- Pharmaceuticals

- Inhalable Drugs Market

Inhalable Drugs Market Size, Share, and Growth Forecast 2026 - 2033

Inhalable Drugs Market by Product (Dry Powder Inhalers, Metered Dose Inhalers, Nebulizers, Soft Mist Inhalers), Application (Asthma, Chronic Obstructive Pulmonary Disease, Cystic Fibrosis, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis, 20262033

Inhalable Drugs Market Size and Trend Analysis

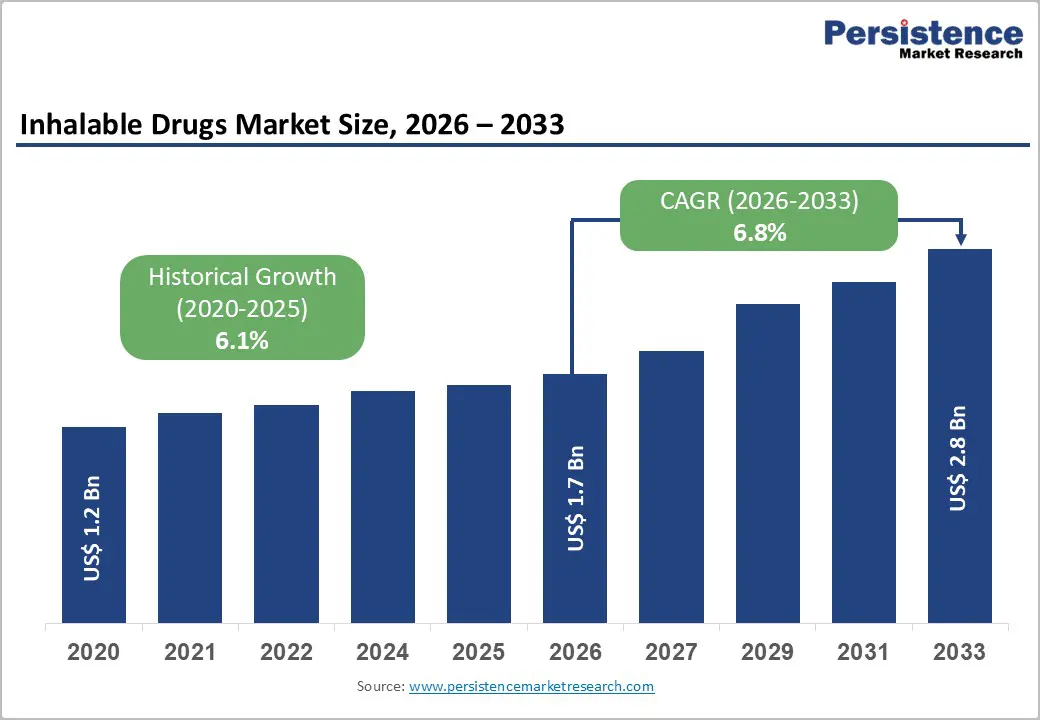

The global inhalable drugs market size is expected to be valued at US$ 1.7 billion in 2026 and projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033. The market growth is propelled by a confluence of disease prevalence, technological innovation, and supportive regulatory frameworks.

According to the World Health Organization, respiratory diseases, including asthma and chronic obstructive pulmonary disease, affect over 300 million individuals globally, with COPD alone causing 3.5 million deaths annually. The aging global population, coupled with increasing urbanization and air pollution, has intensified disease incidence, particularly in developing economies. Advanced inhalation technologies, such as smart inhalers with dose-tracking capabilities, improved dry-powder formulations, and propellants with lower environmental impact, are expanding treatment accessibility and improving patient adherence across demographic groups. Additionally, patent expirations and biosimilar opportunities are democratizing access to inhalable drugs in emerging markets while driving innovation pipelines in developed regions.

Key Industry Highlights:

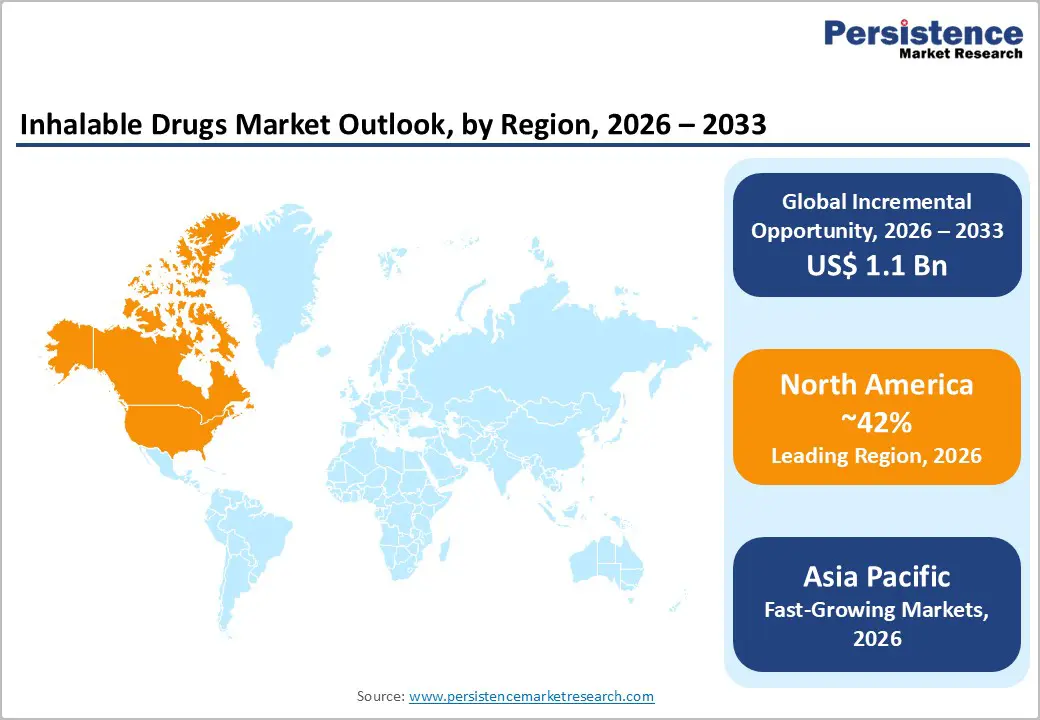

- North America dominated the market with 42% share in 2025, driven by advanced healthcare infrastructure, strong innovation, and established regulatory frameworks.

- The Asia-Pacific region is the fastest-growing region, projected to grow at a 5.96% CAGR through 2033, supported by expanding healthcare access and rising prevalence of respiratory diseases.

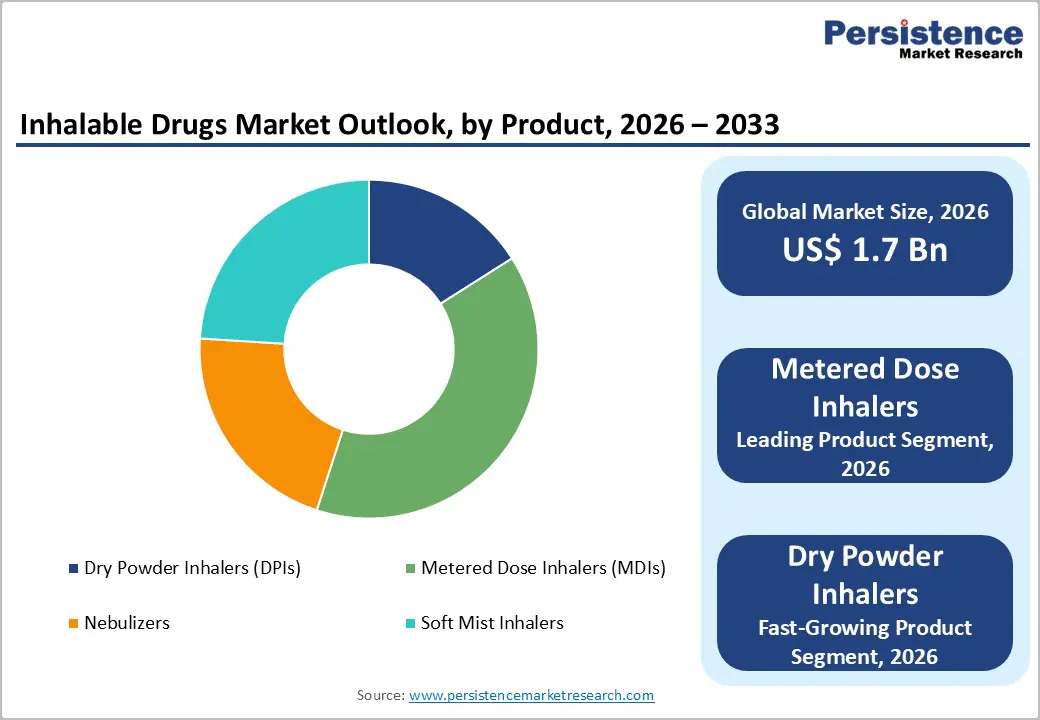

- Metered-dose inhalers (MDIs) led the market with 39% global share, due to widespread clinical adoption and transition to environmentally friendly propellants.

- Dry powder inhalers (DPIs) are the fastest-growing product segment, driven by propellant-free design, portability, and patient preference.

- Biologic-based inhalable therapies present significant growth opportunities, particularly in severe asthma and eosinophilic COPD, supporting premium pricing in developed markets.

| Key Insights | Details |

|---|---|

|

Inhalable Drugs Market Size (2026E) |

US$ 1.7 billion |

|

Market Value Forecast (2033F) |

US$ 2.8 billion |

|

Projected Growth CAGR (2026-2033) |

6.8% |

|

Historical Market Growth (2020-2025) |

6.1% |

Market Dynamics

Drivers - Rising Prevalence of Respiratory Diseases and Unmet Clinical Needs

The incidence of asthma and chronic obstructive pulmonary disease has reached epidemic proportions globally, with profound implications for inhalable drug adoption. In the United States alone, approximately 25 million individuals suffer from asthma, while COPD affects 11 million people and ranks as the third leading cause of death. The Centers for Disease Control and Prevention reports that 40% of persons with asthma experience at least one disease exacerbation annually, resulting in over 1.8 million emergency department visits and approximately 170,000 hospitalizations.

Beyond traditional respiratory conditions, the emergence of severe, uncontrolled asthma phenotypes requiring biologic interventions has expanded the therapeutic window for inhalable drug development. The United States Food and Drug Administration's 2024 approval of dupilumab for COPD, demonstrating 30-34% fewer exacerbations in clinical trials, exemplifies the ongoing innovation pipeline addressing previously underserved patient populations. This growing disease burden, combined with awareness campaigns and improved diagnostic capacity, sustains robust demand for inhaled therapies across geographies and socioeconomic strata.

Technological Advancement in Drug Delivery Systems and Smart Inhaler Integration

Innovation in inhalation device architecture represents a fundamental market accelerant, enhancing therapeutic efficacy and patient compliance simultaneously. Next-generation dry powder inhalers offer superior lung deposition characteristics compared to conventional systems, while metered-dose inhalers utilizing ultra-low-GWP propellants such as AstraZeneca's HFO-1234ze(E) formulation reduce environmental warming potential by 99.9%, addressing regulatory mandates in developed markets. Clinical evidence from digital health platforms demonstrates that inhaler performance metrics such as medication delivery rate, inhalation timing control, and dosage accuracy substantially improve treatment outcomes, reducing exacerbation frequency by 20-30% in real-world settings. These advancements appeal to both healthcare providers seeking objective adherence measurement and patients desiring convenient, intuitive delivery systems, thereby expanding market penetration across hospital, retail, and specialty pharmacy channels.

Restraints - High Development Costs and Regulatory Complexity for Novel Formulations

Pharmaceutical developers face substantial barriers in bringing novel inhalable drug formulations to market, constraining innovation velocity and market entry timelines. Regulatory frameworks established by the United States Food and Drug Administration, European Medicines Agency, and corresponding authorities in the Asia-Pacific regions require comprehensive bioequivalence demonstrations for locally acting inhalation products, necessitating specialized in vitro aerosol particle size distribution studies and pulmonary deposition modeling.

Development costs for complex inhaler-drug combinations frequently exceed US$ 100 million, with clinical trials extending 5-7 years. Generic manufacturers, particularly in low- and middle-income countries, encounter difficulty in replicating complex device mechanics and formulation stability characteristics, resulting in delayed market entry for cost-effective alternatives. This regulatory burden disproportionately impacts small and emerging pharmaceutical enterprises, concentrating market development capabilities among large multinational corporations and limiting product portfolio diversity.

Patient Adherence Challenges and Side Effect Burden in Long-term Therapy

Despite therapeutic efficacy, persistent medication non-adherence undermines real-world clinical outcomes and constrains market growth potential in chronic respiratory disease management. Patients frequently abandon inhaler therapy due to inadequate inhalation technique, adverse events such as bronchospasm and oral candidiasis, and psychological aversion to maintenance therapy. Approximately 50-60% of asthma and COPD patients demonstrate suboptimal adherence patterns, contributing to preventable disease exacerbations and emergency healthcare utilization. Specific formulations, including certain inhaled colistin preparations for cystic fibrosis management, carry documented risks of bronchoreactivity and systemic toxicity when administered without proper clinical supervision. The psychological burden of daily maintenance therapy, particularly in pediatric and geriatric populations, further compounds adherence challenges and limits market expansion among these demographics.

Opportunities- Emerging Biologic Inhalation Therapies and Personalized Medicine Approaches

Biologic-based inhaled therapies targeting specific inflammatory pathways represent a substantial unmet opportunity for pharmaceutical innovators addressing severe, refractory respiratory phenotypes. Monoclonal antibodies including dupilumab, mepolizumab, and tezepelumab, have demonstrated superior efficacy in biomarker-stratified patient populations, with eosinophilic COPD subgroups exhibiting 40-50% exacerbation reductions compared to conventional bronchodilator therapy. Pediatric biologic formulations represent a particularly underexploited opportunity, with current treatment algorithms limited to adult-focused therapies. Additionally, combination biologic approaches simultaneously inhibiting multiple inflammatory pathways offer potential for enhanced clinical response in treatment-resistant populations. This segment appeals to premium-positioned manufacturers capable of supporting biomarker-guided patient stratification and outcomes monitoring infrastructure.

Category-wise Analysis

Product Insights

Metered-dose inhalers commanded 39% of the global inhalable drugs market in 2025, establishing themselves as the dominant product category across respiratory disease indications. Clinical familiarity among both healthcare providers and patients, combined with mature manufacturing infrastructure and regulatory approval pathways, sustains market leadership despite emerging competition from alternative delivery systems. Metered-dose inhalers offer superior dose consistency, portability, and rapid bronchodilation, making them the preferred first-line intervention for acute asthma exacerbations and chronic COPD maintenance therapy.

The transition to ultra-low-GWP propellants, mandated by regulatory authorities in developed markets to comply with Montreal Protocol environmental commitments, has accelerated innovation in metered-dose inhaler formulation architecture.

Approximately 48.54% of digital dose inhalers now incorporate metered-dose inhaler technology with integrated sensors and wireless connectivity, further strengthening category prominence. Manufacturing scale economies and established supply chains across North America, Europe, and Asia-Pacific regions provide competitive advantages for metered-dose inhaler producers, while generic market expansion post-patent expiration promises sustained demand growth through 2033.

Application Insights

Asthma represents the dominant respiratory disease indication for inhalable drugs, commanding market leadership across product categories and geographic regions. Asthma affects more than 300 million individuals globally, with substantial disease burden concentrated in pediatric and working-age adult populations. The disease prevalence demonstrates marked variation across racial and ethnic groups, ranging from 3.5% among Asian populations to 12.3% among non-Hispanic Black Americans in the United States, reflecting underlying environmental justice and healthcare access disparities.

Clinical management algorithms have evolved toward maintenance therapy utilizing combination inhalers incorporating long-acting bronchodilators and inhaled corticosteroids, driving consistent demand for inhalable drug formulations. Biologic therapies targeting IgE-mediated and eosinophilic asthma phenotypes have expanded treatment options for severe, uncontrolled disease presentations previously refractory to conventional therapy.

The therapeutic arms race among pharmaceutical manufacturers, including GSK, AstraZeneca, and Boehringer Ingelheim, has generated robust innovation pipelines targeting asthma across pediatric, adult, and geriatric patient cohorts. Prevalence projections and epidemiological modeling suggest asthma incidence will maintain steady demand through 2033.

Distribution Channel Insights

Hospital pharmacies emerge as a critical distribution channel for inhalable drugs, particularly for acute exacerbation management, biologic therapy administration, and specialized respiratory disease treatment. Hospital-based pharmacy systems control medication procurement, formulary decision-making, and patient education infrastructure, exerting substantial influence on prescriber behavior and therapy selection. Nebulizer-based inhalable drug therapies, utilized extensively in acute care settings for rapid bronchodilation and antibiotic administration in cystic fibrosis management, flow predominantly through hospital pharmacy channels.

Retail pharmacy networks, including both chain and independent pharmacies, have captured significant market share through consumer accessibility, convenient prescription fulfillment, and increasingly sophisticated asthma and COPD disease management support services. Online pharmacy channels represent an emerging distribution frontier, offering convenience-driven medication access and potential cost advantages through direct-to-consumer supply models.

Regulatory frameworks governing online pharmaceutical distribution, reimbursement policies, and patient privacy protections vary substantially across jurisdictions, creating variable penetration rates by geography and therapeutic category.

Regional Insights

North America Inhalable Drugs Market Trends and Insights

North America dominates the global inhalable drugs market with a 42% market share in 2025, sustained by advanced healthcare infrastructure, robust insurance coverage mechanisms, and sophisticated regulatory environments conducive to pharmaceutical innovation. The United States market benefits from the presence of innovation centers and major pharmaceutical corporations including GSK, AstraZeneca, Boehringer Ingelheim, and emerging biotechnology enterprises.

Clinical practice guidelines established by the American Academy of Allergy, Asthma and Immunology and American Thoracic Society drive standardized treatment algorithms emphasizing inhaled therapies as first-line interventions across respiratory disease spectrum. Regulatory harmonization through the United States Food and Drug Administration and Health Canada facilitates streamlined product approval pathways and cross-border pharmaceutical supply arrangements.

Asia Pacific Inhalable Drugs Market Trends and Insights

Asia Pacific is projected as the fastest-growing inhalable drugs market region with projected CAGR of 5.96% through 2033, driven by rapid healthcare infrastructure expansion, pharmaceutical manufacturing capacity development, and escalating respiratory disease prevalence. China and India represent the primary growth engines, with China's urbanization and air pollution challenges creating substantial unmet respiratory disease treatment needs. India has established itself as a global biosimilar manufacturing hub with over 95 approved biosimilars in the domestic portfolio and cost-effective production capabilities enabling market penetration in price-sensitive emerging economies.

Manufacturing advantages in India and China have attracted multinational pharmaceutical investments and technology transfer arrangements, accelerating inhalable drug product development and commercialization timelines. The region's expanding elderly population, particularly in Japan and South Korea, drives chronic respiratory disease prevalence and healthcare expenditure. Government healthcare initiatives across India, Japan, and Southeast Asia have prioritized respiratory disease prevention and treatment accessibility, creating supportive regulatory environments and reimbursement frameworks for pharmaceutical innovation.

Digital health infrastructure development in major metropolitan centers positions Asia-Pacific for accelerated smart inhaler adoption, particularly in urban patient populations capable of accessing mobile health platforms and telemedicine services.

Competitive Landscape

The inhalable drugs market is highly competitive and innovation-driven, characterized by strong emphasis on product differentiation, device technology, and lifecycle management. Market participants compete on factors such as dosing accuracy, ease of use, patient adherence, and environmental sustainability, particularly with the shift toward propellant-free inhalers. Continuous R&D investments support the development of combination therapies, long-acting formulations, and advanced delivery platforms. Generic competition is intensifying, especially after patent expiries of leading inhaled therapies, putting pressure on pricing.

Key Market Developments

- In December 2025, Cipla, a global leader in inhalation therapies, launched Afrezza, the world’s only rapid-acting inhaled insulin, in the Indian market. The drug was indicated for adults with type 1 and type 2 diabetes to help control high blood sugar levels and represented a significant shift in insulin delivery, particularly in a country facing a rapidly growing diabetes burden.

Companies Covered in Inhalable Drugs Market

- GlaxoSmithKline plc (GSK)

- AstraZeneca plc

- Boehringer Ingelheim

- Novartis AG

- Teva Pharmaceutical Industries Ltd.

- Sanofi S.A.

- Pfizer Inc.

- Merck & Co., Inc.

- Cipla Ltd.

- Vectura Group plc

- Sunovion Pharmaceuticals Inc.

- MannKind Corporation

Frequently Asked Questions

The global inhalable drugs market is expected to be valued at US$ 1.7 billion in 2026.

Rising prevalence of asthma and COPD affecting over 300 million individuals globally, combined with technological advancement in smart inhalers enabling real-time medication adherence tracking, propels market expansion. Additionally, World Health Organization documentation of COPD as the fourth leading cause of death worldwide, claiming 3.5 million lives annually, intensifies pharmaceutical innovation investments and clinical practice guideline adoption emphasizing inhaled therapies as first-line interventions across respiratory disease management.

North America dominates the global inhalable drugs market with 42% market share in 2025, supported by advanced healthcare infrastructure, robust insurance coverage mechanisms, pharmaceutical innovation ecosystems centered in the United States, and regulatory frameworks established by the United States Food and Drug Administration and Health Canada facilitating rapid product approval and market commercialization timelines.

Biologic-based inhalable therapies targeting specific inflammatory pathways present substantial expansion opportunities, particularly for severe asthma and eosinophilic COPD patient populations currently underserved by conventional bronchodilator and corticosteroid therapy. Clinical trial data demonstrating 40-50% exacerbation reduction rates in biomarker-stratified populations support premium pricing strategies and justify investment in specialized manufacturing and patient stratification infrastructure.

GlaxoSmithKline plc, AstraZeneca plc, Boehringer Ingelheim, and Novartis AG maintain market leadership through extensive inhalable drug portfolios, established distribution networks, and sustained research and development investments.