- Electrical Equipment & Services

- Limit Switches Market

Limit Switches Market Size, Share, and Growth Forecast 2026 – 2033

Limit Switches Market by Application (Compact Limit Switches, Hazardous Location Limit Switches, Heavy-duty Limit Switches), Actuator Type (Roller Actuated, Plunger Actuated, Lever Actuated, Others), Operation (Momentary/Spring Return, Non-return), End-user (Manufacturing Industry, Metals & Mining Industry, Process Industry, Materials Handling and Transportation Industry, Others), and Regional Analysis for 2026–2033

Limit Switches Market Size and Trend Analysis

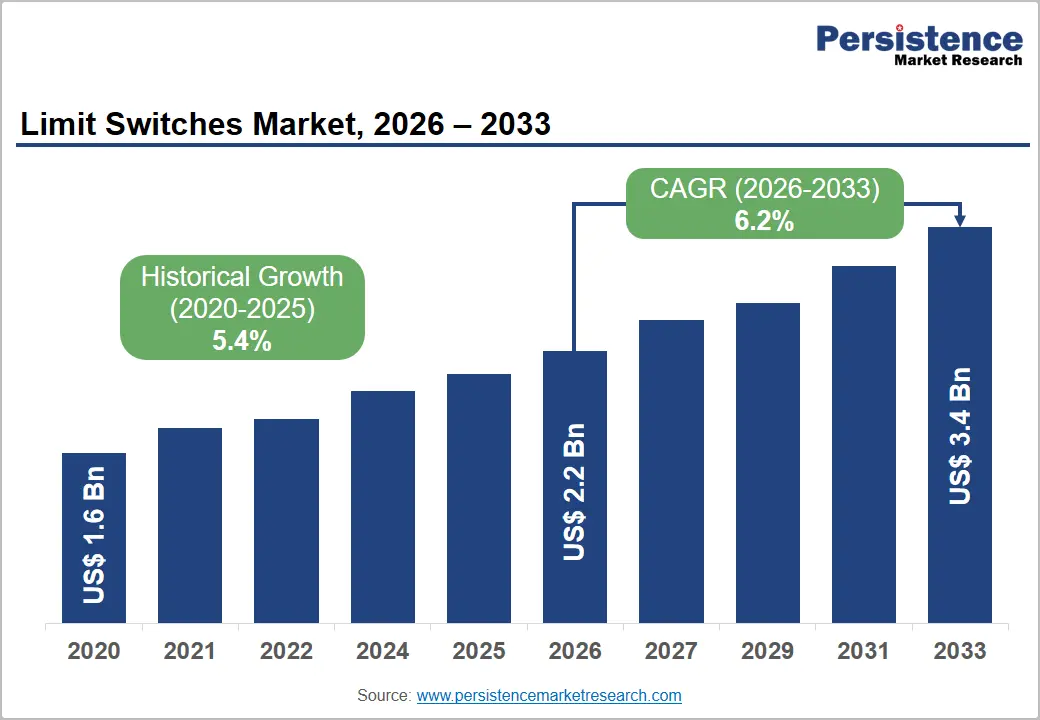

The global limit switches market size is expected to reach US$ 11.8 billion in 2026 and US$ 21.9 billion, growing at a CAGR of 9.2% between 2026 and 2033.

The accelerating adoption of industrial automation drives the market's sustained growth, the proliferation of smart manufacturing under Industry 4.0 frameworks, and growing end-use demand across manufacturing, metals and mining, and materials handling sectors globally. According to the International Federation of Robotics (IFR), global industrial robot installations reached a record 500,000+ units in 2023, each requiring precise position sensing and safety interlock solutions that limit switches reliably provide.

Stringent workplace safety regulations enforced by bodies including OSHA in the United States and the European Machinery Directive (2006/42/EC) are embedding limit switches as mandatory safety components across new and retrofit industrial equipment deployments, creating a structurally supported and regulation-driven demand.

Key Industry Highlights:

- Expansion to Safety Regulations – OSHA, IEC, and ATEX safety regulations are structurally embedding limit switches across industrial machinery, conveyor systems, oil and gas facilities, and hazardous environments, sustaining long-term specification-based procurement demand globally.

- Dominance of Compact Switches – Compact limit switches are likely to hold a value at approximately 44% share in 2026, supported by widespread adoption across packaging machinery, injection moulding systems, conveyor equipment, and industrial automation applications worldwide.

- Hazardous Segment Growth – Hazardous location limit switches are forecast to expand at approximately 11.5% CAGR, fueled by LNG infrastructure, offshore oil platforms, and chemical processing facility safety requirements globally.

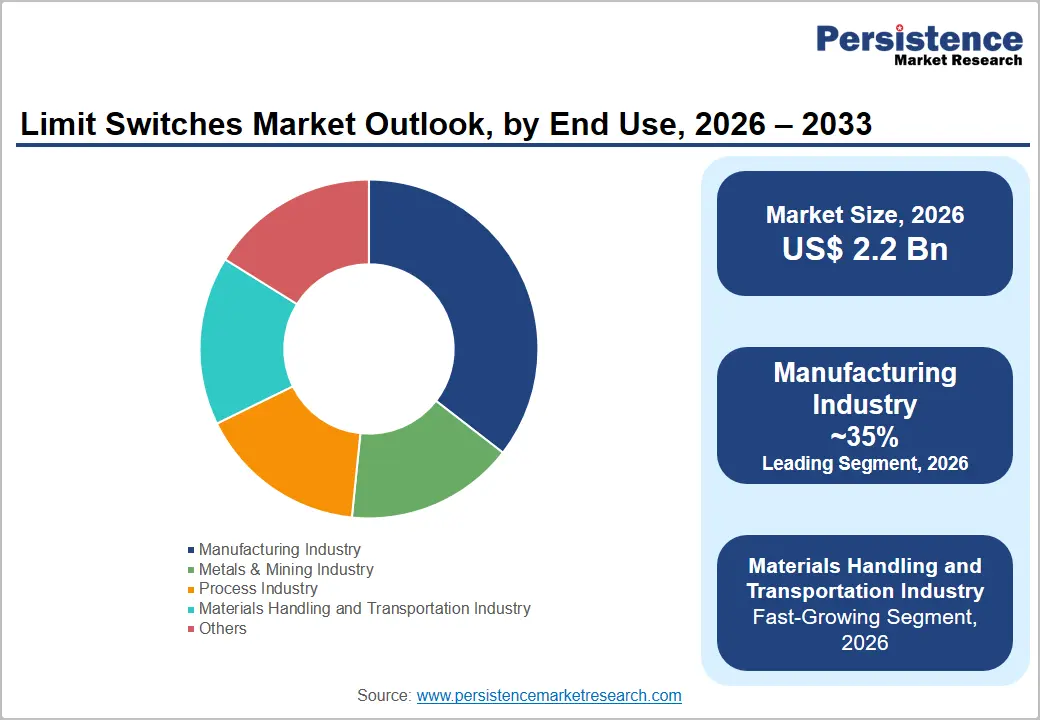

- Manufacturing Industry Leadership – Manufacturing accounted for nearly 35% global share in 2026, driven by high automation adoption across automotive, electronics, robotics, metal fabrication, and industrial assembly production facilities worldwide.

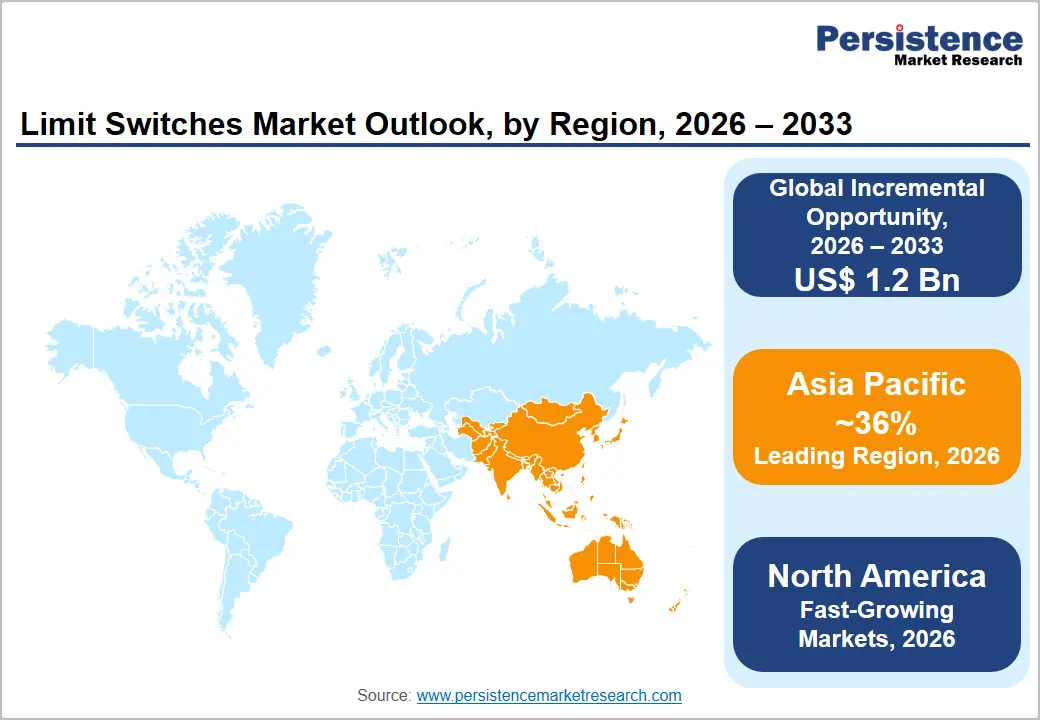

- Asia Pacific Dominance – Asia Pacific is likely to command 36% global share in 2026 and is projected to reach 11.5% CAGR, led by China, India, Japan, and Korea.

- India Automation Momentum – India represented around US$ 700 million market value in 2026 and is projected to reach a positive CAGR supported by PLI-led industrial automation investments.

Market Dynamics

Drivers - Industrial Automation and Smart Manufacturing Mandates Structurally Embedding Limit Switch Demand

The global transition toward automated, digitally integrated manufacturing environments is the most consequential structural demand driver for the limit switches market. The International Federation of Robotics (IFR) reported that global robot density in manufacturing reached 151 robots per 10,000 employees in 2023, with South Korea, Singapore, and Germany leading deployment intensity, each automated production line embedding multiple limit switches as positional feedback, end-of-travel detection, and safety interlock components.

Under Industry 4.0 frameworks, manufacturing enterprises are undertaking systematic equipment upgrades in which legacy electromechanical systems are retrofitted with IoT-enabled sensing components, including smart limit switches with diagnostic output capabilities. The European Commission's Horizon Europe programme has allocated substantial R&D funding toward smart factory infrastructure, including sensing and safety component standardisation. This dual demand stream new installation at greenfield facilities and retrofit demand at existing plants, creates a compounding procurement pipeline that sustains limit switch market momentum across all major industrial end-use segments.

Mandatory Industrial Safety Standards and Workplace Regulation Driving Specification-Based Procurement

Limit switches are embedded by regulatory mandate across a broad range of industrial equipment categories, creating a demand base that is structurally independent of discretionary capital expenditure cycles. In the United States, OSHA Standard 1910.217 and NFPA 79 (Electrical Standard for Industrial Machinery) require position sensing and safety interlock mechanisms, directly specifying limit switch deployment in stamping, pressing, and conveyor equipment.

The European Machinery Directive (2006/42/EC) and IEC 60947-5-1 international standard for low-voltage switchgear govern limit switch technical specifications across European industrial markets, creating a compliance procurement ecosystem that sustains demand at all industrial equipment OEM and end-user tiers. In hazardous environments, ATEX Directive 2014/34/EU (Europe) and NEC Article 501 (USA) mandate explosion-proof and intrinsically safe limit switch configurations at oil and gas, chemical, and mining installations, generating premium-priced procurement that elevates average revenue per unit above standard industrial segments.

Restraints - Competition from Non-Contact Sensing Technologies Displacing Electromechanical Limit Switches

The growing adoption of non-contact proximity sensors including inductive, capacitive, photoelectric, and magnetic reed technologies, presents a structural competitive threat to traditional electromechanical limit switches in automation and material handling applications. IEC 60947-5-2 inductive proximity sensors, in particular, offer longer operational lifespans, no mechanical wear, and faster switching frequencies, making them technically superior in high-cycle-rate applications such as conveyor systems and robotic end-effectors. As sensor prices continue to decline with scale, the total cost of ownership differential that previously favoured limit switches is narrowing, constraining growth at volume-sensitive OEM specification tiers.

Supply Chain Volatility in Electronic Components and Raw Material Cost Pressures

Global semiconductor and electronic component supply chain disruptions documented extensively by the Semiconductor Industry Association (SIA) through 2021–2023 have created persistent lead-time and cost volatility for limit switch manufacturers dependent on microelectronic actuators, printed circuit boards, and precision mechanical sub-assemblies. Raw material cost pressures in zinc alloy, stainless steel, and engineered polymers used in limit switch housing and actuator construction directly impact manufacturing margins. For mid-tier producers competing primarily on price, these cost pressures create margin compression that limits R&D investment capacity and constrains competitive response to technology-differentiated market leaders.

Opportunities - Hazardous Location Limit Switches in Expanding Oil, Gas, and Chemical Processing Infrastructure

Hazardous location limit switches engineered for deployment in potentially explosive atmospheres classified under ATEX, IECEx, and NEC standards represent the fastest-growing application segment in the global limit switches market, projected at a CAGR of approximately 11.5%.

The simultaneous expansion of global LNG liquefaction infrastructure, offshore oil and gas platform development, and chemical process industry facility construction across the Asia Pacific and the Middle East. The International Energy Agency (IEA) reported that global LNG export capacity is expected to expand by over 50% between 2023 and 2030, with each new liquefaction train requiring hundreds of ATEX/IECEx-certified limit switches for valve position monitoring, emergency shutdown interlocks, and conveyor safety systems.

For manufacturers holding dual ATEX and IECEx certification, the hazardous location segment offers premium ASPs 30–60% above standard industrial equivalents, significant barriers to entry from non-certified competitors, and a project-based procurement model with high per-order values from EPC contractors.

Materials Handling and Logistics Automation: Creating High-Volume Limit Switch Procurement Pipelines

The shift toward automated warehouse, distribution centre, and port logistics infrastructure driven by e-commerce fulfilment demands and supply chain resilience investment is creating a high-volume, recurring procurement pipeline for limit switches in the materials handling and transportation end-use segment. Amazon, Alibaba, and JD Logistics are collectively operating hundreds of highly automated fulfilment centres globally, each deploying conveyor systems, sortation equipment, and automated storage and retrieval systems (AS/RS) that integrate limit switches as positional feedback and end-of-travel safety components at scale.

The Logistics Property Company (LPC) and Prologis report continued double-digit growth in automated warehouse construction globally through 2025–2027. The International Material Management Society (IMMS) documents that modern high-throughput sortation systems require 200–500+ limit switches per installation, making the materials handling segment a structurally attractive, volume-driven commercial opportunity for both OEM supply and aftermarket replacement procurement.

Category-wise Analysis

Application Insights

Compact limit switches account for a dominant position in the global limit switches market by application, commanding approximately 44% of the total share in 2026. Compact limit switches characterised by their space-efficient housing designs, standardised IEC 60947-5-1 compliance, and wide operating temperature range are the default specification choice across the broadest range of industrial automation equipment categories, including machine tools, injection moulding machines, packaging machinery, and conveyor drive systems.

Their dominance reflects the composition of global industrial equipment OEM production, which is concentrated in general-purpose manufacturing machinery, where compact form factor and cost-competitive pricing are primary procurement criteria. Key producers, including Omron Corporation, Honeywell, and Schneider Electric, maintain extensive compact limit switch product lines comprising dozens of variants in body size, actuator configuration, and environmental protection rating that ensure OEM design engineers can specify a compliant product without supplier qualification risk. The segment also benefits from the highest aftermarket replacement volume, as compact limit switches in high-cycle manufacturing applications require periodic preventive maintenance and replacement.

Hazardous location limit switches are the fast-growing application segment. Mandatory ATEX Directive 2014/34/EU and IECEx certification requirements for explosive atmosphere deployments in LNG, oil and gas, and chemical plant installations are driving premium-segment procurement growth as global energy infrastructure expands.

Actuator Type Insights

Roller actuated limit switches lead the actuator type segment with approximately 38% of global market share in 2026, reflecting their design suitability across the widest variety of mechanical detection applications. Roller actuators available in configurations including roller plunger, hinged roller lever, and adjustable roller lever provide bidirectional actuation capability and reduced actuation force compared to standard plunger designs, making them the preferred actuator type for cam-operated position detection on machine tool slideway systems, conveyor belt edge detection, and rotating machinery guard interlock applications.

The roller actuator's tolerance of off-axis approach angles and smooth mechanical operation reduces wear and extend service life in high-cycle automation environments, delivering a total cost of ownership advantage over rigid plunger actuators that reinforces OEM specification preference at volume production equipment tiers. Key suppliers Siemens AG (3SE5 series), Telemecanique (Schneider Electric) (XC series), and Eaton (E49 series) maintain roller actuated variants as core catalogue products with broad global distribution support.

Lever actuated limit switches constitute the fastest-growing actuator type, projected at a CAGR of approximately 11.0% in the forecast period. Adjustable lever configurations including adjustable rod, flexible rod, and whisker lever designs, are uniquely suited to object detection and position feedback in automated materials handling equipment, where the lever's sensitivity and adjustable detection range accommodate varying load sizes and approach geometries in high-throughput sortation and conveyor systems.

Operation Insights

The momentary/spring return operation type holds a commanding dominant position in the global limit switches market, accounting for approximately 65% of the total share in 2026. Momentary operation, where the switch contact returns to its default state immediately upon actuator release, is the operationally preferred configuration across the vast majority of industrial safety interlocks, end-of-travel detection, and position sensing applications, because it ensures a fail-safe default output state that conforms to IEC 62061 functional safety requirements for machinery.

In emergency stop and safety gate interlock circuits, the spring return to de-energised state is not merely a preference but a code-mandated safety requirement under ISO 13849-1 (Safety of Machinery Safety-Related Parts of Control Systems), which governs Performance Level (PL) assessment for safety functions. Both Pilz and Schmersal, specialist safety switch manufacturers, confirm that momentary limit switches constitute the overwhelming majority of safety-rated position switch installations across European and North American machine builders, driving the segment's substantial share lead over non-return configurations in certified safety applications.

Non-return (Maintained Contact) limit switches represent the fastest-growing operation type, projected at a CAGR of approximately 10.5% in the forecast period. Their sustained-state output characteristic makes them well-suited for applications requiring persistent signal output independent of physical actuator engagement, including door interlock holding circuits, bin-level indicators, and process valve position confirmation in SCADA-integrated process control architectures.

End-user Insights

The manufacturing industry segment leads the global limit switches market by end-user, holding approximately 35% of the total share in 2026. Manufacturing's leadership position reflects the pervasive application of limit switches across virtually every category of production machinery, CNC machine tools, injection moulding machines, stamping presses, robotic work cells, and assembly automation lines where position sensing, end-of-travel protection, and safety interlock functions are fundamental operational requirements.

The International Federation of Robotics (IFR) confirms that manufacturing accounts for the largest share of global industrial robot installations, with automotive, electronics, and metal fabrication sub-sectors driving the highest automation density and, consequently, the highest per-facility limit switch procurement volumes. Major automotive OEMs, including Toyota, Volkswagen, and General Motors, operating hundreds of highly automated body-in-white and powertrain assembly plants globally, represent anchor customers for high-volume, specification-grade compact and heavy-duty limit switch procurement at both OEM equipment builder and direct-to-plant maintenance supply tiers.

The materials handling and transportation industry is a fast-growing end-user segment, projected at a CAGR of approximately 11.2% in the forecast period. The exponential growth of automated warehousing, e-commerce fulfilment infrastructure, and port automation, with Amazon and Alibaba collectively operating hundreds of robotically intensive distribution centres.

Regional Insights

North America Limit Switches Market Trends

North America accounts for approximately 24% of the global limit switches market share in 2026, driven by a deep-rooted industrial automation culture, stringent OSHA and NFPA safety regulation frameworks that mandate position sensing and interlock components across a wide range of production equipment, and the continued capital investment of U.S. manufacturing enterprises in smart factory upgrades under the CHIPS and Science Act and Inflation Reduction Act (IRA) manufacturing incentive programs. The region's limit switch demand is particularly pronounced in automotive, aerospace, oil and gas, and food and beverage processing sectors that operate large installed equipment bases requiring periodic maintenance and replacement.

Canada contributes through its oil sands and mining industry demand for hazardous location and heavy-duty limit switches, while Mexico's rapidly expanding automotive and electronics manufacturing maquiladora sector is generating new OEM equipment installation demand aligned with North American supply chain reshoring and nearshoring investment trends documented by the Reshoring Initiative in 2024.

U.S. Industrial Automation Drives Limit Switch Demand

The United States holds approximately 85% of the North American limit switch market revenues, contributing an estimated US$ 2.4 billion in 2026 at an approximate CAGR of 8.8% in the coming years. The U.S. market strength derives from four converging demand factors:

- the world's largest installed base of industrial machinery requiring regulatory-mandated safety interlocks,

- the continued automation capital expenditure of automotive OEMs and tier-1 suppliers aligned to EV production line investments,

- the IRA-incentivised domestic semiconductor and clean energy manufacturing facility construction requiring extensive limit switch integration in new production equipment,

- the robust oil and gas infrastructure requiring NEC Article 501-certified hazardous location switches at upstream, midstream, and downstream installations.

Honeywell and Rockwell Automation, both headquartered in the U.S., maintain significant domestic market share anchored by deep OEM specification relationships and comprehensive domestic distribution networks through Grainger, Fastenal, and specialist automation distributors.

Europe Limit Switches Market Trends

Europe holds approximately 28% of the global limit switches market share in 2026, making it the second-largest regional market, anchored by Germany's globally dominant machinery and plant engineering sector, robust regulatory frameworks under the European Machinery Directive (2006/42/EC) and ATEX Directive 2014/34/EU, and the continent's strategic emphasis on industrial digitalisation under the European Commission's Industry 5.0 and Horizon Europe programmes. European OEM machinery builders concentrated in Germany, Italy, Switzerland, and Austria embed limit switches as standard components across exported machine tools, packaging, food processing, and materials handling equipment, generating export-driven global demand that extends the European market's influence beyond the continent itself.

The European Commission's Machinery Regulation (EU) 2023/1230, replacing the Machinery Directive and entering force in 2027 is expected to further standardise safety component specification requirements across EU member states, reducing certification fragmentation and stimulating compliant limit switch procurement upgrades at industrial facilities undertaking safety system harmonisation ahead of the transition deadline.

Germany's Machinery Sector Anchors European Limit Switch Leadership

Germany contributes approximately 28% of European limit switch market revenues in 2026, representing an estimated US$ 960 million, growing at an approximate CAGR of 8.5%. Germany's limit switch market leadership is structurally rooted in the country's unparalleled concentration of industrial machinery OEMs the Verband Deutscher Maschinen- und Anlagenbau (VDMA) reports that Germany is the world's second-largest mechanical engineering exporter after China, with over 6,500 machinery and plant engineering companies collectively generating €240+ billion in annual revenues.

This dense OEM ecosystem is the world's most significant limit switch specification and procurement hub, with companies including Siemens AG (SIRIUS 3SE5 series), Pepperl+Fuchs, and Balluff GmbH headquartered domestically and maintaining deep specification relationships with German machine builders that sustain high-value, technically differentiated limit switch demand above global average ASPs.

UK Process Industry Fuels Limit Switch Specification Demand

United Kingdom accounts for approximately 18% of European limit switch market revenues in 2026, representing an estimated US$ 617 million, advancing at an approximate CAGR of 8.2%. UK is distinguished by a high concentration of process industry demand, particularly in oil and gas, pharmaceuticals, food and beverage, and water treatment sectors where limit switches serve as critical valve position monitoring, actuator interlock, and emergency shutdown sensing components under Health and Safety Executive (HSE) PSSR (Pressure Systems Safety Regulations) and DSEAR (Dangerous Substances and Explosive Atmospheres Regulations) compliance frameworks.

ABB, Rotork Controls, and Bettis (Emerson), leading actuator and valve automation suppliers active in U.K. process industry markets specify limit switches as integral components of their motorised valve assemblies, generating structured procurement through established process automation supply chains.

France's Chemical Industry Sustains Limit Switch Market Demand

France represents approximately 15% of European limit switch market revenues in 2026, contributing an estimated US$ 514 million at an approximate CAGR of 8.0%. France's limit switch demand is significantly shaped by the country's substantial chemical and petrochemical processing sector, including TotalEnergies, Arkema, and Solvay where ATEX-certified hazardous location limit switches are mandatory safety components at classified zone installations.

The French Ministry of Ecological Transition's enforcement of SEVESO III Directive (2012/18/EU) requirements at major hazard industrial sites creates a legally mandated demand floor for certified safety sensing components, including explosion-proof limit switches. France's automotive manufacturing sector anchored by Stellantis (PSA) and Renault contributes further compact limit switch demand at body assembly, powertrain machining, and logistics automation installations across domestic production facilities.

Italy's Manufacturing Sector Powers Limit Switch Revenue Contribution

Italy accounts for approximately 12% of European limit switch market revenues in 2026, representing an estimated US$ 411 million, growing at an approximate CAGR of 7.8% through 2033. Italy's limit switch market is underpinned by the country's world-class industrial machinery manufacturing ecosystem the Associazione Nazionale Costruttori di Impianti (ANIMA) and UCIMU (Italian Machine Tool Manufacturers' Association) collectively represent thousands of machine tool, robotics, and automation equipment builders that embed limit switches as standard industrial components.

Italy's packaging machinery sector, which UCIMA (Italian Packaging Machinery Manufacturers' Association) estimates generates over €8 billion in annual production, is a particularly significant limit switch demand driver, as high-speed packaging lines deploy multiple compact limit switches per machine for flap detection, seal bar position sensing, and conveyor jam protection in continuous production environments.

Asia Pacific Limit Switches Market Trends

Asia Pacific is the leading and fastest-growing regional market for limit switches, commanding approximately 36% of global market share in 2026 and expanding at an estimated CAGR of approximately 11.5%. China's position as the world's largest manufacturing economy, generating over 28% of global manufacturing output according to the World Bank, creates the single largest national limit switch demand base globally, driven by scale across automotive, electronics, metals, and general machinery production. Japan's precision manufacturing culture sustains demand for high-specification, miniaturised limit switch variants, while India's National Manufacturing Policy targets and South Korea's smart factory (K-Smart Factory) government programme are creating new structural demand clusters across the region.

The ASEAN manufacturing growth story led by Vietnam, Thailand, Indonesia, and Malaysia attracting supply chain diversification investment from Japanese, Korean, and Western multinationals is generating a new tier of industrial equipment installation demand across electronics, automotive parts, and consumer goods production facilities that systematically embed limit switches as standard safety and position sensing components in compliance with ISO 4413 (hydraulic) and ISO 4414 (pneumatic) machinery safety standards adopted in ASEAN industrial zones.

China Manufacturing Scale Dominates APAC Limit Switch Demand

China holds approximately 45% of the Asia Pacific limit switch market revenues in 2026, representing an estimated US$ 1.76 billion. China's limit switch market is structurally anchored by the country's position as the world's largest industrial robot user. The IFR reports China deployed over 290,000 industrial robots in 2023, each installation embedding multiple limit switches and its dominant global position in automotive, electronics, and general machinery manufacturing.

The Ministry of Industry and Information Technology (MIIT) of China's "Made in China 2025" initiative and successor smart manufacturing programmes are systematically upgrading factory automation infrastructure across key industrial sectors, creating sustained procurement demand for both domestic suppliers, including CHINT Group and DELIXI Electric and international leaders including Omron, Siemens, and Schneider Electric competing at premium specification tiers in China's tiered industrial market structure.

India's Industrial Automation Boom Accelerates Limit Switch Adoption

India accounts for approximately 18% of the Asia Pacific limit switch market revenues in 2026, equivalent to an estimated US$ 700 million, and is one of the fast-growing markets at a CAGR of approximately 13.5%. India's structural growth driver is the government's Production-Linked Incentive (PLI) Scheme across 13 manufacturing sectors, including automotive, electronics, pharmaceuticals, and food processing, which is attracting domestic and foreign direct investment at greenfield manufacturing facilities that are built to modern automation standards requiring extensive limit switch integration.

The Invest India agency reports over USD 83 billion in committed PLI investment as of 2024, representing a multi-year pipeline of new industrial facility construction. India's expanding mining sector, governed by the Mines Act, 1952 and increasingly adopting mechanised and semi-automated extraction methods, is also driving hazardous location and heavy-duty limit switch demand at coal, iron ore, and bauxite extraction sites across Jharkhand, Odisha, and Chhattisgarh industrial mining clusters.

South Korea Smart Factory Push Fuels Limit Switch Demand

South Korea contributes approximately 12% of the Asia Pacific limit switch market revenues in 2026, representing an estimated US$ 467 million, expanding at an estimated CAGR of approximately 12.2% in the coming years.

South Korea's limit switch market is driven by the country's K-Smart Factory government programme, which targets the conversion of 30,000 small and medium-sized manufacturing enterprises into smart factories by 2025, embedding automated position sensing and safety interlock systems as standard, and the world-class electronics and semiconductor manufacturing infrastructure of Samsung Electronics and SK Hynix that operates hundreds of highly automated fabrication facilities requiring continuous high-precision limit switch deployment.

South Korea's shipbuilding sector, the world's second largest, led by HD Hyundai Heavy Industries and Samsung Heavy Industries, is a significant heavy-duty and hazardous location limit switch consumer, deploying certified sensing components across crane, hoist, and cargo handling systems at shipyard and offshore platform construction facilities.

Competitive Landscape

The global limit switches market is moderately consolidated at the premium branded tier, with Omron Corporation, Honeywell International, Schneider Electric (Telemecanique), Siemens AG, Eaton Corporation, and ABB Ltd. collectively holding approximately 55–60% of global revenues. Key differentiators include IEC 60947-5-1 / IEC 60947-5-2 dual certification portfolios, ATEX/IECEx hazardous location approvals, broad actuator variant coverage, and established OEM design-win relationships at global machine builders.

Emerging competitive strategies include the integration of IO-Link digital communication interfaces enabling predictive maintenance diagnostics, condition monitoring, and real-time positional data reporting a technology differentiator that is reshaping premium-tier competition. The mid-market and regional tier remains fragmented, with CHINT, DELIXI, and multiple Asian domestic manufacturers competing on price-driven specification at volume automation tiers in China, India, and ASEAN markets.

Key Developments:

- March 2025: Omron Corporation launched the D4SL-NK safety limit switch series featuring enhanced IEC 60947-5-3 positive-opening certification and integrated IO-Link digital diagnostic output, targeting smart factory safety gate and access control applications across automotive and electronics OEM equipment builders.

- October 2024: Honeywell International expanded its HDLS Series of explosion-proof heavy-duty limit switches with new IECEx Zone 1 and ATEX Category 1GD dual-certified variants, targeting LNG terminal and chemical plant applications across the Middle East and Asia Pacific, where simultaneous multi-standard certification is a mandatory procurement requirement.

- June 2024: Siemens AG integrated TIA Portal connectivity and IO-Link master compatibility into its 3SE5 SIRIUS heavy-duty limit switch range, enabling real-time actuation cycle counting, wear diagnostics, and predictive maintenance alert generation within Siemens SIMATIC PLC architectures at steel mills and automotive body shop installations.

Companies Covered in Limit Switches Market

- Omron Corporation

- Honeywell International Inc.

- Schneider Electric SE (Telemecanique)

- Siemens AG

- Eaton Corporation plc

- ABB Ltd.

- Rockwell Automation Inc.

- Emerson Electric Co.

- Pepperl+Fuchs SE

- SICK AG

- Balluff GmbH

- Schmersal Group

- CHINT Group

- DELIXI Electric

- Bernstein AG

Frequently Asked Questions

The global limit switches market is expected to be valued at US$ 11.8 billion in 2026 and is projected to reach US$ 21.9 billion growing at a CAGR of 9.2% over the forecast period, representing a cumulative incremental opportunity of US$ 10.1 billion sustained by accelerating industrial automation investment globally.

The primary drivers are the global transition to Industry 4.0 smart manufacturing, with the International Federation of Robotics (IFR) confirming record 500,000+ annual industrial robot installations in 2023 and mandatory industrial safety standards, including OSHA 1910.217, IEC 60947-5-1, and ATEX Directive 2014/34/EU that legally require limit switch deployment across a broad range of production equipment and hazardous location installations globally.

Compact limit switches lead the application segment with approximately 44% global market share in 2025, specified by default across the widest range of industrial automation equipment from CNC machine tools and injection moulding machines to packaging and conveyor systems supported by comprehensive OEM product catalogues from Omron, Schneider Electric (Telemecanique), and Siemens that ensure broad availability and design engineer familiarity at global machine builder specification tiers.

Asia Pacific leads the global limit switches market with approximately 36% share in 2026, driven by China's world-leading industrial robot deployment density (over 290,000 units annually, IFR), India's PLI Scheme-backed greenfield manufacturing investment generating new equipment installation demand, and South Korea's K-Smart Factory programme systematically upgrading 30,000 SMEs to automated production environments requiring position sensing and safety interlock components.

The highest-value opportunity is hazardous location limit switches for LNG and chemical process infrastructure, where the IEA's projected 50%+ global LNG capacity expansion by 2030 and mandatory ATEX/IECEx dual certification requirements create premium ASP procurement growing at a positive CAGR with barriers to entry from non-certified competitors delivering higher margins for approved suppliers at EPC contractor procurement programs globally.