- Pharmaceuticals

- Inhaled Anti-Infectives Market

Inhaled Anti-Infectives Market Size, Share, and Growth Forecast, 2026 – 2033

Inhaled Anti-Infectives Market by Product Type (Antibiotics, Antifungals, Antivirals, Combination Therapies), Application (Pneumonia, Asthma, Bronchitis), and Regional Analysis for 2026 – 2033

Inhaled Anti-Infectives Market Size and Trends Analysis

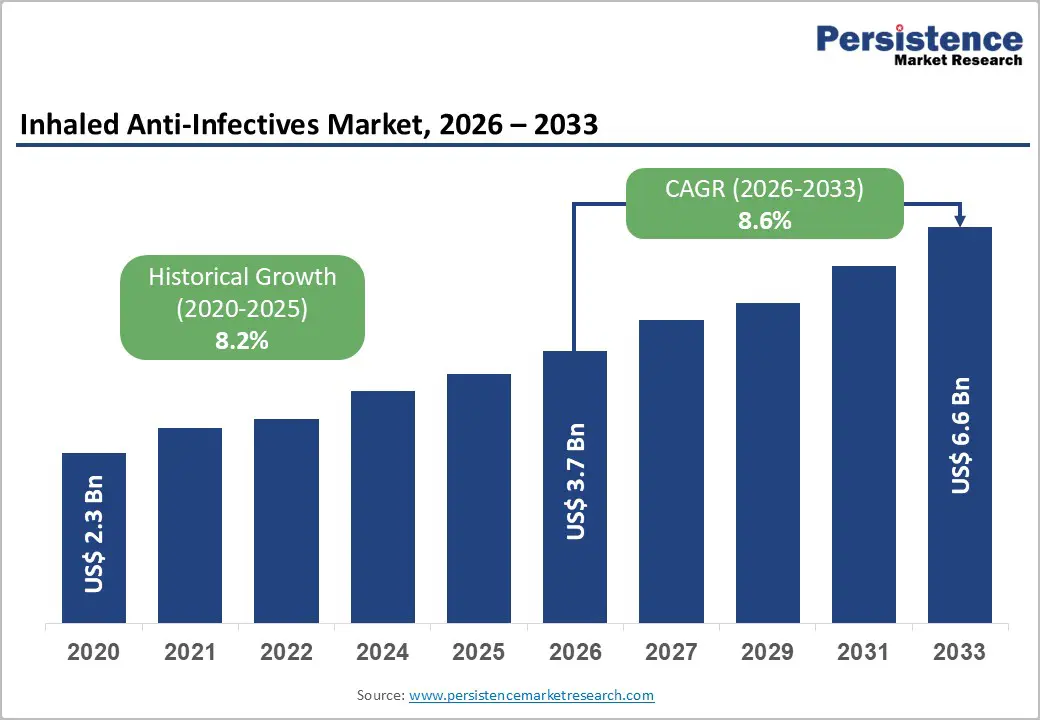

The global inhaled anti-infectives market size is likely to be valued at US$3.7 billion in 2026 and is expected to reach US$6.6 billion by 2033, growing at a CAGR of 8.6% during the forecast period from 2026 to 2033, driven by the rising prevalence of respiratory infections and chronic lung diseases, including cystic fibrosis, bronchiectasis, pneumonia, and hospital-acquired infections, which require targeted lung therapy. Advancements in inhalation drug delivery systems such as nebulizers, soft mist inhalers, and dry powder inhalers have enhanced lung deposition, improved efficacy, and reduced systemic side effects, increasing adoption. There is a growing focus on managing chronic and difficult-to-treat infections, supported by increasing clinical evidence, favorable patient outcomes, and expanding use in specialized healthcare settings.

Key Industry Highlights:

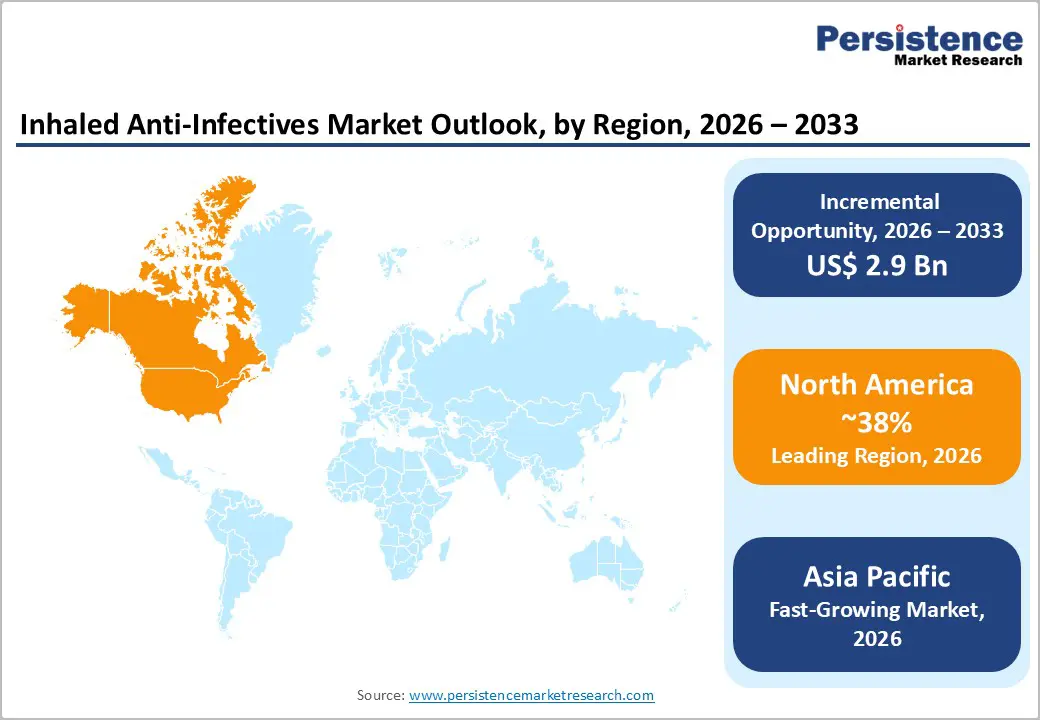

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by advanced healthcare infrastructure and high adoption of inhaled therapies.

- Fastest-growing Region: Asia Pacific, driven by rising healthcare expenditure, increasing respiratory infections, and supportive government initiatives.

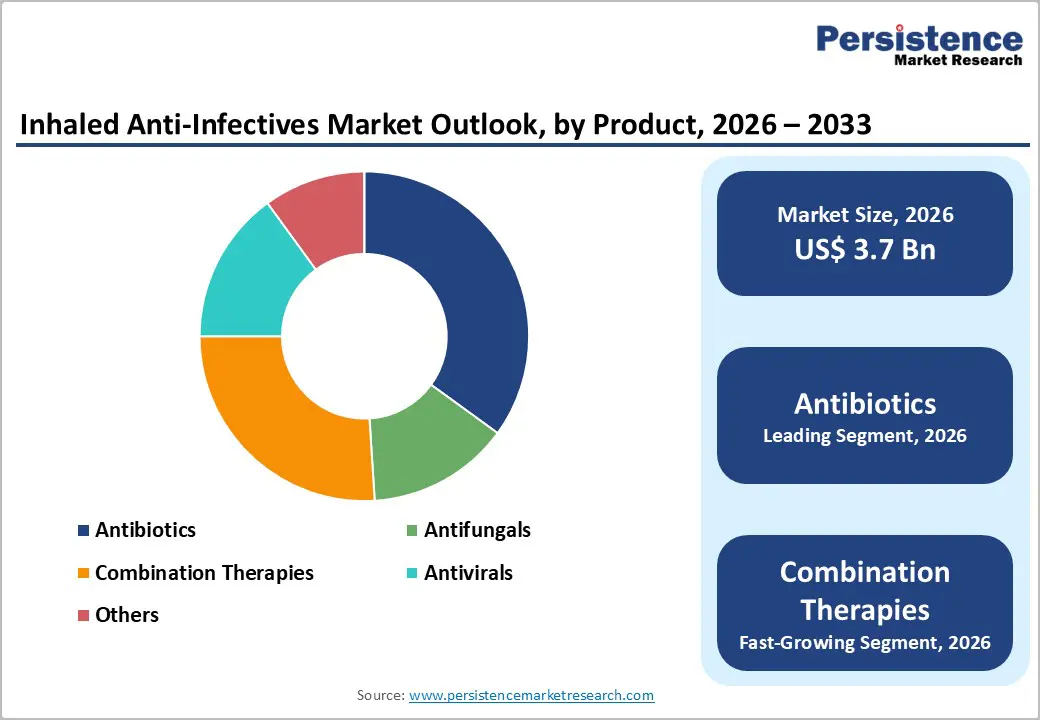

- Leading Product Type: Antibiotics are projected to represent the leading product type in 2026, accounting for 45% of the revenue share, driven by their established use in bacterial respiratory infections and proven efficacy in chronic conditions.

- Leading Application: Pneumonia is anticipated to be the leading application type, accounting for over 50% of the revenue share in 2026, supported by the high incidence of bacterial and hospital-acquired cases requiring targeted inhaled therapy.

| Report Attribute | Details |

|---|---|

|

Inhaled Anti-Infectives Market Size (2026E) |

US$3.7 Bn |

|

Market Value Forecast (2033F) |

US$6.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Respiratory Infections and Chronic Lung Conditions

Respiratory infections such as pneumonia, tuberculosis, and ventilator-associated infections cause substantial morbidity and mortality, particularly among vulnerable populations including children, older adults, and immunocompromised individuals. Hospital-acquired infections, frequently driven by multidrug-resistant pathogens, are increasingly managed with inhaled therapies that deliver high concentrations of drugs directly to the lungs, enhancing therapeutic effectiveness while limiting systemic exposure. One of the most serious and life-threatening respiratory conditions is chronic obstructive pulmonary disease (COPD), which is associated with premature mortality and high death rates. COPD primarily includes emphysema and chronic bronchitis. According to the World Health Organization (2021), asthma affects approximately 4.3% of the population.

Chronic lung diseases also play a significant role in driving market growth by creating sustained demand for long-term maintenance and preventive treatments. Conditions such as COPD and cystic fibrosis lead to progressive lung damage, airway obstruction, and increased vulnerability to bacterial, viral, and fungal infections. Inhaled anti-infective therapies offer a targeted approach by acting directly at the site of infection, thereby improving clinical outcomes and minimizing systemic adverse effects. As reported by the Forum of International Respiratory Societies (FIRS) (2024), more than 200 million people worldwide suffer from COPD, a condition projected to become the third leading cause of death. As a result, healthcare systems are placing greater emphasis on early diagnosis and chronic disease management, contributing to increased prescription and utilization of inhaled anti-infective therapies.

High Development and Regulatory Hurdles

The development of inhaled anti-infective therapies involves extensive formulation optimization to ensure appropriate particle size for deep lung deposition, adequate stability, preserved potency, and minimal airway irritation. Unlike oral or intravenous products, inhaled formulations must meet strict aerosol performance criteria, including precise particle size distribution, aerodynamic properties, and consistent dose delivery. Achieving these requirements relies on advanced delivery technologies such as nebulizers, dry powder inhalers, and soft-mist inhalers, which significantly increase research, development, and manufacturing costs. Clinical trials for inhaled therapies are more complex, as they must assess not only safety and efficacy but also lung deposition characteristics, local tolerability, and potential long-term pulmonary effects.

Regulatory challenges constrain the inhaled anti-infectives market. Regulatory bodies such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and other national authorities demand extensive safety and efficacy data before approval, often requiring more rigorous evaluation than for conventional formulations. Inhaled anti-infectives undergo detailed assessment for local and systemic toxicity, immunogenic responses, and possible adverse pulmonary outcomes, which lengthens development timelines and increases overall costs. Differences in regulatory requirements across regions complicate global commercialization, necessitating customized regulatory submissions for each market. Post-marketing surveillance and ongoing pharmacovigilance requirements also impose additional operational and financial responsibilities on manufacturers.

Expansion in Emerging Markets and Chronic Disease Management

Countries in the Asia Pacific region and Latin America are experiencing a rising prevalence of respiratory infections and chronic lung diseases, driven by urbanization, increasing pollution, smoking, and aging populations. As per the World Health Organization (May 2024, asthma is the most common chronic disease among children worldwide, with approximately 339 million people living with the condition. Governments in these regions are investing in healthcare infrastructure, improving access to advanced therapies, and promoting local pharmaceutical manufacturing to reduce costs. Lower-cost inhalation devices, coupled with affordable drug formulations, have increased accessibility and adoption among patients in outpatient and home care settings. Rising awareness about respiratory health and preventive care has encouraged early diagnosis and treatment, driving the demand for inhaled anti-infectives.

Chronic disease management also significantly contributes to market growth, as conditions such as cystic fibrosis, chronic obstructive pulmonary disease (COPD), asthma, and bronchiectasis require long-term and often repeated treatment. Inhaled anti-infectives provide a targeted approach, delivering high drug concentrations directly to the lungs, reducing systemic side effects, and improving patient adherence compared to oral or intravenous alternatives. With the rise in chronic respiratory disease prevalence, particularly in emerging markets, healthcare providers are increasingly focusing on preventive strategies and continuous management of exacerbations, which drives prescription rates. Clinical evidence supporting the efficacy of inhaled therapies in reducing hospitalizations and improving quality of life reinforces adoption.

Category-wise Analysis

Product Type Insights

The antibiotics segment is expected to lead the inhaled anti-infectives market, accounting for approximately 45% of revenue in 2026, driven by their long-standing use in treating bacterial respiratory infections, particularly in chronic conditions such as cystic fibrosis and bronchiectasis. Inhaled antibiotics such as tobramycin and colistin are commonly prescribed owing to their demonstrated effectiveness in reducing pulmonary exacerbations, enhancing lung function, and lowering rates of hospitalization. Strong clinical evidence supporting these treatments leads clinicians to favor antibiotics over other inhaled anti-infective options, positioning them as a dependable cornerstone of chronic disease management. Inhaled antibiotics benefit from established regulatory pathways and mature manufacturing processes, allowing for efficient large-scale production and broad market availability.

Combination therapies are likely to represent the fastest-growing segment in 2026, supported by the increasing need for multi-pathogen coverage and effective management of antimicrobial resistance in complex respiratory infections. These therapies are designed to deliver multiple active agents in a single inhalation, providing multi-pathogen coverage and addressing antimicrobial resistance in complex respiratory infections. For example, combination formulations such as tobramycin with colistin or amikacin are increasingly being evaluated in clinical trials for cystic fibrosis and ventilator-associated pneumonia, demonstrating enhanced efficacy and reduced exacerbation rates. The growth of combination therapies is fueled by rising awareness of resistant pathogens, the need for more comprehensive treatment regimens, and the expansion of inhalation technologies capable of delivering multiple drugs simultaneously.

Application Insights

Pneumonia is projected to lead the market, capturing around 50% of the revenue share in 2026, supported by the high prevalence of bacterial and hospital-acquired cases requiring targeted inhaled therapy. Inhaled antibiotics are particularly effective for ventilator-associated pneumonia (VAP), delivering high drug concentrations directly to the infection site, which enhances bacterial clearance and reduces systemic toxicity. Hospitals and intensive care units extensively use inhaled therapies for critically ill patients, with products such as inhaled tobramycin showing significant improvement in clinical outcomes. The prevalence of community-acquired pneumonia in regions such as North America and Europe sustains market leadership.

Bronchitis is likely to be the fastest-growing application in 2026, driven by the rising prevalence of acute and chronic bronchitis, particularly among patients with COPD and recurrent respiratory infections. Inhaled anti-infectives are increasingly preferred in bronchitis management as they deliver high local drug concentrations to the airways, improving bacterial clearance while minimizing systemic side effects. For example, the clinical evaluation of inhaled ciprofloxacin, delivered via dry powder or nebulized formulations, for patients with chronic bronchitis and related airway infections, where it has demonstrated potential in reducing bacterial burden and infectious exacerbations caused by Pseudomonas aeruginosa.

Regional Insights

North America Inhaled Anti-Infectives Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by a high prevalence of chronic respiratory diseases, advanced healthcare infrastructure, and strong research and development investment. The U.S., in particular, leads regional demand due to widespread recognition of targeted inhaled therapies for conditions such as cystic fibrosis, chronic obstructive pulmonary disease (COPD), and hospital-acquired pneumonia. The early adoption of cutting-edge inhalation drug delivery systems, including dry powder inhalers, smart nebulizers, and soft mist devices, supports improved lung deposition and patient adherence, which are critical in managing recurring infections and reducing systemic side effects.

Healthcare providers are also integrating digital health solutions and connected inhaler technologies to monitor patient compliance and optimize treatment regimens. For example, Novartis AG, through its TOBI® and TOBI Podhaler® (inhaled tobramycin) products. These therapies are widely approved and used in the U.S. for the management of chronic Pseudomonas aeruginosa lung infections in cystic fibrosis patients. TOBI Podhaler, a dry-powder inhalation formulation, represents a significant advancement over traditional nebulized antibiotics by improving convenience, reducing administration time, and enhancing patient adherence. Its strong adoption across U.S. cystic fibrosis centers has reinforced the clinical value of inhaled antibiotic delivery in chronic respiratory infections.

Europe Inhaled Anti-Infectives Market Trends

Europe is likely to be a significant market for inhaled anti-infectives in 2026, due to the region’s well-established healthcare infrastructure, increasing awareness of pulmonary infections, and high prevalence of chronic respiratory diseases such as cystic fibrosis, bronchiectasis, and COPD. Regulatory frameworks in the EU support the development and approval of innovative inhaled therapies, and European health systems emphasize antimicrobial stewardship and targeted treatment to address resistant infections. Investments in research collaborations and public health initiatives, such as support through EU4Health and professional respiratory societies, continue to strengthen early diagnosis, therapeutic compliance, and uptake of localized pulmonary therapy approaches.

Europe remains a key regional market with resilience and long-term demand for inhaled anti-infectives. For example, Pulmocide Ltd., a U.K.-based biopharmaceutical developer focused on inhaled medicines for life-threatening fungal and viral respiratory infections. Pulmocide’s pipeline includes inhaled formulations targeting conditions such as severe fungal lung infections and viral pathogens that are difficult to treat with conventional systemic therapies. The company’s work exemplifies how European biotech firms are leveraging advanced inhalation technologies and respiratory disease expertise to address unmet needs in antimicrobial resistance and complex infection areas where traditional therapies may be less effective or carry higher systemic risks.

Asia Pacific Inhaled Anti-Infectives Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by rising respiratory infection rates, increasing healthcare expenditure, and expanding access to advanced therapies. Countries such as China and India are key growth hubs due to rapid urbanization, rising air pollution, increasing geriatric populations, and higher prevalence of chronic respiratory diseases such as asthma, COPD, and bronchiectasis. These conditions elevate the demand for targeted pulmonary treatments that deliver drugs directly to the infection site, enhancing therapeutic effects while minimizing systemic side effects. Improving healthcare infrastructure across the region, alongside government initiatives to expand diagnostic and treatment access, increases the adoption of inhaled anti-infectives in both hospital and home care settings.

Local pharmaceutical manufacturers are also entering the space with cost-effective formulations and delivery devices tailored to regional needs, widening treatment access for patients who previously faced financial barriers. For example, Cipla Limited, an Indian multinational pharmaceutical firm that has been actively expanding its respiratory portfolio, including the development and distribution of inhaled anti-infective and respiratory care products in both domestic and international markets. Cipla’s focus on affordable inhalation therapies that address respiratory infections and chronic lung conditions highlights how regional players are responding to unmet treatment needs specific to Asia Pacific. Cipla enhances patient access to effective inhaled therapies.

Competitive Landscape

The global inhaled anti-infectives market exhibits a moderately fragmented structure, driven by the presence of both established pharmaceutical giants and innovative players competing for market share through differentiated products and strategic initiatives. Established players leverage strong brand recognition, comprehensive clinical data, and regulatory experience to retain a competitive advantage in key markets across North America, Europe, and Asia Pacific. The advent of advanced inhalation delivery systems, such as smart nebulizers and dry powder inhalers, also serves as a differentiator among competitors aiming to improve patient adherence and therapeutic outcomes.

Major industry players such as Gilead Sciences, AstraZeneca, GlaxoSmithKline (GSK), Novartis AG, Pfizer Inc., and Johnson & Johnson hold substantial market influence owing to their comprehensive respiratory product portfolios, strong research and development infrastructure, and expansive global distribution networks. Competition among these companies is driven by ongoing product innovation, strategic collaborations, mergers and acquisitions, geographic expansion, and the development of robust patient support programs. Meanwhile, mid-sized and regional companies are strengthening competitive pressure by introducing affordable formulations and specialized therapies designed to address unmet clinical demands.

Key Industry Developments:

- In October 2025, Ritedose Corporation announced that it had received FDA approval to manufacture and market tobramycin inhalation solution, which it licensed from Hikma, for treating Pseudomonas aeruginosa lung infections in cystic fibrosis patients. This product, packaged in 5 ml ampules, represents Ritedose’s first offering for cystic fibrosis and strengthens its position as a leading provider of nebulized inhalation solutions in the U.S. With this addition, Ritedose now boasts the largest portfolio of nebulized drugs in the country, including generic versions of formoterol fumarate, albuterol sulfate, ipratropium bromide, arformoterol tartrate, and cromolyn sodium. The company has also enhanced its manufacturing capabilities, incorporating blow-fill-seal (BFS) technology and expanded cGMP laboratory capacity, ensuring the production of high-quality, reliable, and affordable sterile inhalation therapies..

- In May 2025, Johnson & Johnson announced the launch of the Pitching Respiratory Innovation QuickFire Challenge, inviting innovators worldwide to submit novel ideas for developing treatments for patients with asthma and chronic obstructive pulmonary disease (COPD), with a focus on non-type 2 (non-T2) inflammatory pathways. The initiative aims to address unmet needs in patients whose conditions are driven by non-T2 mechanisms, for whom current therapies may be limited. Selected applicants will have the opportunity to present their research to Johnson & Johnson Innovative Medicine Immunology leaders in a closed-door virtual pitch scheduled for late August 2025.

Companies Covered in Inhaled Anti-Infectives Market

- AstraZeneca

- Johnson & Johnson

- GlaxoSmithKline

- Novartis AG

- Pfizer

- Wockhardt

- Roche

- Sanofi

- Merck

Frequently Asked Questions

The global inhaled anti-infectives market is projected to reach US$3.7 billion in 2026.

The increasing incidence of respiratory infections and chronic pulmonary conditions, combined with progress in targeted inhalation drug delivery technologies.

The inhaled anti-infectives market is expected to grow at a CAGR of 8.6% from 2026 to 2033.

Expansion in emerging economies, development of combination and resistance-targeted therapies, and growing adoption of advanced inhalation delivery systems for home and outpatient care.

AstraZeneca, Johnson & Johnson, GlaxoSmithKline, Novartis AG, Pfizer, Wockhardt, Roche, Sanofi, and Merck are the leading players.