- Pharmaceuticals

- Keloid Treatment Market

Keloid Treatment Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Keloid Treatment Market by Treatment Type (Occlusive Dressing, Compression Therapy, Cryosurgery, Excision, Radiation Therapy, Laser Therapy, Interferon Therapy, Intralesional Corticosteroid Injections, Others), End-user (Hospitals, Dermatology Clinics, Ambulatory Surgical Centers, Others), and Regional Analysis, 20262033

Keloid Treatment Market Share and Trends Analysis

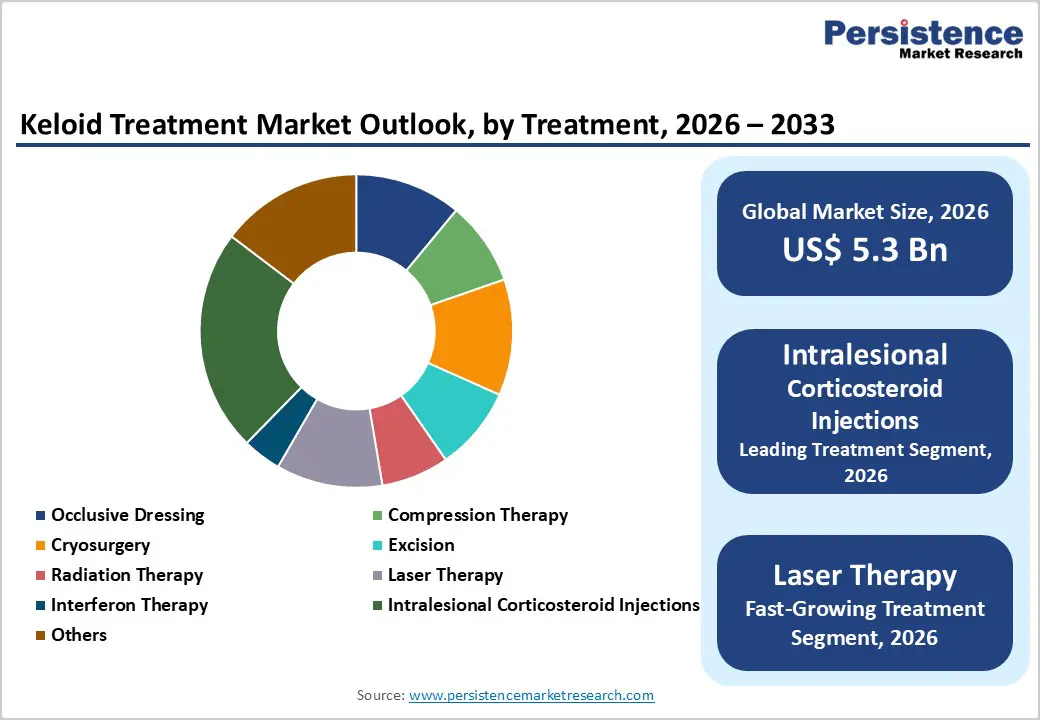

The global keloid treatment market size is expected to be valued at US$ 5.3 billion in 2026 and projected to reach US$ 7.1 billion by 2033, growing at a CAGR of 4.1% between 2026 and 2033. The market growth is primarily driven by the rising prevalence of keloids among populations with darker skin tones, combined with technological advancements in minimally invasive treatment options.

According to clinical epidemiological data, the global prevalence of keloids is estimated at 2-4%, affecting approximately 150-300 million people worldwide. This substantial patient population, coupled with increasing awareness of advanced treatment methodologies and expanding healthcare infrastructure in emerging markets, is creating significant demand for effective keloid management solutions across dermatology clinics, hospitals, and ambulatory surgical centers.

Key Industry Highlights:

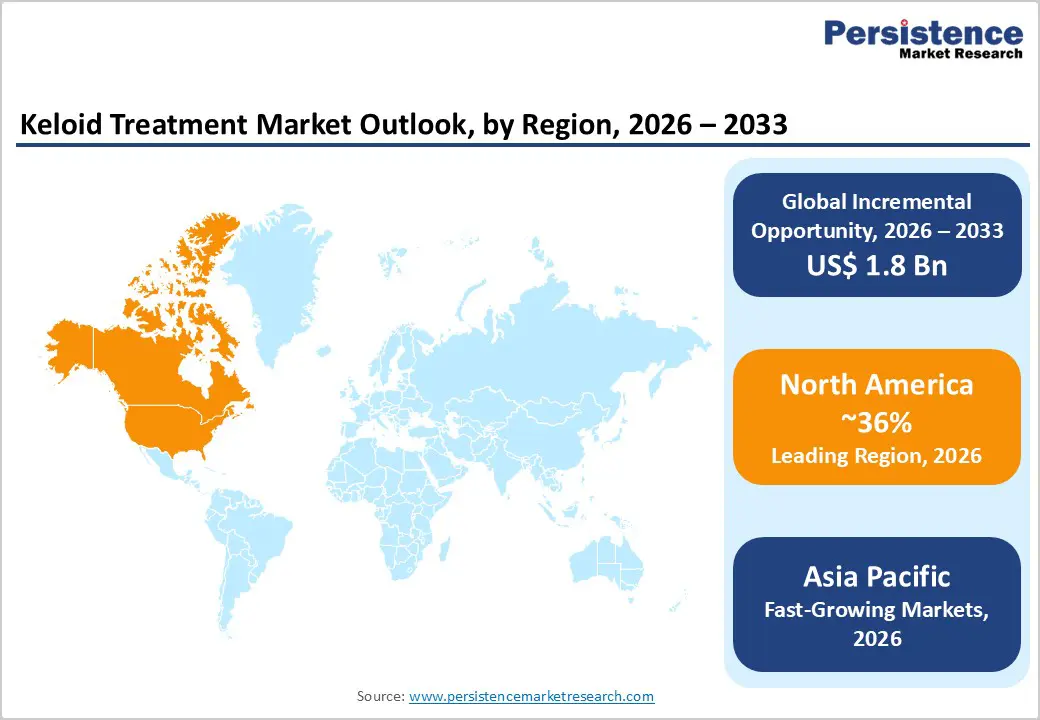

- North America leads the global keloid treatment market with 36% share in 2025, supported by advanced healthcare infrastructure, high spending, strong specialist presence, and favorable regulatory frameworks enabling rapid adoption of innovative therapies.

- Asia-Pacific is the fastest-growing region, driven by large genetically susceptible populations, expanding healthcare infrastructure, and rising expenditure, with China (4.6% CAGR) and India (5.4% CAGR) outpacing global growth.

- Intralesional corticosteroid injections dominate with 23% market share in 2025, owing to proven efficacy, affordability, ease of use, and broad clinical adoption worldwide.

- Laser therapy is the fastest-growing treatment segment (2026–2033), fueled by technological advances, superior cosmetic outcomes, minimal downtime, and expanding use across developed and emerging markets.

- Digital dermatology and telemedicine are emerging as key growth enablers, improving access through AI-assisted diagnosis, personalized care, and remote monitoring, especially in underserved regions.

| Key Insights | Details |

|---|---|

| Market Size (2026E) | US$ 5.3 Billion |

| Market Value Forecast (2033F) | US$ 7.1 Billion |

| Projected Growth CAGR (2026-2033) | 4.1% |

| Historical Market Growth (2020-2025) | 3.7% |

Market Dynamics

Drivers - Rising Prevalence of Keloids in Darker Skin Population

The epidemiological burden of keloids remains disproportionately high among individuals with darker skin phototypes. Clinical research demonstrates that African Americans experience keloid prevalence rates 5 to 16 times higher than Caucasian populations, while Asian and Latino populations also show significantly elevated incidence rates ranging from 4.5% to 16%. This genetic predisposition is further amplified by occupational hazards, surgical procedures, and traumatic injuries more prevalent in developing regions. The National Health Insurance Database from Korea documented that patients with atopic dermatitis exhibit 2.8 times higher risk of keloid development, establishing comorbidity as a critical market driver. As awareness campaigns in developing nations increase diagnosis rates and healthcare accessibility improves in Asia-Pacific, Latin America, and Middle East & Africa, patient demand for professional keloid treatment is accelerating substantially.

Technological Advancement in Minimally Invasive Treatment Modalities

Innovation in laser technology, radiation therapy, and combination treatment approaches is transforming keloid management protocols and expanding treatment efficacy benchmarks. Superficial Radiotherapy (SRT) technology, such as the SRT-100 system developed by Sensus Healthcare, demonstrates a recurrence rate as low as 10% when combined with punch excision, compared to 90% recurrence rates with surgical excision alone. Advanced pulsed dye lasers (PDL), CO2 lasers, and fractional laser systems are gaining adoption across North American and European dermatology clinics due to their ability to target fibrotic collagen without extensive surrounding tissue trauma. Intralesional corticosteroid injections, particularly triamcinolone acetonide (TAC), combined with laser therapy, achieve 75-82.7% reduction in keloid size within 2-5 treatment sessions. These technological breakthroughs are reducing patient discomfort, minimizing downtime, and improving treatment outcomes, thereby driving physician adoption and patient demand across all end-user segments.

Restraints - High Treatment Costs and Limited Insurance Coverage

The financial burden associated with advanced keloid treatments remains a significant barrier to market penetration, particularly in developing economies. Multi-session treatment protocols using laser therapy, radiation therapy, or combination approaches often exceed US$3,000 to US$10,000 per patient course, creating affordability challenges in regions with lower healthcare spending per capita. Insurance coverage variability across jurisdictions with many insurers classifying keloid treatment as cosmetic rather than medical restricts reimbursement availability. In African markets, treatment accessibility is severely constrained by the high financial cost of professional keloid care, limiting patient seeking behavior despite the 6-16% prevalence burden documented in the black African population. This economic constraint disproportionately affects lower-income populations who represent a substantial portion of keloid-affected demographics, thereby capping market expansion in price-sensitive regions.

Opportunity - Rapid Growth of Laser Therapy as Fastest-Growing Treatment Segment

Laser therapy is emerging as the fastest-growing treatment segment with accelerating CAGR during the 2026-2033 forecast period, driven by technological refinement, improved safety profiles, and superior cosmetic outcomes. Advanced laser modalities, including fractional ablative lasers, pulsed dye lasers (PDL), and non-ablative infrared systems, are increasingly adopted across North American and European dermatology clinics and medical aesthetics centers. Research published in Dermatologic Therapy demonstrates that laser therapy combined with excision and radiation therapy achieves superior scar appearance and functional outcomes compared to monotherapy approaches. The medical aesthetics market in Asia-Pacific, particularly in China, India, and Southeast Asia, is witnessing explosive growth in demand for cosmetic dermatology procedures, creating significant utilization opportunities for laser-based keloid treatment. The non-invasive nature, minimal downtime, and customizable treatment parameters of laser systems are driving adoption among younger demographics and physicians seeking cost-effective, high-efficacy treatment options.

Expansion of Digital Dermatology and Telemedicine for Keloid Diagnosis and Treatment Planning

Digital health technologies and teledermatology platforms are revolutionizing keloid diagnosis, treatment planning, and post-treatment monitoring, particularly in underserved regions. Artificial Intelligence-assisted keloid evaluation tools enable standardized assessment, precise measurement, and personalized treatment planning, reducing inter-operator variability and improving clinical outcomes. Telemedicine platforms facilitate remote consultations, reducing geographical barriers for patients in rural and underserved areas accessing specialized dermatological expertise.

Healthcare providers in Asia-Pacific markets, particularly in India and Southeast Asia, are leveraging digital health infrastructure to enhance dermatology service accessibility and increase professional keloid treatment adoption. The integration of AI-powered laser prohibition targeting, at-home laser therapy devices for mild keloid scars, and digital wound monitoring systems is expanding the accessible patient population beyond traditional clinical settings. This technological democratization of keloid treatment delivery creates significant market expansion opportunities, particularly in emerging markets where healthcare infrastructure and specialist availability remain constrained.

Category-wise Analysis

Treatment Type Insights

Intralesional corticosteroid injections command a leading 23% market share in 2025, establishing this modality as the dominant treatment segment across all geographic regions and end-user settings. The clinical supremacy of intralesional corticosteroid administration (ICA) is grounded in multiple mechanisms: inhibition of leukocyte and monocyte migration reducing inflammation, increased vasoconstriction limiting oxygen and nutrient delivery to fibrotic tissue, and suppression of keratinocyte and fibroblast proliferation preventing new collagen synthesis. Triamcinolone acetonide (TAC), used by 95.6% of dermatologists in clinical practice according to peer-reviewed surveys, provides extended tissue residence time and prolonged therapeutic action compared to alternative corticosteroids.

Research demonstrates 82.7% reduction in keloid size between initial and final treatment sessions, with median treatment doses ranging from 4 mg to 40 mg per session across 1-5 treatment cycles. The affordability, ease of administration in office-based settings, minimal downtime, and widespread clinical familiarity position intralesional corticosteroid injections as the preferred first-line treatment modality across hospitals, dermatology clinics, and ambulatory surgical centers, justifying its dominant market position.

End-user Insights

By end-user category hospitals and dermatology clinics serve as primary treatment centers, offering comprehensive, multi-modal therapeutic approaches combining intralesional injections, laser therapy, radiation therapy, and surgical interventions. Ambulatory Surgical Centers (ASCs) are increasingly emerging as specialized facilities for minimally invasive keloid procedures, providing cost-effective laser therapy, radiation therapy, and combination treatment protocols with reduced patient burden.

The proliferation of dedicated dermatology clinics and medical aesthetics centers across North America (accounting for 36% market share) and Asia Pacific is driving treatment accessibility and adoption. Others category encompassing private dermatological practices, plastic surgery clinics, and emerging telemedicine platforms is experiencing rapid growth, particularly in capturing younger demographics seeking cosmetic dermatology solutions. The competitive positioning among end-user categories reflects regional healthcare infrastructure development, specialist availability, insurance reimbursement policies, and patient preference for specialized versus general healthcare settings.

Regional Insights

North America Keloid Treatment Market Trends

North America remains the leading region in the keloid treatment market, driven by its advanced healthcare infrastructure, high patient awareness, and strong demand for both medical and aesthetic scar solutions. The United States, in particular, contributes the largest share with widespread adoption of innovative treatment options such as laser therapy, intralesional corticosteroid injections, silicone?based products, and combination therapies offered across hospitals, dermatology clinics, and ambulatory centres.

High disposable income, robust insurance coverage, and favorable regulatory frameworks support broader access to cutting?edge modalities, while a culturally diverse population with a significant incidence of keloids further boosts demand. The region also benefits from significant R&D investment and a strong presence of key market players that continuously introduce new therapies and scar management products. Consumer interest in non?invasive, cosmetically effective treatments and the growth of over?the?counter options through retail and e?commerce channels are additional trends shaping market growth.

Asia Pacific Keloid Treatment Market Trends

Asia Pacific is emerging as a fast?growing and increasingly important market in the global keloid treatment industry, driven by rising incidence of skin injuries, burns, acne?related scarring, and heightened awareness of treatment options. Countries like China, India, Japan, and South Korea are witnessing significant uptake of both traditional therapies (such as corticosteroid injections and cryotherapy) and advanced modalities like laser treatment, as more clinics and hospitals expand dermatology services across urban centres. The region’s large and diverse population, increasing healthcare spending, and growing demand for aesthetic and minimally invasive solutions are key growth factors. Teledermatology and digital diagnostic tools are also improving access in remote areas, while international skincare and medical aesthetic brands expand their presence. However, uneven access to advanced care in rural zones and varying regulatory environments remain challenges. Overall, Asia Pacific’s keloid treatment market is projected to grow at one of the highest regional rates globally in the coming years.

Competitive Landscape

The keloid treatment market is highly competitive, driven by continuous innovation and the introduction of advanced therapies. Companies focus on developing more effective, safer, and patient-friendly solutions across surgical, non-surgical, and combination modalities. Key strategies include expanding product portfolios, enhancing clinical efficacy, and improving accessibility through diverse distribution channels such as hospitals, dermatology clinics, and online platforms. Technological advancements in laser therapy, cryotherapy, and biologic treatments are shaping market dynamics, while emphasis on non-invasive and cosmetically favorable options attracts growing patient demand.

Key Market Developments

- In August 2025, CUTERA, INC., launched its breakthrough skin revitalization portfolio, Secret by Cutera, in Australia and New Zealand. This milestone marked a significant step in the company’s global expansion strategy and strengthened its position as a worldwide leader in clinically proven, practitioner-first skin technology.

Companies Covered in Keloid Treatment Market

- Novartis AG

- Sensus Healthcare

- RXi Pharmaceuticals, Inc.

- Sonoma Pharmaceuticals, Inc.

- Perrigo Company plc.

- Bristol-Myers Squibb Company

- Pacific World Corporation

- Valeant Pharmaceuticals International, Inc.

- Revitol Corporation

- Avita Medical Limited

Frequently Asked Questions

The global Keloid Treatment Market is expected to be valued at US$ 5.3 billion in 2026, growing from US$ 4.3 billion in 2020, representing substantial market expansion driven by rising prevalence, technological advancement, and increased treatment accessibility across regions.

The market growth is primarily driven by the exceptionally high prevalence of keloids among populations with darker skin phototypes (5-16 times higher in African Americans compared to Caucasians), technological advancement in minimally invasive treatment modalities including laser therapy and radiation therapy, expanding healthcare infrastructure in emerging markets, increasing patient awareness of professional treatment options, and growing adoption of combination therapy protocols improving clinical outcomes.

North America maintains market dominance with 36% market share in 2025, leveraging advanced healthcare infrastructure, high healthcare spending per capita, substantial specialist availability, FDA approval pathways for novel treatments, and robust reimbursement frameworks supporting adoption of advanced keloid treatment modalities.

Laser Therapy represents the key market opportunity as the fastest-growing treatment segment, driven by technological refinement, superior cosmetic outcomes, minimal patient downtime, and expanding adoption across medical aesthetics centers, particularly in Asia-Pacific markets experiencing explosive growth in cosmetic dermatology demand and emerging medical tourism sectors.

Key market participants include Novartis AG, Bristol-Myers Squibb Company, Sensus Healthcare, Perrigo Company plc., RXi Pharmaceuticals, Inc., Sonoma Pharmaceuticals, Inc., Avita Medical Limited, and Pacific World Corporation.