- Specialty & Fine Chemicals

- Phosphorus Pentasulfide Market

Phosphorus Pentasulfide Market Size, Share, and Growth Forecast, 2026 – 2033

Phosphorus Pentasulfide Market by Form (Flakes, Powder, Granules), By Application (Lubricant Additive, Pesticide, Others), By End-user (Automotive, Agriculture, Others), and Regional Analysis 2026 – 2033

Phosphorus Pentasulfide Market Size and Trends Analysis

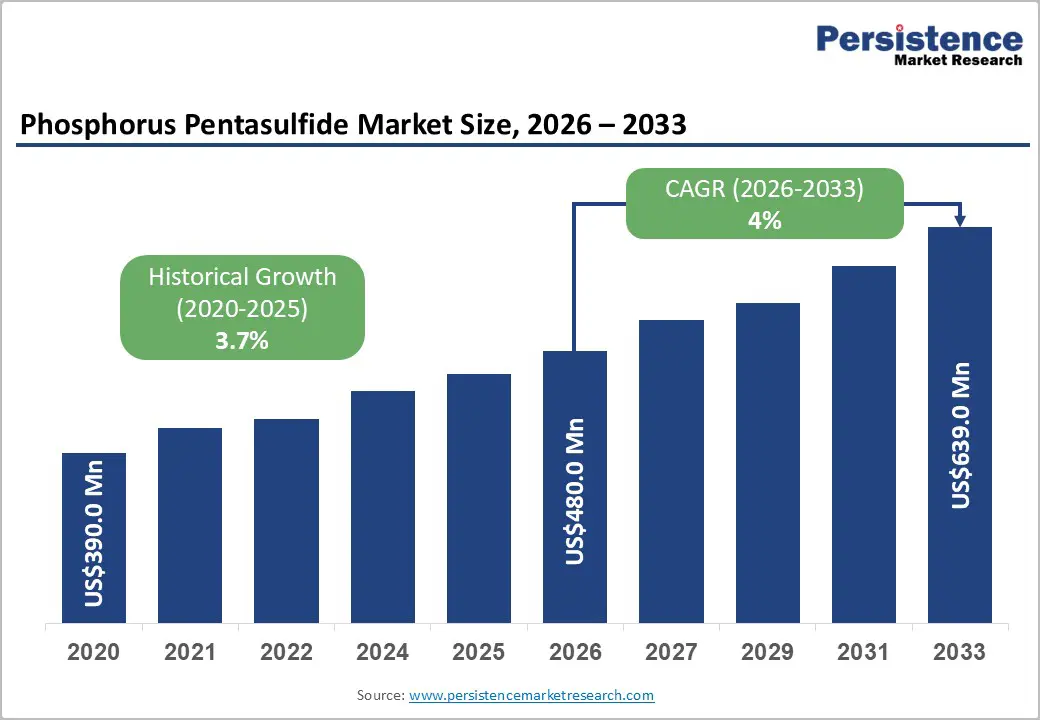

The global phosphorus pentasulfide market size is likely to be valued at US$480 million in 2026 and is expected to reach US$639 million by 2033, growing at a CAGR of 4% during the forecast period from 2026 to 2033, driven by the growing use of phosphorus pentasulfide in lubricant additives, crop protection chemicals, and mining flotation agents, particularly in fast-industrializing economies in the Asia Pacific region.

The surging demand for high-efficiency organophosphate pesticides in emerging economies to ensure food security is projected to bolster market expansion. The shift toward safer material handling is also driving a transition from traditional powder forms to granulated variants, reflecting a broader industrial trend toward operational safety and process optimization.

Key Industry Highlights:

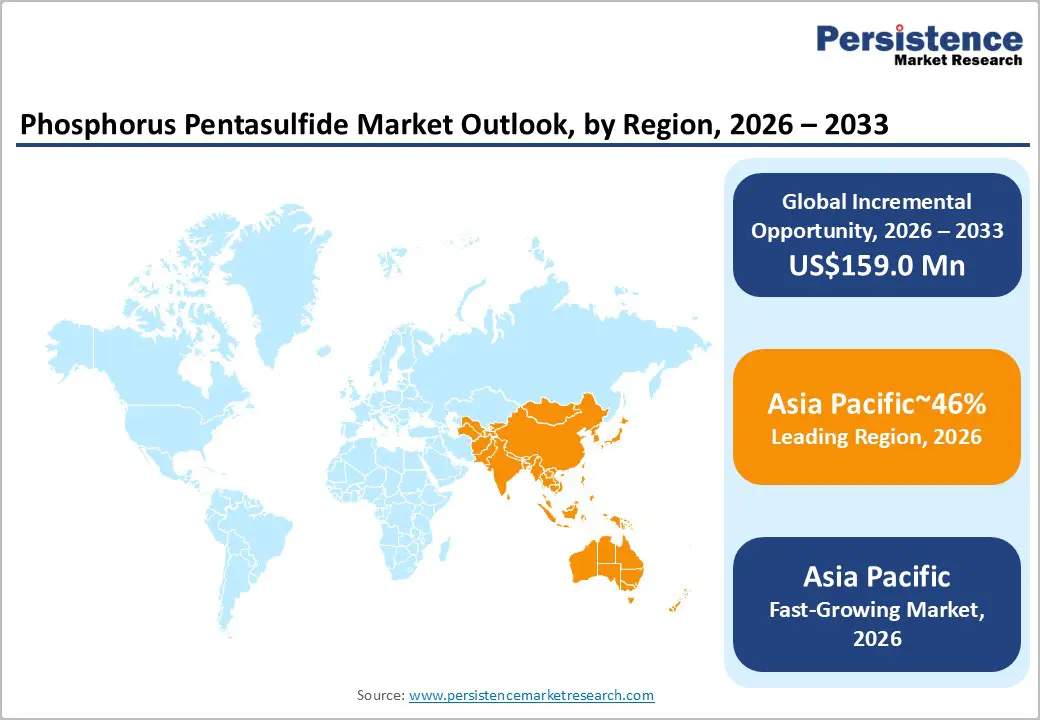

- Leading Region: Asia Pacific is projected to lead due to rapid industrialization, expansive automotive and agricultural sectors, and increasing localization of chemical and additive manufacturing, accounting for approximately 46% share in 2026, supported by advanced particle-size control, automated dosing systems, and optimized reactivity across production clusters.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest due to regulatory harmonization, industrial modernization, and adoption across automotive and specialty chemical sectors, reinforced by compliance-driven process upgrades and technology-enabled supply chains.

- Leading Form: Powder is expected to lead accounting with approximately 46% share in 2026, through industrial adoption, high-throughput synthesis, predictable reactivity, and integration in lubricant additive and agrochemical production workflows.

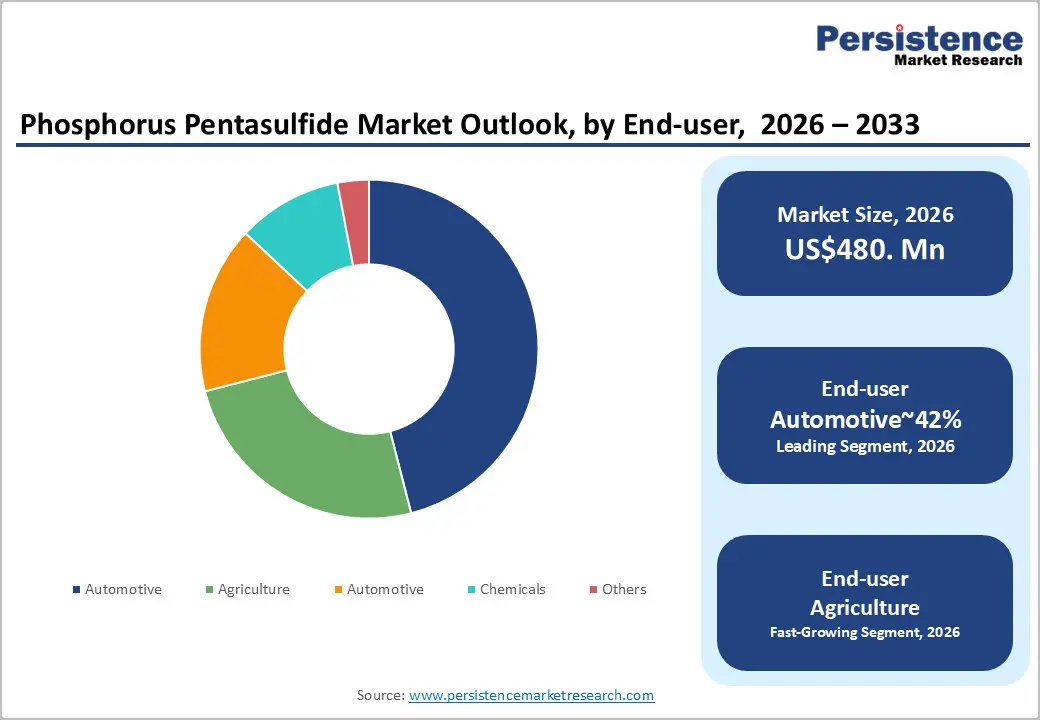

- Leading End-user: The automotive segment is projected to dominate due to its large installed base of internal combustion engines and strong demand for ZDDP-based lubricant additives, holding approximately 42% share in 2026.

| Key Insights | Details |

|---|---|

|

Phosphorus Pentasulfide Market Size (2026E) |

US$480.0 Mn |

|

Market Value Forecast (2033F) |

US$639.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Expansion of Global Agricultural Output and Advanced Crop Protection Solutions

The urgent need to enhance global crop yields to support a growing population is projected to stimulate the demand for effective pest management chemicals. Agricultural stakeholders are increasingly adopting organophosphate-based solutions that offer broad-spectrum control against a wide variety of crop-destroying insects and pathogens. This reliance on proven chemical formulations is expected to drive the consistent use of phosphorus-based intermediates in the synthesis of modern insecticides. As farming practices become more intensive, the application of targeted chemical treatments is anticipated to be a significant contributor to market momentum.

In addition to traditional farming, the rise of large-scale commercial plantations in tropical regions is expected to fuel the consumption of high-reactivity chemical agents. These agents play a crucial role in the manufacturing of fungicides and herbicides that are essential for protecting high-value cash crops from environmental stressors. The ongoing research into more environmentally stable formulations is projected to create a sustained demand for high-quality chemical inputs. Consequently, the agricultural sector is expected to remain a vital pillar for the growth of the chemical intermediate industry through the forecast period.

Rising Demand for High-Performance Lubricant Additives in the Automotive Sector

The global expansion of the automotive industry remains a primary catalyst for the steady consumption of high-grade chemical intermediates. Industrial manufacturing entities are increasingly focusing on the development of specialized engine oils that provide superior thermal stability and wear protection under extreme operating conditions. This trend is expected to sustain the demand for thiophosphorylation agents that are essential for creating protective chemical films on metal surfaces. As vehicle manufacturers shift toward more sophisticated engine designs, the necessity for additives that can reduce friction and prevent oxidation is projected to remain a dominant force in the market.

The transition toward long-drain interval lubricants in heavy-duty commercial vehicles is anticipated to drive the procurement of high-purity chemical precursors. These substances are vital for maintaining the structural integrity of engine components over extended periods of operation. Market participants are expected to witness a consistent requirement for these intermediates as global transportation networks expand and the demand for reliable logistics increases. The integration of advanced chemical engineering practices in the production of lubricant additives is projected to enhance the overall efficiency of internal combustion engines across various geographical regions.

Barrier Analysis – Volatility in Raw Material Procurement and Global Resource Management

The production of high-purity phosphorus derivatives is heavily dependent on the stable availability of elemental yellow phosphorus and sulfur. Fluctuations in the global mining output of these essential minerals are projected to cause periodic imbalances in the chemical manufacturing sector. Factors such as geopolitical tensions and changes in mining policies in key producing regions are anticipated to influence the pricing structure of chemical intermediates. Manufacturers are expected to face difficulties in long-term financial planning due to the unpredictable nature of raw material costs in the international market.

The energy-intensive nature of synthesizing these chemical compounds makes the industry sensitive to shifts in global energy prices. High electricity and fuel costs are projected to elevate the baseline production expenses, potentially limiting the competitive edge of manufacturers in certain regions. The necessity of maintaining high-temperature reactors and specialized processing equipment is expected to remain a significant overhead for industrial facilities. These economic pressures are projected to drive a greater focus on process efficiency and resource optimization among the leading participants in the chemical sector.

Feedstock Price Volatility and Concentrated Production Dynamics

Feedstock price volatility and concentrated production structures are creating structural cost and supply risks across the phosphorus pentasulfide market. Availability and pricing of elemental phosphorus, sulfur, and energy are sensitive to mining cycles, geopolitical trade policies, and transportation disruptions, which propagate uncertainty throughout downstream operations. Limited regional production hubs with strong market control maintain significant leverage over contract terms, particularly for high purity or customized product grades. These dynamics amplify exposure for industrial end users reliant on steady inputs for lubricant additive blending, pesticide synthesis, and specialty chemical production. Periodic maintenance shutdowns, unplanned outages, or logistical bottlenecks further exacerbate supply tightness, constraining procurement flexibility and elevating operational risk.

Concentrated production also introduces structural margins and cost pressures for downstream participants, as sporadic price spikes can affect blending economics and inventory planning. Seasonal demand fluctuations in automotive lubricant or agrochemical applications intersect with supply rigidity, creating cyclical pressure points on procurement strategies. The market participants must navigate a combination of upstream concentration, energy dependency, and logistical vulnerabilities that collectively limit supply elasticity and increase cost volatility across the global value chain.

Opportunity Analysis – Tailored Phosphorus Pentasulfide for Advanced Lubricant Systems

Rising demand for high-performance and specialized lubricant additive systems is creating structural opportunities for differentiated phosphorus pentasulfide products. Original equipment manufacturers are recalibrating specifications for low-viscosity and low-ash engine oils, prompting additive suppliers to develop next-generation ZDDP chemistry and complementary anti-wear packages. Producers capable of delivering consistent purity, controlled reactivity, and customized particle size distributions, alongside secure long-term supply arrangements, can strengthen technical integration with major lubricant formulators. This environment enables premium positioning for specialty grades, facilitates co-development partnerships, and reinforces field validation linkages, supporting formulation optimization and operational reliability across diverse automotive and industrial applications.

Simultaneously, industrial machinery applications are increasingly demanding robust lubrication under elevated loads, higher temperatures, and more intensive duty cycles. This trend is driving incremental adoption of advanced phosphorus-containing additives in gear oils, hydraulic fluids, and metalworking lubricants, where equipment uptime and component longevity are financially significant. Alignment with evolving ISO and OEM performance standards, coupled with environmental compliance considerations, positions phosphorus pentasulfide-based systems as essential contributors to effective asset management and operational cost efficiency across industrial and automotive sectors.

Innovation in Industrial Lubrication for Automated Manufacturing and Robotics

The rapid advancement of industrial automation and robotics is projected to drive the need for specialized lubricants designed for precision machinery. These high-tech applications require additives that can function effectively under micro-load conditions and provide exceptional surface protection. The synthesis of novel thiophosphates is expected to play a vital role in meeting these specialized lubrication requirements. As manufacturing facilities transition toward autonomous operations, the demand for long-lasting and high-reliability lubricants is projected to experience a significant uptick.

Moreover, the expansion of the aerospace and defense sectors is anticipated to provide additional opportunities for the application of advanced chemical intermediates. The development of high-altitude and extreme-temperature lubricants is expected to rely on the unique chemical properties of phosphorus-sulfur derivatives. Market participants are projected to explore collaborative research initiatives with aerospace engineering firms to develop customized lubrication solutions. This focus on high-value, niche applications is anticipated to drive the diversification of the chemical market and provide a hedge against fluctuations in more traditional industry segments.

Category–wise Analysis

Form Insights

The powder segment is anticipated to lead the market, accounting for approximately 46% share in 2026, underpinned by its entrenched role in high-throughput chemical synthesis across lubricant additive and agrochemical production workflows. Adoption remains anchored by predictable reactivity, high surface area, and rapid dissolution, enabling consistent conversion in batch-style reactors. Producers such as ICL Group and Italmatch Chemicals rely on powder grades to maintain process reliability and operational efficiency within established solid handling infrastructure.

Ongoing platform evolution, including improved reactor design and process automation, continues to reinforce replacement cycles and utilization intensity. Powder’s compatibility with existing feeding systems, safety protocols, and thiophosphorylation workflows ensures minimal operational disruption. This combination of mature infrastructure, technical reliability, and integration with major additive and intermediate production lines sustains the segment’s dominance within structured manufacturing environments.

Granules are expected to be the fastest-growing segment, driven by emerging needs for safer handling and process optimization in modern chemical production. Growth is being catalyzed by enhanced flowability, lower dust generation, and reduced moisture absorption, which materially improve operational safety and shelf life during storage and maritime transport.

Accelerating adoption is supported by automated dosing systems and bulk handling innovations, lowering handling friction for new plants and expanding mid-sized manufacturer integration. Companies such as LANXESS incorporate granulated formats to improve dosing precision and process control. As industrial hygiene, operator safety, and modern plant design converge with technical performance, granules are expected to outpace overall market growth by offering a balanced trade-off between reactivity and operational efficiency.

End-user Insights

The automotive segment is expected to lead the market, accounting for approximately 42% share in 2026, underpinned by its entrenched role in ZDDP-containing engine and transmission oils across both original-fill and aftermarket workflows. Adoption remains anchored by the large installed base of internal combustion and hybrid powertrains, where robust lubrication ensures engine longevity, fuel efficiency, and compliance with evolving OEM specifications. Major lubricant marketers such as Shell and ExxonMobil integrate phosphorus pentasulfide derivatives into premium product lines, reinforcing consistent demand across passenger vehicles, heavy-duty trucks, and off-highway machinery.

Platform evolution, including advanced tribological formulations and performance monitoring, continues to reinforce replacement cycles and utilization intensity. Automotive’s dominance is sustained through mature supply chains, established technical expertise, and alignment with warranty structures, providing predictable procurement patterns. This combination of scale, high reactivity requirements, and integration with industry-leading additive portfolios cements the segment’s position within global structured lubricant deployment models.

Agriculture is expected to be the fastest-growing segment in the market, driven by increasing demand for effective crop protection chemicals in high-population and export-focused regions. Growth is catalyzed by structural pressures such as limited arable land, intensified farming practices, and the expansion of modern agrochemical distribution networks. Technology inflection points, including targeted pesticide delivery systems and precision application methods, enhance efficacy and operational efficiency.

Suppliers such as BASF and LANXESS leverage phosphorus pentasulfide-based formulations to meet quality, cost, and regulatory expectations, improving adoption among cooperatives and large-scale growers. Accelerating use is supported by product stewardship programs, registration alignment, and alignment with integrated pest management frameworks. As agricultural production intensifies and chemical performance demands rise, the sector is expected to outpace overall market growth, positioning phosphorus pentasulfide as a critical input for sustainable crop protection.

Regional Insights

Asia Pacific Phosphorus Pentasulfide Market Trends

Asia Pacific is expected to remain the leading market for phosphorus pentasulfide, approximating 46% of global consumption in 2026, supported by rapid industrialization, expansive automotive and agricultural sectors, and is expected to stay the fastest-growing market. The region’s structural dominance is underpinned by extensive production and consumption clusters in China and India, where manufacturers such as Hubei Xingfa Chemicals Group and LANXESS supply phosphorus pentasulfide for lubricant additives, organophosphate pesticides, and mining flotation agents.

Core demand is anchored in high-volume automotive lubricant blending, agrochemical synthesis, and industrial chemical processes, with technology evolution including improved particle-size control, automated dosing systems, and optimized reactivity, enhancing throughput and operational efficiency. This combination sustains Asia Pacific’s preeminence as both a leading consumption hub and a critical production base for phosphorus pentasulfide intermediates.

China is positioned to anchor regional momentum, shaping market dynamics through its dominant automotive manufacturing, chemical production, and mining sectors. Companies such as Hubei Xingfa Chemicals Group drive supply for lubricant additive formulations and organophosphorus agrochemicals, while industrial machinery and automotive OEMs generate steady high-volume demand. Vendor strategies emphasize technical reliability, consistent purity, and long-term supply agreements, facilitating alignment with OEM lubricant specifications and pesticide efficacy requirements.

Forward-looking adoption of advanced process technologies, including granulated product formats, automated handling systems, and precision-reactor applications, is projected to reinforce China’s influence on Asia Pacific’s phosphorus pentasulfide market growth trajectory, solidifying both production leadership and consumption dominance.

North America Phosphorus Pentasulfide Market Trends

North America is expected to remain a mature and structurally stable market, supported by a sophisticated industrial ecosystem and concentrated demand in automotive lubricants and specialty chemical derivatives. The region’s structural positioning is anchored by a high-value manufacturing base, extensive R&D infrastructure, and a concentration of major players such as The Lubrizol Corporation, whose integrated operations ensure consistent supply and advanced thiophosphorylation capabilities.

Core demand is driven by lubricant formulators, additive producers, and industrial chemical users requiring high-purity phosphorus pentasulfide for reliable anti-wear performance and process efficiency. Technology evolution, including process digitization, emission management, and product stewardship, continues to reinforce operational precision, while mature logistics networks and established industrial hubs maintain supply continuity.

The U.S. is expected to anchor regional momentum, shaping North America’s trajectory through advanced manufacturing, targeted R&D, and adoption of high-specification lubricant formulations for passenger, commercial, and industrial vehicle segments. Environmental frameworks administered by the EPA drive process modernization, safer handling practices, and development of low-volatility, high-performance chemical intermediates. Strategic collaboration between additive suppliers and automotive OEMs promotes the co-development of phosphorus-based formulations aligned with evolving engine emission and fuel efficiency standards.

Vendors that integrate local production, terminal infrastructure, and technical service capabilities are positioned to secure long-term agreements, ensuring reliable supply and reinforcing North America’s mature yet technologically advanced phosphorus pentasulfide market.

Europe Phosphorus Pentasulfide Market Trends

Europe is expected to hold a meaningful share of the phosphorus pentasulfide market, characterized by a relatively stable, regulation intensive environment and a well developed automotive and chemical industry base. The region’s demand is shaped by stringent environmental norms, including REACH compliance, worker safety directives, and waste management requirements, all of which influence procurement criteria and preferred product specifications.

Automotive lubricants, industrial oils, and selected agrochemical and specialty chemical applications form the main demand clusters. Producers and importers serving Europe must demonstrate robust documentation, product stewardship, and traceability systems, which favors larger, compliance capable suppliers with established quality management frameworks.

Germany is expected to play a central role in European demand, supported by its strong automotive manufacturing footprint, highly engineered industrial base, and advanced chemical sector. Local lubricant formulators serving global OEMs, together with specialty additive and chemical producers, require reliable access to phosphorus pentasulfide that meets tight impurity, stability, and handling criteria.

As European initiatives around decarbonization, circularity, and safer chemicals progress, German companies are likely to prioritize collaborative relationships with suppliers able to support reformulation efforts, life cycle assessments, and innovation in lower impact additive chemistries. This reinforces the need for technologically capable, sustainability oriented phosphorus pentasulfide vendors in the regional ecosystem.

Competitive Landscape

The global phosphorus pentasulfide market is moderately consolidated, with leadership concentrated among global suppliers such as Hubei Xingfa Chemicals Group, LANXESS, and The Lubrizol Corporation, which collectively shape supply, quality standards, and technological practices across lubricant, agrochemical, and specialty chemical applications. These leading producers exert functional influence through their integrated access to raw materials, proprietary thiophosphorylation processes, and advanced purification technologies, ensuring consistent high-purity product delivery and reliable performance for demanding industrial end users. Competitive positioning within the market is primarily achieved through a combination of horizontal differentiation across product forms and geographic coverage, as well as vertical integration into downstream phosphorus-based chemistries or additive formulations. Industry dynamics are shaped by selective capacity expansions, plant modernizations, and strategic alliances aimed at optimizing logistics, regional penetration, and collaborative product development.

Key Industry Developments:

- In March 2026, Italmatch Chemicals successfully completed a major debt refinancing to fuel strategic growth in phosphorus-based specialties. This financial restructuring strengthens the company's ability to invest in high-growth areas such as EV battery precursors and sustainable phosphorus recovery.

- In January 2026, Perimeter Solutions completed the acquisition of Medical Manufacturing Technologies (MMT) to aggressively expand its footprint in the high-growth medical device market. This move significantly diversifies their portfolio beyond fire safety and lubricant additives, positioning them as a major technical partner in the global healthcare supply chain.

Companies Covered in Phosphorus Pentasulfide Market

- ICL Group

- LANXESS AG

- Hubei Xingfa Chemicals Group Co., Ltd.

- Italmatch Chemicals S.p.A.

- Mitsui Chemicals, Inc.

- Solvay S.A.

- Prayon S.A.

- UPL Limited

- Sichuan Zhishitang Chemical Co., Ltd.

- Zhejiang Jiahua Energy Chemical Industry Co., Ltd.

- Anhui Bayi Chemical Industry Co., Ltd.

- Yunnan Phosphorous Group Co., Ltd.

- Budenheim KG

- Chemtrade Logistics

- Nippon Chemical Industrial

- Santai Aostar Phosphate Chemical

Frequently Asked Questions

The global phosphorus pentasulfide market is projected to be valued at US$480 million in 2026 and is expected to reach US$639 million by 2033, driven by demand in lubricant additives, organophosphate pesticides, and mining flotation agents, particularly across industrializing economies in Asia Pacific.

The expansion of high-efficiency organophosphate-based crop protection solutions supports increased food production and export-focused farming. Adoption of targeted pesticide applications, precision delivery, and regulatory-aligned formulations is anticipated to sustain demand for phosphorus pentasulfide as a critical chemical intermediate.

The phosphorus pentasulfide market is forecast to grow at a CAGR of 4% from 2026 to 2033, reflecting steady consumption in automotive lubricants, specialty chemical intermediates, and agrochemical applications.

Asia Pacific is the leading regional market, accounting for approximately 46% share, supported by industrialization, automotive lubricant blending, large-scale agriculture, and production clusters in China and India, with suppliers such as Hubei Xingfa Chemicals Group and LANXESS driving both supply and technical integration.

The phosphorus pentasulfide market is moderately consolidated, with major suppliers including Hubei Xingfa Chemicals Group, LANXESS AG, ICL Group, The Lubrizol Corporation, Italmatch Chemicals S.p.A., Mitsui Chemicals, Inc., Solvay S.A., Prayon S.A., UPL Limited, Sichuan Zhishitang Chemical Co., Ltd., Zhejiang Jiahua Energy Chemical Industry Co., Ltd., Anhui Bayi Chemical Industry Co., Ltd., and Yunnan Phosphorous Group Co., Ltd.