- Semiconductor Materials & Components

- NAND Flash Memory Market

NAND Flash Memory Market Size, Share, and Growth Forecast 2026 - 2033

NAND Flash Memory Market by Type (SLC (Single-Level Cell), MLC (Multi-Level Cell), TLC (Triple-Level Cell), and QLC (Quad-Level Cell)), Structure (2D (Planar) NAND and 3D NAND), Interface (SATA, PCIe / NVMe, and UFS / eMMC), Application (Smartphones, Solid-State Drives (PC and Console), and Others), and Regional Analysis

NAND Flash Memory Market Size and Share Analysis

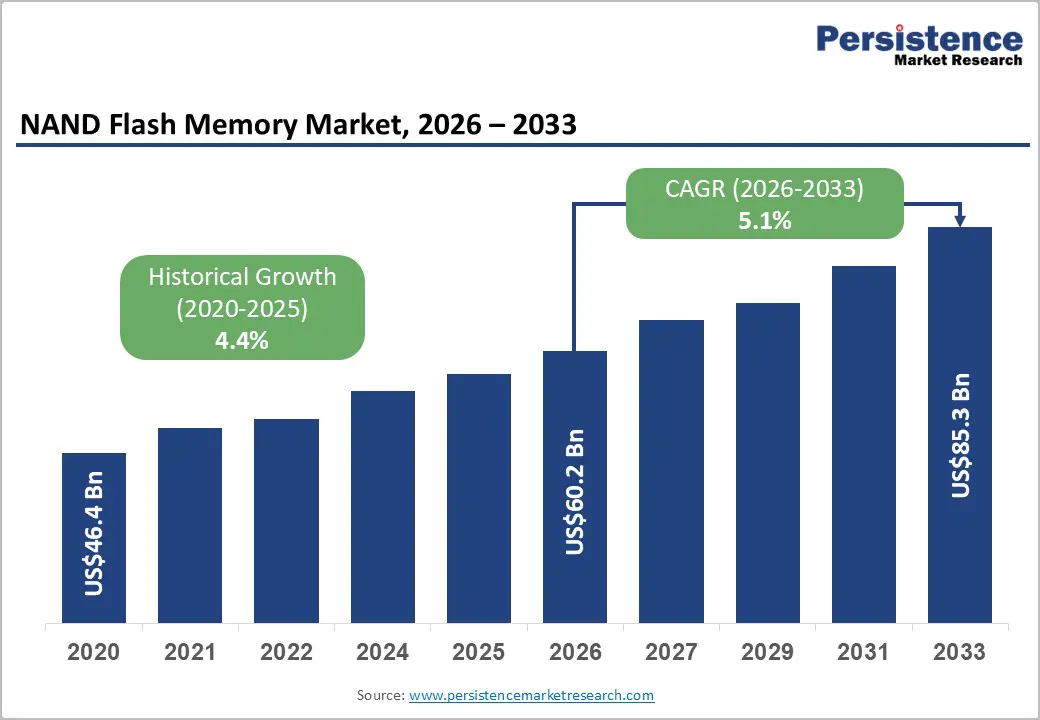

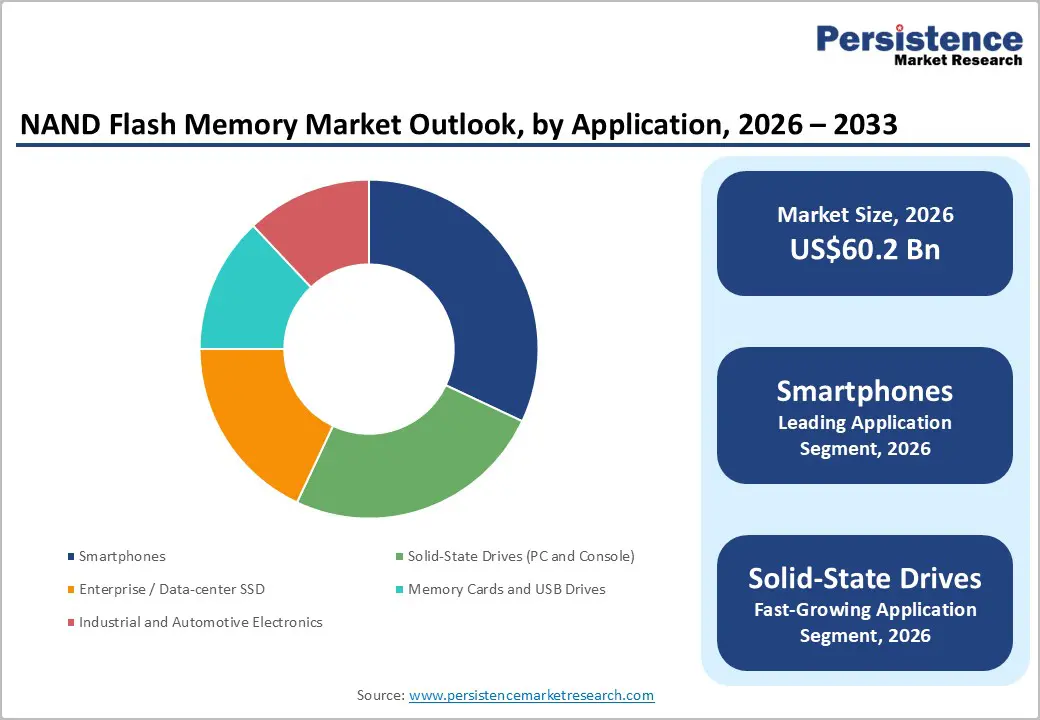

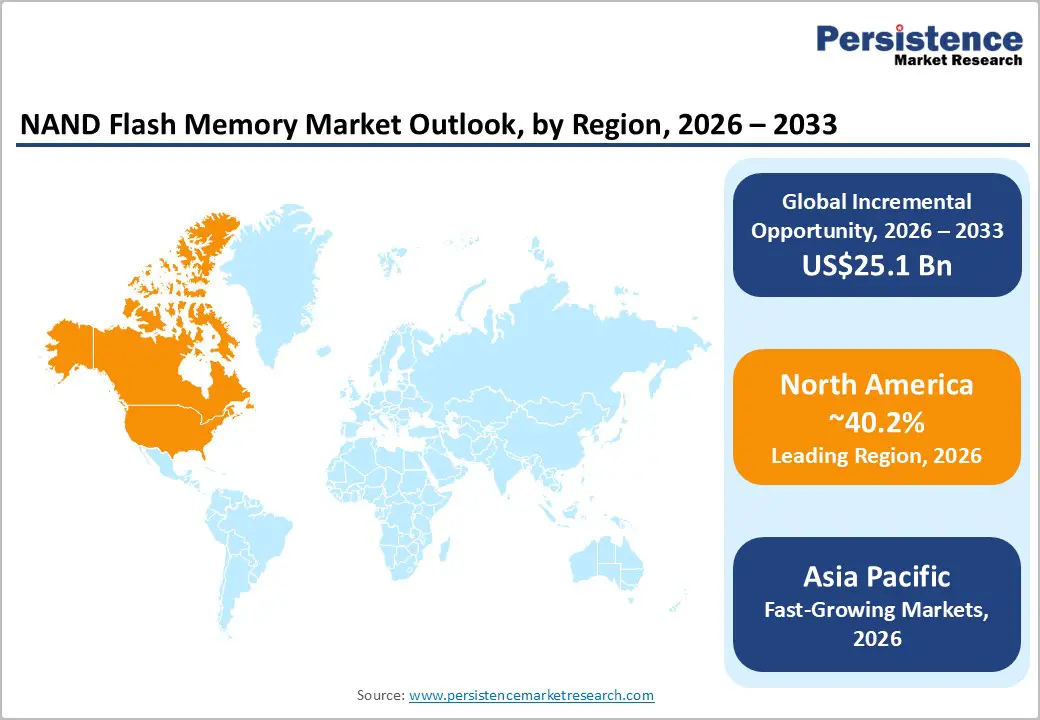

The global NAND Flash Memory market size was valued at US$ 60.2 billion in 2026 and is projected to reach US$ 85.3 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

The market expansion is primarily driven by unprecedented demand for high-capacity storage from artificial intelligence data centers, the accelerated transition from mechanical hard disk drives to enterprise solid-state drives, and the rapid advancement of three-dimensional NAND technology, which enables higher storage density at lower costs. The global surge in artificial intelligence investments has fundamentally transformed storage market dynamics, with major cloud service providers and technology companies substantially increasing their procurement of NAND flash for data center infrastructure.

Key Market Highlights

- Leading Region: North America dominates the NAND Flash Memory market with approximately 40.2% global market share, supported by the concentration of major technology companies, including Intel, Micron, and Western Digital, hyperscale cloud providers, including AWS, Microsoft, Google, and Meta, and extensive data center infrastructure investments supporting artificial intelligence workloads.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing regional market, driven by China's manufacturing dominance, India's rapid digital adoption and smartphone production growth, government-backed digitization initiatives, and strategic investments from major NAND manufacturers establishing production capacity across Vietnam, Thailand, and Malaysia.

- Dominant Application: Smartphones account for the largest application segment, with approximately 32% of total NAND flash consumption, driven by over one billion annual smartphone sales globally, escalating storage requirements for multimedia and applications, and universal deployment across consumer electronics manufacturers.

- Growing Application: Data center solid-state drives represent the fastest-growing application segment, with data center NAND demand now exceeding smartphone demand as of 2024, driven by artificial intelligence infrastructure investment, hyperscale cloud provider expansion, and transition from mechanical hard disk drives to all-flash storage architectures.

- Key Market Opportunity: Automotive electronics sector expansion is the principal market opportunity, with a 11.6% CAGR through 2033, driven by autonomous vehicle development, which requires 100 times the NAND flash of conventional vehicles; advanced driver-assistance systems; electric vehicle battery management systems; and infotainment system sophistication, which accounts for 80% of automotive NAND demand.

| Key Insights | Details |

|---|---|

|

NAND Flash Memory Market Size (2026E) |

US$ 60.2 Bn |

|

Market Value Forecast (2033F) |

US$ 85.3 Bn |

|

Projected Growth CAGR (2026-2033) |

5.1% |

|

Historical Market Growth (2020-2025) |

4.4% |

Market Dynamics

Market Growth Drivers

Robust Data Center Expansion and AI-Driven Storage Demand

The exponential growth in artificial intelligence infrastructure investments has fundamentally reshaped the NAND flash memory market landscape, creating unprecedented demand for high-capacity storage solutions. Major technology companies including Google, Meta, Amazon Web Services, and Microsoft are conducting massive capital expenditures to construct and upgrade data center facilities supporting artificial intelligence model training and inference workloads. According to industry analysis, NAND flash prices rose approximately 15% in the third quarter of 2025, driven by strong demand for enterprise-grade solid-state drives at advanced technology nodes.

The accelerated transition from traditional hard disk drives to enterprise SSDs represents a structural market shift, as organizations recognize the superior performance, energy efficiency, and reliability advantages of flash-based storage. Western Digital's Chief Executive Officer reported that 2024 marked the first year in which data center NAND demand surpassed mobile-device demand, representing a fundamental market inflection point. Supply-demand imbalances have resulted in extended lead times for premium NAND flash products, with major suppliers including Samsung, SK Hynix, Kioxia, and Micron reducing production capacity by 10-25% to manage supply equilibrium and implementing price increases to capture value from constrained supply.

Advancement of Three-Dimensional NAND Technology and Cost Reduction

The maturation of three-dimensional NAND flash technology has enabled dramatic increases in storage density while simultaneously reducing per-gigabyte costs, driving rapid market adoption across consumer and enterprise applications. Three-dimensional TLC (Triple-Level Cell) NAND currently dominates the flash memory market, accounting for approximately 38.09% of total market share in 2024, while three-dimensional QLC (Quad-Level Cell) NAND is experiencing rapid adoption due to its superior cost-effectiveness and storage capacity. Forward Insights forecasted that QLC market share will expand to 30% by 2025, representing a remarkable acceleration from minimal penetration just two years prior.

Technology advancement enables four bits of data storage per memory cell, substantially increasing areal density compared to conventional TLC implementations. Solidigm's 192-layer QLC NAND architecture achieved areal density of 18.6 gigabits per square millimeter, demonstrating architectural innovations that support continued density scaling. Cost reductions are proving particularly consequential for enterprise and data center applications, with prices declining by approximately 40% annually as QLC and advanced TLC technologies achieve manufacturing scale and economic viability.

Market Restraints

Supply Chain Volatility and Production Capacity Constraints

The NAND flash memory market faces persistent challenges from supply chain disruptions, trade restrictions, and constrained manufacturing capacity that limit production expansion despite robust demand. The semiconductor industry confronts fundamental capacity limitations, as expanding NAND manufacturing facilities require extraordinary capital investment, specialized fabrication equipment, and extended construction timelines exceeding three years. Geopolitical tensions, including international trade restrictions and technology export controls, have created uncertainty regarding long-term supply security for NAND manufacturers and their customers.

Manufacturing facilities operate at elevated utilization rates, creating bottlenecks that extend delivery timelines for customers unable to secure long-term supply agreements. SanDisk and other NAND suppliers have explicitly communicated limited capacity to handle unplanned customer orders, necessitating advance communication and commitment to avoid extended lead times. The cyclical nature of semiconductor demand creates periodic oversupply and undersupply conditions that destabilize pricing and complicate investment planning for equipment manufacturers and component suppliers.

Technical Complexity and Process Node Scaling Challenges

The advancement to progressively smaller manufacturing process nodes for NAND flash presents extraordinary technical challenges, increased complexity, and substantial research and development investments required to sustain density improvements. Scaling to smaller process geometries introduces critical reliability and manufacturing challenges, including increased susceptibility to defects, elevated error rates, and challenges in maintaining data integrity under diverse operating conditions.

The technical expertise required for implementing state-of-the-art NAND flash architectures, including three-dimensional stacking techniques, advanced error-correction algorithms, and specialized controller integration, exceeds the capabilities of many organizations. Smaller producers and less-capitalized competitors struggle to maintain technological parity with industry leaders possessing substantial research and development budgets and manufacturing scale advantages. Additionally, legacy integration challenges persist as organizations maintain older NAND-based systems that complicate transitions to newer technology generations.

Market Opportunities

Automotive Electronics and Advanced Driver-Assistance Systems Expansion

The automotive sector represents an exceptionally compelling growth opportunity for NAND flash memory providers, driven by rapid electrification of powertrains, deployment of advanced driver-assistance systems, and transition toward autonomous vehicle architectures. The automotive memory market is projected to grow from US$ 6.8 billion in 2024 to US$ 18.3 billion by 2033, expanding at a CAGR of 11.6%, substantially exceeding growth rates in traditional consumer electronics markets. According to Micron Technology, a fully autonomous Level 5 vehicle requires approximately 30 times the DRAM capacity and 100 times the NAND flash memory compared to conventional vehicles, reflecting extraordinary data storage requirements for autonomous decision-making algorithms, sensor fusion processing, and real-time vehicle control systems.

Infotainment systems represent the dominant application category within automotive NAND flash consumption, accounting for approximately 80% of total automotive NAND storage market demand, driven by high-resolution multimedia displays, advanced navigation systems, and immersive digital cockpit experiences. Modern automotive applications are transitioning from legacy eMMC interfaces to advanced UFS 4.0 and PCIe NVMe storage solutions, enabling enhanced data throughput for complex virtualized computing environments. Micron Technology announced securing billions of dollars in design wins for automotive-grade memory solutions, validating substantial near-term growth opportunities within this vertical market.

Transition from Hard Disk Drives to Enterprise Solid-State Drives in Data Centers

The fundamental transition from mechanical hard disk drives to solid-state drives in enterprise data center environments represents a transformational opportunity generating massive NAND flash consumption growth. Major cloud service providers and hyperscale data center operators are aggressively shifting toward all-flash storage architectures to support artificial intelligence workload requirements, with QLC-based enterprise SSDs displacing nearline HDDs across active archive, large-scale network-attached storage, and software-defined storage applications. Companies including Pure Storage are procuring NAND flash in unprecedented quantities for all-flash arrays supporting artificial intelligence and machine learning infrastructure.

The cost competitiveness between HDDs and enterprise SSDs has shifted dramatically, with price differentials contracting from over 10-fold to 3-4 times as HDD supply shortages and escalating HDD costs reduce the financial justification for traditional disk-based storage. Advanced QLC NAND-based enterprise SSDs offer superior energy efficiency, significantly lower latency, and reduced cooling requirements compared to mechanical alternatives, delivering compelling return-on-investment justification. Forward Insights anticipates QLC SSDs will capture substantial market share in data center applications through enhanced reliability, performance optimization, and complementary technologies supporting coarse I/O block operations.

Category-wise Insights

Type Analysis

The Triple-Level Cell (TLC) NAND flash technology dominates the market with approximately 38% market share, representing the optimal equilibrium between cost-effectiveness, storage capacity, and data reliability characteristics. TLC technology enables three bits of data storage per memory cell, substantially increasing density compared to conventional Single-Level Cell (SLC) and Multi-Level Cell (MLC) architectures while maintaining acceptable manufacturing yields and data integrity parameters. Organizations universally deploy three-dimensional TLC NAND across consumer electronics, including smartphones, personal computers, and memory storage products, due to the mature technology platform, extensive manufacturing ecosystem, and proven reliability track record.

Quad-Level Cell (QLC) NAND is experiencing explosive growth, the fastest-growing segment in the market, with enterprise QLC adoption expected to reach 35% by 2026, up from 10% in 2023. QLC technology stores 4 bits per cell, enabling extraordinarily high areal density and dramatic cost reduction compared to TLC alternatives. Multi-Level Cell (MLC) NAND is experiencing substantial contraction, with global MLC NAND capacity expected to decline 41.7% year-over-year in 2026 as major manufacturers, including Samsung, exit the segment, redirecting capital toward advanced process technologies. SLC NAND maintains a niche in high-reliability, industrial, automotive, and specialized military applications that require extraordinary data integrity and extended endurance.

Structure Analysis

The Three-Dimensional NAND structure has established overwhelming market dominance, capturing approximately 92% of the market, as organizations universally transition from legacy planar architectures to vertically-stacked memory cell designs. 3D NAND technology addresses fundamental density limitations of planar implementations by vertically stacking memory cells, enabling exceptional storage capacity within compact physical dimensions while reducing per-gigabyte manufacturing costs through economies of scale. Industry-leading NAND manufacturers including Samsung, SK Hynix, Micron, and Kioxia have aggressively invested in 3D NAND manufacturing capacity, representing core strategic differentiation and competitive positioning.

Forward Insights forecasts continued momentum toward higher-layer-count 3D NAND technologies, with next-generation architectures supporting 192-256 stacked layers, enabling continued density escalation. Two-Dimensional (Planar) NAND represents legacy technology accounting for approximately 8% of market share, with production concentrated on legacy products and applications where 3D NAND cost premiums exceed justification. Macronix International, traditionally focused on embedded and specialized memory markets, has maintained modest planar NAND production volumes serving niche industrial, automotive, and high-reliability applications demanding specialized manufacturing characteristics.

Interface Analysis

The PCIe/NVMe interface represents the fastest-growing segment, expanding at extraordinary rates as organizations transition from legacy storage protocols toward modern high-performance interfaces. NVMe utilizes the PCIe architecture enabling data transfer rates exceeding 25 times faster than SATA equivalents, with PCIe 4.0 implementations delivering performance approaching 7,000 MB/s and forthcoming PCIe 5.0 enabling 14 GB/s throughput. NVMe command architecture processes requests 2 times faster than legacy AHCI drivers, while IOPS exceed 2 million per second, representing a 900% improvement over SATA alternatives. Enterprise and data center organizations are aggressively adopting PCIe/NVMe storage solutions, with approximately 85% of laptop manufacturers incorporating NVMe SSDs in mainstream models by 2023.

The SATA interface is experiencing rapid market contraction, with SATA SSD penetration declining to below 10% as consumers and enterprises recognize superior performance and energy-efficiency advantages of NVMe technology. UFS/eMMC interfaces remain important in mobile devices and automotive applications, with UFS 4.0 and emerging UFS 4.1 technologies enabling higher bandwidth for complex virtualized automotive computing environments. Modern automotive infotainment systems are transitioning from legacy eMMC 5.1 toward advanced UFS 4.0 storage interfaces to support high-resolution multi-display environments and sophisticated navigation systems.

Application Analysis

The Smartphone segment continues commanding the largest NAND flash application share at approximately 32%, reflecting the ubiquity of mobile devices and escalating storage requirements for multimedia content and applications. Over one billion smartphones are sold annually globally, with modern devices requiring storage capacities of 128GB and above to accommodate high-resolution photography, 4K/8K video recording, sophisticated mobile gaming, cloud-integrated services, and artificial intelligence-enhanced features. However, the Data Center SSD segment is emerging as the fastest-growing application category, with data center NAND demand now exceeding mobile-device demand as of 2024, representing a fundamental market inflection point.

Enterprise Solid-State Drives for data center and cloud computing infrastructure are experiencing explosive adoption driven by artificial intelligence workload expansion, hyperscale cloud infrastructure investment, and the transition from mechanical storage. Enterprise SSD costs are declining from historically prohibitive levels, making all-flash data center architectures economically viable for broader organizational adoption. Memory Cards and USB Drives represent secondary applications requiring portable storage solutions for personal computing and content distribution. Industrial and Automotive Electronics comprise a rapidly growing segment, with the automotive memory market expanding at 11.6% CAGR through 2033, driven by autonomous vehicle development, advanced driver-assistance systems, infotainment sophistication, and electrification requirements.

Regional Insights

North America NAND Flash Memory Trends

North America maintains regional dominance with approximately 40.2% of global market share, supported by the concentration of major technology companies, hyperscale cloud service providers, and advanced manufacturing facilities. The United States hosts headquarters of Intel, Micron Technology, and Western Digital, key NAND flash manufacturers with substantial domestic manufacturing capacity and research and development operations. Amazon Web Services, Microsoft Azure, Google Cloud, and Meta operate extensive data center infrastructures across the region, generating extraordinary demand for enterprise-grade NAND flash storage solutions. North American data center infrastructure investments have accelerated dramatically, with hyperscale operators and colocation facilities constructing new facilities at unprecedented pace to support artificial intelligence workload expansion.

The United States market is characterized by rapid adoption of advanced 3D NAND technology, with PCIe NVMe interfaces becoming standard across consumer and enterprise applications. Major NAND manufacturers maintain competitive pricing for global tenders through manufacturing scale advantages and established customer relationships. The region benefits from mature digital infrastructure, substantial enterprise investment budgets, and leadership in artificial intelligence and cloud computing technologies. Regulatory frameworks and intellectual property protections support extensive research and development investments by NAND manufacturers and system integrators. Market Research suggests significant pricing power remains concentrated among North American NAND suppliers, enabling premium positioning for advanced technology implementations and enterprise solutions.

Europe NAND Flash Memory Trends

Europe represents a substantial regional market characterized by significant data center infrastructure, strong enterprise IT spending, and emphasis on regulatory compliance and sustainable manufacturing practices. Major manufacturing hubs in Germany, France, and the United Kingdom maintain sophisticated digital infrastructure and substantial investments in cloud computing and enterprise data storage solutions. European organizations are increasingly adopting enterprise-grade SSD solutions across manufacturing, financial services, and public-sector institutions that require reliable, high-performance storage infrastructure. The region has established stringent regulatory requirements affecting semiconductor manufacturing, including environmental sustainability mandates and supply chain transparency obligations.

European NAND flash consumption reflects the region's balanced emphasis between consumer electronics and enterprise infrastructure, with particular strength in industrial applications, automotive electronics, and critical infrastructure sectors. Regulatory harmonization initiatives across European Union member states are establishing standardized procurement requirements and sustainability criteria affecting NAND flash specifications and manufacturing practices. The region demonstrates relatively conservative adoption of emerging technologies compared to North American markets, with organizations prioritizing proven reliability and long-term supply stability over cutting-edge performance. European technology vendors and system integrators maintain substantial market share through established relationships with enterprise customers and deep expertise in regulatory compliance requirements.

Asia Pacific NAND Flash Memory Trends

Asia Pacific is emerging as the fastest-growing regional market, driven by rapid semiconductor manufacturing expansion, escalating consumer electronics demand, and government-backed digitization initiatives. China has established itself as the world's largest producer of NAND flash memory, leveraging substantial government support, manufacturing scale advantages, and emerging domestic demand for consumer electronics and data storage solutions. Major NAND manufacturers, including Samsung, SK Hynix, Kioxia, and Micron, maintain extensive manufacturing facilities throughout the Asia Pacific, serving local demand and exporting to global markets. Kioxia announced plans to double NAND flash production capacity by fiscal 2029, representing extraordinary commitment to capacity expansion within the region.

India is experiencing particularly rapid growth in NAND flash consumption, driven by expanding smartphone manufacturing, escalating cloud computing adoption, and government initiatives promoting digital transformation across sectors. ASEAN countries including Vietnam, Thailand, and Malaysia are attracting substantial NAND manufacturing investments from global semiconductor companies seeking to diversify manufacturing footprints beyond China. The region benefits from significant cost advantages in semiconductor manufacturing compared to developed markets, enabling competitive pricing and attractive investment returns for capital-intensive NAND production facilities. Government policies supporting semiconductor manufacturing, research and development investments, and supply chain diversification are accelerating the expansion of NAND flash capacity and ecosystem development across the Asia Pacific, positioning the region for continued market share growth.

Competitive Landscape for the NAND Flash Memory Market

The NAND Flash Memory market exhibits substantial consolidation among major technology companies, with the top four manufacturers Samsung Electronics, SK Hynix, Kioxia, and Micron Technology collectively commanding approximately 92% of global NAND flash production capacity. Samsung Electronics dominates market competition, leveraging exceptional manufacturing scale, advanced process technology capabilities, and comprehensive product portfolio spanning consumer, enterprise, and specialized applications. SK Hynix maintains substantial competitive positioning through differentiated technology implementations, cost-competitive manufacturing, and strategic partnerships with system integrators. Kioxia and Western Digital execute joint venture manufacturing arrangements, optimizing capital efficiency while maintaining technological parity with market leaders.

Micron Technology differentiates through specialized focus on high-reliability and automotive applications, securing substantial design wins with leading vehicle manufacturers. Competitive strategies emphasize continuous investment in research and development for advanced process nodes, manufacturing scale expansion, and specialized product development addressing enterprise and automotive customer requirements. Market leaders compete vigorously with technology differentiation, product performance characteristics, manufacturing scale advantages, and cost-competitiveness. Emerging producers from China, including Changxin Memory and Yangtze Memory Technologies, are investing substantially in NAND flash manufacturing capacity, representing potential future competitive threats as indigenous technology capabilities mature.

Key Market Developments

- In December 2025, Kioxia Achieves Exceptional QoQ Growth of 33.1% in Q3 2025 - Kioxia Holdings Corporation reported extraordinary quarterly revenue growth driven by exceptional enterprise SSD demand and QLC NAND product sales, with market analysts projecting total NAND flash prices will increase 20-25% further through continued supply constraints.

- In November 2025, Western Digital Announces 50% NAND Flash Price Increase - Western Digital Corporation implemented substantial NAND flash pricing adjustments reflecting supply-demand imbalances and exceptional enterprise customer demand for high-capacity SSD solutions supporting artificial intelligence infrastructure.

- In June 2025, Kioxia Announces Mid-to-Long-Term Capacity Expansion Plan - Kioxia Holdings unveiled plans to double NAND flash production capacity by fiscal 2029, demonstrating strategic commitment to capturing market share within the rapidly expanding data center and artificial intelligence storage markets.

Companies Covered in NAND Flash Memory Market

- ADATA

- Cypress Semiconductor

- Greenliant Systems

- Infineon Technologies

- Intel

- ISSI

- Kingston Technology

- Kioxia

- Macronix International

- Micron Technology

- Netlist

- Phison Electronics

- Powerchip Semiconductor

- Samsung Electronics

- Sandisk

Frequently Asked Questions

The global NAND Flash Memory market is projected to reach US$ 85.3 billion by 2033, growing from US$ 60.2 billion in 2026 at a robust CAGR of 5.1%, driven by exponential artificial intelligence data center expansion, accelerated enterprise SSD adoption, and advancement of three-dimensional NAND technologies.

Primary demand drivers include extraordinary artificial intelligence data center infrastructure investments by major technology companies, fundamental transition from mechanical hard disk drives to enterprise SSDs with superior performance and energy efficiency, smartphone manufacturing and multimedia storage requirements with over one billion annual units sold, automotive electronics expansion driven by autonomous vehicle development requiring 100 times greater NAND flash than conventional vehicles, and continuous advancement in three-dimensional NAND technology enabling cost reduction and capacity expansion.

Data center and enterprise solid-state drives represent the fastest-growing application segment, with data center NAND demand now exceeding smartphone demand as of 2024, driven by exceptional artificial intelligence workload expansion, hyperscale cloud provider investment in infrastructure, and accelerated replacement of mechanical hard disk drives with high-performance, energy-efficient flash storage solutions.

North America leads the global NAND Flash Memory market with approximately 40.2% market share, supported by concentration of major NAND manufacturers including Intel, Micron Technology, and Western Digital, hyperscale cloud service providers including Amazon Web Services, Microsoft, Google, and Meta, and extensive data center infrastructure investments supporting artificial intelligence and cloud computing workloads.

Automotive electronics sector expansion represents the principal market opportunity, projected to grow from US$ 6.8 billion in 2024 to US$ 18.3 billion by 2033 at 11.6% CAGR, driven by autonomous vehicle development, advanced driver-assistance systems requiring real-time processing, electric vehicle battery management systems, and infotainment sophistication accounting for 80% of automotive NAND flash demand.

Leading market players include Samsung Electronics commanding approximately 32% market share with 20.7% revenue growth; SK Hynix controlling 18% market share with 5.8% growth; Kioxia Holdings achieving 14% market share with exceptional 28.1% revenue growth and plans to double capacity by fiscal 2029; Micron Technology securing substantial automotive design wins; and Western Digital implementing 50% price increases reflecting supply constraints.