- Medical Devices

- INR Test Meter Market

INR Test Meter Market Size, Share, and Growth Forecast 2026 - 2033

INR Test Meter Market by Product (Device, Test Strips, Lancet), End-user (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Homecare Settings), and Regional Analysis, 2026 - 2033

INR Test Meter Market Share and Trends Analysis

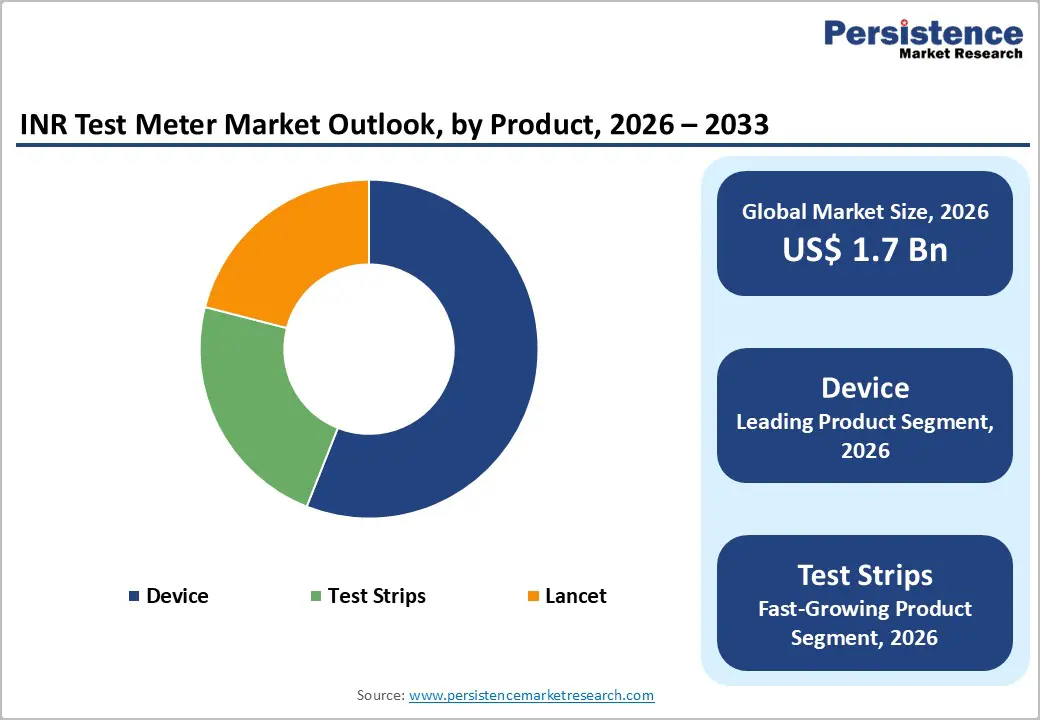

The global INR test meter market size is expected to be valued at US$ 1.7 billion in 2026 and projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

The rising prevalence of cardiovascular diseases requiring long-term anticoagulation therapy is fueling market expansion, as 52.55 million individuals globally suffered from atrial fibrillation and atrial flutter as of 2021, representing a 137% increase from 1990. The aging population, particularly individuals aged 65 years and older who face an exponentially increasing incidence of atrial fibrillation, is driving demand for convenient point-of-care INR (International Normalized Ratio) monitoring devices that enable patient self-management and reduce the burden on healthcare facilities.

Key Industry Highlights:

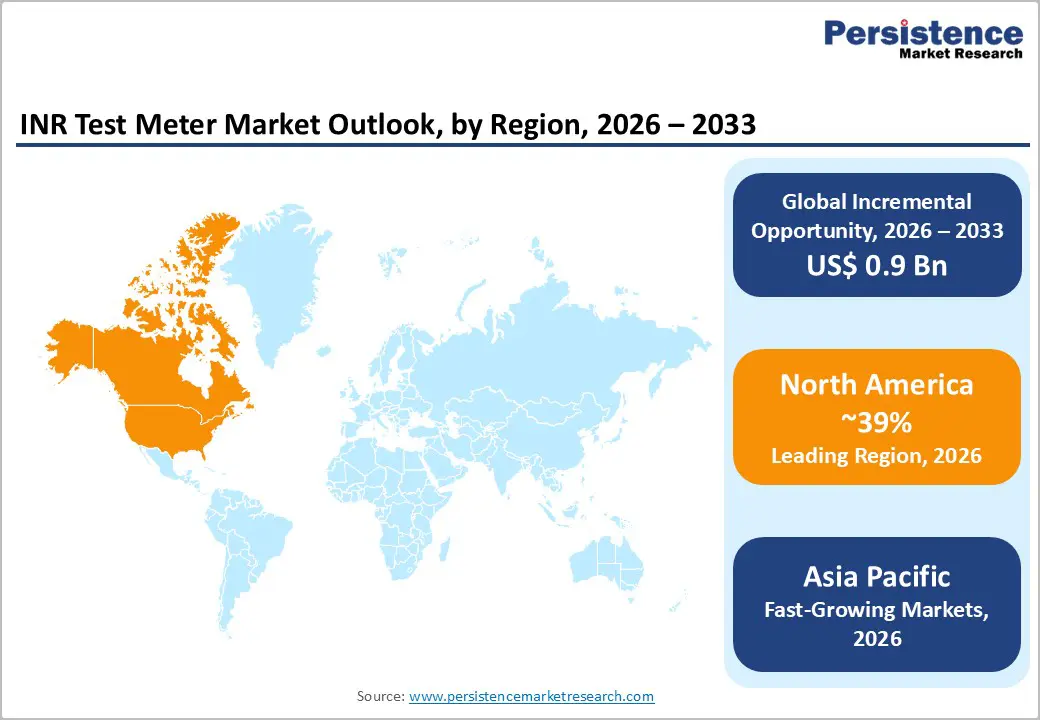

- North America leads with 39% share in 2025, supported by advanced healthcare infrastructure and 8 million projected atrial fibrillation patients by 2050.

- Asia Pacific fastest-growing region driven by demographic transitions across China, Japan, and India.

- Device segment dominates with 56% market share as a foundational technology platform.

- Test Strips are the fastest-growing due to recurring revenue from testing frequency.

- Homecare Settings key opportunity with 79% time in therapeutic range vs 72% conventional care.

| Key Insights | Details |

|---|---|

| INR Test Meter Market Size (2026E) | US$ 1.7 billion |

| Market Value Forecast (2033F) | US$ 2.6 billion |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 5.6% |

Market Dynamics

Drivers - Rise in Burden of Cardiovascular Diseases and Anticoagulation Therapy Requirements

The exponential rise in cardiovascular diseases globally is creating unprecedented demand for INR test meters as essential monitoring tools for patients on vitamin K antagonist therapy, particularly warfarin. According to the World Health Organization, cardiovascular diseases remain the leading cause of death worldwide, with atrial fibrillation affecting an estimated 52.55 million individuals globally as of 2021. The absolute prevalence of atrial fibrillation has nearly doubled from 22.2 million in 1990 to 52.5 million in 2021, demonstrating sustained growth in the patient population requiring anticoagulation monitoring. Furthermore, age-adjusted analysis reveals that individuals aged 70-74 years experienced the highest absolute incidence of atrial fibrillation at 744,978 cases annually, while those aged 90-94 years showed prevalence rates of 11,828 per 100,000 population. The therapeutic requirement for maintaining optimal INR values between 2.0 and 3.0 for most anticoagulation patients necessitates frequent monitoring to balance thromboembolism prevention against hemorrhagic complications, establishing INR test meters as indispensable medical devices in chronic disease management protocols across hospital, clinic, and homecare settings.

Technological Advancements Enabling Patient Self-Management and Telehealth Integration

Rapid innovation in biosensor technology, connectivity features, and miniaturization is transforming INR test meters into sophisticated patient-centric monitoring platforms that facilitate self-testing and remote clinical oversight. Modern devices such as Roche's CoaguChek INRange and Abbott's i-STAT systems incorporate Bluetooth connectivity, smartphone applications, and automated result transmission capabilities that enable seamless data sharing with healthcare providers. The U.S. Food and Drug Administration (FDA) has granted 510(k) clearance to multiple advanced point-of-care coagulation monitoring devices, validating their accuracy and reliability for home-based testing with results available within one minute from just 8 microliters of capillary blood obtained via fingerstick. Clinical studies demonstrate that patient self-testing achieves comparable or superior time in therapeutic range compared to traditional laboratory monitoring, with remote INR monitoring programs associated with higher quality of life and patient satisfaction. The integration of telemedicine platforms accelerated during the COVID-19 pandemic, permanently shifting treatment paradigms toward decentralized care delivery models that rely on portable, user-friendly INR test meter technology.

Restraints - Competition from Novel Oral Anticoagulants Reducing Warfarin Prescriptions

The growing adoption of novel oral anticoagulants (NOACs), including dabigatran, rivaroxaban, apixaban, and edoxaban, poses a significant challenge to INR test meter demand, as these medications do not require routine coagulation monitoring unlike traditional vitamin K antagonists. Healthcare providers increasingly prescribe NOACs as first-line therapy for atrial fibrillation and venous thromboembolism, particularly in developed markets with favorable reimbursement policies, resulting in declining warfarin utilization rates and consequent reduction in INR monitoring frequency among the anticoagulated patient population.

Device Accuracy Concerns and Regulatory Scrutiny

Persistent concerns regarding the accuracy and reliability of point-of-care INR test meters have prompted heightened regulatory oversight from agencies, including the FDA, which has documented multiple instances of erroneous patient results leading to serious adverse events. The FDA has specifically highlighted challenges in evaluating substantial equivalence of prothrombin time/INR devices, noting that accuracy, reliability, result reporting, and device usability issues have led to incorrect dosing decisions with potentially life-threatening consequences. While modern devices demonstrate improved performance, with studies showing 97% correlation with laboratory results using standardized reagents, the narrow therapeutic window of warfarin therapy means even minor measurement discrepancies can result in subtherapeutic anticoagulation, increasing thromboembolism risk, or supratherapeutic values, elevating bleeding complications.

Opportunities

Expansion of Homecare Settings and Patient Self-Testing Adoption

The accelerating shift toward patient-centric care delivery models presents substantial growth opportunities for INR test meter manufacturers targeting the rapidly expanding home care segment, where self-monitoring capabilities offer improved convenience, reduced healthcare costs, and enhanced patient autonomy. Healthcare systems globally are recognizing that patient self-testing programs achieve superior therapeutic outcomes compared to conventional office-based monitoring.

Evidence from multiple clinical trials demonstrates that home INR testing increases time in therapeutic range from approximately 72% to 79%, translating to meaningful reductions in major bleeding events and thromboembolic complications. The integration of remote monitoring services enables healthcare providers to receive automated alerts when patient results fall outside prescribed therapeutic ranges, facilitating timely intervention without requiring physical clinic visits. Regulatory frameworks in developed markets, including the United States, Germany, the United Kingdom, and France, increasingly support reimbursement for patient self-testing equipment and supplies. The demographic reality of aging populations, particularly the projected increase of atrial fibrillation patients to over 8 million in the United States by 2050, combined with chronic healthcare workforce shortages, positions homecare-based INR monitoring as a scalable solution.

Category-wise Insights

By Product

The Device segment maintains a dominant market position, accounting for approximately 56% share in 2025, driven by the critical role of portable INR meters as the foundational technology platform enabling point-of-care coagulation monitoring across clinical and home settings. Leading devices including Roche CoaguChek INRange, Roche CoaguChek XS, Abbott i-STAT PT/INR incorporate advanced electrochemical detection methods using human recombinant thromboplastin to determine prothrombin time with international sensitivity index values of approximately 1.0, ensuring standardized INR calculations comparable to central laboratory analyzers. The FDA's CLIA waiver status granted to devices like the CoaguChek XS system facilitates deployment in low-complexity testing environments, including physician offices and pharmacies. Modern meter technology delivers results within 60 seconds from minimal blood volumes of 8 microliters. However, the Test Strips segment represents the fastest-growing product category with higher CAGR between 2025-2032, reflecting the consumable nature of testing supplies that generate recurring revenue streams proportional to testing frequency.

By End-user

Hospitals constitute the leading end-user segment in the INR test meter market, leveraging point-of-care testing capabilities to expedite clinical decision-making for patients presenting to emergency departments, perioperative settings, and inpatient cardiology units where immediate coagulation status assessment is critical for treatment protocols. Hospital-based anticoagulation clinics serve as centralized management hubs where multidisciplinary teams monitor hundreds of patients on warfarin therapy, utilizing professional-grade devices such as the Roche CoaguChek XS Pro system with barcode reader functionality that integrates with electronic medical records. However, Homecare Settings are emerging as the fastest-growing end-user segment, propelled by the paradigm shift toward patient self-management models that empower individuals to assume direct responsibility for their anticoagulation monitoring using FDA-cleared consumer devices. Remote monitoring programs such as Abbott's Acelis Connected Health service provide training, equipment, supplies, and clinical oversight infrastructure that enables safe and effective home testing. Clinical evidence demonstrates that patient self-testing achieves time in therapeutic range of approximately 79% compared to 72% with conventional care.

Regional Insights

North America INR Test Meter Market Trends and Insights

North America commands the largest regional market share at approximately 39% in 2025, underpinned by the region's advanced healthcare infrastructure, high prevalence of cardiovascular diseases, robust reimbursement frameworks, and established clinical protocols incorporating point-of-care coagulation monitoring into standard anticoagulation management pathways.

The United States demonstrates particularly strong market characteristics, with cardiovascular diseases representing the leading cause of mortality and atrial fibrillation projected to affect over 8 million individuals by 2050. The regulatory environment facilitated by FDA 510(k) clearances has enabled widespread adoption across diverse care settings, while commercial and government insurance programs, including Medicare, provide coverage for patient self-testing equipment.

The region benefits from sophisticated anticoagulation clinic networks and telemedicine infrastructure that support both professional point-of-care testing and patient self-management programs. Major manufacturers, including Roche Diagnostics and Abbott Laboratories, maintain significant North American market presence. Recent developments include the March 2025 launch of Roche's CoaguChek Pro II, reflecting ongoing industry investment in product enhancement.

Asia Pacific INR Test Meter Market Trends and Insights

Asia Pacific INR test meter market is emerging as a significant growth region due to the rising burden of cardiovascular disorders and increasing demand for anticoagulation monitoring. Countries such as China, India, Japan, and South Korea are witnessing higher cases of atrial fibrillation, deep vein thrombosis, and heart valve diseases, which require regular monitoring of blood coagulation levels. Growing healthcare awareness and improvements in diagnostic infrastructure are encouraging the adoption of point-of-care coagulation testing devices.

Additionally, expanding healthcare investments and government initiatives aimed at strengthening chronic disease management are supporting market growth across the region. Hospitals and diagnostic laboratories are increasingly integrating portable INR testing meters to deliver faster results and improve treatment decision-making. The rising preference for home-based healthcare and self-monitoring devices is also contributing to the demand for compact and user-friendly INR meters. Furthermore, the presence of a large aging population and increasing healthcare expenditure are accelerating the uptake of advanced diagnostic technologies. As healthcare systems in the region continue to modernize and accessibility to diagnostic services improves, the Asia Pacific market is expected to witness steady expansion in the coming years.

Competitive Landscape

The INR Test Meter Market is characterized by a moderately competitive environment where manufacturers focus on product innovation, technological advancement, and expansion of distribution networks. Companies are investing in the development of compact, portable, and user-friendly meters that support rapid point-of-care coagulation testing. The increasing demand for home-based monitoring and digital health integration has encouraged the introduction of devices with improved connectivity and data management features. Market participants also emphasize strategic partnerships, regulatory approvals, and geographic expansion to strengthen their presence in emerging healthcare markets.

Key Developments:

- In November 2025, Thermo Fisher Scientific invested approximately INR 85-90 crore to establish a Customer Experience Centre and Bioprocess Design Centre in Genome Valley, Hyderabad. The facility was inaugurated by Telangana’s IT Minister D. Sridhar Babu and was developed to support biopharma research, process development, and workforce training. The centres enabled scientists and industry partners to design, optimize, and scale biologics, vaccines, and advanced therapy manufacturing processes, strengthening India’s life sciences innovation ecosystem and supporting the growth of the country’s biopharmaceutical sector.

Companies Covered in INR Test Meter Market

- Thermo Fisher Scientific

- Merck KGaA

- Bio-Rad Laboratories

- F. Hoffmann-La Roche Ltd.

- QIAGEN

- Danaher

- Miltenyi Biotec

- Claremont BioSolutions

- IDEX

- Parr Instrument Company

- Covaris

- Cell Signaling Technology

- Qsonica

- Roche Diagnostics

- Abbott Laboratories

- Werfen

- Sysmex Corporation

- Siemens Healthineers

Frequently Asked Questions

The global INR test meter market is expected to be valued at US$ 1.7 billion in 2026.

Escalating atrial fibrillation burden affecting 52.55 million globally and technological advancements enabling 79% time in therapeutic range through patient self-testing.

North America leads with 39% market share, supported by FDA clearances and Medicare reimbursement.

Homecare settings expansion with superior clinical outcomes (79% vs 72% therapeutic range), addressing aging demographics.

Roche Diagnostics (CoaguChek), Abbott Laboratories (i-STAT), Werfen, Sysmex, Siemens Healthineers dominate through innovation and service platforms3.