- Biotechnology

- Oncolytic Virus Immunotherapy Market

Oncolytic Virus Immunotherapy Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Oncolytic Virus Immunotherapy Market by Virus Type (Adenovirus, Herpes Simplex Virus (HSV), Vaccinia Virus, Reovirus, Newcastle Disease Virus, Others), Route of Administration (Intratumoral, Intravenous, Others), Indication (Melanoma, Breast cancer, Lung cancer, Ovarian cancer, Prostate cancer, Others), End-user (Hospitals & oncology centers, Ambulatory surgical centers, Cancer research institutes, Others) , and Regional Analysis from 2025 - 2032

Oncolytic Virus Immunotherapy Market Share and Trends Analysis

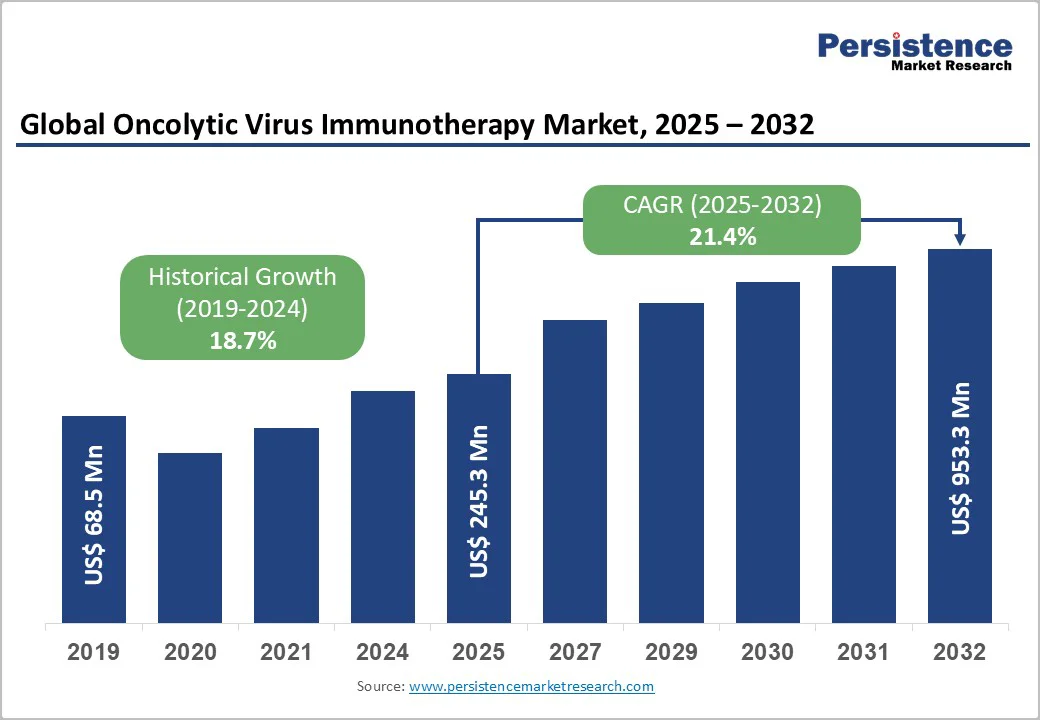

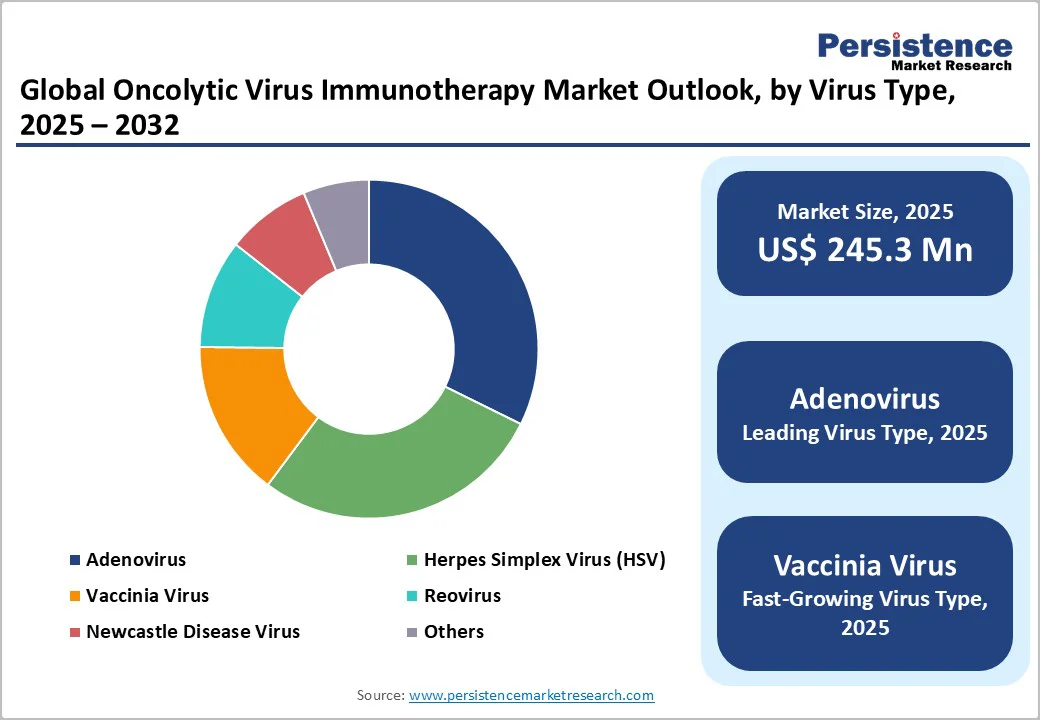

The global oncolytic virus immunotherapy market size is valued at US$245.3 million in 2025 and is projected to reach US$953.3 million, growing at a CAGR of 21.4% during the forecast period from 2025 to 2032.

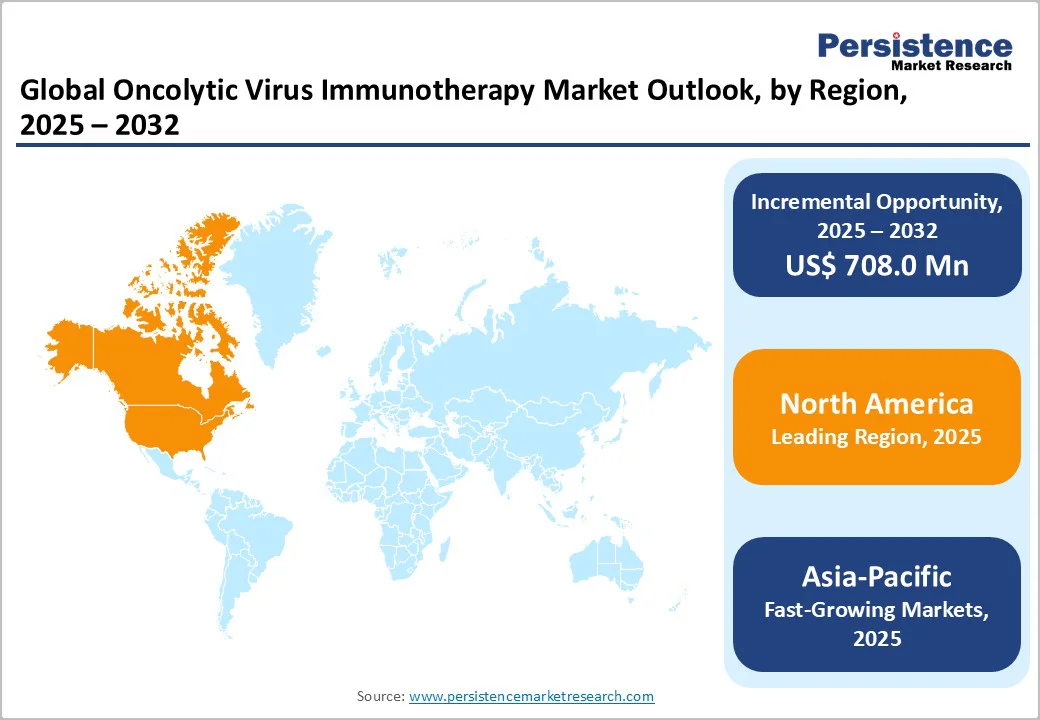

The global oncolytic virus immunotherapy market is expanding steadily, driven by advancements in cancer immunotherapy, rising clinical success of viral vectors, and increasing oncology R&D investments. North America leads due to strong regulatory approvals and established biopharma infrastructure, while Asia Pacific is the fastest-growing region, supported by government funding, clinical trial expansion, and rising cancer incidence.

Key Industry Highlights

- Dominant Virus Type: Adenovirus holds about 32.3% share of the Oncolytic Virus Immunotherapy Market, driven by its genetic flexibility, high tumor selectivity, and widespread use in clinical trials for solid tumors such as lung and colorectal cancers. Its ease of engineering and favorable safety profile further strengthen its market dominance.

- Dominant Route of Administration: Intratumoral delivery accounts for around 53.7% share, supported by precise targeting, reduced systemic toxicity, and enhanced local immune activation. This route remains preferred for accessible solid tumors and has shown superior response rates in ongoing trials.

- Dominant Region: North America, contributing roughly 43.1% of global revenue, leads the market due to robust clinical research networks, FDA-approved products like Amgen’s Imlygic, strong biotech funding, and established oncology care infrastructure.

- Investment Plans: Asia Pacific is the fastest-growing region, fueled by rising cancer prevalence, increasing government support for gene and cell therapies, clinical trial expansion, and partnerships between Western biotechs and regional pharmaceutical firms.

- Market Drivers: Advancements in immuno-oncology, growing adoption of viral-based cancer therapies, rising success in solid tumor indications, and favorable regulatory incentives such as Orphan Drug and RMAT designations.

- Market Opportunity: Development of next-generation engineered viruses with immune-modulating genes, expansion into combination therapies with checkpoint inhibitors, and increased investment in localized manufacturing and clinical capacity across emerging economies.

| Global Market Attributes | Key Insights |

|---|---|

|

Global Oncolytic Virus Immunotherapy Market Size (2025E) |

US$ 245.3 Mn |

|

Market Value Forecast (2032F) |

US$ 953.3 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

21.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

18.7% |

Market Dynamics

Driver – Growing Adoption of Combination Therapy Approaches

The growing adoption of combination therapy approaches is a key driver of the oncolytic virus immunotherapy market. For example, in a phase II study involving 198 patients with unresectable Stage IIIB–IV melanoma, the combination of the oncolytic virus Talimogene laherparepvec (T-VEC) plus the checkpoint inhibitor Ipilimumab produced an objective response rate (ORR) of 35.7%, compared to 16.0% for ipilimumab alone (OR 2.9; p = 0.003). A recent meta-analysis of 15 trials (903 patients) found that combining oncolytic viruses with immune checkpoint inhibitors or chemotherapy resulted in a pooled ORR of 32% (95% CI: 27-36 %). Such enhanced outcomes support broader clinical acceptance of oncolytic virus therapies in combination regimens, thereby increasing their market potential by expanding indications, improving response rates, and attracting investment.

Restraints – Variability in Clinical Response & Patient Selection Challenges

Variability in clinical response and challenges in patient selection act as significant restraints for the Oncolytic Virus Immunotherapy market. A meta-analysis covering 87 studies with 5,385 patients found an overall response rate (ORR) of only 29%, with complete responses in 11% and progressive disease in 32%. Another systematic review of 36 trials (~4,190 patients) showed that benefits of oncolytic therapy varied significantly and were heavily influenced by tumour-immune-microbiome factors. For instance, among melanoma patients, those with AXL-high tumours had an ORR of just 15%, versus 49% in MITF-high tumours. This heterogeneity means that many patients may not respond, making it difficult for clinicians and payers to predict benefit or justify cost. As a result, broad commercial uptake is limited, as the “who will respond” question remains unresolved.

Opportunity – Technological Advancements in Viral Engineering

The rapid advancements in viral engineering represent a major opportunity for the Oncolytic Virus Immunotherapy market. Engineered viruses now express immune-modulating genes, such as GM CSF or IL-12, to turn “cold” tumours into “hot” ones and enhance immune response. Clinical trial reviews report that, as of October 2021, there were 408 registered trials of 31 distinct oncolytic virus products, with 80 % in phase I/II stages—indicating the pipeline acceleration. Moreover, genomic edits in viral platforms are now tailored to specific cancers: for example, engineered viruses targeting non-small-cell lung cancer (with contextual anti-PD-1 therapy) are being developed. These technological enhancements expand applicability across tumour types, facilitate combination regimens, and create differentiated product portfolios, thus opening significant growth avenues for both developers and clinicians.

Category-wise Analysis

By Virus Type, Adenovirus Dominates the Oncolytic Virus Immunotherapy Market

Adenovirus dominates the market with 32.3% share in 2025, due to clear clinical-trial frequency and engineering advantages. Reviews show that approximately 31% of over 130 oncolytic virus clinical trials use adenovirus vectors, more than any other virus family. Adenoviruses are highly amenable to genetic engineering: they possess a well-characterised genome, allow high-titer production, and enable insertion of tumour-selective promoters or therapeutic transgenes without integrating into the host genome. These traits make them a preferred choice for platform development in cancer immunotherapy, which in turn drives their market leadership within the virus-type segmentation for the oncolytic virus immunotherapy market.

By Route of Administration, Intratumoral is gaining traction due to higher local efficacy and lower systemic toxicity

The predominance of intratumoral administration in the oncolytic virus immunotherapy market is driven by its targeted efficacy and reduced systemic toxicity. According to clinical data, among 2,740 patients evaluated across multiple trials, approximately 52% received intratumoral injections, compared to 28% who received intravenous delivery. Intratumoral delivery allows direct virus deposition into the tumor, enhancing viral replication and immune activation locally while minimizing systemic exposure. In a pooled analysis, intratumoral injections achieved an objective response rate of 34%, whereas systemic administration showed only 19% response. This concentration at the tumor site, combined with fewer off-target effects, explains why intratumoral injection remains the dominant route in oncolytic virus immunotherapy.

Regional Insights

North America Oncolytic Virus Immunotherapy Market Trends

North America dominates the oncolytic virus immunotherapy market with 43.1% share in 2025, due to its large cancer burden and strong research infrastructure. In the U.S., for example, around 1.85 million new invasive cancer cases were diagnosed in 2022 (and over 613,000 cancer-related deaths in 2023). At the same time, American research institutions and agencies such as the National Institutes of Health (NIH) have funded cancer research such that U.S. scientists lead the global publication output in oncolytic-virus research. These factors, large unmet need, robust funding, early regulatory approvals and clinical trial networks create a favorable environment for oncolytic virus therapies, solidifying North America’s leadership in development and commercialization.

Europe Oncolytic Virus Immunotherapy Market Trends

Europe stands out as an important region for the oncolytic virus immunotherapy market for several reasons. In 2022 the continent reported approximately 4.47 million new cancer cases (age-standardized rate of 280 per100,000) and nearly 2 million cancer deaths, reflecting a high and growing unmet need for novel therapies. The region’s cancer incidence is disproportionately large representing over 20% of global cases despite having less than 10% of the world’s population. Moreover, European health systems and research institutions are actively investing in oncology infrastructure, early-access programs and cross-country collaborations, making the region attractive for the development and commercialization of advanced therapies like oncolytic viruses.

Asia Pacific Oncolytic Virus Immunotherapy Market Trends

The Asia Pacific region is the fastest-growing market for oncolytic virus immunotherapy largely because of its rapidly increasing cancer burden and emerging infrastructure. For example, in Southern, Eastern and South-Eastern Asia alone, there were an estimated 9.2 million new cancer cases and 5.1 million cancer deaths in 2022, approximately half of the global totals. Furthermore, in the Western Pacific region, nearly 6.8 million new cases were recorded in 2022. The combination of large patient populations, rising incidence, increased healthcare investment, and growing clinical trial activity makes Asia Pacific a key opportunity zone for advanced therapies such as oncolytic virus immunotherapy.

Market Competitive Landscape

Leading companies in the oncolytic virus immunotherapy market focus on innovative viral platforms, clinical pipeline expansion, and global collaborations. They invest in advanced genetic engineering, combination therapy research, and strategic partnerships with hospitals and research institutes to enhance accessibility, improve patient outcomes, and expand adoption across diverse cancer indications worldwide.

Key Industry Developments:

- In October 2025, Replimune announced that the U.S. FDA accepted the resubmission of its Biologics License Application (BLA) for RP1, targeting the treatment of advanced melanoma. This milestone advances the company’s efforts to bring its oncolytic virus therapy to patients, signaling progress toward regulatory approval and potential commercial availability.

- In October 2025, A new IL–2–loaded oncolytic adenovirus engineering service was launched, enabling the development of genetically modified viruses that deliver interleukin-2 directly to tumors. The service aimed to enhance antitumor immune responses, improve therapy efficacy, and accelerate research and clinical applications in cancer immunotherapy.

- In February 2024, Researchers reported that combining oncolytic viruses with T-cell therapy enhanced cancer treatment outcomes. Clinical studies demonstrated that the dual approach improved tumor targeting, increased immune response, and elevated patient response rates compared to T-cell therapy alone, marking a significant advancement in immuno-oncology strategies.

Companies Covered in Oncolytic Virus Immunotherapy Market

- Amgen Inc.

- Creative Biolabs

- Daiichi Sankyo Company Limited

- Genelux Corporation

- Oncorus Inc.

- Replimune Inc.

- Siga Technologies

- Sorrento Therapeutics Inc.

- TILT Biotherapeutics

- Viralytics Ltd.

- Others

Frequently Asked Questions

The global oncolytic virus immunotherapy market is projected to be valued at US$ 245.3 Mn in 2025.

Rising cancer prevalence, advancements in viral engineering, combination therapy adoption, supportive regulations, and increasing healthcare awareness drive market growth.

The global oncolytic virus immunotherapy market is poised to witness a CAGR of 21.4% between 2025 and 2032.

Expanding cancer indications, combination therapies, engineered viral platforms, emerging Asia‑Pacific markets, and strategic collaborations present key opportunities for market growth.

Amgen Inc., Creative Biolabs, Daiichi Sankyo Company Limited, Genelux Corporation, Oncorus Inc., Replimune Inc.