- Medical Devices

- Osmolarity Testing Device Market

Osmolarity Testing Device Market Size, Share, and Growth Forecast, 2026 - 2033

Osmolarity Testing Device Market by Device Type (Benchtop, Portable, Consumables), Application (Dry Eye Disease Diagnosis, Research, Clinical Testing, Pre-Operative Assessment), End-User (Hospitals, Ophthalmic Clinics, Diagnostic Laboratories), and Regional Analysis for 2026-2033

Osmolarity Testing Device Market Share and Trends Analysis

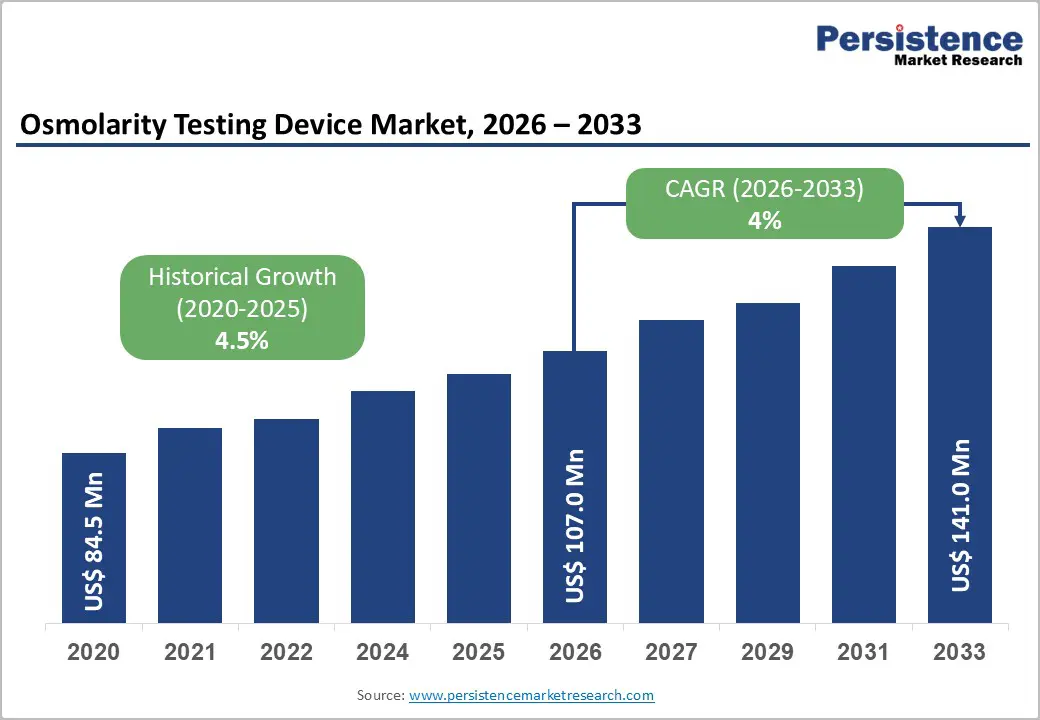

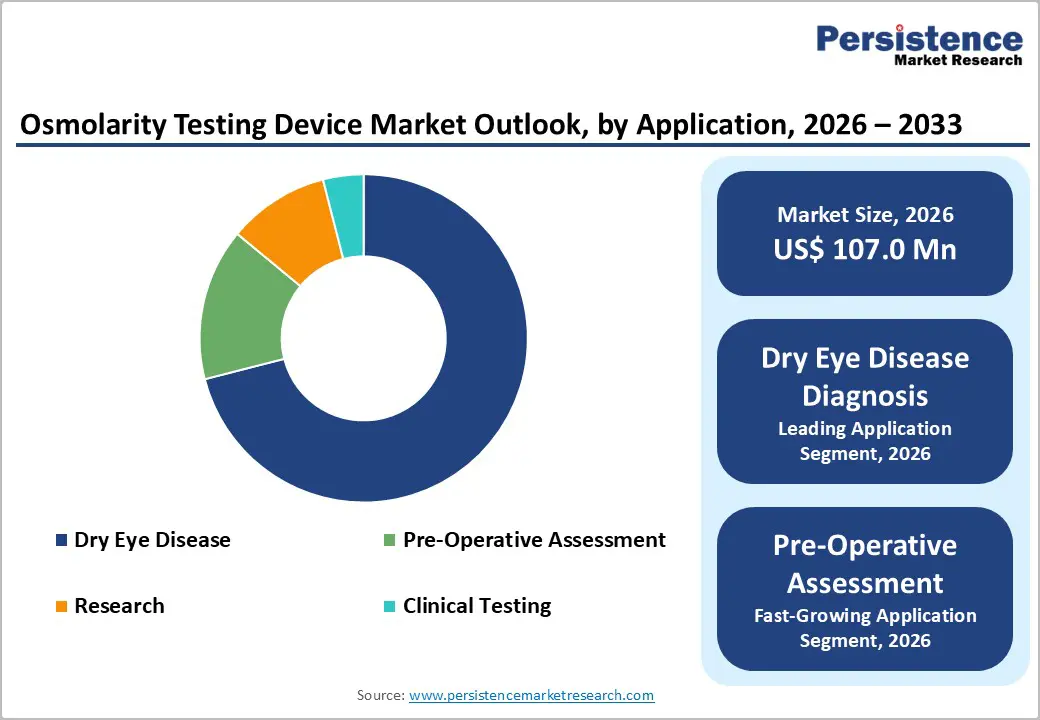

The global osmolarity testing device market size is likely to be valued at US$ 107.0 million in 2026, and is projected to reach US$ 141.0 million by 2033, growing at a CAGR of 4% during the forecast period 2026−2033. The market demonstrates sustained expansion driven by the increasing prevalence of ocular surface diseases, rising awareness about early diagnosis of dry eye syndrome, and technological advancements in point-of-care testing capabilities.

The growing geriatric population worldwide, combined with heightened screen time exposure among working professionals, creates a persistent demand for osmolarity-based diagnostic solutions. Healthcare infrastructure modernization in emerging economies and integration of automated diagnostic platforms into ophthalmology practices further accelerate market penetration, establishing osmolarity testing as a standard diagnostic protocol across developed and developing markets

Key Industry Highlights

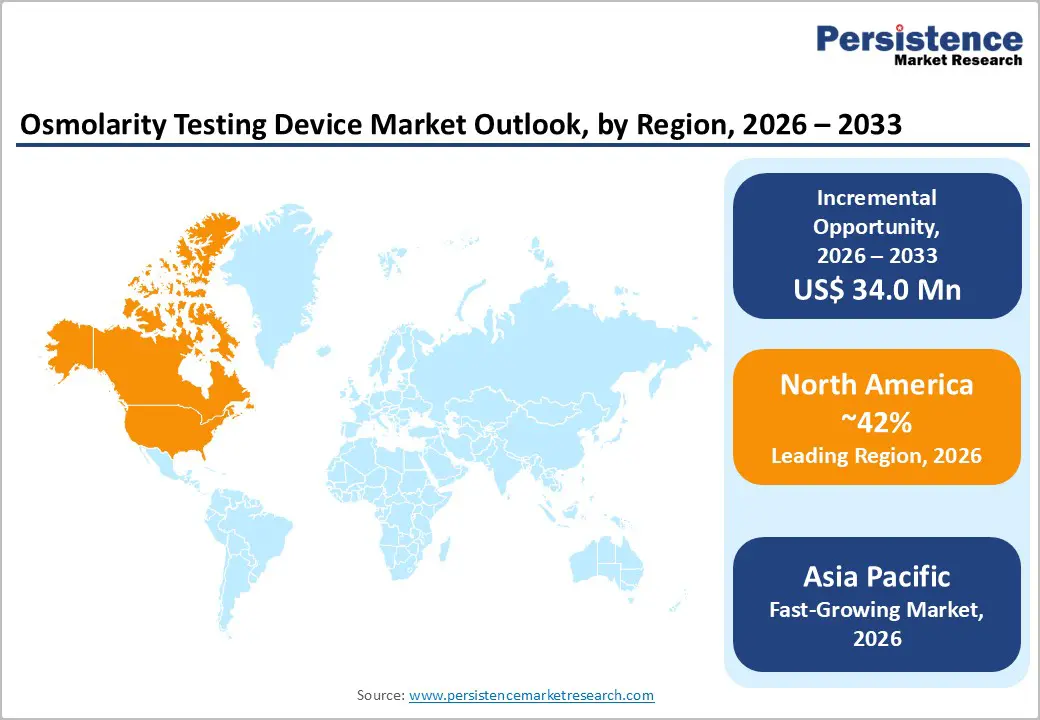

- Dominant Region: North America is expected to dominate with approximately 42% market share in 2026, supported by actives investments in ophthalmic research.

- Fastest-growing Market: The Asia Pacific market is set to be the fastest-growing from 2026 to 2033, due to the rising healthcare expenditure by national and state governments.

- Device Type Leadership: Benchtop devices are poised to lead with nearly 60% revenue share in 2026, while portable devices are likely to be the fastest-growing during the 2026-2033 forecast period.

- Application Dynamics: Dry eye disease diagnosis is slated to command around 71% of the revenue share in 2026, with pre-operative assessment growing the fastest over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

| Osmolarity Testing Device Market Size (2026E) | US$ 107.0 Mn |

| Market Value Forecast (2033F) | US$ 141.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Dry Eye Disease and Ocular Surface Disorders

The global burden of dry eye disease (DED) continues to rise sharply. The National Eye Institute (NEI) reports that dry eye affects nearly 16.4 million Americans, a common condition exacerbated by factors like prolonged screen time. The Tear Film and Ocular Surface Society (TFOS) pinpoints several key contributors. Extended sessions with digital screens dry out eyes quickly. Harsh environmental conditions, such as low humidity or pollution, worsen irritation. Underlying health issues, including autoimmune disorders, add further strain. Healthcare providers observe these factors driving a steady climb in DED cases worldwide.

Osmolarity testing stands out as the leading biomarker for diagnosing and treating ocular surface disorders. Clinicians identify elevated tear osmolarity levels as a definitive indicator of hyperosmolar states. International ophthalmology organizations back this method with rigorous clinical studies. Their strong endorsement encourages broad acceptance among professionals. Diagnostic centers integrate these devices into daily workflows. Specialized eye clinics rely on them for precise assessments. Primary care facilities incorporate the tools to catch issues early. Patients benefit from faster, more accurate interventions. This growing reliance transforms rising disease prevalence into consistent demand. Healthcare networks invest confidently in osmolarity testing equipment to meet clinical needs across various settings.

Technological Advancements in Point-of-Care (POC) Diagnostic Platforms

Advancements in microfluidics and lab-on-a-chip technologies are significantly improving osmolarity testing by reducing sample requirements and accelerating result generation. Engineers are developing compact systems that require only minimal fluid volumes while maintaining analytical accuracy, which is improving usability in clinical environments where sample collection may be limited. Modern analyzers are incorporating impedance-based measurement techniques that have received clearance from the United States Food and Drug Administration (FDA), which is strengthening confidence in performance reliability and regulatory compliance. Automated calibration and standardized measurement protocols are reducing operator-dependent variability, thereby improving reproducibility compared with conventional laboratory methods. Many devices are also integrating wireless connectivity and cloud-based data storage platforms that are enabling secure transfer, remote monitoring, and centralized management of diagnostic results across healthcare networks.

Integration with electronic health record (EHR) systems is further enhancing workflow efficiency by allowing clinicians to access test outcomes directly within patient management platforms. Automated testing capabilities are shortening examination times, which is enabling ophthalmologists to manage larger patient volumes without compromising diagnostic accuracy. Smaller clinics and independent practices are benefiting from simplified operation and reduced infrastructure requirements, which is lowering barriers to technology adoption. Medium-sized healthcare facilities are expanding diagnostic capabilities by incorporating point-of-care osmolarity testing into routine patient assessments. As technological accessibility continues improving, broader adoption across hospitals, specialty clinics, and community healthcare centers is expected to increase testing volumes.

Availability of Alternative Diagnostic Methodologies

The diagnostic approach for ocular surface disease is continuing to rely on several established clinical methods that provide practical and cost-effective evaluation in routine care. Clinicians are using Schirmer’s test to measure tear production, tear break-up time (TBUT) to assess tear film stability, and corneal fluorescein staining to identify epithelial surface damage. These techniques require minimal equipment investment and are therefore widely accessible across ophthalmology clinics and primary care settings. International professional bodies such as the American Academy of Ophthalmology (AAO) and the Tear Film and Ocular Surface Society (TFOS) are recommending osmolarity testing because of its quantitative precision, yet they are also emphasizing that no single diagnostic tool replaces comprehensive clinical assessment. Instead, osmolarity measurement is functioning as a complementary technique that enhances diagnostic confidence when combined with traditional evaluations.

Emerging diagnostic technologies are increasing competitive pressure within the market by offering alternative methods that address specific aspects of ocular surface pathology. Interferometry-based meibography systems are providing detailed imaging of meibomian gland structure, while matrix metalloproteinase-9 (MMP-9) immunoassays are enabling rapid detection of inflammatory markers at the point of care. Additional biomarker-based tests are expanding diagnostic insight into ocular surface inflammation and disease progression. These innovations are diversifying device options for healthcare providers, which is complicating procurement decisions and technology selection. Healthcare economic evaluations are demonstrating that conventional tests often remain more affordable, particularly in resource-constrained environments where budget limitations influence purchasing priorities. Osmolarity testing equipment involves higher upfront and operational costs in comprehensive diagnostic programs, which is encouraging decision-makers to carefully assess cost-benefit tradeoffs.

High Initial Capital Investment and Limited Reimbursement Coverage

Advanced osmolarity testing platforms are requiring significant upfront investment, which is creating adoption barriers for independent practitioners and small ophthalmology clinics with limited capital resources. Equipment acquisition costs are being compounded by recurring expenses associated with single-use test cartridges that are necessary for each diagnostic procedure, which is increasing operational expenditure over time. In regions where healthcare spending is highly price sensitive, these financial pressures are becoming more pronounced. Reimbursement variability across healthcare systems is further affecting return on investment because insurance coverage often does not fully compensate testing costs. The AAO is indicating that private insurers may provide partial reimbursement under certain clinical conditions, yet payment levels frequently remain insufficient to offset equipment and consumable expenses. In emerging economies, where out-of-pocket healthcare spending remains common, patient affordability concerns are limiting testing adoption and reducing procedure volumes.

Small healthcare providers are continuing to face extended financial recovery periods due to these economic constraints. Under optimal utilization conditions, investment payback is typically estimated at 18 to 24 months, while lower patient throughput or limited reimbursement support may extend recovery timelines beyond 36 months. These financial dynamics are slowing market expansion, particularly in cost-sensitive settings. Strategic financing solutions such as equipment leasing arrangements and vendor partnerships are helping reduce upfront burdens for clinics. Healthcare providers are also negotiating bulk purchasing agreements for consumables to improve cost efficiency and operational margins. Advocacy efforts aimed at improving reimbursement policies are expected to support better alignment between diagnostic value and payment structures in the future.

Expansion into Emerging Healthcare Markets

Asia Pacific, Latin America, and the Middle East are presenting significant growth opportunities for osmolarity testing devices as healthcare systems are modernizing and diagnostic capabilities are expanding. Governments in these regions are investing in hospital infrastructure, digital health programs, and universal health coverage initiatives, which is increasing access to advanced medical technologies. Rising disposable income levels are enabling more patients to seek specialized eye care services, while public awareness campaigns are promoting preventive ophthalmic screening and early disease detection. Rapid growth of middle-class populations in countries such as India and China is further strengthening demand for diagnostic tools that support early intervention and chronic condition management. Local distributors are forming partnerships with global medical device manufacturers to facilitate regulatory approval, distribution logistics, and clinician training.

Regional regulatory harmonization initiatives are also improving market accessibility. The ASEAN Medical Device Directive (AMDD) is simplifying approval processes across multiple Southeast Asian countries, which is reducing administrative barriers for manufacturers. Healthcare expenditure across these emerging regions is continuing to rise as governments prioritize population health outcomes and preventive care strategies. Multinational companies that are investing early are gaining first-mover advantages by establishing brand recognition and clinical familiarity among healthcare providers. Development of local manufacturing and assembly hubs is reducing distribution costs and improving supply chain efficiency. Providers are adopting bundled service models that integrate osmolarity testing with broader ophthalmic diagnostics to enhance revenue sustainability. As clinical protocols evolve, payers are aligning reimbursement structures with preventive care objectives, which is supporting routine device integration into clinical workflows.

Clinical Research Expansion and New Therapeutic Development

Pharmaceutical companies conducting clinical trials for emerging dry eye therapies are increasingly incorporating osmolarity testing as an essential measurement parameter because it provides objective assessment of ocular surface status. Researchers are frequently designating tear osmolarity as a primary or secondary endpoint in study protocols, which is strengthening its importance in therapeutic evaluation. The National Institutes of Health (NIH) is tracking multiple ongoing trials that include osmolarity assessment, reflecting its relevance in clinical research. Contract research organizations (CROs) are relying on standardized diagnostic platforms across trial sites to ensure consistent data quality, while academic medical centers are selecting validated devices that meet regulatory expectations. Regulatory authorities such as the U.S. FDA and the European Medicines Agency (EMA) are recognizing tear osmolarity as a credible biomarker for dry eye disease evaluation, which is encouraging pharmaceutical developers to integrate this measurement into regulatory submissions.

Healthcare providers are also expanding the clinical use of osmolarity testing beyond dry eye diagnosis into multiple specialty applications, which is broadening the market potential. Contact lens practitioners are using osmolarity measurements to optimize lens fitting and patient comfort, while refractive surgeons are incorporating testing into preoperative screening protocols to improve surgical outcomes. Oncology specialists are monitoring ocular complications such as graft-versus-host disease in patients undergoing bone marrow transplantation, which is demonstrating additional clinical utility. Diversification across medical disciplines is reducing dependence on a single indication and is strengthening long-term demand stability. Industry consultants are recommending strategic bundling of diagnostic devices with clinical trial support services to enhance value propositions for research sponsors. Companies that are positioning osmolarity platforms as essential tools for regulatory compliance, data accuracy, and patient management are capturing opportunities within research networks and specialty care environments.

Category-wise Analysis

Device Type Insights

Benchtop devices are slated to lead with approximately 60% of the osmolarity testing device market revenue share in 2026. These devices provide high analytical precision and consistent performance in specialized clinical environments. Ophthalmology clinics, research laboratories, and hospital-based diagnostic centers are relying on these systems for complex testing requirements that demand accuracy and reproducibility. Advanced capabilities such as automated sample handling, integrated data management software, and multi-sample processing are supporting high-throughput workflows and improving operational efficiency in settings with large patient volumes. These features are enabling clinicians and researchers to maintain standardized testing protocols while reducing manual intervention. Despite their limitations, institutional buyers are continuing to invest in benchtop platforms due to their established reliability and performance advantages in critical diagnostic applications.

Portable osmolarity testing devices are expected to experience the fastest growth between 2026 and 2033, as healthcare delivery models increasingly emphasize point-of-care diagnostics and decentralized patient management. Advances in miniaturized sensor technology, battery performance, and ergonomic design are enabling lightweight devices that provide rapid results in diverse clinical environments. Primary care clinics, outpatient centers, and community healthcare programs are adopting portable solutions because they improve accessibility in locations with limited infrastructure. These devices are particularly valuable in emerging markets and outreach initiatives that focus on early screening for ocular surface disease. Continuous product improvements are enhancing measurement reliability and usability, allowing this segment to capture expanding opportunities as healthcare systems prioritize flexibility, mobility, and cost-effective deployment strategies.

Application Insights

Dry eye disease diagnosis is poised dominate with nearly 71% of the osmolarity testing market share in 2026 because the condition affects a large global patient population and requires objective measurement for accurate management. Tear osmolarity testing is providing clinicians with quantitative insight into tear film instability, which is supporting precise treatment selection and monitoring of therapeutic response. Growing awareness among healthcare professionals and patients regarding the importance of early detection is strengthening demand for reliable diagnostic tools. Increasing prevalence of dry eye disease associated with aging populations, digital device usage, and environmental factors is further reinforcing segment dominance and sustaining long-term demand for objective diagnostic solutions.

Pre-operative assessment is expected to record the fastest growth between 2026 and 2033 due to rising surgical procedure volumes and greater emphasis on optimizing ocular surface health before intervention. The American Society of Cataract and Refractive Surgery (ASCRS) is identifying undiagnosed dry eye as a major contributor to patient dissatisfaction following procedures such as laser-assisted in situ keratomileusis (LASIK) and premium intraocular lens implantation. Surgeons are integrating osmolarity testing into preoperative screening protocols to detect subclinical tear film abnormalities that may affect surgical outcomes. The International Society of Refractive Surgery (ISRS) is tracking millions of vision correction procedures annually, which is expanding the addressable patient base for diagnostic evaluation. Patients undergoing elective surgical procedures are generally more willing to accept additional testing costs, particularly when improved outcomes and satisfaction are expected.

Regional Insights

North America Osmolarity Testing Device Market Trends

North America is set to command approximately 42% of the market share in 2026. Advanced healthcare systems drive robust demand across the region. Widespread insurance plans cover diagnostic eye services comprehensively. Practitioners and patients recognize dry eye disease risks clearly. The U.S. FDA applies rigorous standards to ensure device quality. Providers trust these platforms for consistent performance in daily use. Major ophthalmology and optometry societies endorse osmolarity measurements in official guidelines. Evidence-based practices shape clinical decisions effectively. Leading manufacturers base headquarters in the United States. They invest heavily in research and development for cutting-edge solutions. Clinical validation studies reinforce product credibility among users.

Reimbursement programs, such as Medicare coverage under Current Procedural Terminology (CPT) code 83861, support widespread adoption. Senior populations expand rapidly, creating steady testing needs. Systemic autoimmune disorders rise steadily, boosting diagnostic volumes. Contact lens wearers seek precise evaluations routinely. Digital screen exposure heightens eye strain awareness nationwide. Established ophthalmic firms compete with agile startups actively. This dynamic spurs continuous technological improvements across the sector. Platform companies need to focus on standardizing osmolarity protocols in acquired networks, enhancing service offerings and revenue streams efficiently.

Europe Osmolarity Testing Device Market Trends

Europe is likely to emerge as the second-largest market for osmolarity testing devices due to comprehensive healthcare coverage systems and strong investment in advanced diagnostics. Public health insurance frameworks across the region are supporting consistent demand by reimbursing clinically validated procedures, which is enabling healthcare providers to integrate osmolarity testing into routine ophthalmic care. High per-capita healthcare expenditure and well-established ophthalmology networks are facilitating broad technology adoption across hospitals and specialty clinics. Germany is leading regional utilization with robust infrastructure and reimbursement support through the statutory health insurance system known as Gesetzliche Krankenversicherung (GKV). The U.K., France, and Spain are also contributing significantly through varied reimbursement mechanisms and national healthcare models.

Manufacturers that successfully navigate European regulatory requirements are gaining competitive advantages because conformity assessment and certification processes are complex and demand substantial expertise. Harmonized regulatory frameworks across European Union (EU) member states are simplifying multi-country market entry once compliance is achieved, which is supporting regional expansion strategies. In the U.K., the National Health Service (NHS) is evaluating cost-effectiveness through assessments conducted by the National Institute for Health and Care Excellence (NICE) before approving widespread technology adoption. France is increasing awareness through public health initiatives and patient advocacy efforts that emphasize early detection of ocular conditions. Private ophthalmology practices are targeting higher-income patient segments with premium diagnostic services that include osmolarity testing.

Asia Pacific Osmolarity Testing Device Market Trends

Rapid healthcare modernization is increasing demand for advanced diagnostic technologies across Asia Pacific, as governments prioritize vision care within national health strategies. Programs such as Healthy China 2030 are promoting preventive healthcare and early disease detection, which is encouraging adoption of ophthalmic diagnostic tools including osmolarity testing. China is leading regional performance due to its large population base and continuous investment in healthcare infrastructure upgrades, while Japan is demonstrating high per-capita utilization supported by advanced medical systems and an aging population that requires specialized eye care. Strong clinical research environments in both countries are validating new technologies and accelerating physician confidence. India is also expanding rapidly because of rising middle-class income levels and insurance initiatives such as Ayushman Bharat that improve access to healthcare services. Thailand, Malaysia, and Singapore are benefiting from medical tourism growth, where hospitals are investing in advanced diagnostics to attract international patients seeking high-quality treatment.

Regional manufacturing ecosystems are improving affordability and supply availability by reducing production and distribution costs. Several countries are hosting device and consumable manufacturing facilities that leverage skilled labor and established supply chains to support local demand. Regulatory frameworks vary across the region, with Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) maintaining rigorous approval standards, while some Southeast Asian countries are implementing more streamlined processes to encourage technology adoption. Price sensitivity remains a constraint in many markets because reimbursement coverage is limited outside developed healthcare systems, which is increasing competition from lower-cost alternatives in primary care environments. Public-private partnerships are supporting infrastructure development and technology deployment, while localization strategies are reducing dependence on imported equipment.

Competitive Landscape

The global osmolarity testing device market structure is moderately consolidated, dominated by leading players such as TearLab Corporation, Johnson & Johnson Vision, ELITechGroup, SBM Sistemi, and I-Med Pharma Inc. These companies capture 35-40% of the market share in 2026. Established players dominate the tear osmolarity testing devices market with strong product lines and wide distribution networks. Brand strength builds customer loyalty effectively. Leaders allocate significant funds to research and development. They enhance device accuracy and usability to meet changing demands. Strategic partnerships strengthen positions steadily. Mergers and acquisitions expand portfolios efficiently.

Geographic outreach targets untapped regions actively. New entrants challenge incumbents, especially in portable units and consumables. These innovators introduce fresh designs that spur competition. Market dynamics accelerate technological advances across segments. Providers benefit from diverse options and falling prices. Decision-makers gain leverage through vendor negotiations. Long-term growth favors adaptable firms that balance innovation with reliability.

Key Industry Developments

- In October 2025, Advanced Instruments and Nova Biomedical unified under the Nova Biomedical brand following the completion of their merger, creating a combined life science tools platform with expanded analytical technologies, global reach, and research capabilities. The integration aims to accelerate innovation and enhance customer support across clinical diagnostics and biopharmaceutical markets while maintaining Advanced Instruments as a portfolio brand for osmolality testing solutions.

- In January 2025, Advanced Instruments launched the OsmoPRO® MAX automated osmometer to boost clinical lab productivity with freezing point depression technology and flow-through automation that eliminates manual pipetting and consumables. Key features include direct sampling from primary tubes, barcode scanning, continuous loading for walk-away operation, and integration with AdvancedQC for quality control, supporting up to 500 tests per system fluid fill.

Companies Covered in Osmolarity Testing Device Market

- TearLab Corporation

- Johnson & Johnson Vision

- Advanced Instruments Inc.

- ELITechGroup

- Precision Systems Science Co., Ltd.

- SBM Sistemi

- I-Med Pharma Inc.

- Gonotec GmbH

- KNAUER Wissenschaftliche Geräte GmbH

- Löser Messtechnik

- Arkray Inc.

- Beijing Precil Instruments Co., Ltd.

- Tianjin Tianhe Analytical Instrument Co., Ltd.

- Shenzhen Mindray Bio-Medical Electronics Co.,

Frequently Asked Questions

The global osmolarity testing device market is projected to reach US$ 107.0 million in 2026.

The market is driven by the rising dry eye disease prevalence and technological advances in portable diagnostics.

The market is poised to witness a CAGR of 4.0% from 2026 to 2033.

Emerging markets and expanded applications in refractive surgery and clinical trials are creating prime growth opportunities.

TearLab Corporation, Johnson & Johnson Vision, ELITechGroup, SBM Sistemi, and I-Med Pharma Inc. are some of the key players in the market.