- Medical Devices

- Manometry System Market

Manometry System Market Size, Share, and Growth Forecast, 2026 - 2033

Manometry System Market by Product Type (Anorectal Manometry System, Anorectal Manometry System Software, Others), Portability (Stand Alone System, Portable System), End-user (Hospitals, Others), and Regional Analysis for 2026 - 2033

Manometry System Market Size and Trends Analysis

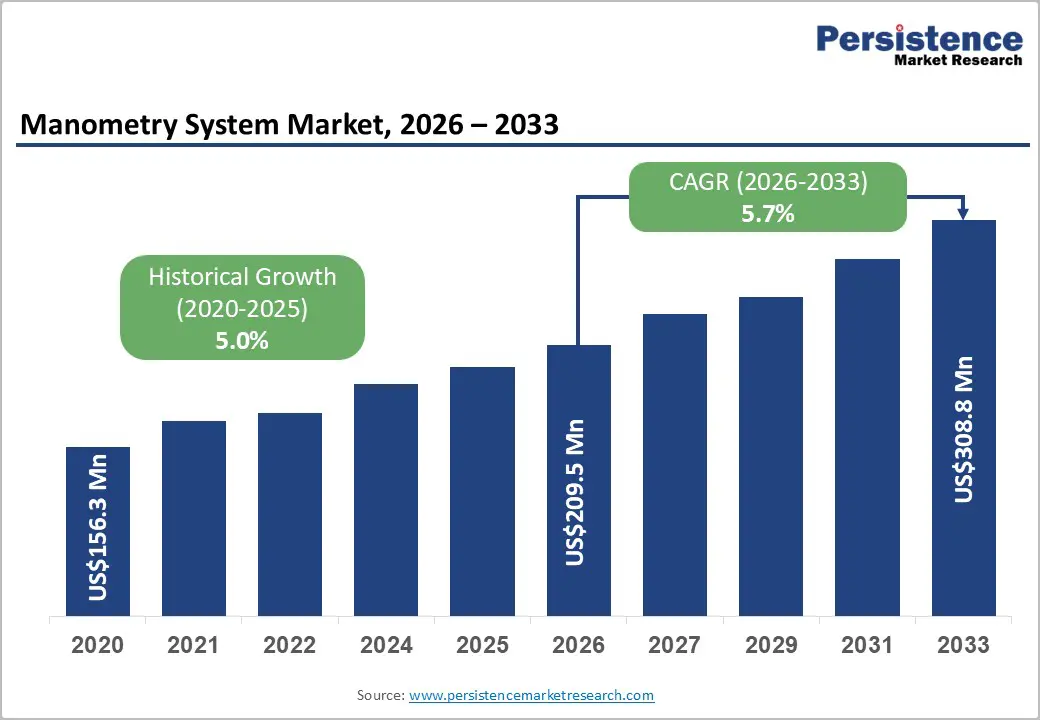

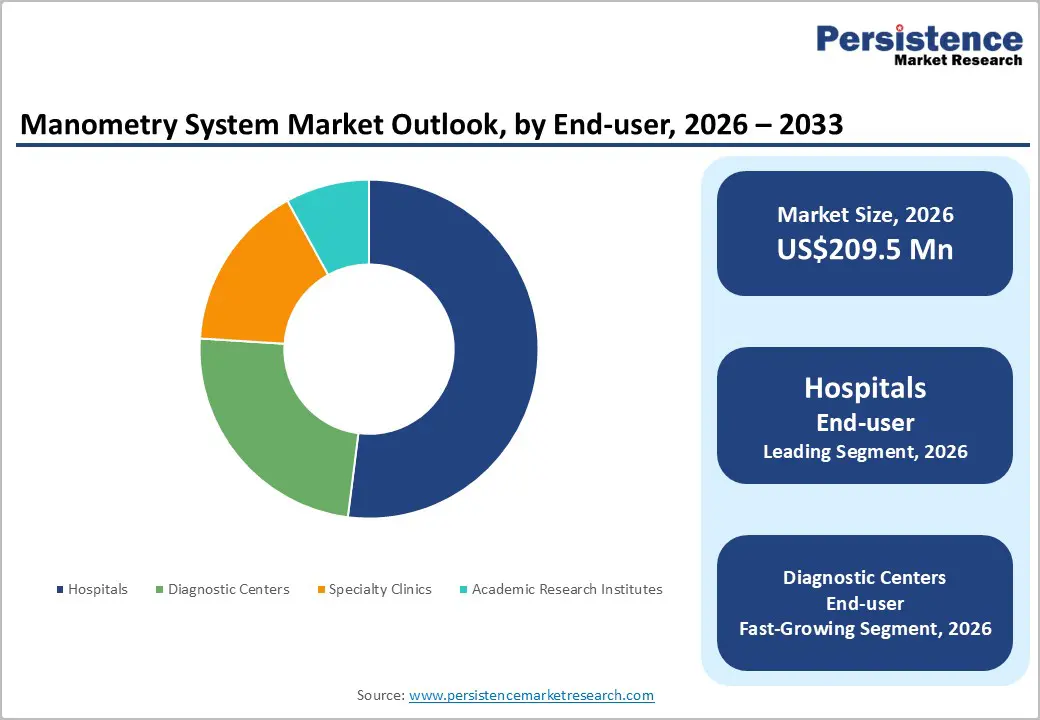

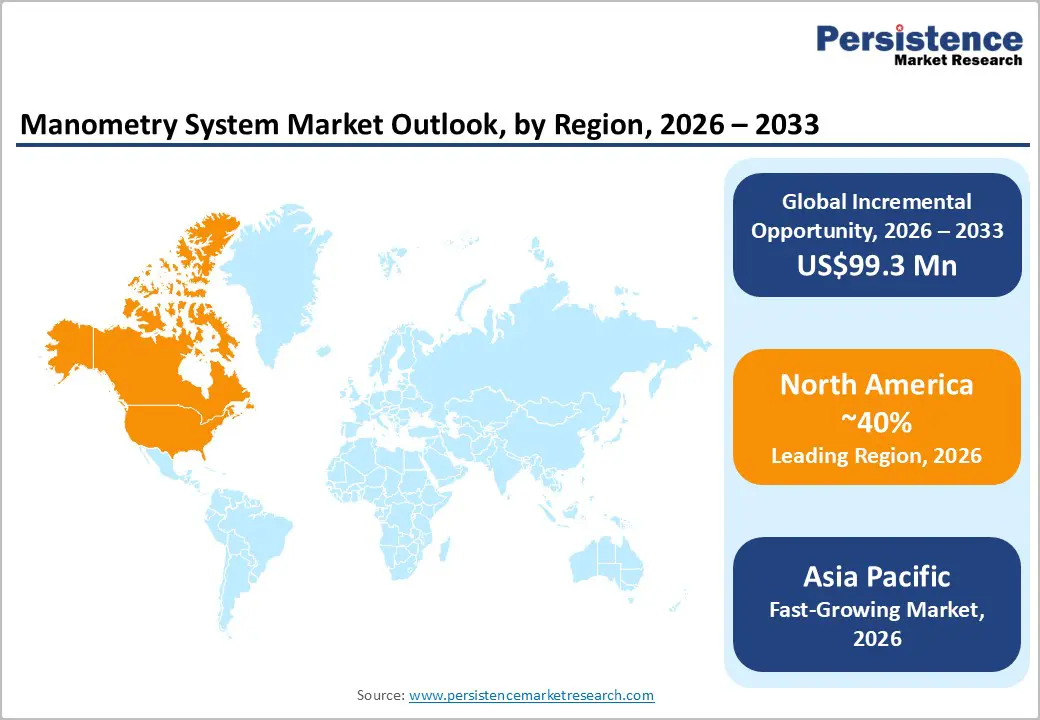

The global manometry system market size is likely to be valued at US$209.5 million in 2026, and is expected to reach US$308.8 million by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033, driven by the increasing prevalence of gastrointestinal motility disorders (achalasia, gastroparesis, chronic constipation), rising adoption of high-resolution anorectal and esophageal manometry for precise diagnosis, growing demand for standardized motility testing in hospitals and specialty clinics, and expanding awareness of functional GI disorders in aging populations.

Growing demand for anorectal manometry system hardware and hospitals' end-use is accelerating adoption across gastroenterology departments and motility labs. Advances in 3D high-resolution catheters, wireless portability, and integrated software analytics are further boosting uptake by offering superior sphincter mapping, real-time pressure visualization, and improved patient comfort. The increasing recognition of manometry systems as the gold-standard diagnostic tool for the objective evaluation of anorectal and esophageal function in emerging neurogastroenterology and pelvic floor disorder markets remains a major driver of market growth.

Key Industry Highlights:

- Leading Region: North America, anticipated to account for a 40% market share in 2026, driven by high GI disorder prevalence, advanced motility labs, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising gastroenterology infrastructure, increasing functional GI diagnosis rates, and growing medical tourism in India and China.

- Dominant Product Type: Anorectal manometry system, to hold approximately 55% of the market share, as it remains the core hardware category.

- Leading End-user: Hospitals, contributing nearly 58% of the market revenue due to the highest procedural volume and specialized GI units.

| Key Insights | Details |

|---|---|

|

Manometry System Market Size (2026E) |

US$209.5 Mn |

|

Market Value Forecast (2033F) |

US$308.8 Mn |

|

Projected Growth CAGR (2026-2033) |

5.7% |

|

Historical Market Growth (2020-2025) |

5.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Functional GI Disorders and High-Resolution Manometry Adoption

The increasing prevalence of functional gastrointestinal (GI) disorders is significantly driving the demand for advanced diagnostic technologies such as high-resolution manometry. Functional GI conditions, including disorders like irritable bowel syndrome, chronic constipation, and esophageal motility disorders, are becoming more common due to factors such as sedentary lifestyles, unhealthy dietary habits, rising stress levels, and aging populations. These conditions often involve abnormalities in the movement and coordination of the digestive tract, which makes accurate diagnosis essential for effective treatment planning.

High-resolution manometry has emerged as a critical diagnostic tool because it provides detailed pressure mapping of the esophagus and anorectal region. Compared with conventional manometry techniques, it offers improved spatial resolution and more precise visualization of muscle contractions and coordination within the gastrointestinal tract. This allows clinicians to identify motility disorders more accurately and differentiate between various functional abnormalities. Healthcare providers are increasingly adopting advanced diagnostic systems to improve patient outcomes and reduce diagnostic uncertainty.

Developments of Portable Systems and Point-of-Care Motility Testing

Advancements in diagnostic technology are enabling the development of portable gastrointestinal motility testing systems, improving accessibility and convenience for both healthcare providers and patients. Traditional motility testing systems are typically large, complex, and confined to specialized hospital settings. Newer portable devices are designed to be compact, user-friendly, and easier to integrate into smaller clinical environments such as outpatient clinics and diagnostic centers. These systems allow clinicians to conduct motility assessments without requiring highly specialized infrastructure.

Portable solutions also support point-of-care testing, which allows gastrointestinal motility evaluations to be performed closer to the patient. This approach helps reduce the need for multiple hospital visits and long waiting times for diagnostic procedures. Faster testing and immediate data availability enable healthcare professionals to make quicker clinical decisions and begin treatment earlier. For patients, portable systems can improve comfort and convenience, particularly for those who require repeated assessments. Technological improvements in sensors, wireless connectivity, and data analysis software have further strengthened the reliability of portable motility testing systems.

Barrier Analysis - High Device Cost and Limited Reimbursement

The high cost of advanced gastrointestinal diagnostic equipment presents a significant challenge for healthcare providers, particularly in small hospitals and diagnostic centers with limited budgets. High-resolution manometry systems, along with their specialized catheters, software, and maintenance requirements, often involve substantial upfront investment. In addition to the initial purchase cost, ongoing expenses such as device calibration, disposable components, and staff training further increase the overall financial burden for healthcare facilities.

Limited reimbursement policies for gastrointestinal motility testing procedures also restrict wider adoption. In several healthcare systems, reimbursement coverage for diagnostic tests related to motility disorders may be insufficient or inconsistent, making it difficult for providers to recover the full cost of equipment and procedures. Some healthcare facilities hesitate to invest in advanced diagnostic systems despite their clinical benefits.

Shortage of Trained Motility Specialists

The limited availability of trained motility specialists acts as a significant barrier to the adoption of advanced gastrointestinal diagnostic technologies. Procedures such as esophageal and anorectal manometry require specialized knowledge to correctly position catheters, conduct the test, and accurately interpret complex pressure patterns generated during the examination. Without properly trained professionals, the risk of inaccurate results and misinterpretation increases, which can affect clinical decision-making and patient management.

Training in gastrointestinal motility diagnostics is often concentrated in large tertiary hospitals and academic medical centers, leaving many smaller hospitals and diagnostic clinics without adequately skilled personnel. The process of training physicians and technicians in motility testing can be time-consuming and resource-intensive, requiring hands-on experience and specialized education.

Opportunity Analysis - Advancements in Portable Systems and Wireless High-Resolution Manometry

Technological advancements in gastrointestinal diagnostic equipment are creating opportunities for the development and adoption of portable and wireless high-resolution manometry systems. Traditional manometry equipment is often large and confined to specialized hospital laboratories, which can limit accessibility and increase the complexity of testing procedures. The introduction of compact, portable systems allows healthcare providers to perform motility assessments in a wider range of clinical settings, including outpatient clinics and smaller diagnostic centers.

Wireless high-resolution manometry systems further enhance convenience by reducing the need for extensive cables and stationary monitoring equipment. These systems can transmit pressure data in real time to connected software platforms, allowing clinicians to monitor and analyze gastrointestinal motility more efficiently. Improved patient mobility and comfort during testing also contribute to better patient compliance and more accurate physiological measurements. The shift toward decentralized healthcare and outpatient diagnostics is encouraging the adoption of these portable solutions. Healthcare providers are increasingly seeking technologies that streamline workflow, reduce procedure time, and improve diagnostic efficiency. Portable and wireless systems can also support remote monitoring and data sharing between healthcare professionals, enabling more collaborative care.

Integration of Artificial Intelligence and Advanced Software

The integration of artificial intelligence (AI) and advanced analytical software into manometry systems presents a significant opportunity for improving diagnostic efficiency and clinical decision-making. Modern gastrointestinal motility testing generates large volumes of pressure data that require careful interpretation by trained specialists. AI-powered algorithms can assist in analyzing these complex datasets by identifying abnormal pressure patterns, motility irregularities, and subtle physiological changes that may be difficult to detect through manual review alone.

Advanced software platforms equipped with automated pattern recognition and data visualization tools enable clinicians to interpret results more quickly and consistently. This reduces variability in diagnosis and supports standardized evaluation of esophageal and anorectal motility disorders. AI-driven systems can provide decision-support insights by comparing patient data with established diagnostic parameters, allowing physicians to reach more confident conclusions.

Category-wise Analysis

Product Type Insights

Anorectal manometry system is anticipated to dominate the market, accounting for 55% of the market share in 2026. Its dominance is driven by increasing diagnoses of anorectal disorders such as chronic constipation, fecal incontinence, and pelvic floor dysfunction. These systems are widely used by gastroenterologists to evaluate the pressure, coordination, and function of muscles in the rectum and anal canal, making them essential for accurate diagnosis and treatment planning. Hospitals and specialty clinics increasingly rely on anorectal manometry as it provides detailed physiological insights that cannot be obtained through conventional diagnostic methods. ManoScan™ AR High-Resolution Anorectal Manometry System, which is widely used by gastroenterologists to evaluate anorectal disorders such as fecal incontinence, chronic constipation, and pelvic floor dysfunction.

Anorectal manometry system software represents the fastest-growing product type, due to the increasing need for advanced data analysis and efficient interpretation of motility test results. These software platforms enable clinicians to visualize pressure patterns, generate detailed reports, and store patient data for future reference. Modern systems also include automated analysis features that help reduce interpretation time and improve diagnostic consistency. ManoView™ AR analysis software, which is used with its ManoScan™ high-resolution anorectal manometry systems. The software enables clinicians to analyze pressure data collected during motility testing and visualize anorectal pressure patterns through advanced graphical displays.

Portability Insights

Stand alone systems are expected to dominate the market, contributing nearly 62% of revenue in 2026, fueled by their ability to provide a complete and dedicated platform for gastrointestinal motility testing within hospitals and specialized gastroenterology laboratories. These systems integrate hardware, sensors, and analytical software into a single unit, allowing clinicians to perform detailed diagnostic procedures with high accuracy and reliability. Large healthcare facilities often prefer stand-alone systems as they support high patient volumes and offer advanced features for comprehensive pressure analysis and reporting.

The portable system segment is expected to witness the fastest growth in the manometry system market due to its ability to offer flexible and convenient gastrointestinal motility testing across a variety of healthcare environments. Unlike conventional fixed systems, portable devices are compact and easy to transport, enabling clinicians to conduct diagnostic procedures in outpatient clinics, smaller hospitals, and specialized diagnostic centers. These systems help reduce infrastructure requirements and improve operational efficiency by allowing quicker setup and smoother patient management. An example is the mcompass Anorectal Manometry System, a lightweight and portable diagnostic device developed to perform anorectal manometry without the need for a dedicated laboratory setup. It enables healthcare providers to carry out motility testing directly within outpatient clinics and physician offices, thereby improving accessibility and convenience for both clinicians and patients.

Regional Insights

North America Manometry System Market Trends

North America is projected to dominate, accounting for 40% of the share in 2026, driven by the strong presence of advanced healthcare infrastructure, increasing awareness of gastrointestinal motility disorders, and the rising adoption of modern diagnostic technologies. Hospitals and specialized gastroenterology clinics in the U.S. and Canada frequently use manometry systems to evaluate pressure and muscle function in the esophagus, anorectal region, and other parts of the gastrointestinal tract. These systems help physicians diagnose conditions such as chronic constipation, swallowing disorders, and pelvic floor dysfunction, which are becoming more commonly reported due to lifestyle changes and aging populations.

The region is seeing the growing use of high-resolution manometry (HRM) systems. These systems provide detailed pressure mapping and improved visualization of gastrointestinal motility patterns compared with traditional diagnostic methods. Many hospitals and specialty clinics are upgrading from conventional systems to HRM technology to improve diagnostic accuracy and clinical efficiency. The integration of advanced software and portable diagnostic systems. Modern manometry systems now include user-friendly software for data visualization and automated analysis, allowing clinicians to interpret results more quickly.

Europe Manometry System Market Trends

Europe market is witnessing stable growth, propelled by the increasing focus on accurate diagnosis of gastrointestinal motility disorders and the region’s strong healthcare infrastructure. Manometry systems are widely used in hospitals, diagnostic centers, and gastroenterology clinics to measure pressure and muscle coordination in the esophagus and anorectal region. These systems help physicians diagnose conditions such as dysphagia, chronic constipation, pelvic floor dysfunction, and fecal incontinence. The growing awareness of digestive health and the increasing number of patients seeking specialized gastroenterology care are contributing to the demand for manometry-based diagnostic procedures across Europe.

Growing adoption of high-resolution manometry (HRM) technology. HRM systems use multiple closely spaced sensors to provide detailed pressure mapping of the gastrointestinal tract, enabling clinicians to detect motility abnormalities with higher accuracy. Many hospitals and specialty clinics in countries such as Germany, France, the U.K., and Italy are adopting these advanced systems to improve diagnostic precision and patient management. Expansion of specialized gastrointestinal diagnostic centers and motility laboratories. These facilities focus on advanced testing procedures and help improve early diagnosis and treatment planning for patients with complex digestive disorders.

Asia Pacific Manometry System Market Trends

Asia Pacific is likely to be the fastest-growing market for manometry systems, driven by expanding healthcare infrastructure, rising awareness of gastrointestinal disorders, and increasing access to advanced diagnostic technologies. Countries such as China, Japan, India, and South Korea are investing heavily in hospital modernization and the expansion of specialized gastroenterology services, which is increasing the adoption of manometry systems for evaluating gastrointestinal motility disorders. These systems are commonly used to diagnose conditions such as dysphagia, chronic constipation, irritable bowel syndrome–related motility issues, and anorectal dysfunction.

Growing adoption of high-resolution manometry (HRM) systems in large hospitals and tertiary care centers. HRM technology provides detailed pressure mapping of the gastrointestinal tract, allowing clinicians to more accurately identify motility abnormalities compared with traditional diagnostic methods. As awareness of advanced diagnostic tools grows, many healthcare providers are upgrading their existing systems to high-resolution platforms. Increasing development of specialized gastroenterology and digestive disease centers across major urban areas. These centers are equipped with modern diagnostic equipment, including esophageal and anorectal manometry systems, to support comprehensive motility testing.

Competitive Landscape

The global manometry system market is characterized by competition between established gastrointestinal motility device manufacturers and emerging diagnostic technology providers. Leading companies such as Medtronic and Laborie maintain a strong presence in North America and Europe due to their extensive installed base, comprehensive catheter and software portfolios, and long-standing partnerships with hospitals and specialized gastroenterology clinics. These companies continue to strengthen their market position by developing advanced high-resolution manometry systems and portable diagnostic platforms that improve clinical workflow and patient comfort.

In the Asia Pacific region, several regional manufacturers are introducing cost-effective manometry systems, making gastrointestinal motility testing more accessible for mid-size hospitals and diagnostic centers. The adoption of anorectal and esophageal manometry systems is increasing as healthcare providers focus on improving diagnostic precision and reducing the risk of misdiagnosis in motility disorders.

Key Industry Developments:

- In May 2024, Laborie Medical Technologies Corp. (Laborie) is proud to introduce the Solar Compact System and Solar Anorectal Manometry Catheter, the first disposable HRAM catheter on the market. These devices significantly advance diagnostic capabilities for defecatory disorders and pelvic-floor dysfunction associated with constipation and fecal incontinence by measuring static and dynamic pressures in the lower gastrointestinal tract.

Companies Covered in Manometry System Market

- EB Neuro S.p.A.

- MEDSPIRA

- Medtronic

- Medica S.p.A.

- RMS Medical Devices

- MARQUAT Génie Biomédical

- Diversatek Inc.

- Dentsleeve International Ltd.

- LABORIE

- Prometheus Group

Frequently Asked Questions

The global manometry system market is projected to reach US$209.5 million in 2026.

The rising prevalence of functional gastrointestinal disorders such as irritable bowel syndrome, chronic constipation, and esophageal motility disorders is increasing the demand for advanced diagnostic tools like high-resolution manometry.

The manometry system market is poised to witness a CAGR of 5.7% from 2026 to 2033.

Technological advancements are enabling the development of portable and wireless high-resolution manometry systems, improving flexibility in gastrointestinal motility testing.

Medtronic, Laborie, Diversatek Inc., MEDSPIRA, and Prometheus Group are the key players.