- Pharmaceuticals

- Neuroendocrine Carcinoma Treatment Market

Neuroendocrine Carcinoma Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Neuroendocrine Carcinoma Treatment Market by Indication Type (Gastroenteropancreatic Neuroendocrine Tumors (GEP-NETs), Others), Drug Class (Somatostatin Analogs, Others), End-user, and Regional Analysis for 2026 – 2033

Neuroendocrine Carcinoma Treatment Market Size and Trends Analysis

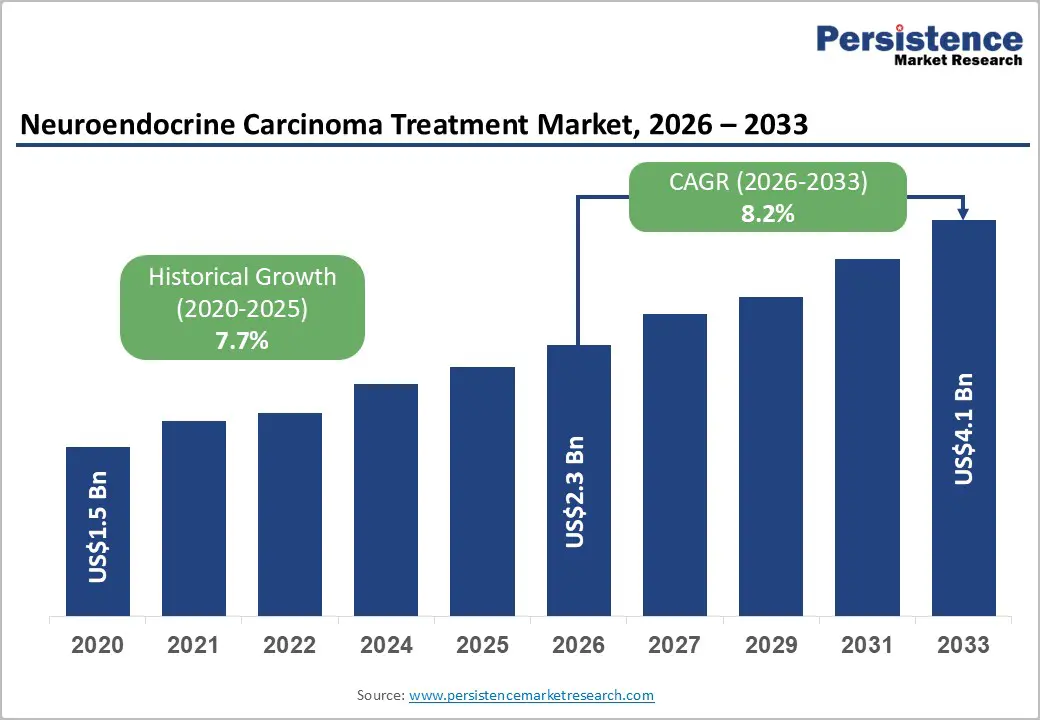

The global neuroendocrine carcinoma treatment market size is likely to be valued at US$2.3 billion in 2026, and is expected to reach US$4.1 billion by 2033, growing at a CAGR of 8.2% during the forecast period from 2026 to 2033, driven by the increasing prevalence of neuroendocrine tumors (NETs), rising diagnosis rates due to improved imaging and biomarker testing, growing adoption of targeted therapies and peptide receptor radionuclide therapy (PRRT), and expanding access to specialized oncology centers. Increasing recognition of neuroendocrine carcinoma treatment as critical for long-term disease control, symptom management, and survival improvement in emerging rare cancer and precision oncology markets remains a major driver of market growth.

Key Industry Highlights:

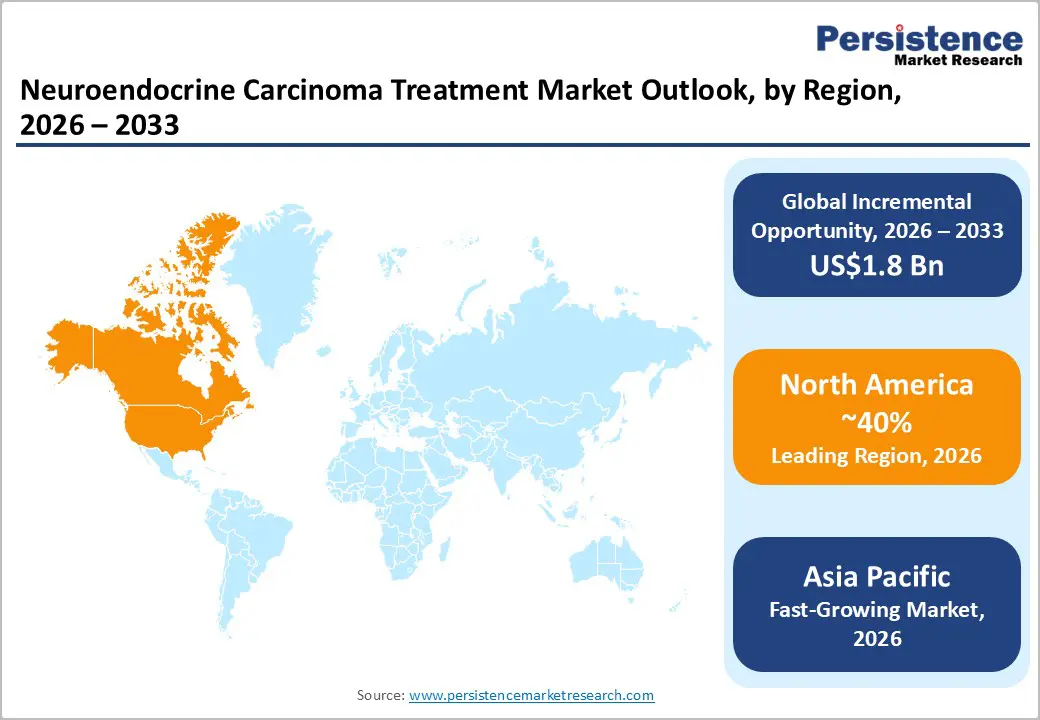

- Leading Region: North America, anticipated to account for a 40% market share in 2026, driven by high NET incidence reporting, advanced PRRT availability, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising NET awareness, increasing oncology infrastructure investment, and growing targeted therapy access in China and India.

- Dominant Indication Type: Gastroenteropancreatic neuroendocrine tumors (GEP-NETs), to hold approximately 55% of the market share, as it remains the most frequently diagnosed subtype.

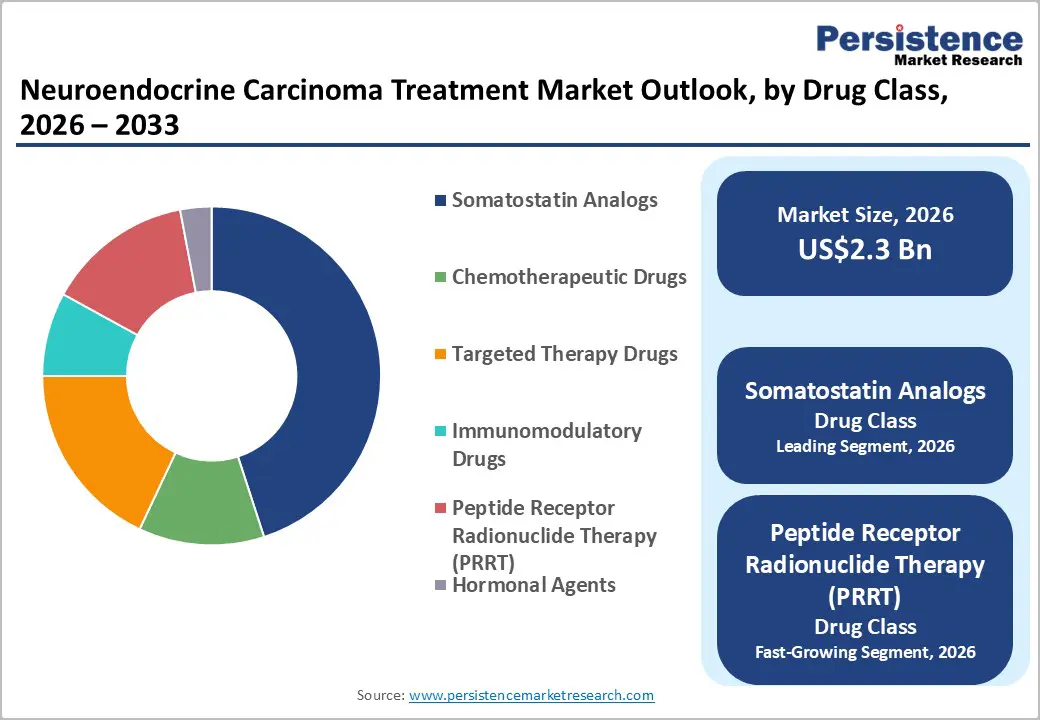

- Leading Drug Class: Somatostatin analogs, contributing nearly 45% of the market revenue, due to their first-line standard of care status.

- October 2025, Lantheus Holdings announced the FDA set a PDUFA date for LNTH-2501, a PET imaging kit for detecting somatostatin receptor–positive neuroendocrine tumors in adults and children.

| Key Insights | Details |

|---|---|

| Neuroendocrine Carcinoma Treatment Market Size (2026E) | US$2.3 Bn |

| Market Value Forecast (2033F) | US$4.1 Bn |

| Projected Growth CAGR (2026-2033) | 8.2% |

| Historical Market Growth (2020-2025) | 7.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising NET Incidence and Targeted Therapy Adoption

The growing burden of neuroendocrine tumors (NETs) is becoming a significant driver of innovation and treatment demand worldwide. Improved diagnostic imaging, biomarker testing, and heightened clinical awareness have led to earlier and more frequent detection of NETs, including previously underdiagnosed gastrointestinal and pancreatic forms. Lifestyle changes, aging populations, and better cancer registries have also contributed to the apparent rise in incidence. Healthcare systems are witnessing an expanding patient pool requiring long-term and specialized therapeutic management.

The shift toward precision medicine has accelerated the adoption of targeted therapies for NET treatment. Unlike conventional chemotherapy, targeted agents act on specific molecular pathways involved in tumor growth and angiogenesis, offering improved progression control and a more favorable safety profile. Therapies such as somatostatin analogs, mTOR inhibitors, and peptide receptor radionuclide therapy (PRRT) are increasingly integrated into treatment guidelines due to their clinical efficacy and ability to enhance quality of life. The availability of oral formulations and personalized treatment sequencing further supports adherence and long-term disease management.

Expanding PRRT and Combination Regimens

Peptide receptor radionuclide therapy (PRRT) is gaining strong clinical momentum as treatment strategies for neuroendocrine tumors continue to evolve. This approach delivers targeted radiation directly to tumor cells by binding radioactive isotopes to somatostatin analogs, which attach to receptors highly expressed on many NET cells. By concentrating radiation at the tumor site while sparing surrounding healthy tissue, PRRT offers improved disease control with a manageable safety profile. Its use has expanded beyond late-line settings and is increasingly considered earlier in the treatment pathway for selected patients with progressive or metastatic disease.

Combination regimens are emerging as a promising strategy to enhance therapeutic outcomes. Clinicians are exploring PRRT alongside radio-sensitizing chemotherapy, targeted agents such as mTOR inhibitors, or immunotherapy to improve tumor response and delay resistance. Combining modalities may help address tumor heterogeneity and overcome mechanisms that limit single-agent effectiveness. Additionally, sequential treatment approaches where PRRT is integrated within a broader personalized care plan are being optimized to extend progression-free survival.

Barrier Analysis – High Treatment Costs and Limited Reimbursement

The management of neuroendocrine tumors often involves advanced diagnostics, long-term pharmacotherapy, targeted agents, and specialized procedures such as peptide receptor radionuclide therapy, all of which contribute to substantial overall treatment costs. Many targeted therapies and biologics are priced at a premium due to complex development processes and limited patient populations. In addition, patients typically require prolonged treatment durations and continuous monitoring through imaging and laboratory testing, further increasing financial burden on both individuals and healthcare systems.

Limited or inconsistent reimbursement policies create additional barriers to access. Coverage criteria may restrict the use of newer therapies to specific disease stages or require failure of conventional treatments first, delaying optimal care. In some regions, public health systems face budget constraints that limit funding for high-cost oncology drugs. Out-of-pocket expenses can therefore be significant, particularly in countries without comprehensive insurance coverage.

Late Diagnosis and Disease Heterogeneity

Neuroendocrine tumors are frequently diagnosed at an advanced stage because early symptoms are often vague, intermittent, or mistaken for common gastrointestinal or respiratory conditions. Many tumors grow slowly and remain clinically silent for years, delaying detection until metastasis has occurred. Limited awareness among patients and primary care providers, along with restricted access to specialized imaging and biomarker testing in certain regions, further contributes to delayed diagnosis. Treatment options may become more complex and prognosis less favorable by the time the disease is confirmed.

Disease heterogeneity adds another layer of clinical challenge. Neuroendocrine tumors vary widely in terms of origin, grade, molecular profile, hormone secretion, and growth rate. Even tumors arising from the same organ can behave differently and respond variably to therapy. This diversity complicates standardized treatment planning and requires individualized therapeutic strategies.

Opportunity Analysis – Growth in Next-Generation PRRT and Biomarker-Driven Therapies

Advancements in molecular oncology are accelerating the development of next-generation peptide receptor radionuclide therapy (PRRT) and biomarker-driven treatment strategies for neuroendocrine tumors. Newer PRRT approaches focus on optimizing radionuclides, improving tumor targeting, and enhancing safety profiles. Innovations include the use of alternative radioactive isotopes with higher energy or shorter tissue penetration ranges, as well as modified somatostatin analogs designed to increase receptor binding affinity. These refinements aim to deliver more potent and precise radiation doses to tumor cells while minimizing damage to surrounding healthy tissues. Research is also exploring repeat dosing strategies and personalized activity adjustments to maximize therapeutic benefit.

Biomarker-driven therapies are reshaping treatment selection and sequencing. Molecular imaging techniques and circulating biomarkers help identify patients most likely to respond to specific targeted agents or PRRT. Genetic profiling and receptor expression analysis allow clinicians to tailor therapies based on tumor biology rather than relying solely on anatomical classification. This precision-based approach improves response rates, reduces unnecessary toxicity, and supports more efficient resource utilization.

Developments in Orphan Drug Designation

Regulatory incentives for rare diseases have significantly influenced the development landscape for treatments targeting conditions with small patient populations, including certain neuroendocrine tumors. Orphan drug designation provides benefits such as market exclusivity for a defined period, fee reductions, tax credits for clinical research, and regulatory support during development. These incentives help offset the high costs and commercial risks associated with developing therapies for limited populations, encouraging both emerging biotech firms and large pharmaceutical companies to invest in rare disease innovation.

Recent developments show a growing number of targeted therapies, biologics, and radiopharmaceuticals receiving orphan status earlier in their clinical development pathways. This early recognition facilitates streamlined regulatory interactions and may allow for accelerated approval processes based on strong surrogate endpoints. Additionally, collaborative research models involving academic institutions, patient advocacy groups, and industry stakeholders are strengthening clinical trial recruitment and data generation in rare disease settings. Advances in molecular diagnostics are also enabling more precise identification of eligible patient subgroups, further supporting orphan drug applications.

Category-wise Analysis

Indication Type Insights

Gastroenteropancreatic neuroendocrine tumors (GEP-NETs) are anticipated to dominate the market, accounting for approximately 55% of the market share in 2026, primarily due to their relatively higher incidence compared to other neuroendocrine tumor subtypes. These tumors originate in the gastrointestinal tract and pancreas, where improved diagnostic imaging, endoscopic procedures, and biomarker testing have enhanced detection rates. A broad range of approved treatment options, including somatostatin analogs, targeted therapies, and peptide receptor radionuclide therapy (PRRT), further supports market dominance. Gastroenteropancreatic neuroendocrine tumors (GEP-NETs) dominate the treatment focus is Advanced Accelerator Applications’ LUTATHERA (lutetium Lu 177 dotatate), which is specifically approved in the U.S. and Europe for treating somatostatin receptor-positive GEP-NETs.

Pulmonary neuroendocrine tumors are likely to be the fastest-growing indication type, driven by rising detection rates and expanding therapeutic options. Improved imaging technologies, including high-resolution CT scans and functional imaging, have increased the identification of lung-based neuroendocrine tumors at earlier stages. Growing clinical awareness and more precise pathological classification have also contributed to better diagnosis. In addition, treatment advancements such as targeted therapies, immunotherapy exploration, and peptide receptor radionuclide therapy (PRRT) for receptor-positive cases are broadening management possibilities. Novartis AG’s oral mTOR inhibitor Afinitor® (everolimus), which received approval from the U.S. Food and Drug Administration (FDA) for the treatment of progressive, nonfunctional lung neuroendocrine tumors in addition to gastrointestinal NETs.

Drug Class Insights

Somatostatin analogs are expected to dominate the market, contributing nearly 45% of revenue in 2026 and propelled by their established role as first-line therapy for many well-differentiated neuroendocrine tumors. These agents effectively control hormone-related symptoms such as flushing and diarrhea while also slowing tumor progression in receptor-positive patients. Their long-acting injectable formulations improve treatment adherence and convenience, supporting sustained use in chronic disease management. Ipsen’s Somatuline Depot (lanreotide) is a long-acting somatostatin analog approved by the U.S. Food and Drug Administration for the treatment of unresectable, well- or moderately differentiated, locally advanced or metastatic gastroenteropancreatic neuroendocrine tumors (GEP-NETs), where it has demonstrated significant improvement in progression-free survival.

Peptide receptor radionuclide therapy (PRRT) represents the fastest-growing drug class, with its targeted mechanism and strong clinical outcomes in receptor-positive patients. By delivering radioactive isotopes directly to tumor cells via somatostatin receptor binding, PRRT enables precise tumor irradiation while minimizing systemic toxicity. Its effectiveness in managing progressive or metastatic disease has expanded its use beyond late-line therapy. Advanced Accelerator Applications’ Lutathera® (lutetium Lu 177 dotatate), the first FDA- and EMA-approved peptide receptor radionuclide therapy (PRRT) for somatostatin receptor-positive gastroenteropancreatic neuroendocrine tumors. Lutathera combines a radioactive isotope with a targeting peptide to deliver radiation directly to NET cells, significantly improving progression-free survival in treated patients and expanding PRRT’s clinical use in NETs.

Regional Insights

North America Neuroendocrine Carcinoma Treatment Market Trends

North America is projected to dominate, accounting for nearly 40% of the share in 2026, driven by the region’s higher NET diagnosis and reporting rates, advanced PRRT centers, and high public awareness of rare tumor benefits. Distribution systems in the U.S. and Canada provide extensive support for neuroendocrine carcinoma treatment programs, ensuring wide accessibility across somatostatin analogs, GEP-NETs, and hospital populations. Increasing demand for targeted, convenient, and easy-to-administer forms is further accelerating adoption, as these formats improve survival outcomes in patients diagnosed at later stages.

Innovation in neuroendocrine carcinoma treatment technology, including stable next-generation PRRT, improved combination delivery, and targeted biomarker enhancement, is attracting significant investment from both public and private sectors. Government initiatives and NCI campaigns continue to promote use against progression risks, quality-of-life concerns, and emerging rare-cancer threats, creating sustained market demand. The growing focus on pulmonary grades and specialty uses, particularly for GEP-NETs and others, is expanding the target applications for neuroendocrine carcinoma treatment.

Europe Neuroendocrine Carcinoma Treatment Market Trends

Europe growth is supported by increasing awareness of NET treatment benefits, strong regulatory systems, and government-led rare-disease programs. Countries such as Germany, France, the U.K., and Italy have well-established oncology frameworks that support routine neuroendocrine carcinoma treatment use and encourage adoption of innovative PRRT and targeted delivery methods. These high-efficacy formulations are particularly appealing for GEP-NET populations, regulatory-conscious centers, and hospital users, improving progression-free survival and coverage rates.

Technological advancements in neuroendocrine carcinoma treatment development, such as enhanced somatostatin analogs, application-targeted delivery, and improved PRRT isotopes, are further boosting market potential. European authorities are increasingly supporting research and trials for therapies against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, long-acting options is aligned with the region’s focus on preventive symptom burden and quality-of-life improvement. Public awareness campaigns and promotion drives are expanding reach in both hospitals and cancer treatment centers, while suppliers are investing in combination regimens and novel variants to increase efficacy.

Asia Pacific Neuroendocrine Carcinoma Treatment Market Trends

Asia Pacific is likely to be the fastest-growing market for neuroendocrine carcinoma treatment in 2026, driven by rising NET incidence, increasing government initiatives, and expanding treatment programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting treatment campaigns to address rare-tumor growth and emerging oncology needs. Neuroendocrine carcinoma treatments are particularly attractive in these regions due to their scalable treatment delivery, ease of adoption, and suitability for large-scale hospital and GEP-NETs drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-administer neuroendocrine carcinoma treatments, which can withstand challenging patient profiles and minimize disease progression. These innovations are critical for reaching domestic centers and improving overall rare-cancer coverage. Growing demand for somatostatin analogs, GEP-NETs, and hospital applications is contributing to market expansion. Public-private partnerships, increased oncology expenditure, and rising investment in NET research and treatment capacity are further accelerating growth. The convenience of treatment delivery, combined with improved control and reduced risk of complications, positions it as a preferred choice.

Competitive Landscape

The global neuroendocrine carcinoma treatment market is characterized by dynamic competition between established oncology leaders and specialized radiopharmaceutical innovators. In North America and Europe, Novartis AG and Advanced Accelerator Applications maintain strong positions supported by extensive research capabilities, established neuroendocrine tumor (NET) treatment networks, and long-standing relationships with oncology centers. Their portfolios include advanced peptide receptor radionuclide therapy (PRRT) platforms and long-acting somatostatin analog formulations, which address both tumor control and symptom management.

In the Asia Pacific region, regional pharmaceutical manufacturers are increasingly introducing cost-competitive therapies, improving treatment accessibility across emerging healthcare systems. Long-acting somatostatin analog delivery systems enhance patient adherence, reduce hormone-related complications, and lower progression risks, supporting broader adoption. Meanwhile, strategic collaborations, licensing agreements, and acquisitions enable companies to combine radioligand expertise with oncology commercialization strength.

Key Industry Developments:

- In July 2025, the European Commission (EC) approved cabozantinib (Cabometyx) for the treatment of adult patients with unresectable or metastatic, well-differentiated pancreatic (pNET) and extrapancreatic (epNET) neuroendocrine tumors (NETs) who had experienced disease progression following at least one prior systemic therapy other than somatostatin analogues. The approval expanded treatment options for patients with advanced NETs and provided a new targeted therapy alternative in the post-first-line setting.

- In March 2025, ITM Isotope Technologies Munich SE presented positive topline Phase 3 COMPETE trial results in Grade 1 and 2 SSTR-positive GEP-NET patients. The company reported that n.c.a. 177Lu-edotreotide (ITM-11) met the primary endpoint and significantly improved progression-free survival compared with everolimus.

Companies Covered in Neuroendocrine Carcinoma Treatment Market

- Pfizer Inc.

- Novartis AG

- Chiasma Inc.

- Hutchison China MediTech Ltd

- AbbVie Inc.

- Bausch Health

- Jubilant Life Sciences Ltd.

- Teva Pharmaceutical Industries Ltd.

- F. Hoffmann-La Roche Ltd

- Mateon Therapeutics, Inc.

Frequently Asked Questions

The global neuroendocrine carcinoma treatment market is projected to reach US$2.3 billion in 2026.

Rising NET incidence and targeted therapy adoption are key drivers.

The neuroendocrine carcinoma treatment market is poised to witness a CAGR of 8.2% from 2026 to 2033.

Next-generation PRRT and biomarker-driven therapies and expansion in Asia Pacific and orphan drug designation are key opportunities.

Novartis AG, Pfizer Inc., Advanced Accelerator Applications, F. Hoffmann-La Roche Ltd, and AbbVie Inc. are the key players.