- Nutraceuticals & Functional Foods

- Non-GMO Food Market

Non-GMO Food Market Size, Share, and Growth Forecast 2026 - 2033

Non-GMO Food Market by Product Type (Beverage, Food), Distribution Channel (Supermarkets/ Hypermarkets, Convenience Stores, Online Retail Stores, Others), and Regional Analysis, 2026 - 2033

Non-GMO Food Market Size and Trend Analysis

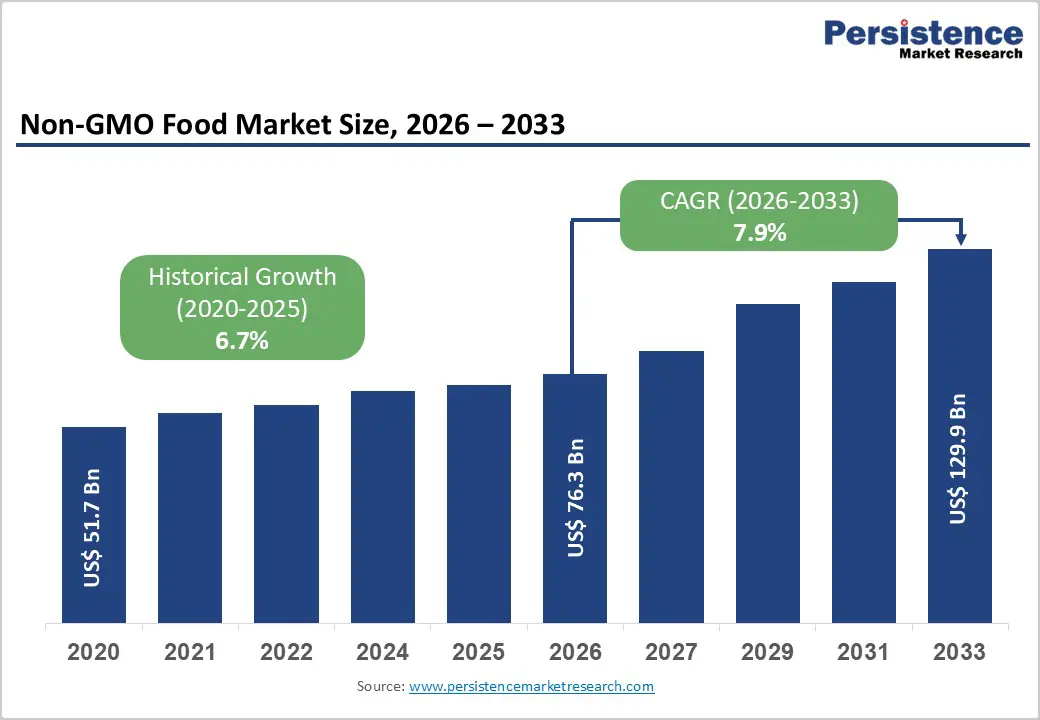

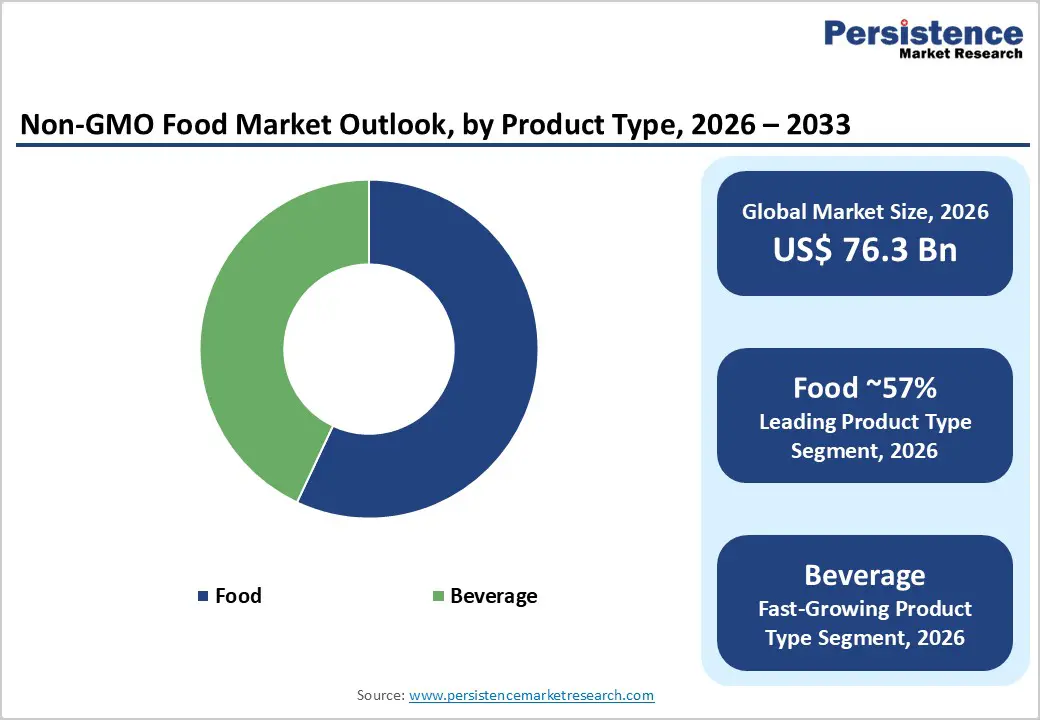

The global Non-GMO Food market size is expected to be valued at US$ 76.3 billion in 2026 and projected to reach US$ 129.9 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033. Sustained consumer demand for clean-label and transparently sourced food products. Increasing health awareness and concern about genetically modified ingredients are encouraging consumers to prefer verified non-GMO options across food and beverage categories.

The expansion of certification programs, such as the Non-GMO Project Verified label, which now covers tens of thousands of products globally, is further strengthening market credibility and adoption. In addition, mandatory GMO labeling regulations in major regions, including the U.S. and the European Union, are improving product transparency and influencing purchasing behavior. Together, these factors are accelerating the shift toward non-GMO offerings, prompting food manufacturers to expand their portfolios and invest in cleaner, more natural ingredient sourcing strategies across global markets.

Key Industry Highlights

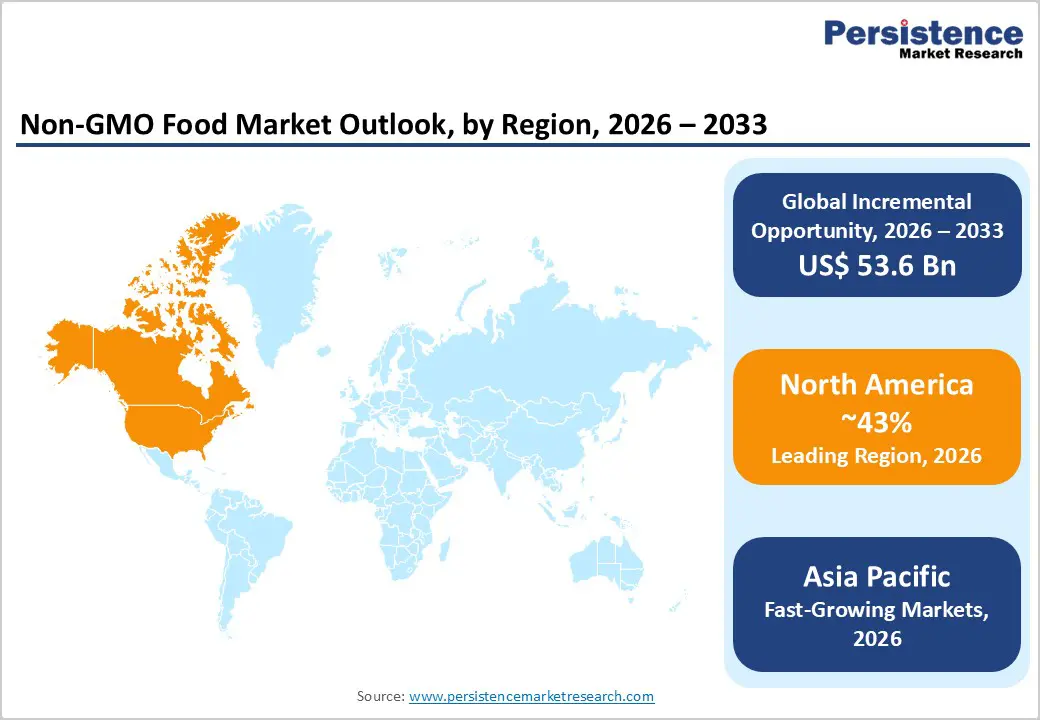

- Leading Region: North America holds ~43% of the global non-GMO food market share in 2025, driven by the maturity of the Non-GMO Project Verified certification ecosystem, mandatory NBFDS labeling, and strong consumer clean-label demand.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, fueled by rising urban middle-class health awareness, progressive GMO labeling regulation in Japan and South Korea, and the rapid expansion of e-commerce grocery channels in India and China.

- Dominant Food Segment: The food segment leads with ~57% of the global non-GMO market in 2025, driven by broad product coverage across packaged foods, grains, dairy alternatives, and snacks with mature non-GMO certification penetration.

- Fast-Growing Food Segment: The beverage segment is the fastest-growing product category, propelled by surging consumer demand for plant-based milks, functional drinks, and clean-label RTD beverages with non-GMO verification among millennial and Gen Z consumers.

- Opportunity: The rapid growth of online retail channels and direct-to-consumer e-commerce platforms enables non-GMO brands to reach and convert health-conscious niche audiences at scale, while enabling superior certification storytelling and subscription-based repeat purchase models.

Market Dynamics

Drivers - Expanding Consumer Awareness and Clean-Label Demand

Heightened consumer focus on food safety, ingredient transparency, and long-term health outcomes is structurally expanding the non-GMO food category across both developed and emerging markets. According to the International Food Information Council (IFIC) Foundation's 2023 Food and Health Survey, over 62% of U.S. consumers actively read ingredient labels, with "non-GMO" ranking among the top purchase-influencing claims alongside "organic."

The non-GMO Project, the leading third-party verification body in North America, reports annual retail sales of verified products exceeding US$ 26 billion in the U.S. alone. This consumer-driven pull compels mainstream food manufacturers and private-label retailers to expand their non-GMO portfolios, broadening distribution and accelerating shelf space capture across supermarkets, natural grocery formats, and e-commerce channels.

Restraints - Premium Pricing and Affordability Barriers in Price-Sensitive Markets

The cost premium associated with non-GMO certified products, driven by higher input costs, rigorous supply chain segregation requirements, and third-party verification expenses, creates a significant affordability barrier that suppresses adoption among lower- and middle-income consumer segments globally.

Research published in the American Journal of Agricultural Economics indicates that non-GMO labeled products command price premiums of 20–30% over conventional equivalents in key categories such as packaged grains, cooking oils, and dairy. This premium constrains penetration depth in high-growth but price-sensitive markets across Southeast Asia, Latin America, and Africa, limiting the addressable base for premium non-GMO positioning.

Opportunities - Surging Demand for Non-GMO Beverages in Health and Wellness Channels

The non-GMO beverage segment represents the fastest-growing product category within the market, presenting a concentrated opportunity for brands positioned at the intersection of clean-label credentials and functional health benefits. Consumer interest in non-GMO juices, plant-based milks, kombucha, and herbal teas is expanding rapidly, particularly among millennials and Gen Z demographics that prioritize ingredient transparency in every consumption occasion. According to the Plant Based Foods Association (PBFA), U.S. retail sales of plant-based beverages exceeded US$ 3 billion in 2023, with a significant share carrying non-GMO verification. The growing footprint of health and wellness specialty retail exemplified by chains like Whole Foods Market and Sprouts Farmers Market and the explosive growth of direct-to-consumer e-commerce channels provide brand builders with scalable pathways to reach health-conscious buyers willing to pay a premium for non-GMO certified beverages.

Category-wise Insights

Product Type Analysis

Based on product type, the market is bifurcated into beverage and food. Among these, the food segment is predicted to dominate by generating a share of around 57% in 2026. Increasing consumer concerns over crop-based additives and processed ingredients used in packaged food items are estimated to spur segment growth. Staples, including canola, soy, and corn, are generally modified in Argentina, Brazil, and the U.S. These are extensively used in frozen items, baked goods, snacks, and breakfast cereals. It has resulted in a rising shift of consumers toward non-GMO certification in food items, as these usually contain fewer modified ingredients.

Beverages, on the other hand, are poised to showcase a decent CAGR through 2033 due to the emergence of functional and plant-based drink segments. These heavily rely on crops such as pea protein, which are often genetically modified in traditional agriculture. Consumers today have become highly conscious of their food ingredients, and hence, the preference for clean-label beverages void of GMOs is increasing. Brands such as Califia Farms and Ripple Foods have already positioned their products as non-GMO, catering to non-GMO and vegan consumers.

Distribution Channel Insights

In terms of distribution channel, the market is trifurcated into supermarkets/hypermarkets, convenience stores, and online retail stores. Out of these, supermarkets/hypermarkets are expected to remain at the forefront with nearly 34% of the non-GMO food market share in 2026. It is attributed to their ability to provide high visibility and wide shelf space for certified clean-label products. This makes them a highly preferred choice for both brands and consumers. The availability of affordable family-sized and bulk packaging of non-GMO products, which are preferred by large households, is also likely to drive the segment.

Online retail stores are speculated to witness considerable growth in the foreseeable future. This is due to targeted consumer segments, wide product selection, and high convenience. E-commerce platforms such as iHerb, Thrive Market, and Amazon offer extensive categories for non-GMO items. In addition, consumers have the chance to read several product reviews and compare prices from different platforms before buying the product. With detailed product descriptions, ratings from previous buyers, and clear ingredient lists, consumers often feel more confident about their purchases.

Regional Insights

North America Non-GMO Food Market Trends and Insights

North America leads the global non-GMO food market with ~43% of global share in 2025, underpinned by a highly developed clean-label retail ecosystem, robust Non-GMO Project Verified certification infrastructure, and strong consumer activism around food transparency. The USDA's NBFDS mandate continues to heighten consumer GMO-awareness, driving brand differentiation through verified non-GMO positioning. The region is expected to sustain premium segment growth through 2033 as retailers expand natural product sections.

U.S. Non-GMO Food Market Size

The U.S. accounts for ~80% of North American non-GMO food market revenue, backed by the largest installed base of Non-GMO Project Verified products globally, exceeding 60,000 SKUs. Consumer spending on natural and organic food channels reached US$ 67 billion in 2023, per SPINS data. The U.S. market trajectory remains strongly upward, driven by mass-market retail expansion and growing millennial household formation.

Europe Non-GMO Food Market Trends and Insights

Europe represents the second-largest non-GMO food market, holding ~27% of global share, driven by the EU's long-standing stringent GMO regulation under Regulation and strong cultural preference for natural, minimally processed food. The European Green Deal's Farm to Fork Strategy targets are further reinforcing a policy environment favorable to clean-label food production. Premium non-GMO categories, including organic bread, dairy, and beverages, are gaining mainstream retail traction across the region.

Germany Non-GMO Food Market Size

Germany is Europe's largest non-GMO food market, contributing an estimated 19–21% of regional revenue. The German Bioökonomierat (German Bioeconomy Council) supports sustainable, non-GMO agricultural practices nationally. High organic and natural food retail density, with Alnatura and dm-drogerie markt serving as key distribution anchors, sustains premium demand. Germany's trajectory points toward continued leadership through growing retailer private-label non-GMO lines.

U.K. Non-GMO Food Market Size

The United Kingdom represents ~14–16% of the European non-GMO food market, with sustained demand anchored by a health-conscious consumer base and strong retailer commitment to clean-label product ranges. Tesco and Sainsbury's have expanded non-GMO and free-from assortments significantly since 2020. Post-Brexit regulatory divergence adds a layer of policy uncertainty, but domestic consumer preference for non-GMO products remains structurally robust.

Asia Pacific Non-GMO Food Market Trends and Insights

Asia Pacific is the fastest-growing regional non-GMO food market through 2033, propelled by rising health awareness among urban middle-class consumers, expanding regulatory scrutiny of bioengineered foods in Japan, South Korea, and Australia, and surging e-commerce channels enabling non-GMO product discovery. China represents significant latent demand; shifting domestic consumer sentiment toward food safety following multiple food safety controversies is accelerating premium imported non-GMO product adoption in urban centers such as Shanghai and Beijing.

India Non-GMO Food Market Size

India represents ~12–15% of the Asia Pacific non-GMO food market, with demand driven by a traditional cultural affinity for natural food ingredients and growing urban consumer awareness of GMO risks. India's Food Safety and Standards Authority (FSSAI) is progressively strengthening GMO food labeling norms. Rising disposable incomes in metro cities and the rapid expansion of organized retail are creating strong structural conditions for non-GMO product penetration through 2033.

Japan Non-GMO Food Market Size

Japan accounts for ~18–20% of the Asia Pacific non-GMO food market, reflecting one of the highest per-capita consumer premiums paid for clean-label food globally. The Consumer Affairs Agency (CAA) of Japan enforces mandatory GMO labeling for 33 food categories, driving active non-GMO product segmentation. Japan's aging but affluent consumer base, combined with strong preference for domestic non-GMO agricultural produce, supports continued premium pricing and category depth expansion.

Competitive Landscape

The global non-GMO food market is moderately fragmented, with a mix of large multinational corporations and mission-driven specialty brands competing across price tiers and distribution channels. Leading players including Nestlé S.A., Danone SA, and The Hain Celestial Group leverage certification portfolios and R&D investment to reinforce clean-label credentials.

Key competitive differentiators include third-party verification (notably Non-GMO Project and USDA Organic), supply chain traceability capabilities, and digital marketing effectiveness. Emerging business model trends include direct-to-consumer e-commerce, subscription food boxes, and co-branded organic-plus-non-GMO product lines that command higher price points and foster repeat purchase loyalty among health-conscious consumer cohorts.

Key Developments

- In April 2025, Jans Enterprises Corp. unveiled Jans Sparkling Prebiotic Drinks in the U.S. These newly launched beverages are lightly carbonated and contain clean ingredients as well as low sugar. These non-GMO beverages were made available in four refreshing, fruity flavors.

- In February 2025, CIRANDA, a premium supplier of certified organic, non-GMO food ingredients, launched its e-commerce website. It aims to provide consumers with a wide range of products on a single platform, including documentation, ordering, ingredient information, and other account management functionalities.

- In December 2024, LT Foods Ltd. introduced a non-GMO certified global gourmet food, DAAWAT Jasmine Thai Rice for consumers in India. It includes the authentic Thai Hom Mali, which is directly sourced from Thailand. This launch helped the company to extend its gourmet food portfolio in India.

Non-GMO Food Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 51.7 billion |

|

Current Market Value (2026) |

US$ 76.3 billion |

|

Projected Market Value (2033) |

US$ 129.9 billion |

|

CAGR (2026–2033) |

7.9% |

|

Leading Region |

North America, ~43% market share (2025) |

|

Dominant Product Type |

Food, ~57% market share (2025) |

|

Top-Ranking Distribution Channel |

Supermarkets/Hypermarkets, ~48% market share (2025) |

|

Incremental Opportunity |

US$ 53.6 billion |

Companies Covered in Non-GMO Food Market

- Amy's Kitchen, Inc.

- Organic Valley

- Blue Diamond Growers

- The Hain Celestial Group, Inc.

- The Kellogg's Company

- Nestle S.A.

- PepsiCo Inc.

- Pernod Ricard

- Clif Bar & Company

- Danone SA

- Others

Frequently Asked Questions

The global non-GMO food market is valued at US$ 76.3 billion in 2026.

Increasing requirement for transparency in food ingredients and rising shift of consumers toward veganism are major drivers.

North America leads the global Non-GMO Food market with ~43% of global market share in 2025.

Surging investment by leading players in online distribution channels and the launch of family packs for large households are the key market opportunities.

The leading companies in the global market include Nestlé S.A., Danone SA, PepsiCo Inc., The Hain Celestial Group, Inc., Amy's Kitchen, Inc., and Blue Diamond Growers, among others.