- Pharmaceuticals

- Osteoporosis Drugs Market

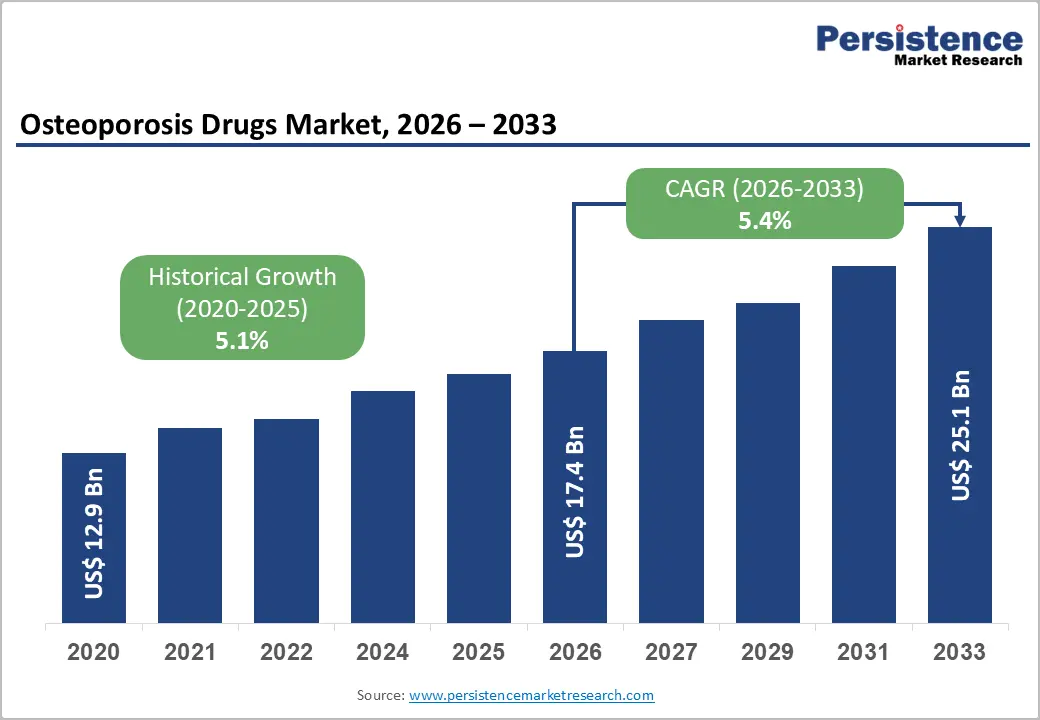

Osteoporosis Drugs Market Size, Share, and Growth Forecast, 2026 - 2033

Osteoporosis Drugs Market by Disease Type (Primary Osteoporosis, Secondary Osteoporosis), Drug Class (Bisphosphonates, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis for 2026 - 2033

Osteoporosis Drugs Market Share and Trends Analysis

The global osteoporosis drugs market size is likely to be valued at US$17.4 billion in 2026 and is estimated to reach US$25.1 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026 - 2033, driven by an accelerating global aging demographic, expanding regulatory approvals for novel bone-modifying agents, and the integration of biologic therapies into standard clinical protocols.

The consistent rise in the population aged 60 years and above, as documented by the United Nations Department of Economic and Social Affairs, directly translates into a structurally larger patient pool requiring long-term pharmacological intervention for bone density preservation.

Key Industry Highlights:

- Leading Disease Type: Primary osteoporosis is set to hold around 74% revenue share in 2026, driven by the expanding global postmenopausal patient demographic experiencing estrogen deficiency.

- Fastest-growing Disease Type: Secondary osteoporosis is projected as the fastest-growing segment, supported by the rising incidence of drug-induced bone density loss.

- Leading Drug Class: Bisphosphonates are estimated to hold roughly 42% revenue share in 2026, due to extensive integration within first-line public reimbursement frameworks.

- Fastest-growing Drug Class: RANK ligand inhibitors are forecast to record the fastest growth, driven by superior clinical efficacy and high compliance subcutaneous dosing profiles.

- Regional Leadership: North America is projected to capture roughly 41% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to rapid demographic aging.

- Competitive Environment: The market reflects a consolidated structure, with key players such as Amgen Incorporated and Eli Lilly and Company leveraging specialized biological IP portfolios.

DRO Analysis

Driver - Growth in post-fracture secondary prevention treatments

Growth in post-fracture secondary prevention treatments has become a major driver of the osteoporosis drugs market due to the high risk of recurrent fractures after an initial event. Patients who experience hip, vertebral, or wrist fractures are significantly more likely to suffer subsequent fractures, leading to increased morbidity, mortality, and healthcare costs. As a result, healthcare systems are increasingly adopting fracture liaison services (FLS) and structured post-fracture care pathways to ensure early diagnosis and timely initiation of osteoporosis therapy. This includes the use of anti-resorptive and anabolic agents to strengthen bone density and reduce future fracture risk. Additionally, hospitals and insurers are emphasizing long-term adherence to treatment protocols, which is boosting sustained drug demand and improving patient outcomes in secondary prevention settings.

Restrain - Drug contraindications in specific populations

Drug contraindications in specific patient populations represent a significant restraint in the osteoporosis drugs market, as they limit the eligible treatment pool and reduce overall drug utilization. Many commonly prescribed osteoporosis therapies, such as bisphosphonates or selective estrogen receptor modulators (SERMs), are not suitable for patients with severe renal impairment, active gastrointestinal disorders, or a history of thromboembolic events. Similarly, anabolic agents like teriparatide may be contraindicated in individuals with prior skeletal malignancies or unexplained elevated alkaline phosphatase levels due to safety concerns. Elderly patients, who form the core target population, often present with multiple comorbidities, making drug selection more complex and restrictive. These contraindications necessitate careful patient screening and limit the use of first-line therapies in real-world settings. As a result, clinicians often resort to less effective alternatives or delayed treatment initiation, ultimately affecting market penetration and therapeutic outcomes in osteoporosis management.

Opportunity - Development of oral bone-forming drugs

The development of oral bone-forming drugs represents a major innovation opportunity in the osteoporosis drugs market, particularly as it addresses long-standing limitations of injectable anabolic therapies. Current bone-building treatments, such as parathyroid hormone (PTH) analogs and sclerostin inhibitors, are primarily administered via subcutaneous injections, which often reduce patient compliance due to discomfort, administration complexity, and long treatment duration. Oral peptide-based therapies under development aim to overcome these barriers by enabling non-invasive, patient-friendly dosing while maintaining or improving therapeutic efficacy. If successfully commercialized, these drugs could significantly improve long-term adherence, especially among elderly patients who struggle with self-injection. Additionally, oral formulations may expand treatment accessibility in settings and emerging markets. This shift is expected to enhance early intervention rates, reduce fracture risk burden, and create a new premium segment within osteoporosis therapeutics.

Category-wise Analysis

Disease Type Insights

Primary osteoporosis is anticipated to secure around 74% of the osteoporosis drugs market share in 2026, reflecting the expanding global population of postmenopausal women experiencing estrogen deficiency. Postmenopausal patients receiving denosumab injections show substantial reductions in bone turnover markers within clinical centers. This high disease prevalence guarantees steady demand for standard long-term therapeutic interventions.

Secondary osteoporosis is expected to be the fastest-growing segment, propelled by rising systemic medical conditions and long-term glucocorticoid prescriptions that induce rapid bone loss. For example, patients undergoing chronic rheumatoid arthritis therapies require concurrent bone protection treatments to prevent secondary bone density depletion. This growing clinical population requires specialized pharmacological interventions to mitigate medication-induced bone fragility.

Drug Class Insights

Bisphosphonates are poised to dominate with a forecast market share of over 42% in 2026, powered by high healthcare infrastructure integration and extensive generic availability that lowers cost barriers. Oral alendronate tablets serve as the standard first-line intervention within global public health insurance reimbursement systems. This deep therapeutic entrenchment maintains large-scale procurement volumes across global healthcare systems.

RANK Ligand Inhibitors are estimated to be the fastest-growing segment, fueled by exceptional clinical efficacy profiles and convenient semi-annual subcutaneous administration routes. Denosumab therapy demonstrates superior long-term bone mineral density improvements compared to traditional oral regimens in clinical trials. This strong physician preference accelerates brand adoption over conventional small-molecule drug choices.

Distribution Channel Insights

Hospital pharmacies are likely to be the leading segment with a projected 48% of the osteoporosis drugs market share in 2026, due to institutional centralization of initial fracture admissions and intravenous drug administrations. Zoledronic acid infusions are administered directly within specialized hospital outpatient departments. This controlled environment ensures dominant hospital control over complex biological therapy distribution channels.

Online pharmacies are anticipated to be the fastest-growing segment, fueled by rapid growth in digital prescription management systems and continuous home-delivery conveniences for chronic therapies. For example, elderly patients utilize digital mail-order pharmacy networks to receive continuous monthly oral therapies without traveling to physical storefronts. This shifting consumer behavior expands digital retail pharmaceutical distribution networks globally.

Regional Insights

North America Osteoporosis Drugs Market Trends

North America is expected to lead with an estimated 41% of the osteoporosis drugs market share in 2026, supported by comprehensive healthcare reimbursement frameworks and rapid adoption of novel biologics. High clinical awareness regarding bone density management, combined with advanced diagnostic infrastructure, accelerates early therapeutic prescription patterns across regional healthcare systems.

U.S. Osteoporosis Drugs Market Insights

The U.S. is projected to experience substantial revenue expansion due to high private capital investments in biopharmaceutical innovation and supportive Medicare coverage policies for injectable therapies. Rising domestic clinical deployment of anabolic bone-forming agents, such as abaloparatide, drives premium segment growth within institutional hospital networks.

Canada Osteoporosis Drugs Market Insights

Canada is forecast to register a steady market growth, driven by public health initiatives focusing on systematic fracture liaison services within regional provincial medical systems. Increased utilization of long-acting anti-resorptive interventions among aged demographics stabilizes long-term pharmaceutical demand across municipal distribution networks.

Europe Osteoporosis Drugs Market Trends

Europe is likely to maintain a prominent market position due to centralized healthcare procurement models and established clinical guidelines prioritizing bone health preservation in aging populations. Strict European Medicines Agency pharmacovigilance frameworks ensure high manufacturing compliance and accelerate biosimilar therapeutic integration.

Germany Osteoporosis Drugs Market Insights

Germany is expected to demonstrate robust development owing to its high domestic manufacturing infrastructure and expansive statutory health insurance coverage for specialized rheumatology interventions. Increasing clinical enrollment in sequential therapeutic protocols enhances long-term drug utilization rates across primary care networks.

U.K. Osteoporosis Drugs Market Insights

The U.K. is anticipated to expand its market presence through National Health Service initiatives targeting early osteoporosis screening and centralized bulk therapeutic procurement strategies. Rising deployment of cost-efficient biological alternatives optimized via digital health monitoring systems reduces the overall treatment delivery costs.

Asia Pacific Osteoporosis Drugs Market Trends

Asia Pacific is forecast to be the fastest-growing market for osteoporosis drugs, stimulated by rapid demographic aging, rising per capita healthcare expenditures, and expanding medical infrastructure across developing economies. Government-led public health programs targeting bone density awareness accelerate therapeutic access across rural and urban communities.

Japan Osteoporosis Drugs Market Insights

Japan is expected to lead regional growth contributions due to its massive super-aged population and comprehensive long-term care insurance models covering advanced bone-preservation therapies. Domestic physician preferences for active vitamin D analogues and novel anabolic interventions drive continuous market value expansion.

China Osteoporosis Drugs Market Insights

China is projected to exhibit rapid volume growth driven by expanding centralized drug procurement programs and heavy state investments in urban hospital infrastructure. Accelerated domestic regulatory approvals for advanced international biological therapies expand available treatment options across provincial medical networks.

Competitive Landscape

The global osteoporosis drugs market is consolidated, with a select cohort of multinational biopharmaceutical corporations exercising substantial control over commercial distribution networks and therapeutic IP portfolios. Amgen Incorporated, Eli Lilly and Company, Pfizer Incorporated, Novartis AG, and Teva Pharmaceutical Industries Limited lead market operations through extensive global supply chains.

These enterprise entities maintain dominant positions by leveraging deep capital reserves, extensive clinical trial pipelines, and established institutional provider relationships. Regulatory compliance demands and specialized biological production requirements create high entry barriers that prevent smaller entities from challenging market leadership. Strategic market positioning relies on continuous lifecycle management and biosimilar defense strategies.

Key Industry Developments;

- In February 2026, CVS Health announced the replacement of Amgen Prolia and Eli Lilly Forteo with lower-cost biosimilar and generic alternatives across selected formularies, accelerating pricing competition in osteoporosis drug treatment access.

- In February 2025, CinnaGen received a positive European Medicines Agency opinion for Zandoriah® (teriparatide), a biosimilar to Eli Lilly Forsteo®, strengthening biosimilar competition in osteoporosis treatment across European healthcare systems.

- In June 2025, Sandoz International AG launched Jubbonti® and Wyost® denosumab biosimilars in the U.S., strengthening treatment accessibility for osteoporosis and bone-related disorders through interchangeable biologic alternatives.

Companies Covered in Osteoporosis Drugs Market

- Amgen

- Eli Lilly and Company

- Pfizer

- Novartis AG

- Teva Pharmaceutical Industries Limited

- Sandoz International AG

- F. Hoffmann-La Roche

- Merck & Co.

- Sanofi

- GlaxoSmithKline

- Asahi Kasei Corporation

- UCB

- Radius Health

- Viatris

Frequently Asked Questions

The global osteoporosis drugs market is projected to reach US$17.4 billion in 2026.

The osteoporosis drugs market is driven by rising aging population levels and increasing incidence of fragility fractures, which is increasing demand for advanced osteoporosis diagnosis and long-term pharmacological treatment.

The osteoporosis drugs market is poised to witness a CAGR of 5.4% from 2026 to 2033.

The osteoporosis drugs market is creating significant growth opportunities through the expansion of biosimilar therapies and increasing investment in anabolic bone-forming drugs that improve treatment accessibility and therapeutic innovation.

Some of the key market players include Amgen Incorporated, Eli Lilly and Company, Pfizer Incorporated, Novartis AG, and Teva Pharmaceutical Industries Limited.