments.

Handling sensitivity also increases capital and operating expenditures for storage, packaging, and logistics systems. Facilities must deploy corrosion-resistant materials, specialized containment vessels, and advanced ventilation systems to mitigate gas. Transportation regulations for reactive acyl chlorides require additional documentation, packaging certification, and hazardous-material handling protocols. These requirements increase procurement costs for downstream users integrating the compound within synthesis operations. Smaller manufacturers and laboratories often encounter infrastructure limitations when accommodating such stringent handling conditions. Risk mitigation investments, therefore, reshape cost structures across the intermediate chemical ecosystem using pivaloyl chloride. Collectively, these safety and infrastructure burdens constrain broader market expansion despite strong demand from pharmaceutical synthesis applications.

Infrastructure Corrosion and Specialized Material Requirements

Pivaloyl chloride exhibits aggressive corrosion of conventional industrial metals used in chemical processing infrastructure. Steel and iron components degrade rapidly when exposed to the compound, particularly under trace moisture conditions. This reactivity creates structural reliability concerns for pipelines, valves, storage vessels, and transfer systems. Manufacturing facilities must therefore avoid standard metallic equipment commonly used for handling organic intermediates. Instead, operators deploy corrosion-resistant containment systems engineered to withstand chemically reactive environments. These material limitations complicate infrastructure design across production plants, distribution terminals, and laboratory synthesis environments. Consequently, infrastructure compatibility challenges introduce operational constraints affecting broader industrial integration of pivaloyl chloride.

Specialized containment materials significantly increase capital expenditure associated with storage and transport logistics. Glass-lined vessels, advanced polymer containers, and fluorinated materials become necessary to ensure long-term chemical stability. Such equipment requires customized fabrication, rigorous inspection procedures, and controlled maintenance schedules during plant operations. Transport packaging standards also mandate chemically resistant materials that prevent container degradation during shipment cycles. These infrastructure adaptations raise procurement costs for manufacturers and downstream chemical processors. Maintenance complexity further increases due to inspection requirements, ensuring corrosion resistance remains uncompromised over time. Collectively, infrastructure compatibility constraints elevate operational costs and limit flexible deployment across conventional chemical manufacturing facilities.

Opportunity Analysis - Continuous Flow Manufacturing and Green Synthesis Integration

The chemical industry is increasingly adopting continuous-flow manufacturing to enhance safety, efficiency, and process stability. This production architecture enables controlled reagent exposure, improving reaction precision for sensitive intermediates such as pivaloyl chloride. Continuous processing reduces batch variability and supports consistent quality across pharmaceutical and fine chemical manufacturing. Integration of microreactor systems enables precise thermal control during highly reactive acylation processes. These systems limit hazardous material accumulation by maintaining smaller reaction volumes within closed environments. Reduced reaction inventory lowers operational risk associated with moisture-sensitive and reactive chemical intermediates. Consequently, continuous flow technologies create favorable conditions for safer and more efficient pivaloyl chloride synthesis.

Green chemistry frameworks further reinforce this opportunity by encouraging waste minimization and energy-efficient reaction pathways. Sustainable synthesis techniques prioritize higher selectivity reactions that reduce unwanted byproduct formation. Pharmaceutical manufacturers increasingly require environmentally responsible intermediates supporting low-emission production standards. Adoption of continuous manufacturing aligns with these sustainability expectations while improving resource utilization across chemical plants. Regulatory encouragement for cleaner industrial processes also strengthens incentives for technology modernization within specialty chemical production. Process intensification achieved through microreactor platforms enhances scalability without proportionally increasing the environmental burden. These developments collectively expand opportunities for sustainable pivaloyl chloride manufacturing within regulated pharmaceutical supply ecosystems.

Sustainable Agrochemical Formulations Supporting Intermediate Demand

Agricultural policy frameworks increasingly promote low-residue crop protection products to improve environmental safety. These regulatory shifts encourage reformulation of pesticides using intermediates compatible with cleaner synthesis pathways. Pivaloyl chloride functions as a valuable acylation reagent supporting selective modification of agrochemical active ingredients. Chemical producers integrate such intermediates to improve molecular stability and application efficiency in crop protection products. Policy emphasis on sustainable agriculture strengthens demand for environmentally responsible pesticide development across major farming economies. Agrochemical manufacturers, therefore, pursue intermediates enabling controlled reactivity and reduced residual toxicity after field application. This evolving regulatory environment expands opportunities for specialty reagents used in modern crop protection chemistry.

Technological convergence between synthetic chemistry and bio-based modifiers further reshapes agrochemical formulation strategies. Selective reaction pathways enable targeted molecular design that reduces ecological persistence and unintended environmental exposure. Such innovations support regulatory compliance while maintaining effectiveness against pests across diverse agricultural ecosystems. Research institutions and chemical producers collaborate to develop intermediates compatible with greener pesticide manufacturing processes. Enhanced selectivity during synthesis reduces waste generation and improves efficiency across agrochemical production facilities. These improvements strengthen sustainability credentials within global crop protection supply networks responding to environmental policy pressures. Consequently, demand grows for intermediates facilitating advanced, environmentally responsible agrochemical formulation development.

Category–wise Analysis

Purity Grade Insights

High purity is projected to lead, accounting for approximately 73% share in 2026, supported by its entrenched role in highly sensitive pharmaceutical synthesis workflows requiring extremely low impurity profiles and consistent reaction reliability. Adoption remains anchored in pharmaceutical active ingredient manufacturing, where acylation reactions demand stringent purity thresholds to maintain molecular stability and avoid degradation during multistep synthesis processes. Enterprises prioritize this grade for predictable reaction selectivity, improved yield stability, and compatibility with high-precision pharmaceutical manufacturing standards across regulated markets. Leading suppliers, including BASF SE, Merck KGaA, and CABB Group, position their high-purity portfolios to integrate tightly within pharmaceutical development ecosystems. This combination of mature infrastructure, validated process reliability, and entrenched pharmaceutical demand sustains the segment’s structural dominance.

High purity is expected to be the fastest-growing segment, driven by the rising precision requirements in pharmaceutical intermediates and specialty chemical synthesis, where impurity control directly influences reaction efficiency and product safety. Growth is catalyzed by advancements in green chemistry synthesis pathways and catalytic reaction engineering that deliver higher yield efficiency and reduced by-product formation during acylation processes. These technological improvements enhance reaction selectivity, enabling pharmaceutical manufacturers to achieve consistent molecular outcomes across complex multi-step synthesis workflows. Accelerating adoption is supported by digitalized process monitoring, advanced analytical validation tools, and integrated production control platforms that reduce operational friction for high-purity manufacturing. Industry leaders, including BASF SE, Merck KGaA, and CABB Group, continue expanding specialized high-purity product lines to capture emerging demand.

Application Insights

Pharmaceuticals are projected to lead, accounting for approximately 49% share in 2026, supported by their entrenched role in complex active pharmaceutical ingredient synthesis requiring highly selective acylation intermediates. Adoption remains anchored within drug development pipelines where protecting group chemistry ensures molecular stability during multistep reaction sequences. Pharmaceutical manufacturers prioritize pivaloyl chloride for steric hindrance advantages that prevent unwanted side reactions and improve synthesis precision. Leading suppliers, including BASF SE, Merck KGaA, and CABB Group, maintain specialized pharmaceutical-grade portfolios tailored for high-spec synthesis workflows. This combination of mature pharmaceutical infrastructure, validated reaction chemistry, and persistent drug development demand sustains the application segment’s structural dominance.

Pharmaceuticals are expected to be the fastest-growing segment in the Pivaloyl Chloride market, driven by increasing molecular complexity within modern drug discovery and expanding demand for advanced active pharmaceutical ingredients. Growth is catalyzed by the rising adoption of prodrug technologies, where pivaloyloxymethyl modifications enhance oral bioavailability and therapeutic stability. Continuous flow chemistry platforms further strengthen adoption by improving reaction control, safety, and yield efficiency during acylation processes. Pharmaceutical manufacturers increasingly integrate digitalized quality monitoring and automated synthesis systems to maintain ultra-low impurity thresholds for sensitive drug molecules.

Regional Insights

Asia Pacific Pivaloyl Chloride Market Trends

Asia Pacific is expected to remain the leading regional market, accounting for approximately 56% share in 2026, supported by the region’s unparalleled concentration of pharmaceutical and agrochemical manufacturing capacity. Demand is projected to remain anchored in large-scale active pharmaceutical ingredient synthesis and crop protection chemical production, where cost-efficient intermediate manufacturing supports global supply chains. Extensive chemical industrial parks, integrated petrochemical feedstock availability, and strong export-oriented production infrastructure are anticipated to reinforce the region’s structural dominance in specialty intermediate manufacturing. As global pharmaceutical and agrochemical producers continue relocating intermediate synthesis capacity toward Asia Pacific, the region is positioned to remain both the dominant and fastest-scaling production hub within the global pivaloyl chloride ecosystem.

China is expected to function as the primary anchor shaping Asia Pacific’s regional market trajectory through its vast chemical manufacturing clusters and vertically integrated intermediate production networks. Large-scale chemical parks across coastal industrial provinces are projected to sustain high-volume production capacity while enabling rapid scaling of export-oriented synthesis operations. Chinese producers are expected to expand investments in high-purity distillation infrastructure, digitalized plant monitoring systems, and integrated feedstock supply chains to strengthen global competitiveness. This convergence of manufacturing scale, policy-driven industrial modernization, and export-focused production capability is positioned to sustain Asia Pacific’s structural leadership within the pivaloyl chloride market.

North America Pivaloyl Chloride Market Trends

North America is expected to remain a mature and structurally stable market, supported by deep pharmaceutical research capabilities and an established specialty chemical innovation ecosystem. Demand is projected to remain anchored in high-value active pharmaceutical ingredient synthesis, where precision chemical intermediates and high-purity reagents sustain consistent utilization across advanced drug development workflows. While large-scale commodity manufacturing is expected to remain concentrated in Asia, North America is positioned to retain strategic importance in niche chemical synthesis, contract development activities, and complex reaction engineering requiring stringent quality controls. These structural advantages are expected to reinforce the region’s positioning as a premium innovation hub rather than a volume-driven production center.

The U.S. is expected to function as the central anchor shaping North America’s regional market trajectory through its concentration of pharmaceutical research institutions, contract manufacturing organizations, and advanced chemical engineering capabilities. Regulatory oversight under the U.S. Food and Drug Administration is anticipated to maintain stringent compliance thresholds for pharmaceutical intermediates, reinforcing demand for high-purity reagents within regulated drug synthesis environments. Major pharmaceutical and specialty chemical vendors are expected to prioritize technology-enabled process optimization strategies to strengthen product consistency and regulatory traceability. This convergence of regulatory rigor, technological modernization, and pharmaceutical innovation is positioned to sustain North America’s strategic influence within the pivaloyl chloride market.

Europe Pivaloyl Chloride Market Trends

Europe is expected to remain a structurally important and mature regional market, supported by strong regulatory harmonization and a deeply integrated chemical manufacturing ecosystem. Demand is projected to remain anchored in specialty chemical synthesis and pharmaceutical intermediate production, where high compliance standards reinforce consistent utilization of precision acylation reagents. The region’s industrial structure is anticipated to emphasize operational efficiency through integrated production systems and advanced chemical processing infrastructure. Sustainability frameworks linked to environmental governance are expected to accelerate the transition toward circular chemistry models and lower-emission production architectures.

Germany is expected to function as the central anchor shaping Europe’s regional market trajectory through its advanced chemical manufacturing clusters and vertically integrated production architecture. The country’s Verbund model, widely implemented by major chemical producers such as BASF SE, is projected to reinforce efficient resource utilization by linking feedstock processing, intermediate synthesis, and downstream chemical production within integrated industrial complexes. Regulatory alignment under frameworks such as REACH and broader European sustainability initiatives is anticipated to encourage further investment in safe handling infrastructure and environmentally responsible synthesis pathways. This convergence of industrial integration, sustainability policy alignment, and advanced chemical engineering capabilities is positioned to sustain Europe’s structural relevance in the pivaloyl chloride market.

Competitive Landscape

The global pivaloyl chloride market is moderately consolidated, with leadership concentrated among global suppliers such as BASF SE, Merck KGaA, and CABB Group, while a wider base of regional manufacturers across Asia contributes to the remaining supply landscape. These leading firms exert significant influence through advanced purification capabilities, pharmaceutical-grade quality systems, and established distribution networks that align with stringent procurement standards across pharmaceutical and specialty chemical manufacturing. Competitive positioning across the market increasingly reflects a blend of scale-driven production efficiency and specialization in ultra-high-purity chemical synthesis, where established players leverage vertical integration and long-term supply relationships with pharmaceutical manufacturers. Industry dynamics are expected to emphasize capacity modernization, supply chain resilience, and deeper integration with pharmaceutical and fine chemical ecosystems, as vendors pursue partnerships, selective acquisitions, and technology upgrades to reinforce their strategic positioning within high-specification chemical intermediate markets.

Key Industry Developments:

- In January 2026, BASF SE announced the full operational capacity of its expanded pivalic acid and acid chloride chain in Ludwigshafen. This increases regional supply security in Europe, reducing lead times for pharmaceutical companies requiring high-purity intermediates. It is used as an initiator in polymerization (e.g., producing TBPP for plastics) and in manufacturing specialty coatings and peroxyesters.

- In January 2026, Specialty materials company Celanese achieved ISCC Carbon Footprint Certification for its ECO-C products, validating the use of captured carbon in high-performance polymer production. This certification enables a low-carbon, mass-balanced "green" version of pivaloyl chloride for pharmaceutical manufacturers, targeting a market expected to reach US$300 million by 2035.

Companies Covered in Pivaloyl Chloride Market

- BASF SE

- Merck KGaA

- CABB Group

- Mitsui Chemicals, Inc.

- Lanxess AG

- AlzChem Group AG

- Eastman Chemical Company

- Avantor, Inc.

- Lianhe Chemical Technology Co., Ltd.

- Hangzhou Electrochemical Group Co., Ltd.

- Jiangxi Jinkai Chemical Co., Ltd.

- Meghmani Finechem Ltd.

- Shandong Novista Chemical Co., Ltd.

- Liyang Ruipu Chemical Co., Ltd.

- Shandong Jiahong Chemical Co., Ltd.

- Hebei Jinhong Chemical

Frequently Asked Questions

The global pivaloyl chloride market is projected to be valued at US$172.5 million in 2026 and is expected to reach US$249.2 million by 2033, driven by rising demand in pharmaceutical and agrochemical synthesis, where it functions as a key acylation intermediate.

The growth in pharmaceutical synthesis, particularly for antibiotics and osteoporosis drugs, increases demand for high-purity intermediates. Pivaloyl chloride stabilizes reactive intermediates, ensures precise selectivity, and supports consistent yields in complex multi-step reactions, reinforcing its structural role within regulated drug manufacturing ecosystems.

The global pivaloyl chloride market is forecast to grow at a CAGR of 5.4% from 2026 to 2033, reflecting sustained expansion in high-purity chemical intermediate demand across pharmaceutical and agrochemical applications.

Asia Pacific is the leading regional market, accounting for approximately 56% share, supported by dense pharmaceutical and agrochemical manufacturing clusters, cost-efficient production infrastructure, and large-scale chemical park integration in China and India.