- Medical Devices

- Sputum Liquefaction Market

Sputum Liquefaction Market Size, Share, and Growth Forecast, 2026 - 2033

Sputum Liquefaction Market by Product Type (Mucolytic Agents, Chemical Liquefying Agents, Medical Devices), Clinical Procedure (Homogenization, Others), End-user (Diagnostic Laboratories, Others), and Regional Analysis 2026 - 2033

Sputum Liquefaction Market Size and Trends Analysis

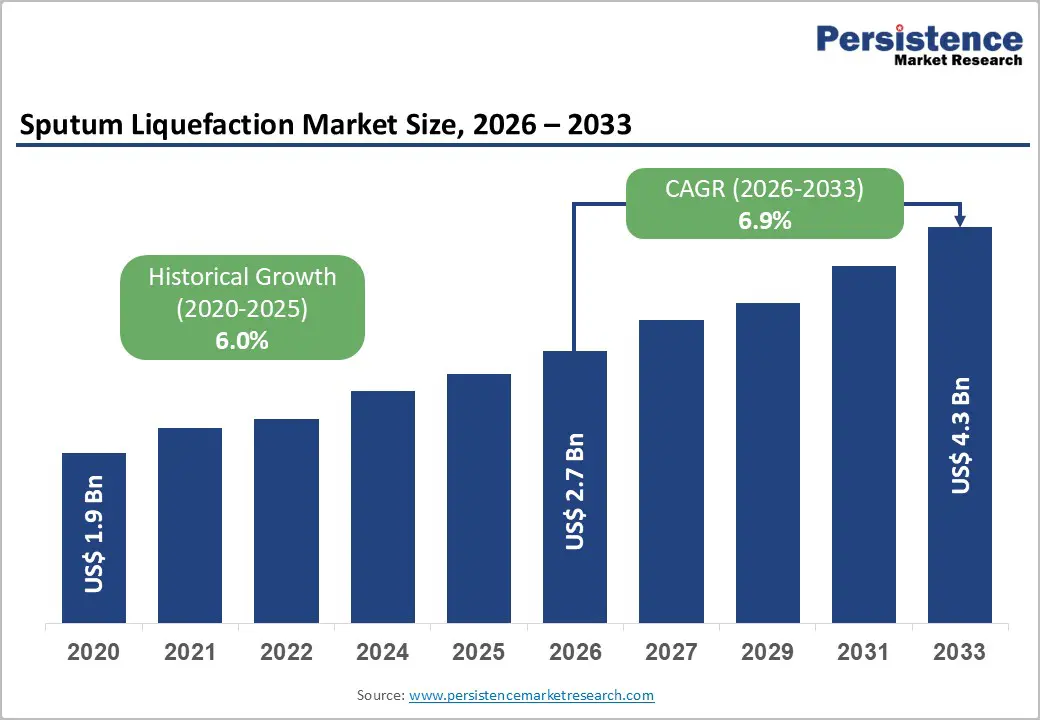

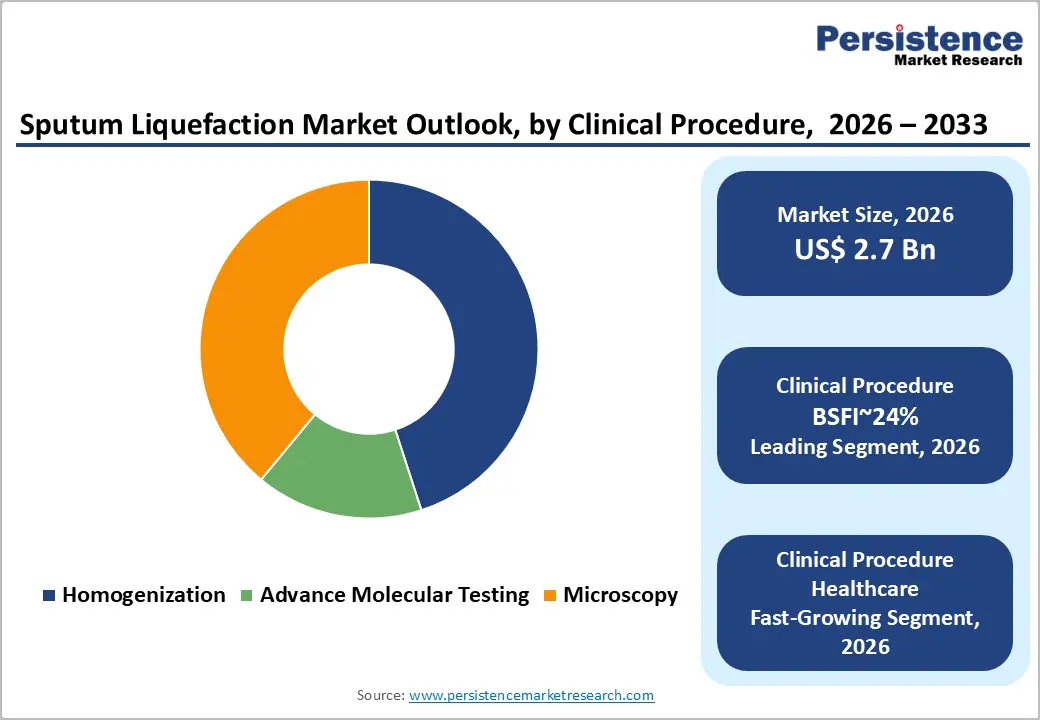

The global sputum liquefaction market size is likely to be valued at US$2.7 billion in 2026 and is expected to reach US$4.3 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by the rising respiratory disease prevalence, including TB and COPD, which boosts the demand for effective sputum processing in diagnostics. Advancements in mucolytics such as DTT and NAC, alongside automated devices, enhance sample homogenization for accurate testing.

The market is also benefiting from a strategic shift toward decentralized diagnostic laboratory settings, particularly in emerging economies where respiratory health infrastructure is undergoing rapid expansion. Growth is supported by continued investments in respiratory healthcare infrastructure, rising adoption of laboratory diagnostics in developing regions, and improvements in reagents and protocols that improve speed and consistency of liquefaction.

Key Industry Highlights:

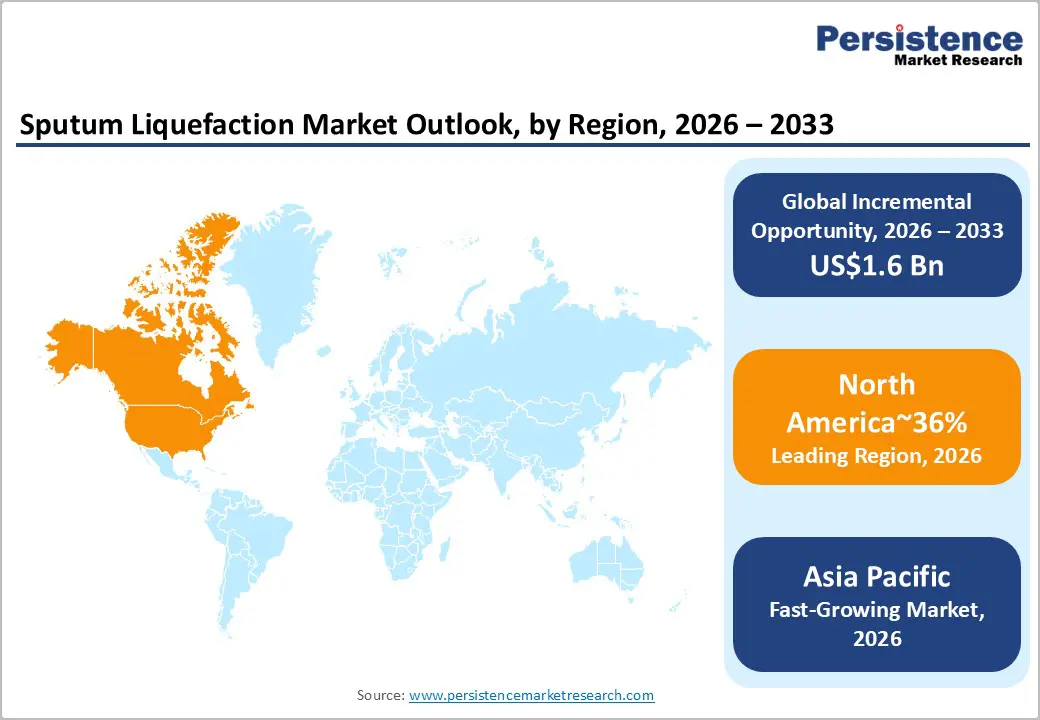

- Leading Region: North America is projected to lead due to high-throughput diagnostic laboratories, AI-enabled and automated platforms, and ecosystem advantages, accounting for approximately 36% share in 2026.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest due to rising respiratory disease prevalence, government healthcare initiatives, and adoption across decentralized laboratory and point-of-care sectors.

- Leading Product Type: Mucolytic agents are expected to lead, accounting for approximately 43% share in 2026, through industrial adoption, reproducibility, workflow integration, and high-value diagnostic applications.

- Leading Clinical Procedure: Homogenization is projected to dominate for simplicity, operational reliability, adoption, and functional use across key diagnostic sectors, holding approximately 45% share in 2026.

| Key Insights | Details |

|---|---|

|

Sputum Liquefaction Market Size (2026E) |

US$2.7 Bn |

|

Market Value Forecast (2033F) |

US$4.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Technological Integration of Molecular Diagnostics

The widespread integration of molecular diagnostics, particularly Nucleic Acid Amplification Tests (NAAT) and RT-PCR, is reshaping the sputum liquefaction market by redefining pre-analytical sample requirements. Unlike conventional microscopy, molecular assays demand fully homogenized and contaminant-free sputum to prevent microfluidic obstruction and reduce PCR inhibitor interference. This technical necessity is elevating reliance on specialized chemical mucolytic agents, including Dithiothreitol and N-acetyl-L-cysteine, which achieve high liquefaction efficiency while preserving microbial nucleic acid integrity.

The adoption of these agents is closely linked to laboratory workflows that prioritize accuracy, throughput, and reproducibility, creating structural shifts in reagent selection, procurement, and value-chain logistics. Regulatory and quality assurance frameworks also increasingly mandate standardized sample processing protocols to ensure reliable molecular diagnostic outputs across diverse laboratory settings. This drives technology-led investment in reagent innovation, process automation, and validation, embedding higher operational precision and analytical reliability throughout the sputum pre-processing segment.

The migration toward molecular testing is stimulating demand for integrated sample preparation systems and automated liquefaction platforms capable of handling complex respiratory matrices. Laboratories are adjusting cost structures to accommodate high-performance reagents and specialized consumables, impacting margin allocations and procurement strategies. The evolution of molecular assay platforms encourages harmonization between sample pre-treatment and downstream analytical instrumentation, linking reagent efficacy directly to diagnostic sensitivity and specificity. The interplay between technological evolution, regulatory compliance, and value-chain adaptation underscores the strategic significance of advanced liquefaction agents in supporting high-quality molecular diagnostics. As adoption scales across clinical and public health laboratories, this driver structurally amplifies market demand while reinforcing the critical role of standardized, technology-compatible sputum liquefaction workflows.

Technological Advancements in Sputum Liquefaction Platforms

The emergence of acousto-fluidic liquefaction technologies is reshaping sample preparation dynamics by enabling continuous low-shear processing without compromising cellular integrity or diagnostic targets. These physics-driven devices outperform manual homogenization by delivering consistent rheological transformation while minimizing operator variability and workflow bottlenecks. Parallel development of automated liquefaction platforms has accelerated throughput and reduced hands-on processing duration relative to legacy manual methods, reinforcing laboratory efficiency and quality control metrics.

Regulatory clearances for integrated liquefaction solutions have strengthened institutional confidence in device adoption across clinical and reference laboratory settings. Standardized operations embedded within these platforms enhance reproducibility and reduce pre-analytical error, aligning with external quality assurance frameworks and accreditation standards. The technical maturation of liquefaction hardware is therefore repositioning this segment as a critical enabler within respiratory diagnostics value chains rather than a peripheral reagent step.

The adoption of advanced liquefaction devices is lifting the product-based segment’s contribution to total revenues. Integration at point-of-care and decentralized testing sites is expanding addressable installation bases beyond centralized laboratories. Endorsement of standardized liquefaction protocols by global health authorities is expanding volume requirements within tuberculosis and broader respiratory testing workflows. This regulatory alignment fosters greater demand elasticity and justifies capital allocation toward specialized hardware procurement. Value chain cost structures are adjusting to accommodate the capital intensity of automated platforms, altering total cost of ownership calculations for laboratory managers. Collectively, these technological advancements are modifying competitive dynamics and expanding market depth for both devices and associated reagents.

Barrier Analysis - Cost Barriers in Automated Sputum Liquefaction Adoption

The high capital intensity of automated sputum liquefaction systems constitutes a structural barrier within the diagnostic market, particularly affecting small-to mid-sized laboratories and low-resource settings. While these devices offer reproducible, high-throughput sample processing and improved biosafety, their acquisition and operational costs, including specialized consumables, maintenance, and calibration, significantly elevate the total cost of ownership. As a result, institutions with limited budgets continue to rely on manual or semi-automated chemical liquefaction methods. These lower-cost alternatives, while financially accessible, introduce variability in sample homogenization, compromise reproducibility, and elevate occupational exposure risks due to manual handling of viscous respiratory specimens.

At the market and value-chain level, this cost barrier constrains adoption rates for high-end mechanical devices despite their technical advantages, creating segmentation between well-funded laboratories and resource-limited facilities. Procurement decisions are heavily influenced by budgetary cycles and grant-dependent funding, which slows the diffusion of automated solutions in regions with high tuberculosis and respiratory disease prevalence. Consequently, reagent-based manual workflows remain dominant in operational pipelines, while device manufacturers face structural challenges in scaling adoption across heterogeneous laboratory environments.

Safety and Reagent Toxicity Constraints in Sputum Liquefaction

Occupational safety and chemical stability issues constitute significant restraints within the sputum liquefaction market, particularly for high-risk respiratory pathogens such as Mycobacterium tuberculosis. Traditional decontamination agents, including sodium hydroxide, deliver effective sample processing but pose handling hazards and can compromise sample integrity without strict adherence to safety protocols. Concurrently, mucolytic reagents such as Dithiothreitol exhibit limited shelf-life once reconstituted, necessitating frequent daily preparation that introduces variability in concentration, potential reagent waste, and workflow inefficiencies. These factors collectively heighten operational complexity and impose additional training, storage, and quality control requirements across laboratory environments.

Safety and reagent limitations directly influence product design, procurement strategies, and standard operating procedures. Manufacturers are compelled to develop formulations that combine stability, reduced toxicity, and pre-measured dosing to mitigate handling risks and ensure consistent liquefaction performance. Regulatory compliance frameworks and occupational safety standards further reinforce the need for less hazardous, more robust reagents. Consequently, these constraints shape market segmentation by limiting adoption in laboratories lacking infrastructure for stringent safety and storage protocols, while driving technological innovation toward safer, standardized chemical solutions.

Opportunity Analysis - AI-Enabled Sample Quality Optimization in Sputum Liquefaction

The integration of artificial intelligence with mechanical sputum liquefaction platforms is transforming pre-analytical workflows by enabling real-time monitoring and adaptive control of sample processing parameters. AI-driven sensors assess viscosity, homogeneity, and cellular integrity continuously, dynamically adjusting mechanical agitation or chemical dosing to achieve consistent sputum liquefaction for downstream molecular and culture-based assays. This automation enhances reproducibility, minimizes operator-dependent variability, and ensures alignment with stringent laboratory quality standards.

The convergence of AI with hardware platforms also facilitates data-driven validation, process documentation, and regulatory compliance, embedding intelligent oversight within routine diagnostic operations. Such technological sophistication elevates operational efficiency, reduces sample rejection rates, and integrates predictive maintenance insights to sustain device performance across high-throughput laboratory environments.

AI-enabled liquefaction devices strengthen adoption in hospital-based and centralized laboratories, where precision, scalability, and workflow standardization are critical. Value-chain implications include increased demand for advanced sensors, software integration, and AI-compatible reagents, reshaping cost structures and procurement priorities. Regulatory authorities are increasingly recognizing AI-supported quality assurance as a differentiator in diagnostic accuracy, reinforcing investment in intelligent platforms. Consequently, AI convergence not only drives premium market positioning but also establishes a benchmark for technological differentiation, operational reliability, and standardization across sputum processing workflows.

Point-of-Care Device Innovations in Sputum Liquefaction

Advancements in point-of-care sputum liquefaction devices are redefining sample preparation workflows by enabling decentralized, rapid, and standardized processing outside traditional laboratory environments. Compact, integrated platforms combine mechanical homogenization with optimized chemical agents to produce homogenous sputum suitable for molecular or microbiological analysis in near real-time. These innovations reduce reliance on centralized laboratories, shorten turnaround times, and minimize pre-analytical errors associated with sample transport and handling.

Regulatory endorsements and alignment with global tuberculosis and respiratory disease guidelines enhance adoption, while standardization protocols embedded within these devices improve reproducibility and biosafety compliance across diverse healthcare settings. Point-of-care integration also supports high-frequency screening initiatives, enabling early detection in outpatient and community-based testing programs.

The point-of-care liquefaction devices influence procurement strategies, laboratory workflow design, and cost allocation by embedding automated processing at the collection site. Manufacturers focus on reagent stability, device portability, and maintenance simplicity to meet operational constraints in low-resource or remote settings. These innovations shift the market toward decentralized diagnostic infrastructure, expanding adoption across emerging and mature regions while reinforcing demand for compatible chemical agents and consumables. Consequently, the segment is positioned as a structural enabler of efficient, standardized, and high-quality sputum diagnostics across heterogeneous healthcare delivery models.

Category-wise Analysis

Product Type Insights

Mucolytic agents are expected to lead, accounting for approximately 43% share in 2026, driven by their entrenched role in both conventional and molecular diagnostic workflows in 2026. These agents, including DTT, NAC, and Bromhexine, deliver consistent disulfide-bond disruption across diverse sputum viscosities, ensuring high-quality homogenates for smear microscopy, NAAT, and RT-PCR assays. Adoption remains anchored by cost-effectiveness, operational simplicity, and compatibility with standardized laboratory protocols, with enterprises prioritizing reproducibility, workflow integration, and sample integrity in high-throughput settings.

Ongoing platform evolution, including pre-measured buffers, dual-action formulations, and microfluidic integration, continues to reinforce utilization intensity. Leading brands such as Thermo Fisher Scientific (Sputolysin), BD (BBL™ MycoPrep™), and Alpha Tec Systems and their portfolios lock in laboratory workflows, enabling predictable demand. This combination of mature infrastructure, reagent reliability, and high operational alignment sustains the dominance of mucolytic agents across structured deployment models globally.

Medical devices are expected to be the fastest-growing segment, driven by emerging needs for standardized, high-throughput processing across hospital and diagnostic laboratory environments. Growth is catalyzed by automation, acoustofluidic on-chip technologies, bead-beating systems, and AI-enabled viscosity sensors, which materially improve reproducibility, biosafety, and processing speed for delicate or high-viscosity samples.

The adoption is being driven by integrated closed-loop systems, digital audit trails, and reduced manual handling, which minimize operator exposure to infectious aerosols and lower labor requirements. Leading companies, such as Bertin Technologies (Precellys), Omni International, and Hielscher Ultrasonics, are offering modular mechanical solutions to meet early-stage demand while creating operational switching barriers.

Clinical Procedure Insights

Homogenization is expected to lead the market, accounting for approximately 45% share in 2026, driven by its foundational role in virtually all clinical respiratory diagnostics. This procedure ensures viscous sputum specimens are converted into uniform liquids, enabling accurate pipetting, slide preparation, and representative sampling across microscopy, culture, and molecular workflows. Adoption remains anchored by operational reliability, workflow standardization, and compatibility with automated liquid culture systems, with laboratories prioritizing sample integrity, reproducibility, and biosafety in high-throughput environments.

Ongoing technological evolution, including micro-bead homogenizers, aerosol-free sealed chambers, and digital homogeneity scanning, continues to reinforce utilization intensity and reduce pre-analytical errors. Leading brands such as Copan Diagnostics (Snot-Box™), BD (MycoPrep™), Miltenyi Biotec (gentleMACS™), and Alpha Tec Systems (NAC-PAC®) lock in enterprise workflows. This combination of mature infrastructure, technological integration, and consistent clinical outcomes sustains homogenization’s dominance across structured diagnostic settings globally.

Advanced molecular testing is expected to be the fastest-growing segment, driven by accelerating adoption of NAAT, RT-PCR, and Next-Generation Sequencing for respiratory pathogens. Growth is catalyzed by the need for ultra-pure, inhibitor-free sputum samples that preserve microbial DNA/RNA integrity while enabling rapid turnaround in drug-resistant TB, influenza, and post-COVID testing scenarios.

Accelerating adoption is supported by integrated molecular platforms, one-pot liquefaction reagents, and digital microfluidic systems that automate sample preparation and minimize operator exposure. Brands including Cepheid (Xpert MTB/RIF), Qiagen (QIAamp DNA Microbiome Kit), Hain Lifescience, Zymo Research (DNA/RNA Shield™), and Molbio Diagnostics (Truenat™) are deploying advanced solutions to capture early-cycle demand and embed workflow fidelity. As analytical sensitivity, cold-chain independence, and WHO prequalification expand, molecular testing liquefaction is poised to outpace overall market growth during the forecast period.

Regional Insights

North America Sputum Liquefaction Market Trends

North America is expected to maintain its position as the leading regional market in the global sputum liquefaction ecosystem, approximating 36% of the overall market share in 2026. The region’s structural dominance is anchored in its concentration of high-throughput diagnostic laboratories, extensive adoption of automated mechanical liquefaction platforms, and deep integration of molecular and point-of-care workflows.

Advanced healthcare infrastructure, supported by a dense network of CLIA-certified labs, facilitates rapid deployment of AI-enabled and microfluidic liquefaction solutions, while strategic domestic manufacturing by Thermo Fisher, Danaher, and BD ensures supply continuity and platform standardization. Demand is reinforced by the high prevalence of chronic respiratory diseases, widespread use of NAAT and molecular panels, and consistent reimbursement policies that justify premium instrumentation, collectively sustaining North America’s leadership in precision respiratory diagnostics.

The U.S. anchors regional momentum, driving adoption of integrated mechanical and chemical liquefaction solutions across both clinical and research settings. Investment flows focus on “Triple-demic” preparedness, home-based sputum collection, and molecular proteomics/metabolomics programs, while FDA 510(k) clearance, CLIA mandates, and CDC TB guidelines reinforce compliance-driven deployment.

Leading market players, including Danaher (Cepheid), Thermo Fisher Scientific, BD, Abbott Laboratories, and QuidelOrtho, are expanding AI-integrated homogenizers, closed-system microfluidic devices, and pre-measured reagent kits to optimize workflow efficiency and biosafety. Ongoing innovation in acoustofluidic, bead-beating, and cloud-connected platforms positions the U.S. to continue shaping regional adoption patterns, ensuring North America remains the reference market for high-value, automated sputum liquefaction systems over the forecast horizon.

Asia Pacific Sputum Liquefaction Market Trends

Asia Pacific is expected to register the fastest growth trajectory, driven by a high prevalence of Tuberculosis (TB), COPD, and residual COVID-19 cases, combined with expanding healthcare infrastructure and industrial-scale manufacturing advantages. Transition from manual to automated and semi-automated sputum processing solutions is set to accelerate, supported by government programs, digitization of laboratory workflows, and decentralization of respiratory care.

Cost-sensitive markets are increasingly adopting localized, low-cost reagents and portable liquefaction devices, while sustainability and AI-enabled diagnostic integration reinforce the long-term scalability of solutions. Cross-border investments and public health funding, particularly in India, China, and Southeast Asia, are expected to strengthen supply chains, expand district-level molecular diagnostic networks, and catalyze adoption in rural and semi-urban regions, positioning Asia Pacific as the global innovation and volume-driven hub for sputum management technologies.

India anchors regional momentum, shaping both demand and supply dynamics through large-scale public health initiatives such as Ayushman Bharat and the expansion of district-level GeneXpert NAAT facilities for TB detection. Policy support, including eased import regulations via CDSCO and incentives for domestic manufacturing, is expected to enhance local production of sputum processing kits and reagents, reducing cost barriers.

Leading vendors such as Yuwell, ReaMetrix, Cepheid, Jiangsu Folee Medical Equipment, and BD are projected to focus on portable, AI-enabled, and minimally invasive devices to meet the needs of decentralized care. Forward-looking adoption trends emphasize rapid molecular-grade liquefaction, digital workflow integration, and regulatory-compliant solutions, reinforcing Asia Pacific’s role as the primary growth engine for high-volume.

Europe Sputum Liquefaction Market Trends

Europe is expected to remain a structurally stable market in the global landscape. The region’s positioning is anchored in stringent regulatory harmonization under the EU. Demand is primarily driven by centralized laboratory automation, chronic respiratory disease monitoring, and targeted Cystic Fibrosis research, while sustainability mandates accelerate adoption of multi-use mechanical homogenizers over single-use chemical kits. High public healthcare coverage across Germany, the U.K., and France ensures predictable procurement cycles, supporting continued enterprise penetration by certified vendors such as Roche Diagnostics, Hain Lifescience, and Bertin Technologies. Integration of digital microbiology platforms and aerosol-free bead-beating systems further strengthens Europe’s stable adoption of automated, high-precision sputum processing technologies across research and clinical applications.

Germany anchors the regional momentum, driving market standardization through its extensive TB screening programs and Cystic Fibrosis Centers of Excellence, which demand highly concentrated mucolytic and mechanical homogenization solutions. Regulatory oversight, including IVDR compliance and occupational health mandates, enforces closed-system processing, guiding vendor strategies toward pre-validated chemical reagents and mechanical devices.

Leading European suppliers, such as Roche Diagnostics, Bertin Technologies, Hain Lifescience, Eppendorf, and Mast Group, are expanding offerings in aerosol-free homogenization, digital workflow integration, and molecular-grade reagents. Forward-looking adoption is expected to focus on personalized respiratory medicine, high-throughput automation, and sustainable laboratory operations, reinforcing Europe’s stable, compliance-driven market role while maintaining consistent revenue streams across national healthcare systems.

Competitive Landscape

The global sputum liquefaction market is moderately fragmented, with leadership concentrated among global suppliers such as BD (Becton Dickinson), Cepheid, Thermo Fisher Scientific, and Roche Diagnostics. These leaders matter because their platforms set functional benchmarks for high-throughput sample processing, molecular-grade liquefaction, and closed-system biosafety compliance, directly shaping laboratory procurement decisions and operational standards.

Competitive positioning is defined by horizontal differentiation across manual, semi-automated, and fully automated solutions, as well as vertical integration with molecular diagnostics, AI-enabled workflow tools, and reagent supply chains. Industry behavior is increasingly characterized by platform evolution toward modular, portable, and digital-ready systems, consolidation of service-led laboratory support networks, and selective mergers or acquisitions aimed at strengthening molecular capabilities or geographic reach.

Companies Covered in Sputum Liquefaction Market

- Becton, Dickinson and Company (BD)

- Thermo Fisher Scientific Inc.

- Copan Diagnostics Inc.

- Hardy Diagnostics

- Roche Diagnostics

- Alpha-Tec Systems

- Greiner Bio-One

- Pro-Lab Diagnostics

- Merck KGaA (Sigma-Aldrich)

- ELITechGroup

- Hain Lifescience (Bruker)

- MWE (Medical Wire & Equipment)

- Bio-Rad Laboratories

- Danaher Corporation (Cepheid)

- G-Biosciences

- Boehringer Ingelheim

Frequently Asked Questions

The global sputum liquefaction market is projected to be valued at US$2.7 billion in 2026 and is expected to reach US$4.3 billion by 2033, driven by rising prevalence of respiratory diseases such as tuberculosis and COPD, increasing adoption of molecular diagnostics, and the shift toward automated and point-of-care sputum processing systems.

Integration of molecular diagnostics, including NAAT and RT-PCR, demands fully homogenized, contaminant-free sputum, elevating reliance on specialized mucolytic agents and automated liquefaction platforms. This ensures reproducibility, reduces PCR inhibition, and aligns with regulatory standards, making technology-driven sample processing essential for accurate respiratory diagnostics and high-throughput laboratory workflows.

The sputum liquefaction market is forecast to grow at a CAGR of 6.9% from 2026 to 2033, reflecting rising demand for automated, AI-enabled, and high-throughput sample preparation solutions across clinical, research, and decentralized laboratory settings globally.

North America is expected to lead, accounting for approximately 36% share in 2026, supported by dense networks of CLIA-certified laboratories, early adoption of AI-enabled and automated platforms, high chronic respiratory disease prevalence, and strategic domestic manufacturing by companies such as Thermo Fisher, BD, and Danaher.

The sputum liquefaction market is moderately fragmented, with leadership concentrated among BD (Becton Dickinson), Cepheid, Thermo Fisher Scientific, Roche Diagnostics, Copan Diagnostics, Hain Lifescience, Alpha-Tec Systems, Danaher, Greiner Bio-One, and Eppendorf. These companies compete through platform innovation, molecular-grade reagents, AI integration, and closed-system biosafety solutions.