- Medical Devices

- Photobiostimulation Devices Market

Photobiostimulation Devices Market Size, Share, and Growth Forecast, 2026-2033

Photobiostimulation Devices Market by Device Type (Laser Devices, LED‑Based Devices, Infrared Devices, UV Light Devices, Others), Application (Pain Management, Wound Healing, Cosmetic, Neurological, Others), End-User (Hospitals & Clinics, Specialty Clinics, Personal Use, Others), and Regional Analysis for 2026-2033

Photobiostimulation Devices Market Share and Trends Analysis

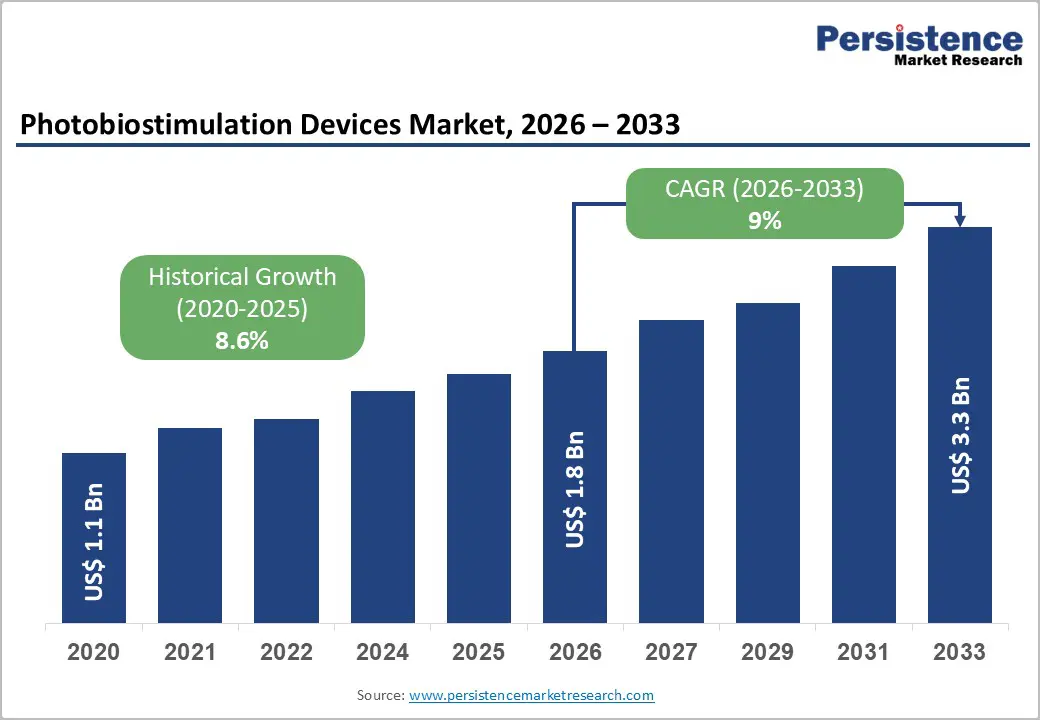

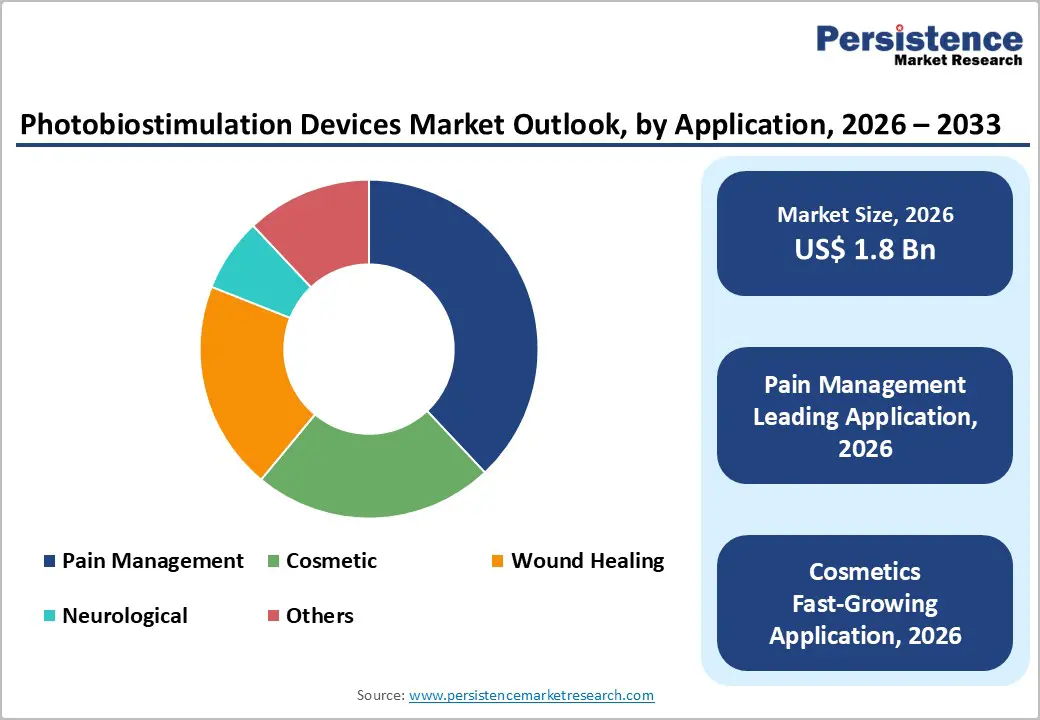

The global photobiostimulation devices market size is likely to be valued at US$ 1.8 billion in 2026, and is projected to reach US$ 3.3 billion by 2033, growing at a CAGR of 9% during the forecast period 2026-2033.

The market is expanding as the demand for non-invasive therapeutic technologies is heightening across clinical and consumer segments. Healthcare providers are integrating light based therapies into pain management, musculoskeletal rehabilitation, and wound healing protocols. Patients are also showing higher acceptance of drug free treatment options that minimize systemic side effects. At the same time, consumer awareness of at home phototherapy solutions is rising, particularly for chronic pain relief and dermatological support. Technological advancement is accelerating product refinement and market maturity. Innovations in light emitting diode (LED), low level laser, and infrared delivery platforms are improving treatment precision, energy efficiency, and portability. Expanding healthcare infrastructure in emerging economies is enhancing device accessibility in outpatient clinics and rehabilitation centers. Clearer regulatory pathways that define device safety and efficacy standards are strengthening physician confidence and facilitating commercialization across professional and personal care channels.

Key Industry Highlights

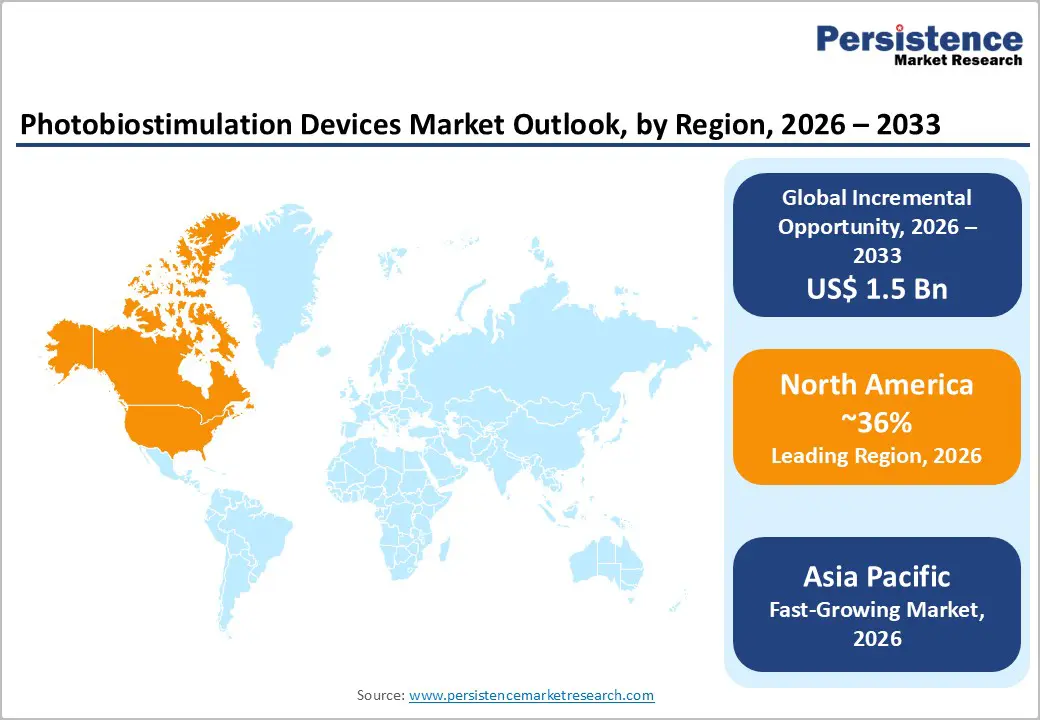

- Regional Leadership: North America is poised to lead with an estimated 36% share in 2026, while Asia Pacific is expected to register the highest CAGR of around 11.3% through 2033, supported by rapidly improving healthcare infrastructure.

- Dominant Device Types: Laser devices are set to command the largest revenue share in 2026, while LED based devices are likely to grow the fastest through 2033, driven by affordability and multi wavelength therapy applications.

- Leading Applications: Pain management is expected to lead with the 38% market share in 2026, while cosmetics is slated to post the highest 2026-2033 CAGR of about 10.5%, reflecting post-surgical care integration.

- Primary End-Users: Hospitals and clinics are anticipated to dominate with the largest market share in 2026, whereas personal use devices are likely to expand the fastest from 2026 to 2033, fueled by rising consumer wellness trends.

- Competitive Environment: Key competitive trends include innovations in portable and AI integrated devices, strategic regional partnerships, and market expansion initiatives targeting high-growth hubs in Asia Pacific and Latin America.

| Report Attribute | Details |

|---|---|

|

Photobiostimulation Devices Market Size (2026E) |

US$ 1.8 Bn |

|

Market Value Forecast (2033F) |

US$ 3.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Widening Prevalence of Chronic Pain and Musculoskeletal Conditions to Fuel Growth

The increase in the prevalence of chronic pain and musculoskeletal disorders worldwide is a primary driver of the photobiostimulation devices market growth. According to the World Health Organization (WHO), musculoskeletal system disorders affect over 1.7 billion people worldwide, with prevalence increasing annually due to aging populations, sedentary lifestyles, and occupational strain. Low-level laser and LED therapy devices provide non-invasive, evidence-based solutions for pain reduction and inflammation management. Their clinical effectiveness in orthopedics, physical therapy, and rehabilitation has resulted in widespread adoption across hospitals and specialty clinics.

Clinical studies consistently demonstrate that photobiostimulation therapy reduces recovery times and improves functional outcomes, reinforcing confidence among healthcare providers. Moreover, CES 2026 highlighted Wontech’s launch of converged treatment platforms integrating laser technology with electrical stimulation and AI-enabled monitoring, showcasing how innovations are addressing chronic pain and functional recovery. Such high-profile industry demonstrations increase clinician awareness, accelerate adoption, and expand the market beyond traditional therapy settings.

Technological Innovation and Regulatory Validation

Continuous advancements in photobiostimulation technology are driving market expansion. Innovations in precision light delivery, wavelength customization, and portable form factors have enhanced therapeutic efficacy and usability. Multi-wavelength LEDs, advanced optics, and AI-assisted treatment planning allow clinicians to optimize therapy outcomes. Compact red-light devices and wearable designs now extend applications into personal wellness, cosmetic therapy, and skin rejuvenation.

Regulatory support has further strengthened market growth. For instance, in January 2025, the U.S. Food and Drug Administration (FDA) approved LumiThera’s Valeda Light Delivery System, the first photobiomodulation therapy for dry age-related macular degeneration (AMD), validating device safety and clinical effectiveness. This milestone underscores broader acceptance of light-based therapies for serious medical applications, encouraging hospitals and specialty clinics to adopt photobiostimulation solutions across multiple therapeutic areas. The combination of innovation and regulatory recognition reinforces both clinical and consumer confidence, creating long-term market momentum.

High Initial Investment and Reimbursement Limitations

The high upfront cost of advanced photobiostimulation devices, particularly precision laser and multi-wavelength LED systems, continues to limit market penetration. Hospitals, specialty clinics, and rehabilitation centers in budget-sensitive regions may defer purchases due to capital constraints. Beyond acquisition, ongoing maintenance, calibration, and operator training add to total expenditures, creating financial barriers for smaller providers. Procurement cycles can get extended due to internal approval processes, delaying integration into clinical workflows and reducing the speed at which new therapies reach patients.

Furthermore, reimbursement uncertainties exacerbate adoption challenges. The Centers for Medicare & Medicaid Services (CMS), for example, proposed changes to physician payment rules and withdrew a Local Coverage Determination (LCD) for certain skin substitute products, leaving device reimbursement criteria unclear. These policy shifts illustrate how inconsistent coverage and evolving reimbursement frameworks may discourage providers from investing in new photobiostimulation technologies, particularly for emerging indications beyond pain management. Limited reimbursement also impacts device marketing strategies and the financial viability of expanding home-use products.

Complex Regulatory Requirements and Standardization Challenges

Stringent regulatory oversight from the U.S. FDA and European Medicines Agency (EMA)-notified bodies continues to pose hurdles for device manufacturers. Obtaining approvals for new therapeutic indications or next-generation devices requires extensive clinical evidence, safety documentation, and compliance with evolving international standards. These requirements extend timelines and increase development costs, especially for innovative or hybrid technologies. In addition, manufacturers must continuously monitor post-market safety reporting and comply with quality management audits, which adds operational complexity and resource demands.

Regulatory complexity is further intensified in Europe with the Medical Device Regulation (MDR) and the European Union (EU) Artificial Intelligence Act, imposing layered compliance on advanced therapeutic devices. Variability in treatment protocols, wavelength outputs, and clinical documentation can impact outcomes and clinician confidence. These challenges together can delay market entry, limit global expansion, and slow adoption of photobiostimulation devices across both clinical and consumer segments. Manufacturers may also face higher legal and liability risks if compliance gaps occur, further increasing barriers to market growth.

Adoption of Advanced Medical Devices in Emerging Economies to Erect New Growth Frontiers

The burgeoning economies of Asia Pacific, Latin America, and parts of Africa represent a major growth frontier for the photobiostimulation devices market. Rapid modernization of healthcare infrastructure, rising disposable incomes, and increasing prevalence of chronic conditions are driving demand for advanced light-based therapies. Growing patient awareness and adoption of non-invasive treatment options further fuel interest in these regions, creating strong business opportunities for device manufacturers. These trends are reinforced by urbanization, expansion of private healthcare networks, and increasing investment in health technologies, which collectively create a fertile environment for market growth.

Strategic partnerships with regional hospitals, specialty clinics, and healthcare networks can enable faster market entry and distribution. The government initiatives such as Southeast Asia’s medical device regulatory reliance programs in 2025 allow participating countries to recognize approvals granted by trusted regulatory authorities, reducing duplication of clinical data requirements and speeding up market authorization. This regulatory harmonization lowers barriers to entry, shortens time to revenue, and facilitates faster adoption, particularly in China, India, and ASEAN countries, which are expected to outpace global growth rate in device uptake and establish early market leadership.

Integration with Adjunctive Therapies, AI, and Digital Health to Open New Avenues

The integration of photobiostimulation technologies with digital health platforms and adjunctive therapies represents a transformative market opportunity. Combining light therapy with telemedicine, remote patient monitoring, and AI-assisted treatment planning enhances clinical validation and improves patient adherence. Personalized therapy regimens, real-time optimization, and outcome tracking strengthen therapeutic efficacy while providing actionable data for clinicians. These capabilities also allow integration with hospital electronic health record (EHR) systems, enabling seamless documentation and analysis across patient populations and care pathways.

Recent trends support this shift, including wearable health monitoring devices, AI-enabled telehealth platforms, and fully remote clinical trials for light-based therapies. For example, LumiThera partnered with digital health providers to connect its Valeda Light Delivery System to a telemonitoring platform, allowing clinicians to track patient response in real time during home-based therapy. Such integrations demonstrate that photobiostimulation can be seamlessly incorporated into connected healthcare ecosystems, enabling predictive treatment adjustments, data-driven care, and the development of subscription-based or outcomes-based revenue models.

Category-wise Analysis

Device Type Insights

Laser devices is estimated to continue to lead in 2026, capturing roughly 42% of the photobiostimulation devices market revenue share, as clinicians trust these devices for precise light delivery and deep tissue penetration for musculoskeletal therapies, post operative recovery, and pain management. Their effectiveness, validated outcomes, and established regulatory clearances support broad adoption in hospitals and specialty clinics where accuracy and clinical confidence matter. As foundational therapeutic tools, lasers remain integral to advanced clinical care protocols and ongoing device demand, reinforcing their leadership in the overall device mix.

LED based devices are anticipated to be the fastest growing segment, expanding at an estimated CAGR of 10.2% from 2026 to 2033, due to their cost efficiency, versatility, and broad applicability across clinical and consumer wellness ecosystems. These systems support dermatological, cosmetic, and at home light therapy use, appealing to clinics and individual users alike. Supporting this trend, L’Oréal unveiled new infrared and LED powered skin and hair devices at CES 2026, including flexible LED face masks and infrared styling tools that merge wellness tech with consumer usability, showcasing how light technologies are crossing over from clinical to mass markets and driving LED innovation.

Application Insights

Pain management is expected to dominate consumer applications, accounting for an estimated 38% of the photobiostimulation devices market share in 2026, driven by the non-invasive effectiveness of this technology in reducing inflammation and supporting recovery from chronic conditions such as arthritis, neuropathy, and tendinopathy. Its broad applicability ensures adoption in physical therapy, sports medicine, and home wellness environments, where clinicians and patients increasingly prefer alternatives to pharmacological interventions. Rising awareness of therapeutic light devices and increasing integration into preventive care further anchor pain management as the dominant application.

The cosmetics segment is projected to be the fastest-growing, with an approximate 2026-2033 CAGR of 10.5%, fueled by the popularity of LED and infrared light therapies for skin rejuvenation, anti-aging, and texture improvement. Consumer adoption is exemplified by the FDA-cleared Therabody TheraFace Mask Glo, a cordless full-face LED therapy mask combining red, blue, and infrared wavelengths for firming, glow, and skin recovery. This product demonstrates how photobiostimulation has expanded from clinical therapy to daily beauty routines, validating the segment’s growth potential and highlighting the rising consumer preference for safe, effective at-home cosmetic light treatments.

Regional Insights

North America Photobiostimulation Devices Market Trends

North America is expected to remain the largest market for photobiostimulation devices in 2026, capturing roughly 37% of global revenues, propelled by advanced clinical infrastructure, widespread insurance coverage, and high prevalence of chronic pain and musculoskeletal disorders. Adoption is strongest in hospitals, specialty clinics, and outpatient therapy centers, while non-invasive devices for pain management, rehabilitation, and dermatology drive clinical demand. Regulatory clarity from the U.S. FDA enables predictable approvals and supports multi-wavelength and AI-enabled platforms. Growing consumer interest in home wellness and cosmetic applications further expands market reach. Professional associations increasingly endorse light therapy, reinforcing adoption and awareness.

Industry developments highlight this momentum. For example, at Cosmoprof North America 2025 in Las Vegas, brands such as JMOON launched phototherapy-based anti-aging devices combining EMS, red LED, and near-infrared technology. These launches demonstrate strong consumer demand and clinic-to-home crossover trends, reinforcing North America’s dual growth path: robust clinical uptake paired with expanding at-home adoption. This confirms the region’s leadership in both therapeutic and wellness photobiostimulation markets.

Europe Photobiostimulation Devices Market Trends

Europe is a key hub for photobiostimulation devices, driven by well-funded healthcare systems, an aging population, and harmonized regulatory standards across the EU. Countries such as Germany, the U.K., France, and Spain show strong adoption, with hospitals, rehabilitation centers, and dermatology clinics integrating light-based therapies into routine care. The EU MDR streamlines approvals and ensures consistent safety and performance, allowing suppliers to operate efficiently across borders. Clinical guidelines promoting multimodal treatment approaches and expanding outpatient networks further support adoption. Growing consumer interest in non-invasive cosmetic procedures also contributes to market momentum, creating demand across both professional and personal applications.

Recent regulatory and industry developments highlight this progress. In June 2025, for instance, the UK Medicines and Healthcare products Regulatory Agency (MHRA) implemented stricter Post-Market Surveillance requirements, mandating active monitoring of device safety and performance. This initiative enhances accountability and builds confidence among clinicians and patients. Combined with wider adoption of medically validated LED systems in dermatology and sports medicine, these measures demonstrate Europe’s commitment to safe, evidence-based photobiostimulation while supporting steady and sustainable market growth.

Asia Pacific Photobiostimulation Devices Market Trends

Asia Pacific is likely to emerge as the fastest-growing regional market for photobiostimulation devices, predicted to showcase a CAGR of around 9% between 2026 and 2033, fueled by expanding healthcare infrastructure, rising chronic disease prevalence, and growing consumer awareness. China, Japan, and India are leading this surge, with hospitals adopting photobiostimulation for rehabilitation, pain management, and dermatology, while at-home devices are gaining traction among consumers. Regulatory frameworks are gradually aligning with international standards, helping global suppliers enter the market more easily. Meanwhile, ASEAN countries such as Indonesia, Malaysia, and Vietnam are seeing rising disposable incomes and better access to healthcare, further broadening adoption.

Real-world innovations highlight the region’s dynamism. Japanese wellness companies introduced compact LED beauty and skincare devices for home use, signaling strong consumer demand. Later, in December 2025, India launched a laser shoe, with support from the Department of Science and Technology (DST), for neuropathic pain, a clinically validated and affordable solution for local markets. These examples show how Asia Pacific is embracing both consumer and clinical applications, making it a hub of innovation and high-growth opportunities in the photobiostimulation space.

Competitive Landscape

The global photostimulation devices market structure is moderately consolidated, with the top vendors, including ABB, Siemens, Schneider Electric, and Eaton, controlling over half of the revenue share. These established players have been leveraging their extensive utility relationships, regulatory expertise, and integrated hardware-software platforms. They are also known to invest heavily in R&D to maintain technological leadership in advanced analytics, AI-driven maintenance, and cybersecurity.

Meanwhile, regional and niche competitors such as Hitachi Energy and Mitsubishi Electric are focusing on specialized segments and geographic strongholds. Barriers such as regulatory compliance and complex system integration limit new entrants, but digitalization trends are enabling software-centric companies to participate through cloud-based solutions. Market consolidation is expected to increase gradually as global leaders acquire smaller vendors to expand geographically and technologically, while software and analytics firms continue collaborating via integration partnerships.

Key Industry Developments

- In February 2026, a Telangana-based startup CuraPod raised INR 20 crore to scale production and market its wearable pain management devices, which use light and heat therapy to offer non-invasive relief. The funding is aimed at broader product development and expanded distribution channels in India’s rapidly growing digital health market.

- In September 2025, Alcon finalized the acquisition of LumiThera, securing the Valeda Photobiomodulation (PBM) system for treating dry Age-Related Macular Degeneration (AMD). Clinical trials (LIGHTSITE I–III) confirmed improvements in visual acuity, highlighting the system’s efficacy. The acquisition expands Alcon’s retina care portfolio beyond surgical interventions to non-invasive, office-based light therapy.

- In August 2025, the U.S. Department of Defense (DOD) awarded a US$ 4.6 million grant to a University of Utah and NYU partnership to study Vielight’s PBM technology for traumatic brain injury (TBI). This funding underscores government interest in exploring non-invasive photobiostimulation for neurological applications.

Companies Covered in Photobiostimulation Devices Market

- Philips Healthcare

- THOR Photomedicine Ltd

- BioLight Technologies LLC

- Erchonia Corporation

- Bioflex Laser

- K Laser USA, Inc.

- NeoLight LLC

- Vielight Inc.

- Theralase Technologies Inc.

- Zimmer Biomet Holdings

- Lumaflex

- RevelAi Health

Frequently Asked Questions

The global photobiostimulation devices market is projected to reach US$ 1.8 billion in 2026.

Rising prevalence of chronic pain, musculoskeletal disorders, and growing adoption of non-invasive light therapies drive the market.

The market is poised to witness a CAGR of 9% from 2026 to 2033.

Expanding demand in emerging markets and integration with digital health and AI-enabled therapies present key opportunities.

Lumenis, Koninklijke Philips, BTL Industries, MedLight, and Wontech are some of the key market players.