- Automotive Components & Materials

- Motor Driver IC Market

Motor Driver IC Market Size, Share, and Growth Forecast, 2026 - 2033

Motor Driver IC Market by Motor Type (Brushed DC Motor, Brushless DC (BLDC) Motor, Stepper Motor), Technology (MOSFET, IGBT), Voltage Range (Low Voltage (Up to 48V), Medium Voltage (48V - 240V), High Voltage (Above 240V)), Vertical and Regional Analysis for 2026 - 2033

Motor Driver IC Market Size and Trends

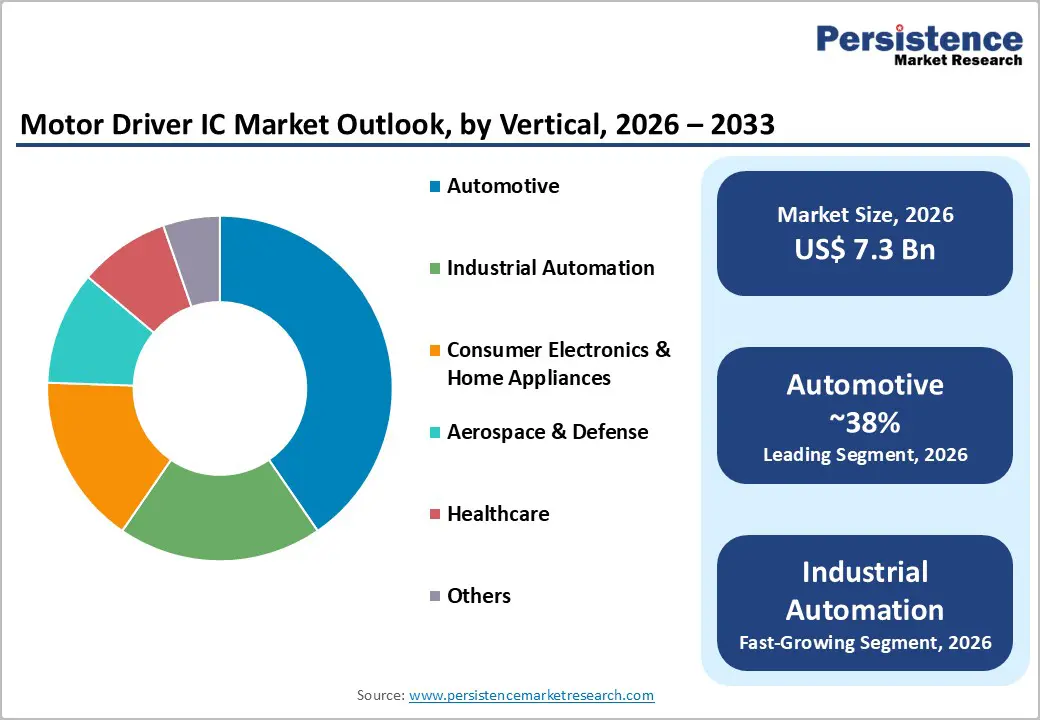

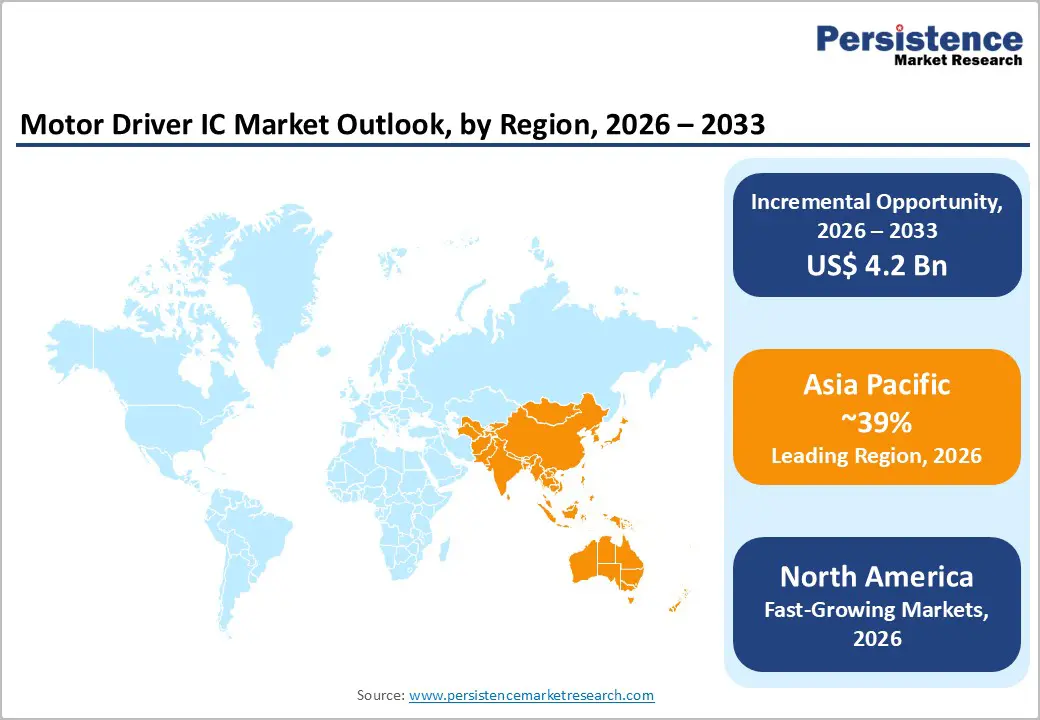

The global motor driver ic market size is projected to rise from US$7.3 Bn in 2026 to US$11.5 Bn by 2033. It is anticipated to witness a CAGR of 6.7% during the forecast period from 2026 to 2033, driven by the widespread adoption of automation in industrial systems, the rapid electrification of vehicles across passenger and commercial segments, and the rising demand for compact, energy-efficient motor control solutions in consumer and healthcare devices.

Governments and regional authorities are also pushing for higher energy-efficiency standards in appliances and industrial equipment, further strengthening the need for advanced motor driver integrated circuits that regulate speed, torque, and direction with minimal losses.

Key Industry Highlights:

- Leading Motor Type: Brushless DC (BLDC) motors dominate with over 42% market share in 2026, valued at more than US$ 3.1 Bn, driven by rising demand for energy-efficient, low-noise, and maintenance-free solutions across electric vehicles, robotics, drones, and consumer electronics. Stepper motors are the fastest-growing, supported by increasing adoption in precision-driven applications such as 3D printing, CNC machinery, and medical devices.

- Leading Technology: MOSFET-based motor driver ICs lead with over 70% market share in 2026, valued at more than US$ 5.1 Bn, due to superior switching efficiency, compactness, and thermal performance. IGBT technology is gaining traction in high-power applications such as EV traction systems, industrial drives, and renewable energy installations.

- Leading Voltage Range: Medium voltage (48V-240V) dominates with over 45% share in 2026, valued at more than US$ 3.3 Bn, owing to its optimal balance of performance, cost, and safety across automotive and industrial applications. High voltage (above 240V) is the fastest-growing segment, expanding at a CAGR of 10.3%, driven by increasing demand in industrial motors, large EVs, and renewable energy systems.

- Leading Vertical: Automotive holds the largest share at over 38% in 2026, valued at more than US$ 2.8 Bn, supported by rapid electrification, increasing integration of motor control systems, and stringent emission norms. Industrial automation is the fastest-growing vertical, fueled by the rise of smart factories, robotics, and demand for high-efficiency motion control systems.

- Leading Region: Asia Pacific leads with over 42% market share in 2026, valued at more than US$ 3 Bn, driven by strong manufacturing ecosystems, EV adoption, and consumer electronics demand. North America holds the largest share, at over 23%, driven by advanced semiconductor innovation and EV incentives. The Asia Pacific region also remains the fastest-growing, thanks to rapid industrialization and government-backed electrification initiatives.

| Key Insights | Details |

|---|---|

| Motor Driver IC Market Size (2026E) | US$7.3 Bn |

| Market Value Forecast (2033F) | US$11.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

DRO Analysis

Driver - Expansion of Drones, Robotics, and e-Mobility Platforms

The rapid proliferation of drones, service robots, and e-mobility platforms is a key growth driver, as each platform relies on multiple small, high-efficiency motor controllers. For example, consumer and industrial drones typically integrate 4-channel full-bridge motor driver ICs to control brushless propeller motors, enabling precise speed regulation and extended battery life. In last-mile delivery drones and autonomous inspection robots, compact <48 V motor driver ICs with integrated PWM and current sensing are becoming standard, driven by the need for low weight, low EMI, and high reliability. As governments permit expanded urban drone operations and companies scale warehouse-automation robots, the per-unit motor-IC count in these systems is expected to rise further, reinforcing demand for small-form-factor, high-efficiency motor driver ICs.

Rise of Energy-Efficiency Regulations and MEPS Standards

Stringent Minimum Energy Performance Standards (MEPS) and global motor-driven-unit regulations are pushing manufacturers to replace legacy brushed-DC motors with high-efficiency BLDC and servo systems, boosting demand for advanced motor driver ICs. In the United States, the Department of Energy (DOE) has progressively tightened motor-efficiency rules for HVAC and industrial-pump systems, directing OEMs to adopt variable-speed motor-drive architectures that depend on MOSFET-based motor driver ICs with sensorless control. Countries such as China and India are aligning with or surpassing these standards through motor-efficiency labelling programs, which incentivize the replacement of millions of low-efficiency motor units with BLDC-based systems supported by modern motor driver ICs.

Restraint - Supply Chain Volatility and Component Shortages

The motor driver IC remains exposed to semiconductor-supply-chain disruptions, including fluctuations in wafer-fabrication capacity, shortages of power MOSFETs and gate-driver components, and logistics bottlenecks. During the 2020-2023 period, global automotive and industrial-electronics manufacturers faced extended lead times for motor driver ICs, with some vendors reporting delivery windows of up to 52 weeks for critical gate-driver devices. Such volatility forces design engineers to redesign entire motor-control subsystems or delay product launches, which temporarily slows down demand growth. Geopolitical tensions and export-control regimes around certain semiconductor-fabrication technologies have led to localized capacity constraints, particularly for high-voltage, automotive-qualified motor driver ICs that require stringent safety certifications.

High Design Complexity and System-Integration Costs

Integrating motor driver ICs into complex systems, especially in automotive, aerospace, and medical applications requires significant engineering effort, rigorous validation, and compliance with domain-specific standards such as ISO 26262, IEC 60601, and DO-178C/DO-254. Developers must account for EMI/EMC, thermal dissipation, fault-diagnostic capabilities, and functional-safety requirements, which drive up R&D and testing costs. For example, advanced BLDC motor driver ICs with embedded current sensing, overcurrent protection, and thermal shutdown features often require custom firmware and careful PCB layout to avoid oscillation and shoot-through conditions. Smaller OEMs that lack in-house power-electronics expertise prefer turn-key modules over discrete motor driver ICs, which limit the incremental unit growth of standalone ICs in price-sensitive segments.

Opportunity - Rising Penetration in Renewable Energy and Smart Grid Systems

Solar panel-tracking systems, wind-turbine-pitch actuators, and substation-auxiliary-drive systems increasingly rely on motor driver ICs to optimize angle control, load-matching, and maintenance-automation. According to a study, global solar-tracking deployments have grown by roughly 10-20% per year since 2020, with each tracking array requiring several stepper or BLDC motor driver ICs to adjust panel orientation based on real-time irradiance data. Semiconductor players are developing high-voltage motor driver ICs and integrated gate-driver solutions that support 48-600 V DC systems, enabling efficient motor control in off-grid, microgrid, and utility-scale installations. As governments push renewable-energy-share targets and utilities invest in grid automation, the motor driver IC market is gaining traction in a high-margin, long-lifecycle segment that values reliability and precise motion control.

Emergence of AI-Driven and Predictive Motor Control Platforms

The convergence of artificial intelligence (AI), edge-computing, and motor-control algorithms is creating a new opportunity for intelligent motor driver ICs that support predictive maintenance, adaptive control, and self-diagnosis. Industrial and automotive OEMs are embedding on-chip intelligence into motor driver ICs to enable real-time adjustment of torque, vibration-suppression, and anomaly detection, which reduces downtime and energy consumption. According to a study, AI-enabled motor control improves system efficiency by 5-10% while reducing mechanical wear and maintenance costs by up to 10%-20%, making it attractive for high-uptime industrial environments and mission-critical healthcare devices. As edge-AI accelerators and low-power computing platforms become more accessible, motor driver IC manufacturers differentiate by offering AI-ready motor control ICs that combine sensor integration, on-chip analytics, and secure communication interfaces tailored for Industry 4.0, smart vehicles, and connected appliances.

Category-wise Analysis

Motor Type Insights

Brushless DC (BLDC) Motor dominates the market, capturing more than 42% market share in 2026 with a value exceeding US$ 3.1 Bn, due to increasing demand for energy-efficient, low-noise, and maintenance-free motors in electric vehicles, robotics, drones, and consumer electronics. Their precise speed control, high torque-to-weight ratio, and long operational life make them highly suitable for modern automation and mobility solutions.

Stepper Motor is expected to grow at a significant rate due to their precision positioning capabilities, making them essential for 3D printers, CNC machines, and automated medical devices. The rising trend toward industrial automation and smart manufacturing is significantly boosting the adoption of stepper motor driver ICs.

Technology Insights

MOSFET holds over 70% market share in 2026, with a value exceeding US$ 5.1 Bn, due to their high switching speed, low on-resistance, and energy-efficient performance. They are widely preferred in applications demanding compactness, reliability, and minimal heat generation, such as automotive subsystems, consumer electronics, and industrial machinery.

IGBT is expected to grow rapidly due to their high voltage and current handling capabilities, which make them suitable for electric vehicle traction systems, industrial motor drives, and renewable energy installations. As efficiency, thermal management, and reliability become key factors, more industries are choosing the right technology based on operational demands and application voltage.

Voltage Range Insights

Medium Voltage (48V - 240V) commands the largest market share at over 45% in 2026, with a value exceeding US$ 3.3 Bn as it provides an optimal balance between performance, safety, and cost across automotive, industrial, and home appliance applications. It is ideal for electric mobility solutions such as e-bikes, scooters, and small EVs, as well as moderate-power industrial automation systems.

High Voltage (Above 240V) is expected to grow at a CAGR of 10.3% driven by industrial motors, large-scale EVs, and renewable energy systems demanding high power and efficiency. Infrastructure upgrades, increasing energy consumption, and government incentives for electrification are further accelerating demand for high-voltage motor drivers.

Vertical Insights

Automotive holds over 38% market share in 2026, with a value exceeding US$ 2.8 Bn, due to rising adoption of electric and hybrid vehicles and the need for efficient motor control in traction, steering, braking, and HVAC systems. Automotive OEMs are integrating motor driver ICs to improve energy efficiency, reduce emissions, and ensure vehicle safety and reliability.

Industrial Automation is expected to grow significantly, fueled by smart factories, robotics, and process optimization initiatives. Industries increasingly demand high-precision, reliable, and energy-efficient motor control solutions to reduce downtime, improve productivity, and comply with global energy and safety standards.

Regional Insights

North America Motor Driver IC Market Trends

North America holds over 23% share in 2026, reaching US$ 1.7 Bn value. The U.S. remains a global leader in motor driver IC adoption, particularly in the automotive and consumer electronics sectors. Government incentives promoting electric vehicles and energy-efficient devices are fueling demand. Companies are actively developing next-gen MOSFET and IGBT driver ICs tailored for North American OEMs. The region benefits from a mature innovation ecosystem with advanced semiconductor fabrication facilities, accelerating the deployment of BLDC and stepper motor drivers in both industrial automation and aerospace. According to a study, over 60% of EV controllers in the U.S. use MOSFET-based motor drivers, highlighting technology preference and regulatory alignment.

Asia Pacific Motor Driver IC Market Trends

Asia Pacific holds over 42% share in 2026, reaching over US$ 3 Bn value, and is expected to grow rapidly, driven by manufacturing expansion, EV adoption, and consumer electronics demand. China continues to dominate low-voltage and medium-voltage IC deployment for EVs, home appliances, and industrial automation. Japan and India are witnessing increased stepper motor driver adoption in precision manufacturing and robotics. The presence of local semiconductor fabs and government support for electrification and automation projects is strengthening regional growth.

Europe Motor Driver IC Market Trends

Europe is expected to hold more than 20% share by 2026, due to stringent emissions regulations and increasing EV penetration, particularly in Germany, France, and the U.K. Automotive manufacturers are integrating high-efficiency BLDC and stepper motor drivers to meet environmental standards. Companies have expanded R&D initiatives in Germany for next-generation automotive ICs. Harmonized regulations under the European Union and incentives for energy-efficient industrial systems are boosting adoption in industrial automation. According to a study, BLDC motor adoption in European smart factories has grown by over 20 - 25% in the past three years, reflecting strong regional dynamics.

Competitive Landscape

The global Motor Driver IC market is moderately consolidated, with a handful of key players dominating due to strong portfolios and advanced R&D capabilities. Companies focus on product differentiation through energy-efficient MOSFET and IGBT technologies, integrated IoT-enabled ICs, and high-voltage solutions for EVs and aerospace. Emerging business models include custom IC solutions, licensing, and strategic partnerships with automotive OEMs. The competitive landscape emphasizes innovation, quality, and regulatory compliance as core differentiators.

Key Developments:

- In February 2026, STMicroelectronics launched its STSPIN9P series of 75V motor-driver ICs, designed to support scalable industrial drive applications up to 500W across multiple motor types. The new half-bridge and full-bridge devices enable simplified system design with integrated regulators and high-efficiency operation, targeting industrial automation, robotics, and appliances.

- In January 2026, Oriental Motor launched its first stainless steel brushless DC motor under the BLE2 Series, designed for high-pressure, high-temperature washdown environments with IP67/IP69K protection and corrosion-resistant construction.

Companies Covered in Motor Driver IC Market

- Texas Instruments

- Infineon Technologies AG

- STMicroelectronics

- ON Semiconductor

- NXP Semiconductors

- ROHM Semiconductor

- TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION

- Analog Devices, Inc.

- Renesas Electronics

- Microchip Technology

- Monolithic Power Systems

- Allegro MicroSystems

- Others

Frequently Asked Questions

The global motor driver IC market is projected to be valued at US$7.3 Bn in 2026.

Increasing demand for energy-efficient systems and miniaturized electronic components is accelerating the adoption of advanced motor driver ICs across industries are key driver of the market.

The market is expected to witness a CAGR of 6.7% from 2026 to 2033.

Advancements in AI-driven automation and energy-efficient motor technologies are creating strong growth opportunities.

Texas Instruments, Infineon Technologies AG, STMicroelectronics, ON Semiconductor, NXP Semiconductors, ROHM Semiconductor, TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION are among the leading key players.