- Hardware & Software IT Services

- Parental Control Software Market

Parental Control Software Market Size, Share, and Growth Forecast 2026 - 2033

Parental Control Software Market by Platform (Android-based, iOS-based, and Windows-based), Deployment (On-Premise and Cloud), End-user (Residential and Educational), and Regional Analysis 2026 - 2033

Parental Control Software Market Size and Share Analysis

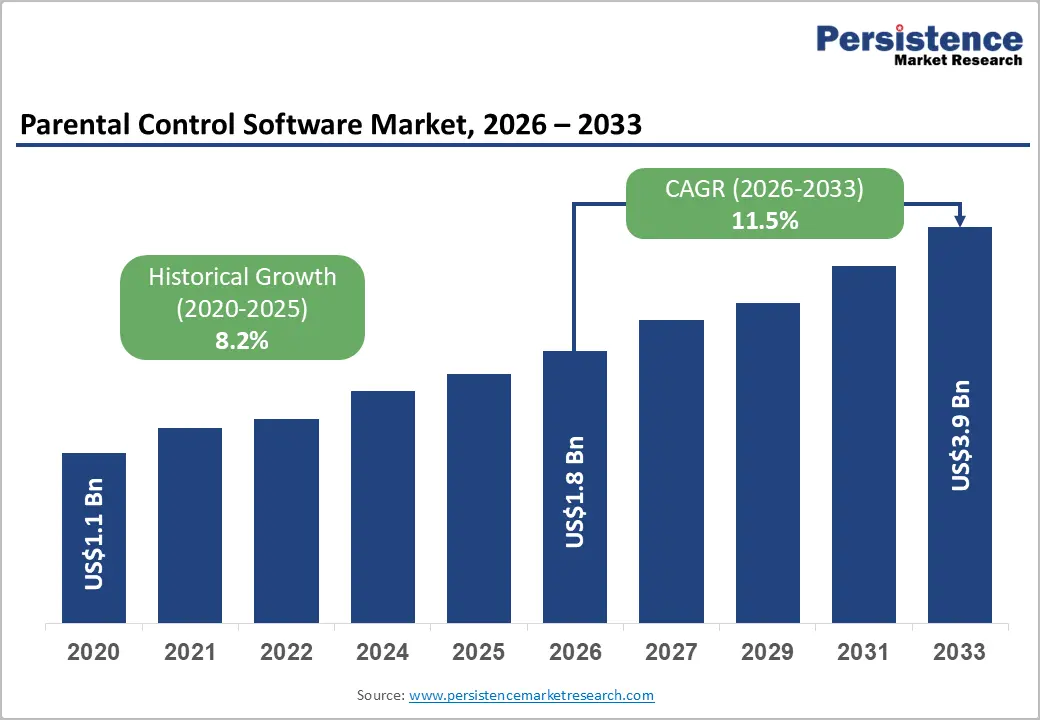

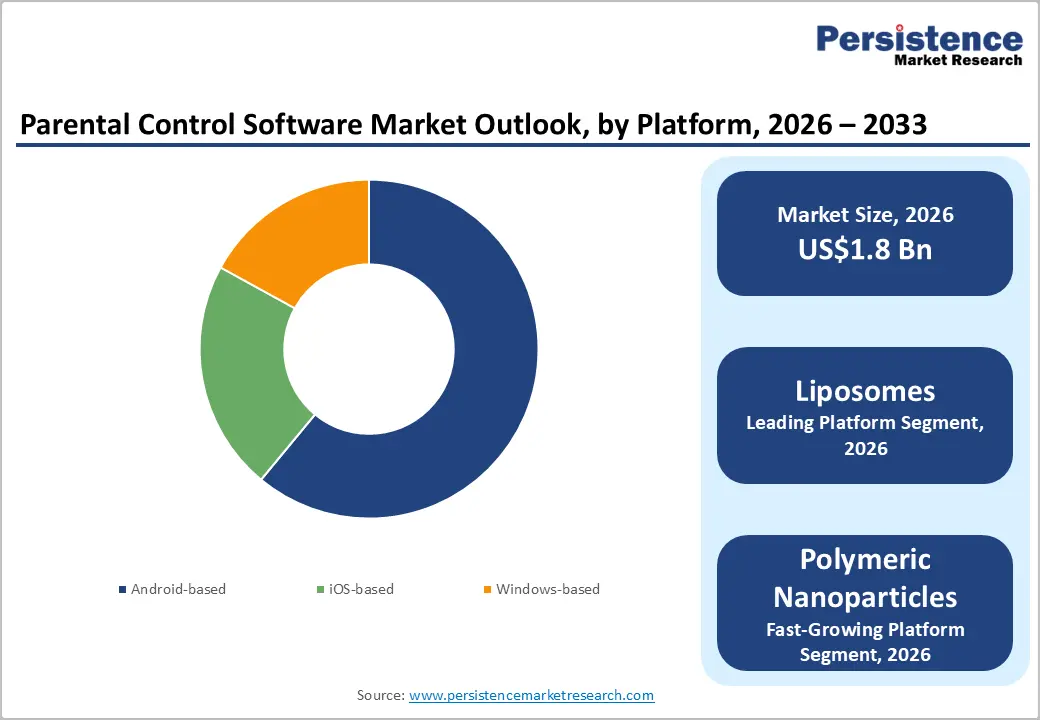

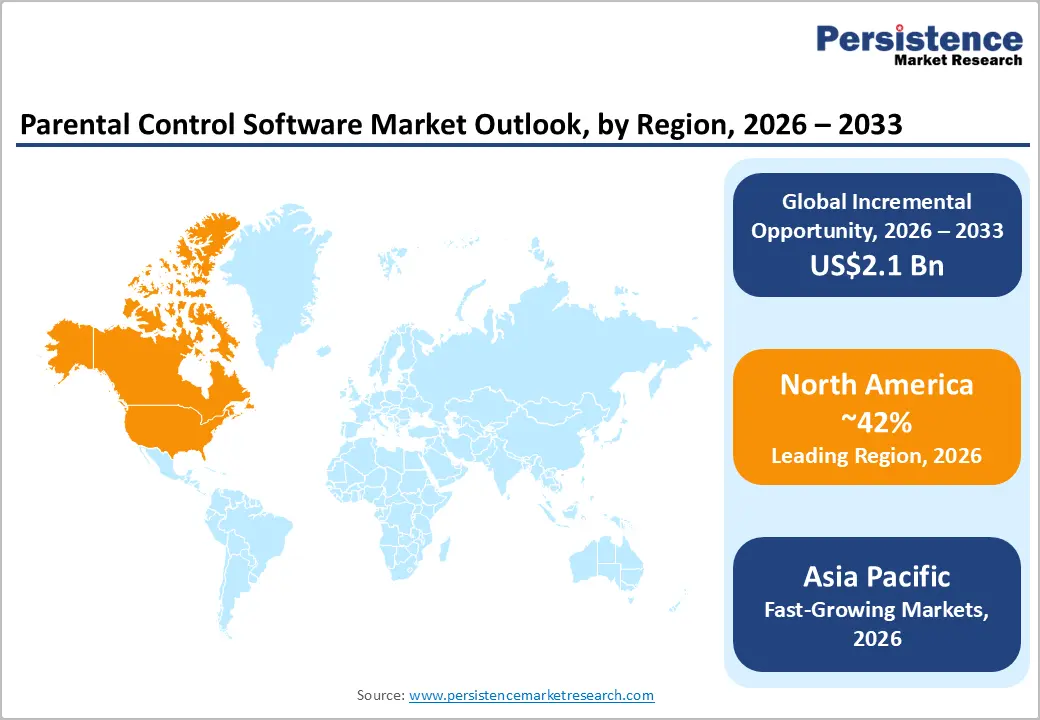

The global parental control software market size is likely to be valued at US$ 1.8 Bn in 2026 and is projected to reach US$ 3.9 Bn by 2033, growing at a CAGR of 11.5% between 2026 and 2033.

The market is primarily driven by the escalating concern over cyberbullying, online grooming, screen addiction among minors, and stringent government regulations such as the UK Online Safety Act and COPPA in the United States. As digital device ownership among children under 8 years old surpasses 51%, parents are increasingly adopting sophisticated monitoring solutions to ensure digital well-being.

Key Industry Highlights:

- Leading Region: North America, with 42% share, leads the global parental control software market, supported by high regulatory awareness, early adoption of digital safety solutions, and widespread smart device usage among children.

- Fastest-Growing Region: Asia Pacific leads with a 14.2% CAGR, driven by rapid smartphone penetration and rising internet access among minors in India and China.

- Dominant End User: The Residential segment accounts for the majority of market revenue, fueled by recurring family subscriptions and the normalization of digital parenting practices.

- Fastest-Growing Platform: The iOS platform segment is expected to grow the fastest, driven by rising adoption of privacy-first parental control solutions, higher willingness to pay for premium subscriptions in developed markets, and greater regulatory alignment with Apple’s consent-based supervision framework.

- Key Market Opportunity: The integration of Artificial Intelligence (AI) for real-time cyberbullying detection, behavioral risk analysis, and contextual alerting represents a significant value-creation opportunity for market participants.

| Key Insights | Details |

|---|---|

|

Parental Control Software Market Size (2026E) |

US$ 1.8 Bn |

|

Market Value Forecast (2033F) |

US$ 3.9 Bn |

|

Projected Growth CAGR(2026-2033) |

11.5% |

|

Historical Market Growth (2020-2025) |

8.2% |

Market Dynamics

Drivers - Surge in Social Media Usage and Cyberbullying Concerns

The rapid growth of social media usage among children and adolescents is a key driver for the global parental control software market. Teenagers are spending increasing amounts of time on platforms such as Instagram, TikTok, and Snapchat, where exposure to cyberbullying, harassment, inappropriate content, and online predators is significantly higher. Studies indicate that over 30% of teenagers experience bullying either online or at school, while lifetime cyberbullying exposure is projected to reach nearly 60% by 2025. This escalating digital risk environment is compelling parents to adopt proactive monitoring solutions rather than reactive interventions.

Parental control software offers real-time alerts, keyword detection, social media monitoring, and content filtering, enabling parents to intervene early before psychological harm occurs. As awareness of digital threats grows, families are increasingly willing to pay for premium subscriptions that provide comprehensive protection across multiple apps and devices. This heightened concern for child safety directly translates into stronger adoption rates and sustained market growth.

Integration of AI and Machine Learning in Safety Tools Driving Consumer Trust

The adoption of Artificial Intelligence (AI) and Machine Learning (ML) technologies has emerged as a transformative growth driver for parental control software solutions. Modern platforms leverage AI-driven algorithms to analyze behavioral patterns, communication tone, and contextual signals across messages, images, and online interactions. This enables early detection of serious risks such as cyberbullying, self-harm ideation, online grooming, or emotional distress, without requiring parents to manually monitor every interaction.

For instance, solutions offered by Bark use AI to scan text messages, emails, photos, and social media activity, alerting parents only when potential threats are identified. This selective alert system helps resolve the long-standing tension between child privacy and parental oversight. AI systems continuously evolve by learning new slang, emojis, and emerging online behaviors, ensuring relevance in rapidly changing digital ecosystems. As parents gain confidence in the accuracy, discretion, and adaptability of AI-powered tools, user retention improves and adoption accelerates, reinforcing long-term market expansion.

Restraints - Data Privacy and Security Concerns

A significant barrier to the adoption of Parental Control Software is concern about data privacy. Parents are increasingly wary of how third-party applications store and utilize their children's sensitive data, including location history, browsing habits, and private conversations. Reports of data breaches and the potential for these apps to be exploited by bad actors create a "trust deficit" in the market.

Strict data protection laws, such as GDPR in Europe, impose heavy compliance burdens on software providers. If a company fails to transparently communicate its data handling practices, it risks alienating privacy-conscious parents, thereby restraining potential market expansion.

Bypass Techniques by Tech-Savvy Children

The effectiveness of parental control tools is often challenged by the technical proficiency of the younger generation. Children are increasingly finding ways to bypass restrictions using Virtual Private Networks (VPNs), proxy servers, or simply by factory resetting devices. Tech-savvy teenagers share workaround methods on forums and peer networks, rendering basic blocking features obsolete.

This "cat-and-mouse" dynamic frustrates parents who feel that the software does not deliver on its promise of control. Consequently, some parents may view these paid solutions as ineffective expenditures, preferring free, OS-level controls like Apple Screen Time or Google Family Link, which limit the revenue potential for third-party standalone vendors.

Opportunity - Expansion into the Educational Sector (EdTech Integration) Creates a Scalable B2B Growth Avenue

The increasing adoption of digital learning models presents a compelling opportunity for parental control software providers to expand beyond household applications into the education sector. The widespread implementation of 1:1 device programs, where each student is issued a school-managed laptop or tablet, has heightened the need for centralized monitoring, content filtering, and classroom management tools. Educational institutions are under growing pressure to ensure student safety, regulatory compliance, and academic focus across both on-campus and remote learning environments.

Vendors such as Qoria Ltd and Bark are already leveraging this opportunity by offering integrated solutions that function seamlessly across school and home networks. This “whole-community” protection model enables vendors to secure long-term B2B contracts with schools and districts while simultaneously strengthening brand presence among parents. Cross-selling opportunities emerge as parents seek continuity in digital safety controls outside school hours. As global investments in EdTech infrastructure continue to rise, the convergence of classroom management and child online safety is expected to remain a high-growth opportunity for market participants.

Growth in Digital Adoption in Emerging Markets and Mobile-First Economies Presents Significant Untapped Market Potential

Emerging markets, particularly across Asia Pacific and Latin America, represent a substantial growth opportunity for the global parental control software market. Countries such as India, Indonesia, and Brazil are experiencing accelerated smartphone penetration, declining data costs, and younger populations coming online at earlier ages. Despite this rapid digital adoption, awareness and usage of parental control and digital safety solutions remain comparatively low, creating a large addressable user base.

Market participants can capitalize on this gap by developing localized, mobile-first, and Android-centric solutions that align with regional usage patterns and price sensitivities. Offering lightweight applications with tiered pricing or freemium models can lower adoption barriers in cost-conscious markets. Strategic partnerships with regional telecom operators, mirroring models such as Bark’s collaboration with T-Mobile, enable vendors to bundle parental control features within family data plans. This distribution strategy reduces upfront costs for consumers, accelerates user acquisition, and positions parental control software as a default component of mobile connectivity in high-growth developing economies.

Category-wise Analysis

Platform Insights

The Android-based segment is the leading platform in the parental control software market, holding a dominant share of approximately 61%. This dominance is justified by the open nature of the Android operating system, which allows developers to create more granular and intrusive monitoring features, such as call recording and advanced app blocking, that are often restricted on the closed iOS ecosystem. The global volume of Android devices, particularly in emerging markets like India and China, far outstrips that of iOS devices. Parents often provide children with affordable Android smartphones as their first device, driving the volume-based leadership of this segment.

The iOS platform continues to represent a strategically important and rapidly maturing sub-segment driven by strong brand loyalty, high average selling prices, and premium user demographics. Despite the inherent restrictions of the iOS ecosystem, such as limited background access and tighter sandboxing of third-party applications, vendors have successfully adapted by focusing on user-centric interfaces, cloud-based functionality, and consent-based controls that align with Apple’s privacy-first policies.

Deployment Insights

Cloud-based deployment holds a leading position in the global parental control software market, accounting for approximately 58% of the total market share. This dominance is driven by cloud solutions' ability to provide real-time synchronization, remote access, and centralized control across multiple devices. Parents can instantly modify settings, review activity logs, restrict applications, or lock devices remotely using their own smartphones, regardless of their child’s physical location. This “anytime, anywhere” management capability has become a critical requirement for modern digital parenting, particularly in households with multiple connected devices.

Cloud-based platforms enable automatic and continuous software updates, ensuring that threat databases remain current without requiring manual intervention. This allows parental control solutions to rapidly recognize newly launched apps, emerging social media platforms, and evolving online threats. The scalability, low maintenance requirements, and improved responsiveness of cloud-based models make them highly attractive to both consumers and vendors, reinforcing their leadership over on-premise or device-only deployment models.

End-user Insights

The residential segment represents the largest end-user category in the parental control software market, accounting for approximately 72% of total revenue. This leadership is fundamentally driven by parents’ continuous need to safeguard children in an always-connected digital environment. Unlike educational institutions, which operate within fixed schedules, controlled networks, and budgetary constraints, households require 24/7 monitoring and management across personal smartphones, tablets, laptops, and gaming devices.

The growing concept of “digital parenting”, coupled with increased awareness of online risks, has normalized the use of subscription-based safety applications within families. Parents increasingly view these tools as essential digital utilities rather than optional add-ons. As a result, recurring household subscriptions remain the primary volume driver for leading vendors such as Norton and Qustodio. While adoption in the educational sector is expanding steadily, individual residential subscriptions continue to account for the majority of market revenue.

Regional Insights

North America Parental Control Software Trends

North America currently holds nearly 42% share and dominates the global parental control software market, supported by high disposable incomes, advanced digital infrastructure, and a mature regulatory environment prioritizing child online safety. The United States leads regional adoption, driven by early exposure to smart devices. Reports indicate that over 51% of children under the age of eight own a mobile device. This early and widespread device usage significantly expands the addressable market for parental monitoring solutions.

The regulatory landscape, shaped by frameworks such as the Children's Online Privacy Protection Act (COPPA) and the proposed Kids Online Safety Act (KOSA), has created a compliance-focused ecosystem that favors established and trusted vendors. Companies such as Bark and Norton benefit from this environment through increased institutional trust and brand credibility. Additionally, partnerships between software providers and telecom operators, such as Bark’s collaboration with T-Mobile, are improving distribution by bundling parental control tools with family mobile plans. The region’s strong innovation ecosystem further supports frequent feature upgrades, particularly in AI-driven content analysis and behavioral monitoring.

Europe Parental Control Software Trends

Europe’s parental control software market is defined by its strong emphasis on data privacy, regulatory harmonization, and ethical digital supervision. The enforcement of the General Data Protection Regulation (GDPR), alongside the UK Online Safety Act becoming fully enforceable by 2025, has compelled vendors to adopt privacy-by-design principles in their solutions. Countries such as the United Kingdom, Germany, and France are leading this shift, demanding child safety tools that balance protection with respect for minors’ data rights.

As a result, the region is witnessing a growing preference for “guided supervision” models rather than covert monitoring. Parental control solutions increasingly emphasize transparency, consent, and communication between parents and children. The European Union’s continued investment in digital literacy and online safety education is driving demand for school-grade filtering and monitoring tools that comply with stringent regional privacy standards, supporting steady institutional adoption.

Asia Pacific Parental Control Software Trends

Asia Pacific is projected to register a CAGR of 14.2% and emerge as the fastest-growing region in the global parental control software market, fueled by rapid digital adoption, declining smartphone prices, and a large population of young internet users. Major markets such as China, India, and South Korea are experiencing an unprecedented expansion in internet access among children and adolescents.

In China, strict government regulations limiting minors’ gaming hours and online activity have created a compliance-driven demand for tools to manage and monitor screen time. India, meanwhile, is witnessing strong growth as affordable smartphones penetrate semi-urban and rural areas, bringing millions of first-time young users online. Cultural emphasis on academic performance across the region further increases demand for parental control software that blocks distractions, such as gaming and social media, during study hours. East Asia’s manufacturing ecosystem enables the integration of pre-installed parental control features on locally produced devices, strengthening regional adoption.

Competitive Landscape

The parental control software market is moderately fragmented, characterized by a mix of cybersecurity giants and specialized niche players. While established antivirus vendors like Norton and Kaspersky leverage their existing customer base to bundle parental controls, specialized firms such as Qustodio and Bark differentiate themselves through dedicated, feature-rich standalone apps. The market is witnessing a trend of consolidation and ecosystem expansion. Companies are shifting from simple "blocking" models to holistic "family safety" platforms that include location tracking, driving monitoring, and identity theft protection. Competitive differentiation is increasingly centered on AI capabilities, specifically the ability to monitor encrypted platforms like WhatsApp and Snapchat without compromising device performance or user privacy.

Key Market Developments

- In May 2025, Bark Technologies launched a strategic partnership with AKKO, a device protection platform. This collaboration integrates device insurance and repair services directly into the Bark ecosystem, offering parents a comprehensive safety and physical protection package for their children's devices.

- In November 2025, Bark Technologies updated its multi-year MVNO agreement with T-Mobile. This deal positions T-Mobile as the exclusive nationwide network for the Bark Phone, ensuring reliable connectivity and expanding the reach of Bark's hardware-software combined solution.

- In October 2024, Qoria Ltd completed the acquisition of Ayra Group Pty Ltd (trading as OctopusBI) for AUD 9.11 million. This strategic move enhances Qoria's data analytics capabilities, enabling deeper insights into student digital well-being across its education portfolio.

Companies Covered in Parental Control Software Market

- Norton

- Kaspersky Lab

- Qustodio LLC

- Mobicip

- McAfee LLC

- FamilyTime

- SafeDNS

- MSPs

- Bark

- Corun Digital Corporation

- ADFLOW Networks

- AT & T Inc.

- Qoria Ltd.

- Alphabet Inc.

- Avast Software s.r.o

Frequently Asked Questions

The global market is projected to reach a value of US$ 3.9 billion by 2033, growing from US$ 1.8 billion in 2026, witnessing a CAGR of 11.5% from 2026 to 2033.

The primary drivers include the rising incidence of cyberbullying, increased screen time among children, and stringent government regulations like COPPA and the UK Online Safety Act.

The Android-based platform segment leads the market, accounting for approximately 61% of the share due to high global device volume and OS flexibility.

North America dominates the global market, driven by high digital literacy, widespread device ownership among minors, and a robust regulatory framework.

A significant opportunity lies in integrating AI and Machine Learning to provide real-time, context-aware monitoring of encrypted messaging apps and social media platforms.