- Industrial Goods & Service

- Metal Fabrication Market

Metal Fabrication Market Size, Share, and Growth Forecast, 2026 - 2033

Metal Fabrication Market By Process Type (Cutting, Machining, Others), Material Type (Steel, Aluminum, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Metal Fabrication Market Size and Trends Analysis

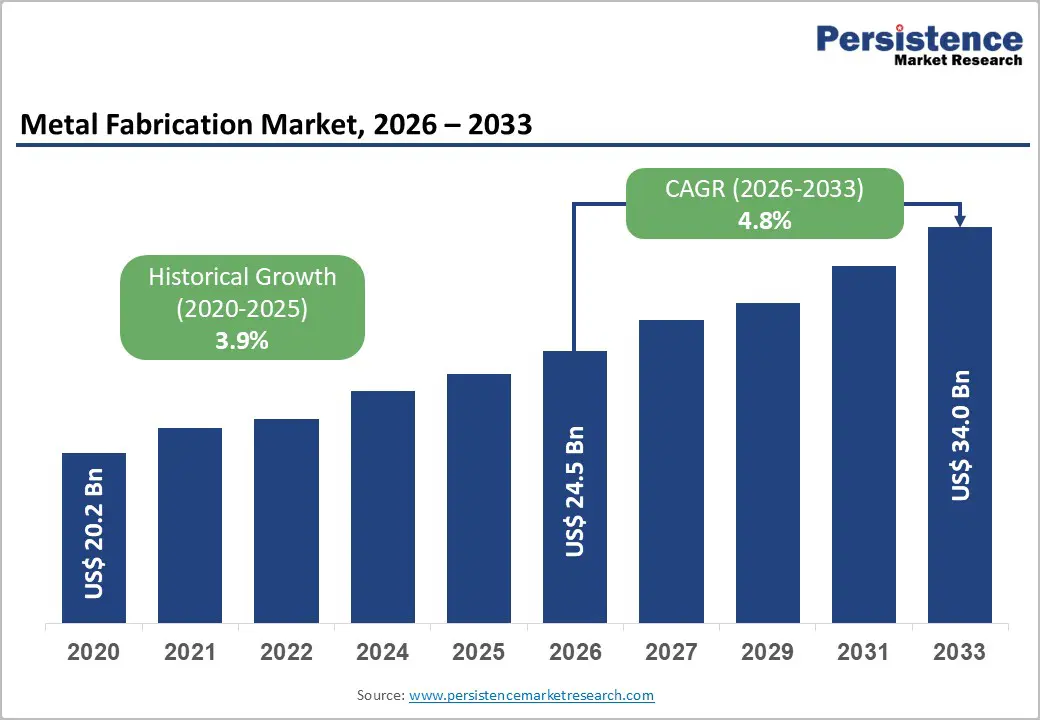

The global metal fabrication market size is likely to be valued at US$ 24.5 billion in 2026 and is expected to reach US$ 34.0 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033, driven by the increasing automation across manufacturing facilities, growing demand for lightweight fabricated components in transportation equipment, and sustained global infrastructure development.

Expansion of advanced machining technologies and digital manufacturing platforms is improving productivity across fabrication facilities. However, volatile raw-material prices, energy costs, and skilled-labor shortages remain operational challenges that companies must strategically address.

Key Industry Highlights:

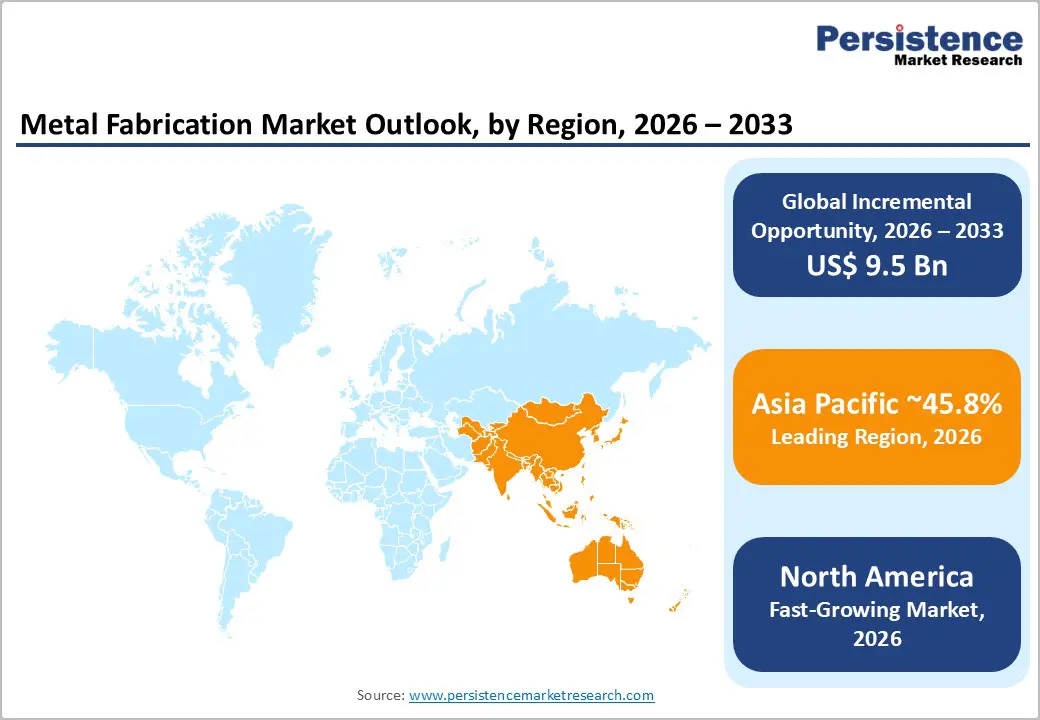

- Leading Region: Asia Pacific is projected to hold the dominant position in the market, accounting for approximately 45.8% of market share, supported by large-scale manufacturing capacity, strong infrastructure development, and expanding industrial production in China, India, and Southeast Asia.

- Fastest-growing Region: North America is projected to be the fastest-growing regional market, driven by accelerating investments in advanced manufacturing, electric vehicle production, and aerospace component fabrication, supported by government initiatives aimed at strengthening domestic industrial supply chains.

- Investment Plans: Fabrication companies across major industrial economies are increasing capital investments in automation technologies, robotic welding systems, and advanced CNC machining centers, with many manufacturers allocating 10-15% of operational modernization budgets toward smart factory upgrades and digital production monitoring systems.

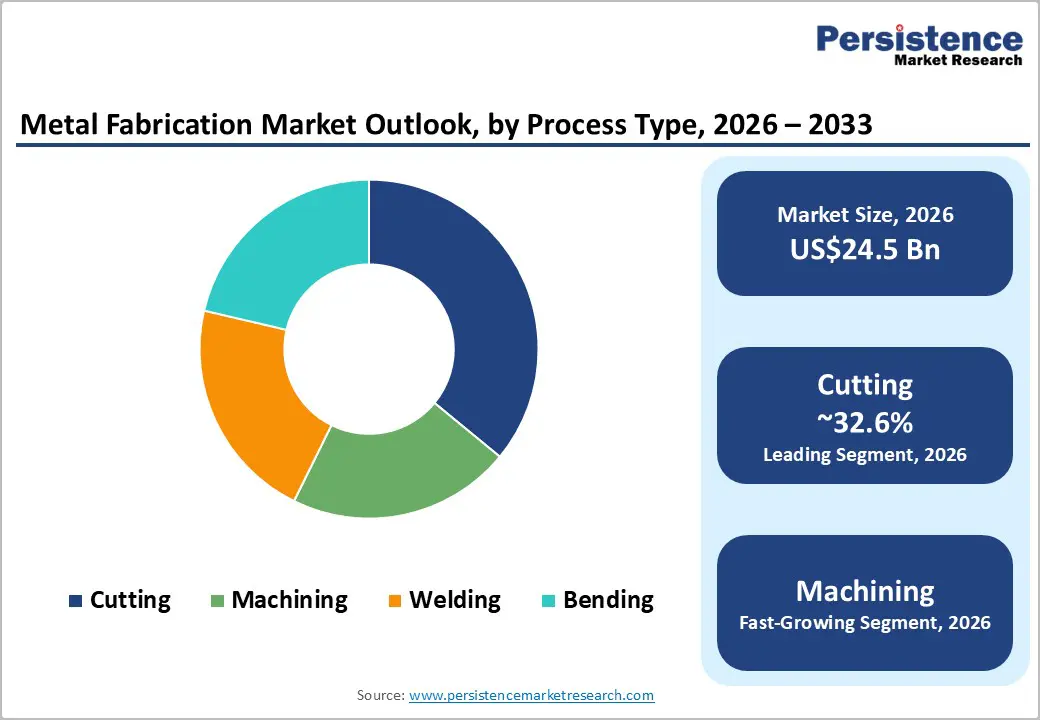

- Dominant Process Type: Cutting processes are anticipated to contribute approximately 32.6% of market share, due to their extensive use in sheet metal processing, structural fabrication, and high-volume industrial component manufacturing.

- Leading Material Type: Steel remains is estimated to account for over 49.5% of market share, driven by its strength, durability, and cost efficiency in construction structures, industrial equipment manufacturing, and energy infrastructure projects.

| Key Insights | Details |

|---|---|

| Metal Fabrication Market Size (2026E) | US$24.5 Bn |

| Market Value Forecast (2033F) | US$34.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Automation and Precision Manufacturing Technologies

The rapid adoption of computer numerical control (CNC) machining, robotics, and integrated fabrication systems is significantly improving productivity across metal fabrication facilities. Automation allows manufacturers to achieve higher production accuracy, lower cycle times, and improved operational efficiency. Modern fabrication environments are increasingly integrating digital production monitoring, robotics-assisted welding, and automated material handling systems. These advancements allow manufacturers to process complex components with tighter tolerances and minimal material waste. As industrial manufacturers adopt Industry 4.0 manufacturing systems, demand for precision fabricated components continues to grow. Companies investing in automated fabrication cells benefit from higher equipment utilization rates and improved production consistency, strengthening their competitive positioning in global supply chains.

Increasing Demand for Lightweight Metals in Transportation

The transportation industry is undergoing a structural shift toward lightweight materials, particularly aluminum and advanced alloys. Automotive manufacturers, aerospace companies, and electric vehicle producers are actively reducing vehicle weight to improve fuel efficiency and extend battery performance. This shift has created significant demand for precision metal fabrication processes capable of handling lightweight materials while maintaining structural integrity. Advanced fabrication techniques such as laser cutting, friction stir welding, and high-precision machining enable manufacturers to fabricate complex lightweight structures for transportation equipment. As electrification and aerospace production expand globally, fabrication companies capable of working with lightweight alloys will capture higher-value contracts and long-term supply agreements.

Expansion of Global Infrastructure Development

Government-led infrastructure programs are significantly increasing demand for fabricated metal products used in bridges, commercial buildings, industrial plants, and transportation networks. Fabricated steel structures remain essential components of large-scale infrastructure projects due to their strength, durability, and cost efficiency. Rapid urbanization across emerging economies is also driving the construction of residential complexes, logistics hubs, and industrial facilities. These projects require structural beams, reinforcement components, sheet metal assemblies, and custom metal parts. As infrastructure investments continue globally, fabricated metal components will remain indispensable in large-scale construction and industrial development projects.

Barrier Analysis - Raw Material Price Volatility

Metal fabrication companies depend heavily on raw materials such as steel, aluminum, and copper, whose prices fluctuate based on global commodity markets. Sudden increases in raw material prices can significantly affect profit margins, particularly for companies operating under long-term fixed-price contracts. Fluctuations in energy costs also influence production expenses, as fabrication processes such as laser cutting, welding, and machining require significant electricity consumption. These cost pressures often force companies to renegotiate supply contracts or absorb short-term financial losses, limiting operational flexibility.

Skilled Workforce Shortage

The transition toward automated and digitally controlled fabrication systems has increased the need for highly skilled technicians. Operators must possess expertise in CNC programming, robotics operation, and advanced welding technologies. However, many industrial regions face shortages of qualified workers capable of operating modern fabrication systems. Companies must invest significantly in workforce training and certification programs to maintain operational efficiency. These training requirements increase operational costs and may slow facility expansion in regions with limited technical labor availability.

Opportunity Analysis - Regional Manufacturing and Nearshoring

Global manufacturers are increasingly shifting production closer to end markets in order to reduce supply chain risks and transportation costs. This trend toward regional manufacturing and nearshoring creates opportunities for fabrication companies located near major industrial clusters. Local fabrication facilities can offer shorter lead times, improved quality control, and enhanced collaboration with equipment manufacturers. Companies that establish regional fabrication hubs with automated production capabilities are well-positioned to capture supply contracts from automotive, aerospace, and industrial equipment manufacturers.

Expansion of Value-Added Fabrication Services

Many customers are seeking fabrication partners that can deliver integrated manufacturing solutions rather than standalone processing services. These solutions include design for manufacturability, precision machining, surface finishing, coating, assembly, and quality inspection. By offering integrated services, fabrication companies can increase project value and strengthen long-term customer relationships. The adoption of digital manufacturing software also enables companies to manage complex production workflows more efficiently, creating additional revenue opportunities across the fabrication value chain.

Technological Advancements in Fabrication Equipment

Continuous improvements in laser cutting systems, automated welding robots, and advanced forming technologies are enabling fabricators to produce complex components with higher efficiency and accuracy. New equipment designs also reduce material waste and energy consumption. Companies adopting these technologies can expand their production capabilities and enter specialized markets such as aerospace components, renewable energy structures, and electric vehicle parts. These sectors require high-precision fabricated components and offer strong long-term growth potential.

Category-wise Analysis

Process Type Insights

Cutting is anticipated to remain the leading segment, accounting for approximately 32.6% of the market share in 2026. Cutting technologies such as laser cutting, plasma cutting, and waterjet cutting are widely used for sheet metal processing, structural fabrication, and component preparation across multiple industries. These processes enable manufacturers to produce precise shapes with minimal material waste, making them essential in sectors that require high-volume and standardized metal components. Laser cutting technology has significantly improved efficiency by enabling automated nesting software, high-speed production cycles, and improved material utilization rates. For example, laser cutting systems are widely used in the automotive industry for chassis parts and body panels, while construction companies rely on plasma cutting to process structural steel beams used in infrastructure projects. The integration of automated cutting systems within smart factories is further improving production throughput and operational efficiency across fabrication facilities.

Machining is anticipated to be the fastest-growing process segment during the forecast period. Machining processes involve removing material from metal components using advanced computer numerical control (CNC) equipment to achieve precise dimensions and complex geometries. Growing demand for high-precision components in aerospace, automotive, medical equipment, and industrial machinery is driving strong growth in machining services. Advanced multi-axis CNC machines, automated tooling systems, and real-time monitoring technologies allow fabrication companies to manufacture complex parts with minimal manual intervention. For instance, aerospace manufacturers require precision-machined turbine components and structural brackets, while electric vehicle manufacturers rely on CNC machining for battery housings and drivetrain components. These technological advancements improve production accuracy, reduce errors, and enable fabricators to deliver highly customized components required in modern manufacturing environments.

Material Type Insights

Steel is anticipated to remain the dominant material in metal fabrication, accounting for over 49.5% of market share in 2026. Steel’s exceptional strength, durability, and cost efficiency make it the preferred material for large-scale construction structures, heavy equipment manufacturing, and industrial machinery components. Fabricated steel beams, plates, and reinforcement elements are widely used in bridges, commercial buildings, pipelines, and energy infrastructure projects. Structural steel fabrication is particularly critical for high-rise construction and industrial facilities where load-bearing capacity and structural reliability are essential. For example, steel frameworks are extensively used in stadium construction, transportation infrastructure, and power generation facilities, where large structural assemblies must withstand extreme environmental conditions. The availability of multiple steel grades, including carbon steel, stainless steel, and alloy steel, further expands its application across engineering and manufacturing projects.

Aluminum is anticipated to be the fastest-growing material segment in the metal fabrication market. The increasing use of lightweight materials in transportation and aerospace industries has significantly boosted demand for aluminum fabrication. Automotive manufacturers are incorporating aluminum components into vehicle frames, body panels, and structural reinforcements to reduce weight and improve fuel efficiency. Similarly, aerospace manufacturers rely heavily on aluminum alloys due to their high strength-to-weight ratio and corrosion resistance, making them ideal for aircraft fuselage structures and wing assemblies. The rapid expansion of the electric vehicle industry is also accelerating aluminum usage in battery enclosures, cooling systems, and structural components. Fabrication companies capable of processing aluminum through advanced welding, precision machining, and forming techniques are therefore experiencing increasing demand from manufacturers seeking lightweight and high-performance metal components.

Regional Insights

North America Metal Fabrication Market Trends - Automation, EV Manufacturing, and Aerospace Precision Fabrication

North America represents one of the most technologically advanced markets for metal fabrication. The U.S. leads regional demand due to its strong industrial manufacturing base and continuous investment in advanced production technologies. The region hosts several global leaders in metal processing equipment and welding technologies, including Lincoln Electric, Kennametal, and Hypertherm, which supply fabrication systems and industrial solutions to manufacturers across aerospace, automotive, and energy sectors. Their continued investment in advanced welding systems, cutting technologies, and digital fabrication platforms is helping strengthen North America’s manufacturing capabilities.

The region has witnessed significant growth in automated fabrication systems, robotics integration, and precision machining capabilities. Manufacturers in aerospace, automotive, and defense industries rely heavily on specialized fabrication suppliers to produce high-precision components. For example, aerospace manufacturers such as Boeing depend on advanced machining and metal forming processes for aircraft structural components, driving demand for high-precision fabrication services. Similarly, electric vehicle manufacturers, including Tesla, have expanded North American production facilities, increasing the need for fabricated aluminum battery housings, vehicle frames, and drivetrain components. Government initiatives aimed at strengthening domestic manufacturing are also contributing to regional growth. U.S. industrial policy programs designed to improve supply chain resilience and expand advanced manufacturing capabilities are encouraging companies to expand local fabrication operations.

These initiatives support sectors such as electric vehicle production and renewable energy equipment manufacturing, where fabricated metal components are critical for battery systems, wind turbine structures, and industrial machinery. The regulatory environment in North America emphasizes workplace safety, environmental compliance, and product quality standards. Fabrication companies must comply with strict occupational safety guidelines and emissions regulations, particularly those enforced by industrial safety agencies. While these regulations increase compliance costs, they also encourage the adoption of cleaner manufacturing technologies and energy-efficient equipment, which improves long-term operational sustainability. Investment activity across North America continues to focus on modernizing fabrication facilities. Companies are installing automated cutting systems, robotic welding equipment, and advanced CNC machining centers to improve production capabilities. A notable example is the expansion of advanced manufacturing facilities by TRUMPF in the U.S., where the company has invested in smart factory infrastructure to support local production of laser cutting systems and automated fabrication technologies.

Europe Metal Fabrication Market Trends - Precision Engineering Leadership and Smart Factory Integration

Europe maintains a strong position in the global metal fabrication industry due to its highly developed industrial sector and advanced engineering capabilities. Countries such as Germany, the U.K., France, and Spain play critical roles in regional manufacturing supply chains. The region is home to several leading fabrication technology companies, including TRUMPF, Bystronic, and Prima Industrie, which supply advanced laser cutting systems, bending machines, and automated fabrication technologies to industrial manufacturers worldwide. Germany is widely recognized as a global leader in industrial machinery and precision engineering. German fabrication facilities integrate advanced automation technologies and digital production monitoring systems into their operations.

Companies such as Siemens and Thyssenkrupp rely on fabricated metal components for industrial machinery, energy infrastructure, and advanced engineering systems. Germany’s strong machine tool industry also supports the development of highly automated fabrication lines that improve productivity across European manufacturing sectors. The U.K. and France maintain strong fabrication capabilities in sectors such as aerospace, defense manufacturing, and energy infrastructure. Aircraft manufacturers such as Airbus depend on high-precision metal components produced through advanced machining and forming processes. These aerospace manufacturing activities create a steady demand for specialized fabrication services.

European regulatory policies emphasize environmental sustainability, energy efficiency, and product safety. Fabrication companies must comply with stringent environmental regulations related to emissions control, waste management, and workplace safety. These regulations are encouraging companies to adopt energy-efficient laser systems, automated welding equipment, and sustainable manufacturing practices. Investment across Europe increasingly focuses on digital manufacturing technologies and smart factory systems. Fabrication companies are integrating machine connectivity, predictive maintenance systems, and advanced analytics to improve operational efficiency. These innovations support Europe’s global reputation for high-precision engineering and advanced manufacturing technologies, allowing regional manufacturers to maintain strong competitiveness in global industrial markets.

Asia Pacific Metal Fabrication Market Trends - Large-Scale Industrial Manufacturing and Infrastructure-Driven Demand

Asia Pacific is projected to hold the largest share of the market, accounting for approximately 45.8% of the market in 2026. The region’s dominance is driven by large-scale manufacturing activity, rapid industrialization, and extensive infrastructure development. Several global manufacturing leaders operate large fabrication facilities across the region, supported by expanding industrial supply chains and strong export-oriented production. China represents the largest fabrication market within the region due to its massive industrial production capacity and strong manufacturing ecosystem.

Chinese industrial companies such as China Baowu Steel Group and Shanghai Electric play major roles in supplying fabricated metal components for construction projects, energy systems, and industrial machinery. The country’s infrastructure expansion, including high-speed rail networks, large commercial developments, and energy facilities, continues to generate strong demand for fabricated steel structures and industrial components. Japan remains a major hub for advanced manufacturing technologies and precision machining. Japanese industrial equipment manufacturers such as Yamazaki Mazak and Amada Co., Ltd., produce highly sophisticated machine tools and fabrication systems used globally. Their continuous innovation in laser cutting, CNC machining, and automation technologies strengthens Asia Pacific’s leadership in advanced manufacturing capabilities.

India is emerging as a rapidly growing fabrication market due to expanding infrastructure development and government initiatives promoting domestic manufacturing. Engineering and industrial conglomerates such as Larsen & Toubro and Bharat Forge are investing in large-scale fabrication facilities to support infrastructure projects, defense manufacturing, and energy sector development. These investments are increasing domestic production of fabricated components used in power plants, transportation infrastructure, and industrial machinery.

Automotive companies such as Toyota Motor Corporation and Honda Motor Co., Ltd. operate major manufacturing plants in these countries, increasing regional demand for fabricated metal components used in vehicle production. Asia Pacific’s combination of large manufacturing capacity, competitive labor costs, strong industrial supply chains, and rapid infrastructure development positions the region as the leading contributor to global metal fabrication production. Continued investments in industrial technology and manufacturing facilities are expected to sustain the region’s dominant market position throughout the forecast period.

Competitive Landscape

The global metal fabrication market is moderately fragmented, consisting of numerous regional fabrication companies alongside large industrial equipment manufacturers and specialized fabrication service providers. Small and medium-sized fabrication workshops dominate commodity metal processing services such as cutting and welding.

However, large multinational companies specializing in advanced fabrication technologies, automation equipment, and integrated manufacturing solutions hold stronger positions in high-precision industrial markets. Companies that offer advanced capabilities such as automated machining, robotic welding, and integrated assembly services maintain significant competitive advantages in high-value industrial sectors. Leading companies in the metal fabrication industry focus on automation integration, advanced machining capabilities, and expanded service offerings. Firms are investing in smart factory technologies, digital manufacturing platforms, and robotics-assisted fabrication systems to improve efficiency and maintain competitive advantages.

Key Industry Developments:

- In October 2025, TRUMPF launched the TruLaser Weld 5000 automated laser welding system at Blechexpo, featuring improved setup speed and a touch-based programming interface that allows operators to adjust welding positions directly on the machine. The system is designed to improve efficiency for automated metal fabrication and small-batch production environments.

- In September 2025, Siemens and TRUMPF announced a strategic partnership to advance digital manufacturing and AI-enabled production systems. The collaboration integrates Siemens’ Xcelerator digital platform with TRUMPF’s fabrication equipment and software solutions to enable interoperable and data-driven manufacturing processes.

Companies Covered in Metal Fabrication Market

- TRUMPF

- Amada Co., Ltd.

- Bystronic

- Mazak Corporation

- Lincoln Electric

- O'Neal Manufacturing Services

- Ryerson Holding Corporation

- Metcam Inc.

- Mayville Engineering Company, Inc.

- BTD Manufacturing

- Colfax Corporation

- Alcoa Corporation

- Thyssenkrupp AG

- Komaspec

- Kapco Metal Stamping

- Standard Iron & Wire Works

Frequently Asked Questions

The global metal fabrication market is estimated to reach US$24.5 billion in 2026.

The metal fabrication market is projected to reach US$34.0 billion by 2033.

Key industry trends include the adoption of advanced CNC machining and robotic welding technologies, growing use of laser cutting and automated fabrication systems, and rising demand for lightweight materials such as aluminum in automotive and aerospace manufacturing. Increasing integration of smart factory technologies and digital production monitoring systems is also transforming fabrication operations.

Under process type segmentation, cutting processes represent the leading segment, accounting for approximately 32.6% of the total market share, primarily due to the widespread use of laser, plasma, and waterjet cutting in sheet metal processing and structural fabrication applications.

The metal fabrication market is projected to grow at a CAGR of 4.8% between 2026 and 2033.

Major companies include TRUMPF, Amada Co., Ltd., Lincoln Electric, Yamazaki Mazak, and Bystronic.