- Automotive Components & Materials

- Mid-Lift Axle Market

Mid-Lift Axle Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Mid-Lift Axle Market by Product Type (Mechanical, Hydraulic, Electric, Air Suspension), Vehicle Type (Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Off-Road Vehicles, Agricultural Machinery), End-User (Logistics & Transportation, Construction, Commercial Vehicles), and Regional Analysis for 2026-2033

Mid-Lift Axle Market Share and Trends Analysis

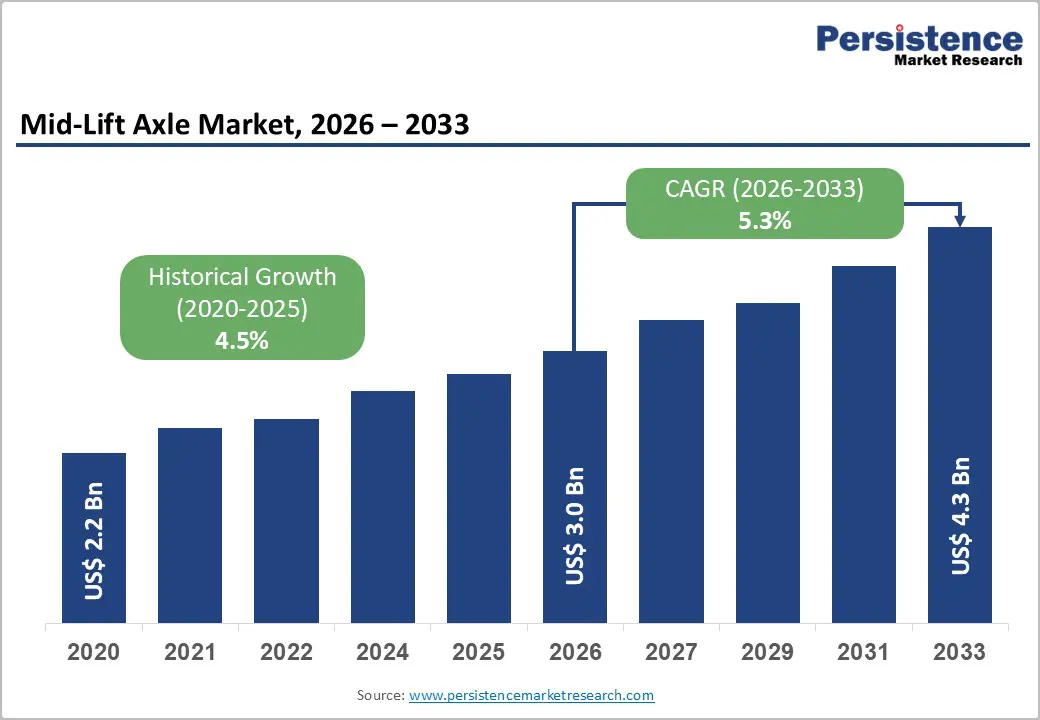

The global mid-lift axle market size is likely to be valued at US$ 3.0 billion in 2026, and is projected to reach US$ 4.3 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026−2033. This sustained expansion is underpinned by the rapid modernization of commercial vehicle fleets, stringent axle load regulations governing road infrastructure protection, and mounting demand for fuel-efficient, load-adaptive transportation solutions across diverse end-use industries worldwide.

Primary growth catalysts include expanding freight logistics networks, infrastructure development programs in emerging economies, and the progressive electrification of heavy commercial vehicles. Technological integration spanning automatic load sensing, telematics-enabled axle management, and lightweight composite materials continues to redefine product value propositions and extend addressable market boundaries.

Key Industry Highlights

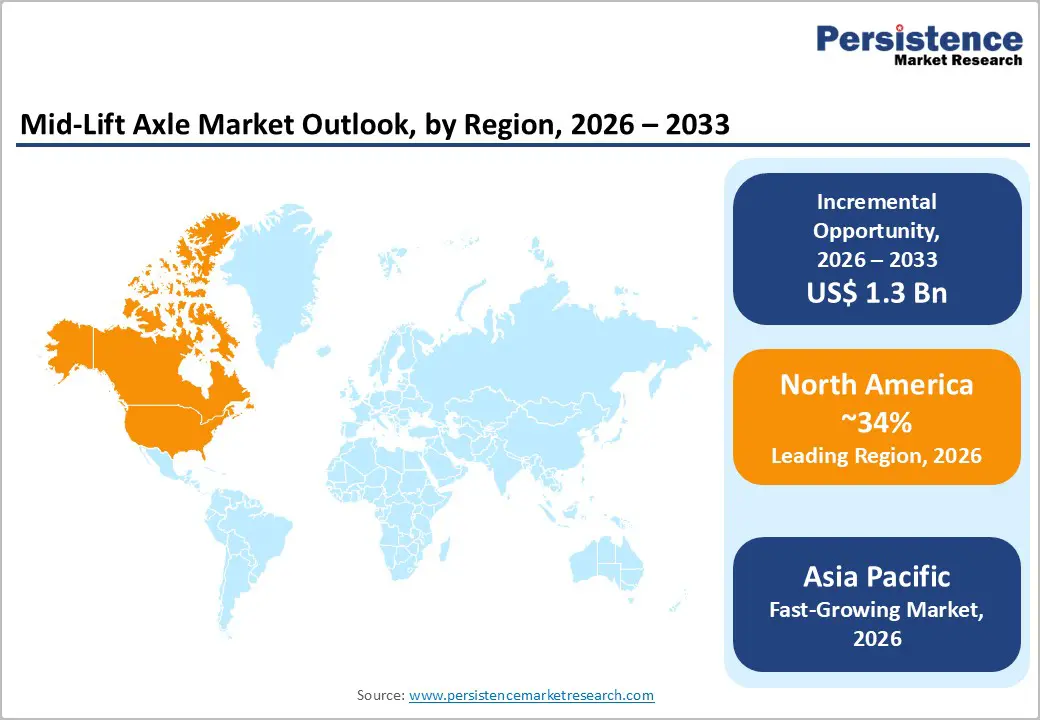

- Dominant Region: North America is expected to command about 34% market share in 2026, supported by its vast fleet of heavy commercial vehicles.

- Fastest-growing Region: The Asia Pacific market is set to be the fastest-growing during the forecast period, due to the massive industrial output and commercial vehicle production.

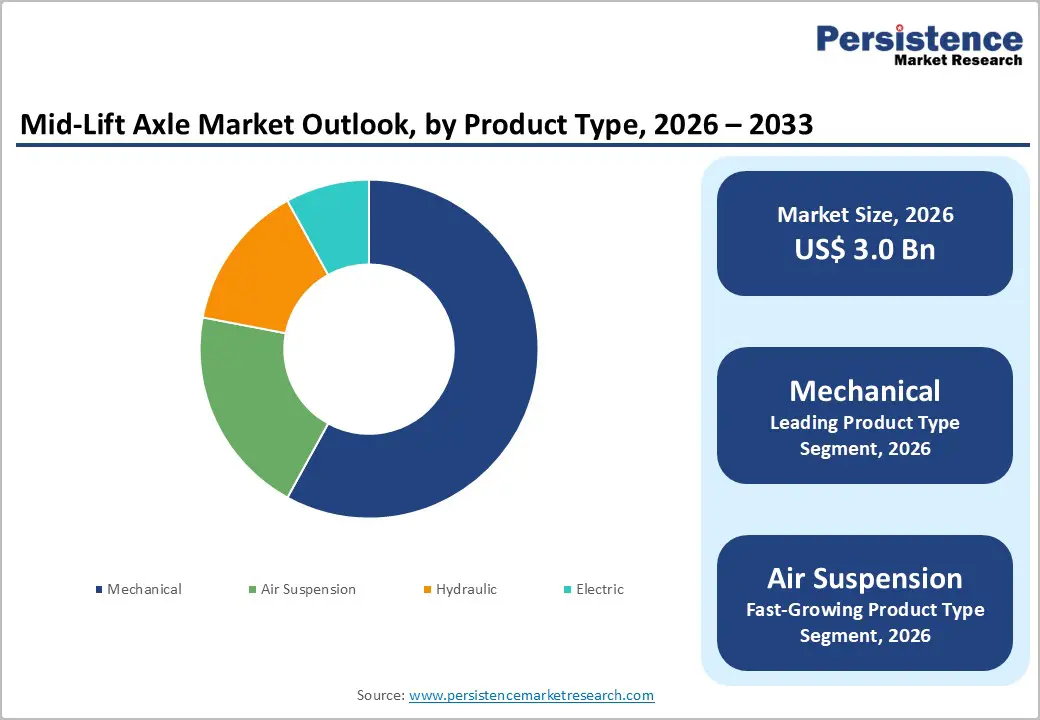

- Leading & Fastest-growing Product Type: Mechanical currently dominates the product type segment, commanding approximately 58% of total market revenue, while air suspension is likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing Vehicle Type: Heavy commercial vehicles (HCVs) represent the dominant segment, capturing approximately 68% of market revenue share in 2026, with light commercial vehicles (LCVs) expected to be the fastest-growing over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

| Mid-Lift Axle Market Size (2026E) | US$ 3.0 Bn |

| Market Value Forecast (2033F) | US$ 4.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

DRO Analysis

Stringent Axle Load Regulations and Road Infrastructure Protection Mandates

Governments in major markets enforce stricter axle load limit regulations. They aim to safeguard road infrastructure and cut maintenance costs. In the United States (U.S.), the Federal Highway Administration (FHWA) sets a maximum single-axle load of 20,000 pounds and tandem-axle limits of 34,000 pounds through the Federal Bridge Formula. The European Union (EU) applies Directive 96/53/EC, with later updates, to restrict truck axle loads to 11.5 tonnes per non-driving axle. Fleet operators invest in mid-lift axle setups to meet these rules. These systems distribute payloads evenly across axles. Operators raise the mid-lift axle during lighter loads. This practice avoids overload fines and extends vehicle life.

Regulators will continue to tighten these standards in the coming years. They respond to rising freight volumes and aging roadways. Fleet managers adopt mid-lift axles to ensure full compliance. Such configurations optimize weight distribution during varied operations, such as long-haul trips or urban deliveries. Manufacturers innovate designs that integrate seamlessly with modern suspensions. These advancements enhance stability and fuel efficiency without compromising capacity. Businesses gain a competitive edge by reducing downtime from inspections. They also lower risks tied to regulatory penalties. Over time, mid-lift axles will become standard in heavy-duty fleets. This shift supports sustainable transport practices. Governments promote these technologies through incentives. Fleet operators prepare for future mandates by upgrading equipment now.

Commercial Vehicle Fleet Modernization and Electrification Trends

The global commercial vehicle sector undergoes a major transformation toward electrification and autonomous operations. Manufacturers develop electric and hybrid heavy-duty trucks that demand advanced load handling. Mid-lift axles with electronic controls manage weight precisely to extend driving range and protect battery health. Fleet operators integrate these systems into vehicles for better performance during daily routes. Suppliers innovate designs that adjust axle positions automatically based on cargo levels. This approach boosts overall efficiency in transport networks. Digital platforms enhance this trend by linking axle sensors to telematics systems. Companies such as Trimble and Geotab provide software that monitors loads in real time.

Vehicles respond instantly to changes, such as shifting payloads on highways or city streets. Original equipment manufacturers (OEMs) incorporate these features into production lines worldwide. They ensure compatibility with autonomous driving tech that predicts load shifts. In the future, fleets will rely on such integrated solutions to cut energy use and maintenance needs. Operators gain insights from data analytics to plan routes more smartly. This combination drives down operational costs over time. Suppliers position themselves as key partners in the supply chain. They develop durable components suited for high-voltage environments. Electrification accelerates the adoption of smart axles across regions. Businesses prepare for regulatory pushes on zero-emission transport. Mid-lift technologies evolve to support longer hauls without frequent recharges. The sector advances toward fully connected, sustainable operations that redefine logistics standards.

Supply Chain Vulnerabilities and Raw Material Price Volatility

Mid-lift axle production relies heavily on raw materials such as steel and aluminum. Suppliers face ongoing price swings due to global trade tensions and energy market shifts. Manufacturers secure long-term contracts to stabilize costs. They also explore alternative alloys that maintain strength while reducing expenses. Fleet buyers negotiate bulk deals to share risks with producers. Companies diversify sourcing from multiple regions to avoid single-point failures. This strategy strengthens resilience against sudden disruptions in commodity markets. Electronic components add further challenges to the supply chain. Electronic control units (ECUs) require semiconductors that experience periodic shortages from chip fabrication delays. Producers stockpile critical parts and partner with tech firms for priority access.

They integrate software updates to simplify hardware needs over time. Fleet operators face delays in vehicle assembly as a result. Managers plan procurement to align with production timelines. In the future, makers will adopt additive manufacturing for faster prototyping. This method cuts lead times during component scarcity. Businesses build buffer inventories to protect delivery schedules. Supply chain teams use predictive analytics to forecast bottlenecks early. Manufacturers shift toward regional hubs to shorten transport routes. These steps ease margin pressures and support steady output. Operators mitigate procurement uncertainties through flexible leasing options. The industry evolves with dual-sourcing practices that balance cost and reliability. Producers invest in vertical integration to control key inputs directly.

High Initial Capital Investment and Complex Retrofitting Requirements

Small and medium-sized fleet operators hesitate to adopt mid-lift axle systems due to high initial investments. These setups demand substantial funds for air suspension components, electronic controls, and professional fitting. Operators weigh these expenses against immediate operational gains. Manufacturers offer modular designs that simplify integration into standard chassis. Fleet managers explore financing plans to spread costs over time. Suppliers develop basic versions suited for budget constraints in developing regions. This flexibility encourages gradual uptake among smaller businesses. Teams assess total ownership costs, including fuel savings and downtime reduction. Operators prioritize vehicles with high mileage to maximize returns from upgrades.

Retrofitting current trucks poses extra hurdles for widespread use. Engineers address frame alignment, brake adjustments, and compliance checks during modifications. Authorities require fresh approvals to verify safety standards after changes. They also provide digital guides for self-diagnosis of fit issues. In the future, producers will standardize mounting points across models for quicker swaps. Fleets will benefit from plug-and-play kits that cut labor needs. Managers turn to government subsidies for infrastructure upgrades to offset outlays. Suppliers innovate lighter materials to lower transport fees for remote sites. This evolution eases entry barriers over time. Businesses build maintenance networks to support long-term reliability. Operators gain confidence through pilot programs that prove payback periods. The sector advances with collaborative financing from banks focused on transport efficiency.

Integration of IoT and Predictive Maintenance Capabilities

Mid-lift axle systems gain transformative potential through embedded Internet of Things (IoT) sensors and predictive analytics. Manufacturers integrate these technologies to monitor loads instantly and detect component wear early. Systems alert operators to issues before breakdowns occur. Fleets schedule maintenance proactively, which minimizes unplanned stops. Suppliers design platforms that connect axles to central dashboards for remote oversight. This setup improves safety on routes with variable payloads. Companies offer upgrades that retrofit older units with smart modules. Operators access data via mobile apps to optimize daily decisions. Producers partner with software firms to refine algorithms over time.

Advanced features create high-value revenue streams for axle makers. They charge more for connected versions due to enhanced reliability and uptime. Businesses launch subscription services for ongoing analytics and diagnostics. OEMs license these tools to vehicle builders for seamless integration. Aftermarket support grows through over-the-air updates that extend product life. Fleets reduce total costs by avoiding major repairs via early warnings. Suppliers differentiate offerings with customizable dashboards for specific industries, such as logistics or construction. In the future, fully integrated ecosystems will link axles to autonomous controls. This evolution supports zero-downtime operations in electrified fleets. Manufacturers secure long-term contracts with data-sharing agreements.

Policy-Driven Infrastructure Investment in Developed Economies

Major economies launch massive public infrastructure programs. These initiatives boost demand for commercial vehicles and axle systems. The Infrastructure Investment and Jobs Act of the U.S. funds extensive road and bridge projects. This effort sustains heavy freight transport across key routes. The EU enforces the Trans-European Transport Network (TEN-T) Regulation. Authorities aim to complete core network corridors. Freight operators move larger volumes to support construction timelines. Governments coordinate with logistics firms to ensure material delivery. Planners prioritize durable vehicles for rugged project sites.

These policies spark prolonged procurement for advanced mid-lift axles. Manufacturers supply high-capacity systems that meet strict load rules. Fleet owners upgrade trucks to handle increased payloads efficiently. Suppliers ramp up production to match rising orders from contractors. Regional hubs emerge to serve local build programs. Businesses secure multi-year contracts with OEMs. Operators integrate axles that adjust for varied terrains and weights. Policy-makers link funding to emission standards, favoring efficient designs. Authorities will expand these networks further. They respond to trade growth and urbanization pressures. Producers innovate modular axles for quick fleet adaptations. Logistics firms gain an edge through reliable uptime during peak construction phases. Governments foster public-private partnerships to accelerate rollout.

Category-wise Analysis

Product Type Insights

Mechanical currently dominates the product type segment, commanding approximately 58% of total market revenue in 2026, due to its robust construction and affordability. Operators prefer them in heavy-duty applications such as construction and logistics, where they endure harsh conditions with minimal upkeep. These systems use simple mechanisms for reliable lifting, suiting cost-sensitive fleets in regions like North America and Europe. Their dominance persists as they align with regulatory weight limits without complex electronics. Market reports highlight mechanical types capturing over half the volume, driven by established supply chains and OEM integrations.

Air suspension is likely to be the fastest-growing segment during the 2026-2033 forecast period, propelled by superior adjustability and fuel savings during unloaded travel. They gain traction in transportation sectors for smooth handling and compliance with strict axle regulations. Advanced pneumatic controls enable precise load distribution, appealing to modern fleets focused on efficiency. Innovations in materials reduce weight further, enhancing appeal in Asia-Pacific markets. This segment outpaces others through integration with telematics for real-time management.

Vehicle Type Insights

HCVs represent the dominant segment, capturing approximately 68% of the market revenue share in 2026, owing to their essential need for load optimization in multi-axle setups. High revenue per axle assembly reinforces this position. Construction haulage, bulk liquid transport, and intermodal container logistics generate steady demand. HCVs benefit from robust ties with OEMs. Fleets replace axles frequently to maintain performance. Large operators increasingly adopt telematics for axle management. These systems enable real-time monitoring and adjustments. Operators optimize payloads while complying with weight regulations. HCV dominance persists through reliable supply chains and technological upgrades. This segment captures the largest share through proven efficiency in demanding applications.

LCVs are expected to be the fastest-growing segment over the 2026-2033 forecast period. Refuse collection vehicles, concrete mixers, and municipal utility trucks drive this expansion. Operators favor mid-lift axles for precise weight control in urban operations. These vehicles navigate tight streets with variable loads daily. Manufacturers tailor systems for frequent stop-start cycles. Fleets achieve better stability and reduced tire wear as a result. Urbanization accelerates demand in growing cities worldwide. Local governments upgrade utility fleets to meet efficiency standards. This segment outpaces others with higher adoption rates.

Regional Insights

North America Mid-Lift Axle Market Trends

North America is set to command a significant portion of the mid-lift axle market share at approximately 34% in 2026. The United States drives primary demand through its vast fleet of heavy commercial vehicles. Operators rely on these systems to meet Federal Bridge Formula standards. The formula requires even load distribution across multiple axles. Canada adds significant volume from resource extraction and construction activities. Heavy payloads demand robust axle solutions in these sectors. Regulators enforce mature frameworks that promote compliance. OEMs maintain strong partnerships with suppliers. Aftermarket networks support ongoing maintenance and upgrades effectively.

Growth accelerates through key policy and market shifts. The Infrastructure Investment and Jobs Act funds extensive road and bridge projects. E-commerce expansion increases freight volumes on highways. Major carriers electrify long-haul fleets, which need adaptive axles for battery weight. Hendrickson, Dana, and Meritor (now under Cummins) invest heavily in innovation. They develop advanced technologies for connected management. Proprietary designs give them an edge in performance. Aftermarket services generate high margins via diagnostics and retrofits. Fleets adopt telematics for real-time adjustments. In the future, producers will integrate artificial intelligence to predict wear patterns. Operators gain efficiency from seamless electrification compatibility. Governments incentivize green upgrades through subsidies. Suppliers expand local production to cut lead times.

Europe Mid-Lift Axle Market Trends

Europe serves as the second-largest regional market for mid-lift axles. Germany anchors the continent with its strong automotive and commercial vehicle production. Companies such as DAF, MAN (Maschinenfabrik Augsburg-Nürnberg), and Mercedes-Benz Trucks lead manufacturing efforts. These firms rely on extensive freight networks for distribution. The United Kingdom maintains solid demand through retail and food logistics, even after Brexit supply chain adjustments. France and Spain add volume from agriculture, construction, and transport. Spain's growing logistics centers support Mediterranean trade flows. Harmonized rules under the European Union (EU) Weights and Dimensions Directive push fleets toward compliant axle designs.

Policy initiatives accelerate the adoption of advanced systems. The EU Green Deal and Fit for 55 package promote commercial vehicle electrification. These frameworks require electronically managed axles for zero-emission powertrains. Operators integrate smart solutions to balance battery weight and payloads effectively. Volvo Trucks, Scania, and Daimler Trucks collaborate with suppliers on research and development (R&D). They embed intelligent features into electric vehicle platforms. Manufacturers seize consolidation chances in a fragmented component market. Well-funded players pursue mergers to scale production. Fleets benefit from standardized designs across borders. Governments offer incentives for green upgrades that enhance efficiency.

Asia Pacific Mid-Lift Axle Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing mid-lift axle market through 2033. China dominates with its massive industrial output and commercial vehicle production. The government invests heavily in national expressway networks under the 14th Five-Year Plan. These projects boost freight transport needs across provinces. India stands out as a dynamic growth area. The National Logistics Policy drives fleet modernization to lower transport costs. Infrastructure upgrades spur demand for heavy-duty trucks in construction and trade. Japan maintains steady uptake through preferences for advanced technology and strict enforcement of weight limits, while the ASEAN is accelerating industrialization.

Cost advantages fuel this regional momentum. Manufacturers benefit from nearby raw material sources and skilled labor pools. Domestic consumption rises as economies urbanize rapidly. Suppliers localize production to serve OEMs efficiently. Fleets adopt mid-lift axles to improve payload handling on improved roads. Governments offer incentives for vehicle upgrades tied to emission goals. In the future, producers will integrate smart features for electric fleets. Logistics firms gain an edge through reliable uptime in high-volume corridors. Regional trade pacts enhance cross-border haulage demands. Suppliers form joint ventures to tap local expertise. Asia Pacific shapes global supply chains with scalable innovations.

Competitive Landscape

The global mid-lift axle market structure is moderately consolidated, dominated by leading players such as Hendrickson International, Dana Incorporated, SAF-Holland SE, BPW Group, and Ridewell Corporation. These players collectively capture 55-60% of the market share. Leading companies strengthen their dominance through relentless product innovation, strategic collaborations, and global expansion drives. They allocate significant resources to R&D for cutting-edge axle technologies that boost payload efficiency and integration.

Partnerships with OEMs embed mid-lift axles seamlessly into vehicle platforms, ensuring market-ready solutions. Firms expand footprints in high-growth areas such as the Asia Pacific via localized production. They prioritize electric vehicle compatibility and smart diagnostics to meet evolving fleet needs. These tactics create barriers for newcomers while capturing value in aftermarket services. Operators gain reliable systems that enhance compliance and reduce downtime costs.

Key Industry Developments

- In January 2026, Mack Trucks introduced an Automatic Standby Mode for its 6×2 liftable pusher axle, automating suspension pressure equalization and eliminating manual driver intervention. The system enhances mid-lift (pusher) axle efficiency by optimizing load distribution, preventing axle overload, and improving fuel economy and maintenance outcomes in variable-load operations.

- In December 2025, Kenworth expanded its medium-duty battery-electric lineup with the T280E, T380E, and T480E, offering configurable platforms for regional, utility, and vocational fleet applications. Notably, the trucks support flexible wheelbases and lift axle installations, strengthening their relevance for mid-lift axle configurations in weight distribution, payload optimization, and multi-application fleet operations.

- In May 2025, Yuill & Dodds added five new DAF XG 530 6x2 tractor units with mid-lift axles, replacing older DAF XF trucks as part of its fleet renewal strategy. The vehicles were supplied by Asset Alliance Group under a contract hire deal that includes full repair and maintenance support, improving operational efficiency and reliability.

Companies Covered in Mid-Lift Axle Market

- Hendrickson International

- Dana Incorporated

- SAF-Holland SE

- Meritor, Inc. (Cummins)

- BPW Group

- Ridewell Corporation

- ReycoGranning

- Schmitz Cargobull AG

- Kessler & Co. GmbH

- JOST Werke SE

- Steyr Powertrain GmbH

- Dongfeng Axle Co., Ltd.

- Tata Motors Ltd.

- Hyundai Transys Inc.

Frequently Asked Questions

The global mid-lift axle market is projected to reach US$ 3.0 billion in 2026.

Infrastructure investments and freight growth are boosting the demand for heavy-duty vehicles with efficient load management and driving the market.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Major opportunities lie in the booming logistics sector in Asia Pacific, with smart IoT integration offering high-growth potential for advanced systems.

Hendrickson International, Dana Incorporated, SAF-Holland SE, BPW Group, and Ridewell Corporation are some of the key players in the market.