- Non-food Packaging

- Packer Bottle Market

Packer Bottle Market Size, Share, and Growth Forecast 2026 - 2033

Packer Bottle Market by Material Type (Glass, Plastic, Metal, Others), by Capacity (<100 mL, 100-500 mL, 500 mL-1 L, 1 L), Closure Type (Screw Cap, Snap Cap, Child-Resistant Cap, Flip-Top Cap, Dropper, Pump), by Industry (Pharmaceuticals, Food & Beverages, Cosmetics & Personal Care, Chemicals, Nutraceuticals, Laboratory & Research), and Regional Analysis, 2026 - 2033

Packer Bottle Market Size and Trend Analysis

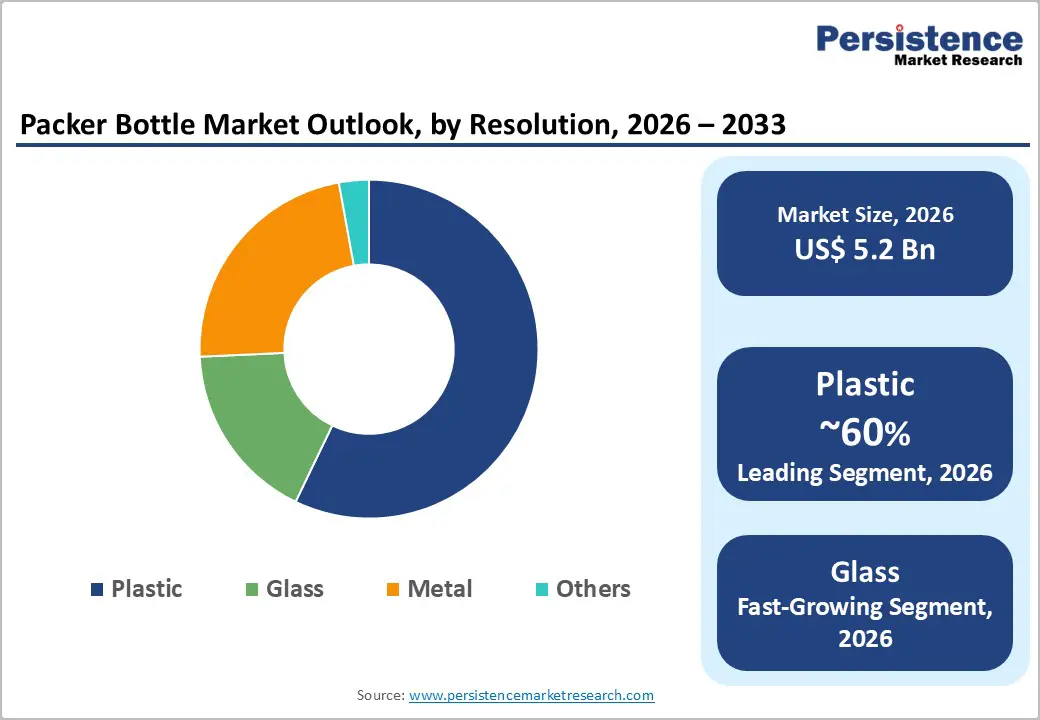

The global packer bottle market size is likely to be valued at US$ 5.2 Billion in 2026 and is expected to reach US$ 7.6 Billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033.

Rising demand from the expanding pharmaceutical and nutraceutical industries drives this growth, as packer bottles provide essential UV protection for light-sensitive products like tablets, capsules, and supplements.

Key Market Highlights

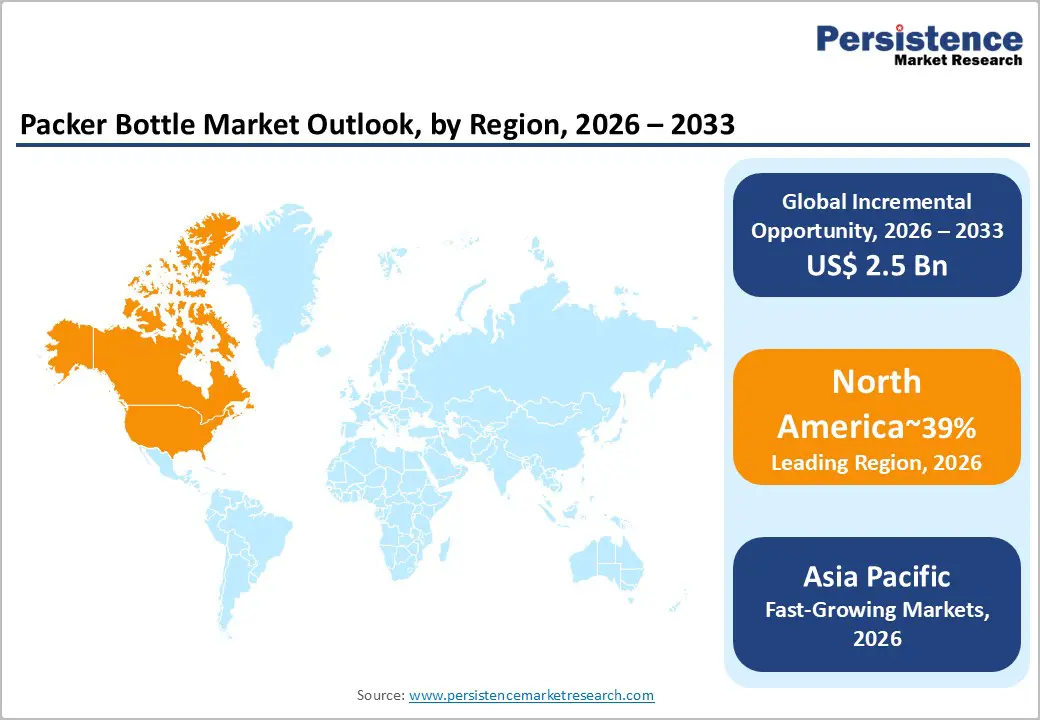

- Leading Region: North America leads the market, holding 39% share, due to US pharma dominance and FDA regulations driving compliant packer bottle demand.

- Fastest Growing Region: The Asia Pacific is the fastest-growing region, with a rising CAGR of 7.2%, driven by China and India's manufacturing for pharmaceutical exports.

- Leading Segment: Plastic dominates Material Type with 60% share for versatile pharma packaging.

- Fastest Growing Segment: 100-500 mL is the fastest growing Capacity segment at 6.8% CAGR, ideal for dosing in nutraceuticals.

- Key Opportunity: Sustainable smart packaging offers a key opportunity amid EU regulations and pharma personalization.

| Key Insights | Details |

|---|---|

| Packer Bottle Market Size (2026E) | US$ 5.2 Billion |

| Market Value Forecast (2033F) | US$ 7.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Driver - Pharmaceutical and Nutraceutical Industry Expansion Driving Sustained Demand for Protective and UV-Resistant Packer Bottle Packaging

The rapid expansion of the pharmaceutical and nutraceutical industries is a key driver of growth in the global packer bottle market. Rising global population, increasing life expectancy, and growing awareness of preventive healthcare have significantly boosted demand for medicines, vitamins, and dietary supplements. These products often require UV-resistant and moisture-protective packaging to maintain their stability and effectiveness over time. Packer bottles are widely used because they protect light-sensitive formulations such as tablets, capsules, and syrups from degradation.

Pharmaceutical sales in the United States reached a significant level, reflecting strong production volumes that directly increase demand for reliable packaging solutions. As healthcare access improves across developing and developed regions, manufacturers are scaling production, further supporting packer bottle consumption. The growing focus on chronic disease management, self-medication, and wellness supplements reinforces long-term demand, convincing stakeholders that the market will continue to grow steadily alongside healthcare sector expansion.

Strict Global Regulatory Frameworks Accelerating Adoption of Tamper-Evident and Child-Resistant Packer Bottle Solutions

Strict regulatory requirements across the pharmaceutical, chemical, and food industries significantly support the adoption of packer bottles. Regulatory authorities such as the US FDA, CPSC, and European agencies mandate packaging standards focused on product safety, tamper resistance, and child protection. These regulations require manufacturers to use packaging that ensures product integrity during storage, transportation, and consumer use. Packer bottles equipped with tamper-evident and child-resistant features help companies comply with these mandatory guidelines while minimizing risks of contamination, misuse, or accidental ingestion.

In Europe, transport and safety directives further reinforce the need for durable and compliant packaging formats. Regulatory compliance also enhances consumer trust, which is particularly critical in healthcare-related products. Pharmaceutical production volumes are expected to rise, indirectly increasing packaging demand. As regulations continue to tighten, packer bottles remain a preferred solution for compliant packaging.

Restraint - Rising Environmental Concerns and Anti-Plastic Regulations Creating Sustainability Challenges for Traditional Packer Bottle Materials

Growing environmental concerns and rising scrutiny over plastic waste present a notable restraint for the packer bottle market, particularly for conventional plastic packaging. Governments and regulatory bodies worldwide are introducing stricter rules to reduce single-use plastics and improve recycling rates. The European Union, for instance, has implemented policies to minimize plastic waste and promote circular economy practices. These regulations, combined with increasing consumer awareness, are shifting preferences toward eco-friendly and sustainable packaging alternatives.

Traditional plastic packaging bottles are criticized for their contribution to environmental pollution and landfill accumulation. Additionally, compliance with sustainability norms often increases production costs, as manufacturers must invest in new materials, recycling technologies, or redesigns. These factors can limit scalability and slow market adoption, especially in price-sensitive regions. As sustainability expectations continue to rise, manufacturers are under pressure to innovate quickly, making environmental concerns a key challenge impacting market growth.

Supply Chain Disruptions and Volatile Raw Material Prices Limiting Cost Stability and Production Efficiency in Packer Bottles

Global supply chain disruptions and volatile raw material prices have emerged as significant challenges for the packer bottle market. Events such as pandemics, geopolitical tensions, and logistics bottlenecks have affected the availability of key raw materials, including HDPE, PET, and polypropylene resins. Fluctuating resin prices increase production costs for bottle manufacturers, directly impacting profit margins and pricing strategies.

Delays in raw material supply can disrupt production schedules, leading to shortages for end-use industries such as pharmaceuticals, nutraceuticals, and cosmetics. These disruptions are particularly problematic in regions where manufacturers rely heavily on imports for resin supply. As a result, companies may be forced to raise prices, reduce output, or delay product launches, affecting competitiveness in cost-sensitive markets. While some manufacturers are diversifying their supplier base or increasing inventory buffers, ongoing volatility continues to constrain market growth and adds uncertainty to long-term planning.

Opportunity - Growing Innovation in Sustainable and Recyclable Materials, Unlocking New Growth Opportunities for Packer Bottle Manufacturers

Innovation in sustainable materials presents a strong growth opportunity for the packer bottle market. Manufacturers are increasingly investing in eco-friendly alternatives such as bioplastics, recycled polypropylene, and monomaterial designs to align with global sustainability goals. Regulations like the EU Packaging Regulation 2025/40 are accelerating the shift toward recyclable and low-impact packaging solutions. These advanced materials offer improved barrier properties, durability, and compatibility with pharmaceutical applications while reducing environmental footprint.

Berry Global’s ClariPPil bottles have achieved RecyClass A certification, highlighting their recyclability and market acceptance. Sustainability-driven innovation also aligns well with the growing e-commerce and direct-to-consumer health product segments, in which packaging plays a key role in branding. In nutraceuticals, premium brands increasingly use green packaging to differentiate themselves and attract environmentally conscious consumers. As sustainability becomes a competitive advantage, the adoption of innovative materials is expected to drive long-term market growth.

Advancements in Smart Packaging Technologies Enhancing Patient Safety, Compliance, and Value Creation in Packer Bottle Applications

Smart packaging technologies are creating new growth avenues within the packer bottle market, particularly in pharmaceutical and home-care segments. Features such as tamper-evident seals, RFID tracking, and advanced child-resistant closures enhance product safety, traceability, and patient compliance. Regulatory bodies like the FDA encourage the adoption of packaging that improves medication adherence and reduces misuse. Innovations such as Gerresheimer’s Gx Cap, which integrates digital tracking and smart closure systems, support personalized medicine and remote patient monitoring trends.

These technologies are especially valuable for biologics, specialty drugs, and chronic disease treatments that require precise dosing and monitoring. As the global burden of chronic illnesses rises, demand for intelligent packaging solutions continues to grow. Smart packaging not only improves patient safety but also generates additional value for manufacturers and investors by enabling premium pricing, data integration, and long-term differentiation in high-growth pharmaceutical markets.

Category-wise Analysis

Material Type Insights

Plastic dominates the material segment, accounting for approximately 60% of the packer bottle market due to its versatility, lightweight, and cost efficiency. Materials such as HDPE, PET, and polypropylene are widely preferred across pharmaceutical, nutraceutical, and food applications. Plastic bottles offer excellent moisture resistance and sufficient barrier protection, making them suitable for tablets, capsules, and liquid formulations.

Their ability to be molded into various shapes and sizes provides flexibility for branding and functional design. Additionally, plastic supports high-volume, scalable manufacturing, which is essential for large pharmaceutical producers. Compared with glass bottles, plastic bottles are less fragile, easier to transport, and more economical for everyday use. Despite growing sustainability concerns, plastic continues to dominate due to ongoing innovations in recyclable and monomaterial designs that address environmental regulations while preserving performance and affordability.

Capacity Insights

The 100-500 mL capacity segment leads the packer bottle market with an estimated 45% share, driven by its suitability for pharmaceutical and nutraceutical applications. This size range offers an optimal balance among product volume, dosing accuracy, and consumer convenience. Bottles in this category, such as 200 cc containers, are commonly used to dispense capsules, tablets, and liquid supplements.

Their compact size supports efficient storage, transportation, and shelf placement, making them attractive for both manufacturers and retailers. This capacity range aligns well with standard dosage requirements and capsule size charts, ensuring consistency across product lines. Additionally, smaller- to mid-sized bottles reduce waste and improve portability, which is increasingly important for on-the-go consumers. The widespread adoption of this segment across multiple end-use industries reinforces its dominance and supports steady demand growth.

Closure Type Insights

Child-resistant caps hold the largest share in the closure type segment, accounting for approximately 40% of the market. Their dominance is driven by strict safety regulations enforced by agencies such as the FDA and the US Consumer Product Safety Commission. These closures are mandatory for pharmaceutical products to prevent accidental ingestion by children. Common designs include push-and-turn and squeeze-and-turn mechanisms, which effectively restrict child access while remaining user-friendly for adults.

These closures are tested and certified under standards such as ISO 8317, ensuring consistent safety performance. The growing emphasis on patient safety, especially for prescription medications and supplements, continues to support adoption. As pharmaceutical portfolios expand to include potent drugs and home-use therapies, the demand for reliable child-resistant closures remains strong, reinforcing their leadership position within the packer bottle market.

Industry Insights

The pharmaceutical industry dominates the end-use segment, accounting for nearly 50% of total packer bottle demand. This dominance is driven by the extensive use of packer bottles for tablets, capsules, syrups, and other oral medications that require protection from UV light and moisture. Compliance with FDA and global regulatory standards makes packer bottles an essential packaging solution for pharmaceutical manufacturers.

Packer bottles help maintain product efficacy, extend shelf life, and ensure safe handling throughout the supply chain. As pharmaceutical R&D and production continue to expand globally, the sector is expected to remain the largest and most stable end user of packer bottles.

Regional Insights

North America Packer Bottle Market Trends

North America demonstrates strong growth potential for the packer bottle market, driven primarily by the United States’ leadership in pharmaceutical production. With pharmaceutical sales exceeding USD 678 billion in 2023, the region generates consistent demand for compliant and high-quality packaging solutions. Strict FDA regulations on child-resistant and tamper-evident packaging encourage ongoing innovation in pack-and-bottle designs.

Healthcare spending in the US is projected to reach USD 7.1 trillion by 2031, further supporting long-term packaging demand. An aging population and rising prevalence of chronic diseases contribute to increased medication consumption. Leading companies such as Berry Global are actively investing in sustainable and recyclable packaging solutions, strengthening the regional ecosystem. These factors collectively position North America as a mature yet innovation-driven market for packer bottles.

Europe Packer Bottle Market Trends

Europe’s packer bottle market is shaped by strong regulatory harmonization and a clear focus on sustainability. Countries such as Germany, the UK, and France are implementing the EU Packaging Regulation 2025/40, which emphasizes recyclability, waste reduction, and circular economy principles. Pharmaceutical packaging manufacturers are increasingly adopting monomaterial designs and recycled plastics to meet these requirements. Companies like Gerresheimer are integrating smart packaging technologies to enhance quality, traceability, and patient safety.

Sustainability-driven innovation has strengthened market resilience despite regulatory pressures. Spain and other Southern European markets are also aligning with these standards, promoting eco-friendly pharmaceutical packaging solutions. Europe’s robust regulatory framework and commitment to sustainable practices continue to drive steady demand and encourage technological advancements in the packer bottle market.

Asia Pacific Packer Bottle Market Trends

Asia-Pacific is the fastest-growing region for the packer bottle market, supported by expanding pharmaceutical manufacturing in China, India, and Japan. China accounts for approximately 42% of the regional pharmaceutical packaging market, benefiting from large-scale production capacity and export-driven demand. India’s rapidly growing biogenetic drug industry further fuels the need for cost-effective and compliant packaging solutions. Infrastructure expansion, favorable government policies, and rising healthcare access across ASEAN countries contribute to market growth.

Cost advantages and availability of skilled labor make the region attractive for global pharmaceutical outsourcing. Additionally, increasing domestic consumption of medicines and nutraceuticals supports sustained demand. As regional manufacturers scale production and adopt international quality standards, Asia Pacific is expected to remain a key growth engine for the global packer bottle market.

Competitive Landscape

The global packer bottle market is moderately fragmented, with leading players such as Berry Global and Gerresheimer collectively holding around 37% market share. These companies leverage strong R&D capabilities, global manufacturing footprints, and strategic acquisitions to maintain competitive advantage. Market leaders focus on developing recyclable materials, smart closures, and customized pharmaceutical packaging solutions.

Smaller and emerging players compete through niche offerings, clean-room manufacturing, and flexible production models. The rise of e-commerce and direct-to-consumer healthcare products has intensified competition, encouraging innovation and differentiation. Sustainability, regulatory compliance, and advanced packaging features remain key strategic priorities. Overall, the competitive landscape reflects a balance between established multinational players and agile regional manufacturers, supporting steady market evolution and innovation.

Key Market Developments

- In October, 2024: Berry Global launched its ClariPPil clarified polypropylene bottles, offering enhanced recyclability with RecyClass A certification for nutraceuticals and healthcare applications, promoting sustainability and improved product protection versus traditional PET packaging.

- In July, 2024: Silgan Holdings agreed to acquire Weener Plastics for €838 million, strengthening its dispensing and specialty closures portfolio across healthcare, personal care, and food markets.

- In November, 2024: Berry Global introduced new LDPE easy-squeeze ophthalmic bottles qualified with Aptar Pharma’s dispenser, enhancing ergonomic delivery for preservative-free eye care products.

Companies Covered in Packer Bottle Market

- Berry Global Group, Inc.

- Amcor Plc

- Coveris Holdings S.A.

- Gerresheimer AG

- Comar LLC

- Graham Packaging Company

- Maynard & Harris Plastics

- Alpha Packaging Inc

- O-Berk Company LLC

- Clarke Container Inc

- United States Plastic Corporation

- Resilux NV

- Silgan Holdings Inc.

- Plastipak Holdings, Inc.

- Altium Packaging

- Bericap GmbH & Co KG

Frequently Asked Questions

The market is valued at US$ 5.2 Billion in 2026, reaching US$ 7.6 Billion by 2033 at 5.6% CAGR.

Expansion in pharmaceutical and nutraceutical sectors, plus FDA regulations, boosts need for UV-protective packaging.

Pharmaceuticals dominates with 50% share due to stability needs for medications.

North America leads via US pharma sales and regulatory frameworks.

Sustainable materials and smart tech like RFID for pharma personalization.

Leaders include Berry Global, Amcor Plc, and Gerresheimer AG focusing on innovations.