- Medical Devices

- Nebulizers, Inhalers, and Respirators for Asthma Treatment Market

Nebulizers, Inhalers, and Respirators for Asthma Treatment Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Nebulizers, Inhalers, and Respirators for Asthma Treatment Market by Device Type (Nebulizers, Inhalers, Respirators), Functionality (Single-Dose Delivery, Multi-Dose Delivery, Continuous-Flow Devices), Technology (Electrostatic Devices, Smart Inhalers, Traditional Manual Inhalers), Application and Regional Analysis for 2025 - 2032

Nebulizers, Inhalers and Respirators for Asthma Treatment Market Size and Trends Analysis

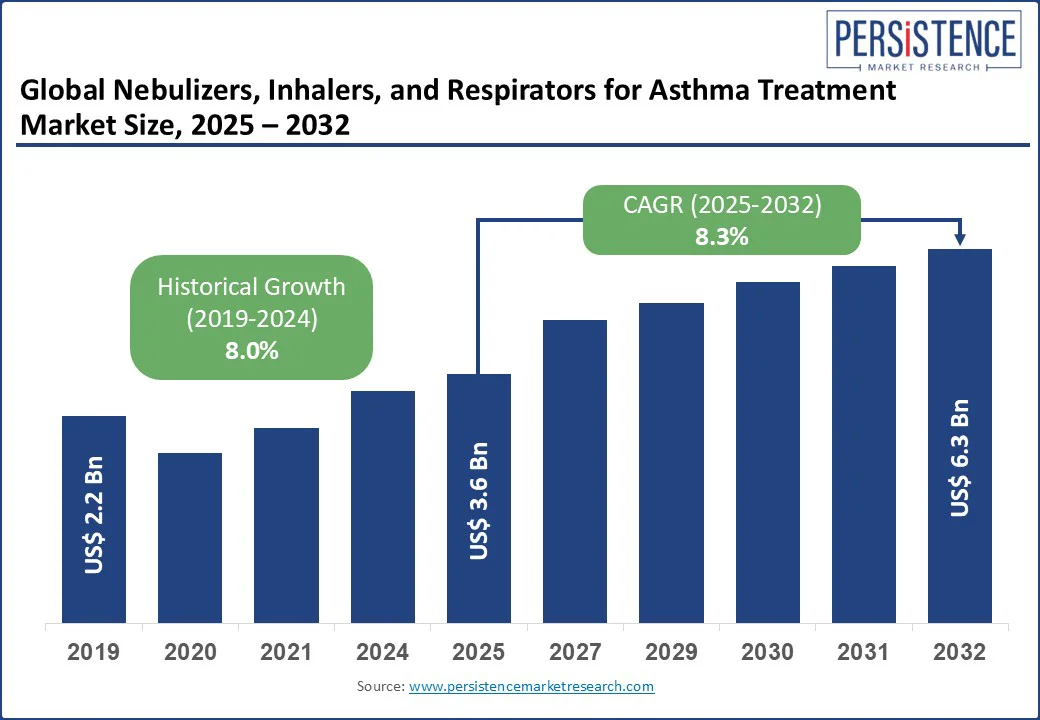

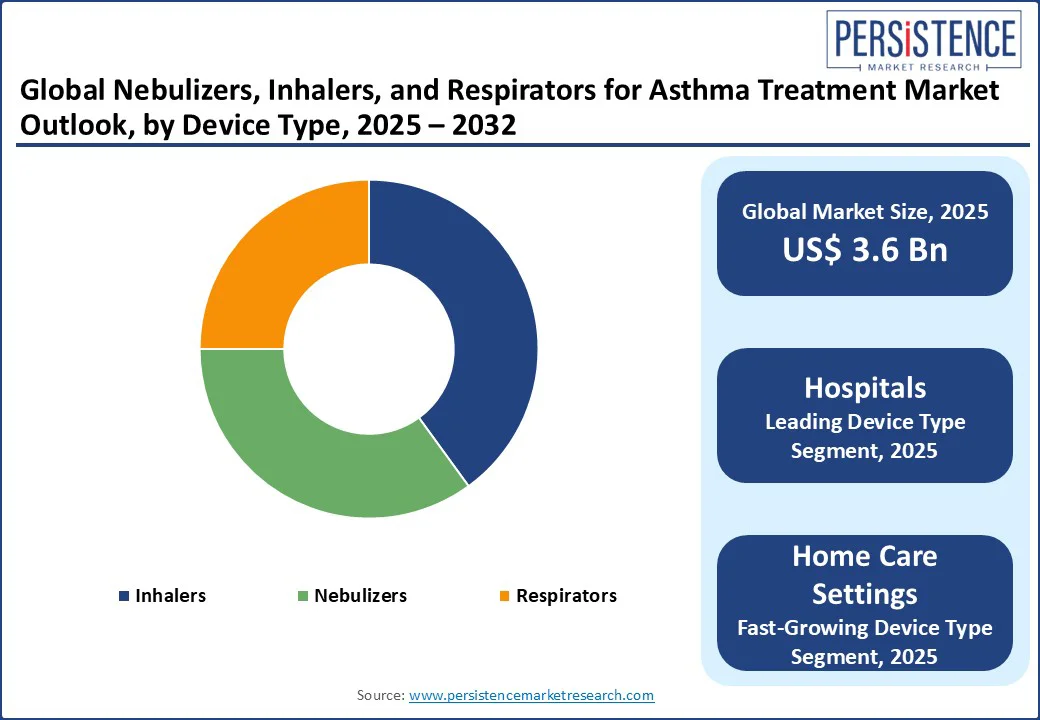

The global nebulizers, inhalers, and respirators for asthma treatment market size is likely to be valued at US$3.6 Bn in 2025 and expected to reach US$6.3 Bn by 2032, growing at a CAGR of 8.3% during the forecast period 2025 - 2032.

The nebulizers, inhalers, and respirators for asthma treatment market is driven by the rising prevalence of asthma and the growing demand for efficient respiratory drug delivery systems. Growing use of Bluetooth-enabled inhalers with mobile apps for real-time monitoring and adherence tracking. Integration of inhalation devices with wearables and cloud-based platforms for personalized asthma management. Emergence of combination inhalers (ICS + LABA) and connected nebulizers for severe asthma care.

Key Industry Highlights:

- Inhalers Lead: Inhalers hold a 50% market share in 2025, driven by metered dose inhalers (MDI) and asthma drug delivery systems.

- Smart Inhalers Growth: Smart Inhalers are fueled by connected inhalers and nebulizers.

- Chronic Asthma Surge: Chronic Asthma Treatment is driven by maintenance inhalers. Relies heavily on long-term control medications, especially inhaled corticosteroids (ICS) and combination therapies (e.g., ICS + LABA).

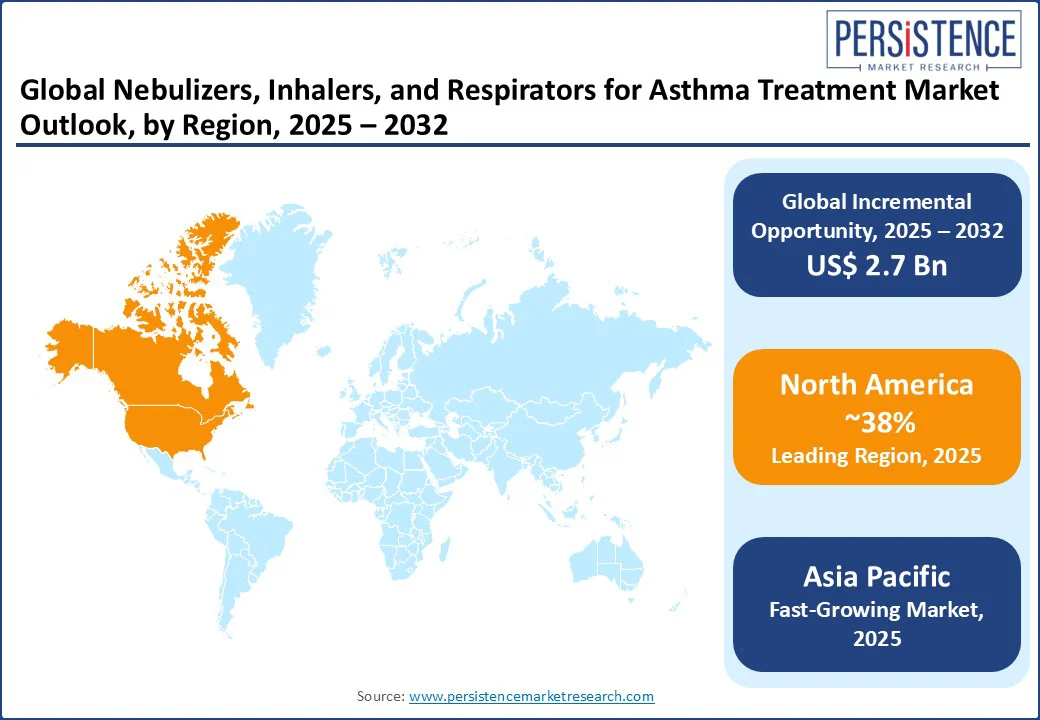

- Regional Dominance: North America commands a 38% market share, while the Asia Pacific is the fastest growing with 20%.

- Innovation Impact: Home respiratory therapy devices and wearable respiratory health monitors boost respiratory care products by 12% in 2025.

- Technology Adoption: Aerosol therapy devices drive 10% growth in pulmonary drug delivery systems.

- Healthcare Demand: Battery-operated nebulizer machines enhance asthma treatment devices for home use by 15%.

|

Global Market Attribute |

Key Insights |

|

Market Size (2025E) |

US$3.6 Bn |

|

Market Value Forecast (2032F) |

US$6.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.0% |

Market Dynamics

Driver: Rise in Global Prevalence of Asthma Cases

The nebulizers, inhalers, and respirators for asthma treatment market is driven by the rising global prevalence of asthma, as well as the increasing demand for asthma treatment solutions, including respirators and devices. Globally, 339 Mn people suffer from asthma, driving the need for asthma drug delivery systems, metered dose inhalers (MDI), and breathing treatment machines.

Respiratory therapy devices for asthma control, such as maintenance inhalers and aerosol therapy devices, are essential for managing chronic asthma, while pediatric nebulizers cater to younger patients.

Home respiratory therapy devices and battery-operated nebulizer machines enable convenient treatment, boosting the adoption of respiratory care products. The integration of connected inhalers and nebulizers, as well as wearable respiratory health monitors, enhances patient compliance, aligning with the growing focus on chronic disease management and personalized healthcare.

Restraint: High Cost of Advanced Devices

The nebulizers, inhalers, and respirators for asthma treatment market faces a significant restraint due to the high cost of advanced devices, impacting the adoption of connected inhalers and nebulizers and wearable respiratory health monitors.

The average cost of smart inhalers ranges from US$100 to US$300, limiting affordability for patients in low-income regions and smaller healthcare facilities. This cost barrier restricts the scalability of aerosol therapy devices, pulmonary drug delivery systems, and home respiratory therapy devices, particularly for pediatric nebulizers and anti-asthmatic devices, hindering market penetration in cost-sensitive markets.

Opportunity: Advancements in Smart Inhaler Technology

Advancements in smart inhalers and connected inhalers, and nebulizers present a significant opportunity for the nebulizers, inhalers, and respirators for asthma treatment market. With 25% of asthma patients adopting digital health solutions in 2025, there is a growing demand for respiratory care products integrated with wearable respiratory health monitors.

These technologies enhance treatment adherence and monitoring, driving innovation in asthma drug delivery systems and aerosol therapy devices. The focus on digital healthcare aligns with global respiratory health trends, encouraging manufacturers to develop home respiratory therapy devices and maintenance inhalers, positioning the industry for growth in tech-driven asthma management.

Category-wise Analysis

Device Type Insights

Inhalers hold a 50% market share in 2025, driven by their widespread use in asthma treatment through metered dose inhalers (MDI) and maintenance inhalers. With 55% adoption in 2025, inhalers are favored for their portability and effectiveness in asthma drug delivery systems, supporting chronic asthma treatment. They integrate easily with both controller medications (ICS) and rescue drugs (SABAs), reinforcing their central role in asthma care.

Nebulizers are fueled by demand for pediatric nebulizers and battery-operated nebulizer machines. With 12% growth in 2025, these devices are gaining traction in home respiratory therapy, particularly for severe asthma cases requiring aerosol therapy. Nebulizers are indispensable in emergency rooms and critical care for managing severe asthma attacks that require high-dose medication delivery.

Functionality Insights

Multi-dose delivery commands a 45% market share in 2025, driven by its use in maintenance inhalers and asthma drug delivery systems. Multi-dose delivery systems are widely used in maintenance inhalers, such as metered-dose inhalers (MDIs) and dry powder inhalers (DPIs), which are essential for long-term asthma control. With 50% adoption in 2025, multi-dose devices support chronic asthma treatment with convenient, repeated dosing.

Jet nebulizers and breathing treatment machines fuel continuous-flow devices, which deliver a steady stream of medication, which is critical during severe asthma attacks or for patients who struggle with inhaler techniques. With 10% growth in 2025, these devices are adopted in hospital settings for the management of acute asthma attacks.

Technology Insights

Traditional Manual Inhalers hold a 55% market share in 2025, driven by their affordability and widespread use in asthma treatment. With 60% adoption in 2025, these inhalers support metered dose inhalers (MDI) and anti-asthmatic devices for broad accessibility. These devices deliver medication directly to the lungs for both chronic asthma management and acute attack relief, making them essential in treatment protocols.

Smart Inhalers are fueled by connected inhalers and nebulizers. With 15% growth in 2025, smart inhalers enhance pulmonary drug delivery systems with digital monitoring, aligning with wearable respiratory health monitors. Smart inhalers integrate Bluetooth connectivity and digital sensors, allowing real-time monitoring of medication usage and patient adherence. These inhalers ensure precise dosing, improving therapeutic outcomes and reducing medication wastage.

Application Insights

Chronic Asthma Treatment holds a 50% market share in 2025, driven by maintenance inhalers and respiratory care products. With 55% adoption in 2025, this segment supports long-term management with asthma drug delivery systems.

Chronic asthma management relies heavily on long-term control medications, especially inhaled corticosteroids (ICS) and combination therapies (e.g., ICS + LABA). These are central to reducing airway inflammation and preventing attacks, making this segment foundational to asthma care.

Acute Asthma Attacks Management fueled by breathing treatment machines and aerosol therapy devices. With 12% growth in 2025, this segment is driven by hospital-based respiratory therapy devices for asthma control. Urbanization, air pollution, and climate change are leading to more frequent and severe asthma exacerbations, creating a higher demand for quick-relief therapies.

Regional Insights

North America Nebulizers, Inhalers, and Respirators for Asthma Treatment Market Trends

North America holds a 38% global market share in 2025, with the U.S. leading due to high asthma prevalence and advanced healthcare infrastructure, generating US$ 1.44 Bn in sales in 2025. The U.S. market grows at a CAGR of 8.1%, driven by demand for respirators and asthma devices, with 65% of asthma patients using metered dose inhalers (MDI) in 2025.

Key drivers include a 10% increase in asthma diagnoses, boosting maintenance inhalers and home respiratory therapy devices. GlaxoSmithKline (GSK) and AstraZeneca drive 25% of regional revenue, with connected inhalers and nebulizers seeing 10% growth. The focus on chronic disease management fuels pulmonary drug delivery systems and aerosol therapy devices.

Europe Nebulizers, Inhalers, and Respirators for Asthma Treatment Market Trends

Europe accounts for a 30% global share, led by Germany, the UK, and France. Germany’s market grows at a CAGR of 8.2%, driven by high asthma rates and healthcare access, with 60% of patients using respiratory care products in 2025. UK’s growth is propelled by pediatric nebulizers, with NHS clinics adopting breathing treatment machines.

France witnessed a 12% growth in asthma drug delivery systems, driven by demand for anti-asthmatic devices. EU healthcare investments, with €100 Mn in respiratory care in 2025, boost aerosol therapy devices. Boehringer Ingelheim holds a 10% market share, leveraging maintenance inhalers.

Asia Pacific Nebulizers, Inhalers, and Respirators for Asthma Treatment Market Trends

Asia Pacific is the fastest-growing region, with a CAGR of 8.8%, led by China, India, and Japan. China holds a 45% regional market share, driven by a 15% increase in asthma cases in 2025, boosting respirators and asthma devices. India’s market is fueled by rising healthcare access, with 70% of urban patients using home respiratory therapy devices in 2025.

Japan’s connected inhalers and nebulizers drive 10% growth in pulmonary drug delivery systems, supported by its aging population. Cipla and PARI lead, supported by US$2 Bn in healthcare investments by 2030, enhancing respiratory care products.

Competitive Landscape

The global nebulizers, inhalers, and respirators for asthma treatment market is highly competitive, with respiratory care companies focusing on innovation, accessibility, and patient-centric solutions. GlaxoSmithKline (GSK) and AstraZeneca lead in metered dose inhalers (MDI), while Philips excels in battery-operated nebulizer machines.

Pulmonary drug delivery systems, aerosol therapy devices, and connected inhalers and nebulizers drive competition. Strategic partnerships and R&D investments in home respiratory therapy devices and wearable respiratory health monitors are key differentiators, addressing chronic asthma management and patient needs.

Industry Developments

- In August 2024, the proven Philips launched a battery-operated nebulizer machine, Side Stream nebulizers are designed to boost airflow, via an active venturi system, resulting in fast drug delivery and short treatment times. Featuring a unique diamond jet design which helps to minimize wear from Side Stream will provide consistent drug delivery time after time, making Philips Side stream nebuliser an ideal choice for aerosol drug delivery you can trust.

- In 2022, Cipla expanded its pulmonary drug delivery systems portfolio in Asia Pacific region, focusing on advanced inhalation therapies and respiratory care solutions. This strategic move enabled the company to strengthen its presence in emerging markets, where asthma prevalence and demand for affordable inhalers and nebulizers are rapidly increasing.

- In July 2021, PARI GmbH collaborated with TWT Digital Health (TWT) and developed the PARI Connect app. This app can be used to plan inhalations, take medications, or make doctor’s appointments and enables the user to observe all the facts of their therapy. The app also communicates via Bluetooth with the eTrack controller, a control unit for PARI’s eFlow Technology nebulizer.

Companies Covered in Nebulizers, Inhalers, and Respirators for Asthma Treatment Market

- GlaxoSmithKline (GSK)

- AstraZeneca

- Boehringer Ingelheim

- Philips

- Omron

- 3M Health Care

- Dräger

- Cipla

- PARI

- Gerresheimer

- Aptar Pharma

- Others

Frequently Asked Questions

The nebulizers, inhalers and respirators market is projected to reach US$ 3.6 Bn in 2025, driven by respirators and asthma devices.

Rising asthma prevalence, drives demand for asthma drug delivery systems.

The nebulizers, inhalers, and respirators for asthma treatment market grows at a CAGR of 8.3% from 2025 to 2032, reaching US$ 6.3 Bn by 2032.

Smart inhalers, with 25% patient adoption, offer opportunities for connected inhalers and nebulizers.

Key players include GlaxoSmithKline (GSK), AstraZeneca, Boehringer Ingelheim, and Philips.