- Automotive

- In-Dash Navigation System Market

In-Dash Navigation System Market Size, Trends, Share, and Growth Forecast 2026 - 2033

In-Dash Navigation System by System Type (Standalone In-Dash Navigation Systems, Integrated In-Dash Navigation Systems, Aftermarket In-Dash Navigation Systems, OEM Embedded Navigation Systems), by Installation Type (Factory Installed, Dealer Installed, Consumer Installed), by Display Technology, by Vehicle Type, by Sales Channel, by Regional Analysis, 20262033

In-Dash Navigation System Market Size and Trend Analysis

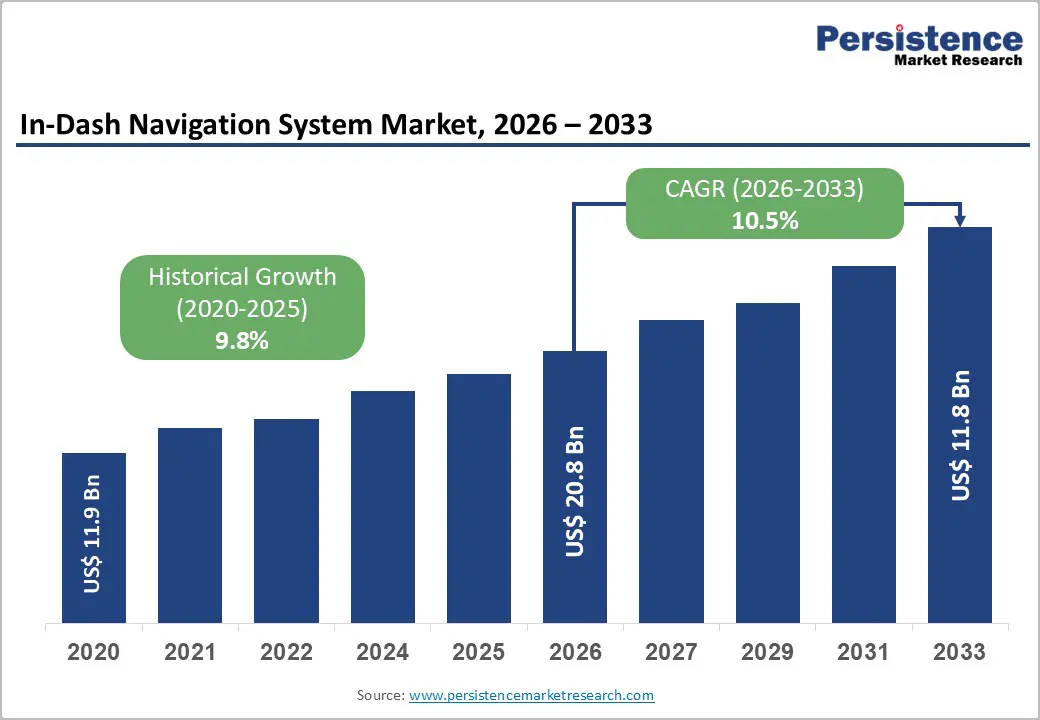

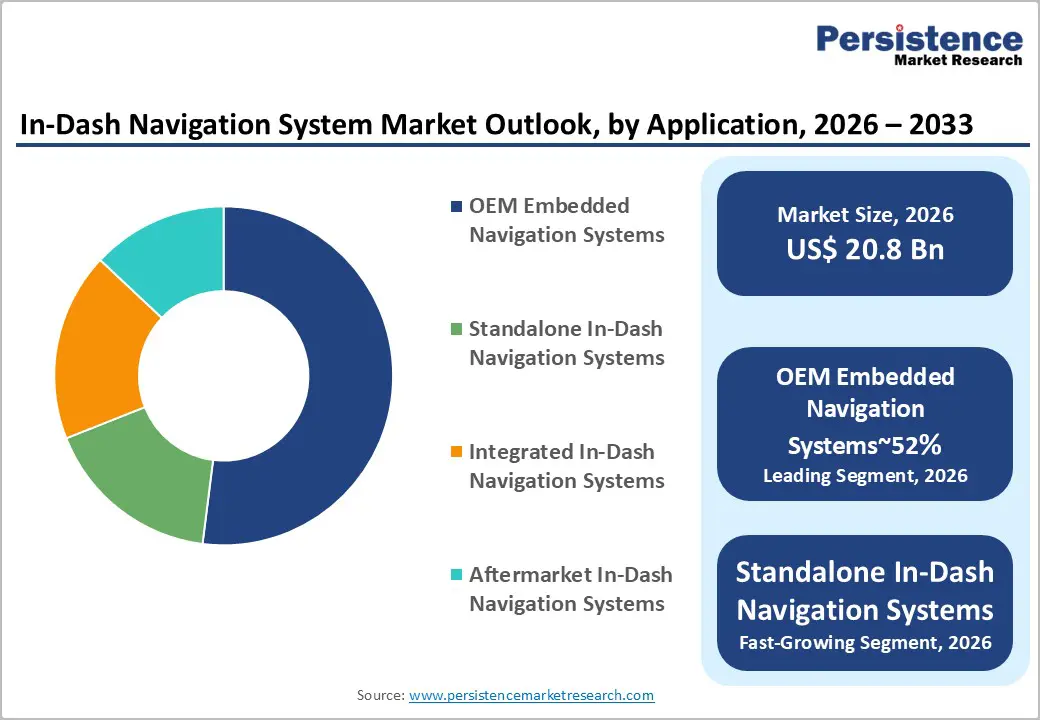

The global In-Dash navigation system market size is likely to be valued at US$ 20.8 billion in 2026 and is expected to reach US$ 41.8 billion by 2033, growing at a CAGR of 10.5% during the forecast period from 2026 to 2033. Market growth is driven by ADAS-integrated navigation adoption, EV-specific routing needs for charging and range optimization, and AI-enabled, cloud-based, voice-controlled systems enhancing safety, efficiency, and user experience.

Key Industry Highlights:

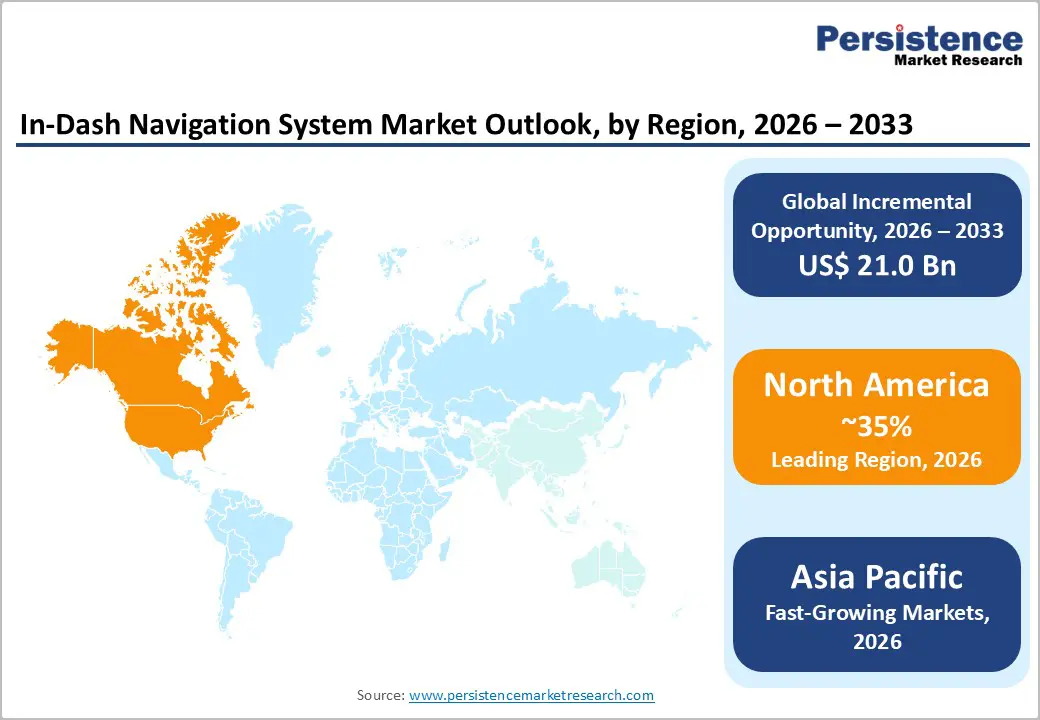

- Leading Region: North America commands approximately 35% of global in-dash navigation system market share, valued at US$ 7.91 billion in 2025, supported by mature automotive infrastructure, high ADAS adoption, and Apple CarPlay/Android Auto integration across 70-85% of mid-range and luxury vehicles.

- Fastest Growing Region: Asia Pacific expands fastest at 15.50% CAGR, driven by China and India rapid industrialization, 12.5% growth in Indian automotive demand, and accelerating EV production requiring specialized navigation for charging optimization and range management.

- Leading Segment: OEM-embedded navigation systems command 52% market share, preferred by consumers for superior hardware-software integration, seamless ADAS coupling, and manufacturer warranty support, outperforming aftermarket solutions across all vehicle segments.

- Fastest Growing Segment: Passenger cars represent 45% market share with 8% annual growth, driven by consumer demand for advanced infotainment systems and connected driving experiences supporting premium pricing and sustained market dominance.

- Key Opportunity: Electric vehicle integration represents fastest-growing opportunity, with EV routing incorporating 2 million charger locations, real-time availability prediction, and battery range optimization commanding premium pricing and supporting margin expansion across Asia Pacific, North America, and European markets.

| Key Insights | Details |

|---|---|

| In-Dash Navigation Systems Market Size (2026E) | US$ 20.8 Bn |

| Market Value Forecast (2033F) | US$ 41.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.8% |

Market Dynamics

Drivers - Rapid electric vehicle adoption is accelerating demand for intelligent navigation systems with advanced charging optimization and battery range management

The rapid growth of electric vehicle adoption is significantly increasing demand for advanced in-dash navigation systems designed specifically for EV users. These systems now play a critical role by integrating charging-station optimization, battery range estimation, and real-time energy-consumption monitoring. As global EV charging infrastructure expands, navigation providers such as HERE Technologies offer access to nearly 2 million charging connectors worldwide, with most providing real-time availability updates.

EV-focused navigation helps reduce range anxiety by calculating optimal routes that balance travel time with planned charging stops while accounting for terrain, traffic, and weather conditions. In India, the automotive navigation market is growing at a 12.5% CAGR, driven by rising vehicle sales and demand for connected technologies. Automakers increasingly view EV-optimized navigation as a value-added feature that enhances user confidence and justifies premium pricing. These capabilities are becoming essential as consumers prioritize reliable, stress-free EV journeys.

Growing integration of navigation with ADAS and connected platforms is transforming in-car systems into safer, smarter driving ecosystems

In-dash navigation systems are increasingly integrated with ADAS and connected vehicle platforms to deliver safer, smarter, and more seamless driving experiences. Modern systems now combine GPS navigation, vehicle telematics, safety alerts, and real-time data exchange into a single interface. Voice recognition accuracy has improved by nearly 25% over the past five years, significantly reducing driver distraction and improving usability.

In 2024, global installations exceeded 80 million units, with Asia Pacific and North America accounting for nearly two-thirds of total demand. OEM-installed systems dominate the market due to superior integration, reliability, and infotainment compatibility. Consumers now expect features such as over-the-air updates, real-time traffic data, and smartphone connectivity through Apple CarPlay and Android Auto. In the UK, the navigation market is expanding at a 7.1% CAGR, driven by demand for connected mobility and congestion-aware routing solutions.

Restraints - Free smartphone navigation apps and aftermarket alternatives are challenging the value proposition of factory-installed in-dash navigation systems

Smartphone-based navigation apps such as Google Maps, Apple Maps, and Waze pose strong competition to in-dash navigation systems by offering real-time updates, crowdsourced alerts, and free access. Many consumers perceive these applications as comparable alternatives, particularly in budget and mid-range vehicles where cost sensitivity is high. The availability of aftermarket retrofit solutions has further fragmented the market, allowing vehicle owners to upgrade older models at a lower cost than OEM-installed systems.

As a result, buyers increasingly question the value of factory-fitted navigation systems. Technical challenges, including wireless charging compatibility issues and cybersecurity risks in cloud-connected platforms, add further complexity. Manufacturers must carefully balance advanced features with system reliability and data security. These competitive and technical pressures continue to limit broader market expansion, especially among price-conscious consumer segments.

High development costs and complex vehicle integration requirements are limiting widespread adoption of advanced in-dash navigation solutions

Advanced in-dash navigation systems require significant upfront investment, making them costly for both manufacturers and consumers. High-resolution displays, AI-driven routing algorithms, cloud connectivity, and vehicle system integration raise overall development and component costs. Complexity increases further when systems must be adapted across different vehicle platforms, legacy architectures, and varying regional regulations. Smaller OEMs and aftermarket suppliers often struggle with extended development timelines and customization requirements.

Premium navigation systems typically cost 15–25% more than standard infotainment units, limiting adoption in budget-focused segments. Additionally, growing concerns around data privacy, location tracking, and third-party data sharing add compliance burdens, particularly in Europe under strict GDPR regulations. These regulatory and cost challenges increase operational risk and slow market penetration, despite rising consumer interest in connected and intelligent navigation solutions.

Opportunity - Autonomous vehicle development is creating new opportunities for navigation systems to become core platforms for automated driving decisions

The advancement of autonomous and semi-autonomous vehicles presents major growth opportunities for in-dash navigation systems. Navigation is evolving from a driver-support feature into a core decision-making platform for automated driving. Advanced systems now support lane-level guidance, hazard visualization, and augmented reality overlays that clearly display vehicle intentions. Companies such as Garmin, TomTom, and Bosch are investing heavily in AI-based predictive routing to anticipate traffic patterns and adjust routes proactively.

Navigation platforms are also being integrated into fleet management systems for autonomous delivery, ride-sharing, and urban shuttle services. These applications open new revenue streams through subscriptions and data analytics. Supportive government policies and smart mobility initiatives across Europe and Asia Pacific are accelerating standardization. As automation levels increase, navigation systems will become essential infrastructure for safe and efficient autonomous mobility.

Expanding EV charging networks and smart city initiatives are unlocking growth opportunities for intelligent, energy-optimized navigation platforms

The rapid expansion of EV charging networks and smart city projects is creating strong opportunities for navigation system providers. Modern navigation platforms now integrate charging station mapping, real-time availability, dynamic pricing, and energy optimization. India’s goal of deploying more than 25,000 charging stations by 2024 underscores the acceleration of infrastructure development.

Navigation systems that support low-emission zone routing and environmental impact tracking are gaining traction in cities such as London, Berlin, and Paris. Machine learning-based prediction tools help estimate charger availability, reducing uncertainty for EV drivers. Providers that partner with charge point operators and e-mobility platforms can offer seamless reservations, payment integration, and optimized charging schedules. These value-added services generate additional revenue through transaction fees and data services while improving user confidence and supporting global EV adoption.

Category-wise Analysis

System Type Insights

OEM embedded navigation systems hold approximately 52% market share due to their seamless integration with vehicle hardware, infotainment systems, and ADAS modules. Consumers prefer factory-installed systems because they offer higher reliability, better cybersecurity, and full manufacturer warranty support. OEM solutions provide deeper access to vehicle control units, enabling advanced safety and performance features not available in aftermarket alternatives.

Automakers are increasingly offering navigation as a standard feature in mid-range vehicles, expanding market reach and achieving economies of scale. These systems support offline maps, real-time traffic updates, and voice commands integrated directly into vehicle interfaces. Strong consumer trust in OEM platforms allows manufacturers to maintain premium pricing and stable margins. As connectivity and safety expectations rise, OEM navigation systems will continue to dominate the competitive landscape.

Vehicle Type Insights

Passenger cars account for roughly 45% of total market share, supported by strong demand for infotainment, safety, and connected driving features. Navigation systems are increasingly standard in mid-range models, driving wider adoption across consumer segments. Commercial vehicles represent a significant share, with fleet operators relying on navigation for route optimization, fuel efficiency, and real-time tracking.

Luxury vehicles remain technology leaders, adopting advanced AI routing, AR displays, and premium interfaces. Electric vehicles are the fastest-growing segment, requiring specialized navigation for charging planning, battery monitoring, and energy-efficient routing. These EV-specific features are becoming essential differentiators for automakers competing in both emerging and premium markets. As vehicle connectivity becomes standard, navigation demand will continue expanding across all vehicle categories.

Display Technology Insights

LCD and LED displays together account for nearly half of the market due to their affordability, reliability, and established manufacturing base. Touchscreen systems dominate user interfaces, reflecting consumer preference for smartphone-like interaction and responsive gesture controls. OLED displays represent the fastest-growing segment, expanding at a 14% CAGR due to superior image quality, deeper contrast, and improved energy efficiency.

These advantages are particularly valuable in electric vehicles, where power consumption directly impacts driving range. Advanced display technologies also support augmented reality overlays, lane guidance, and customizable visuals, enhancing user experience. Although OLED systems command higher prices, consumers increasingly view them as premium features worth the investment. As display innovation continues, visual quality will play a key role in navigation system differentiation.

Sales Channel Insights

OEM sales channels dominate the market with a 65% share, as automakers prioritize factory installation for quality assurance and system integration. OEM-installed systems benefit from warranty coverage and consistent performance standards. Aftermarket channels serve consumers seeking upgrades or replacements, accounting for roughly 38% of demand. Dealer-installed aftermarket systems command higher prices due to professional installation and extended support.

These solutions appeal to vehicle owners who value reliability and customization. While aftermarket options remain cost-effective alternatives, OEM channels maintain a strong advantage through brand trust and deeper vehicle integration. Both channels will continue to coexist, addressing different consumer needs and price points.

Regional Insights

North America In-Dash Navigation System Market Trends

North America continues to dominate the global in-dash navigation system market, holding around 35% market share, valued at approximately US$ 7.91 billion in 2025 and projected to reach nearly US$ 22.20 billion by 2035, growing at a CAGR of 10.87%. This strong position is supported by a well-established automotive ecosystem, high consumer adoption of advanced technologies, and widespread integration of navigation systems with ADAS platforms. The United States maintains one of the highest vehicle ownership rates globally, driving demand for premium infotainment and navigation solutions.

Around 75% of mid-range and luxury vehicles now feature factory-installed navigation systems. Apple CarPlay and Android Auto have become standard expectations, offering real-time traffic updates, voice control, and personalized routing. Regulatory focus on vehicle safety further accelerates adoption. Fleet operators increasingly deploy GPS-based routing to improve efficiency. Growing EV adoption, particularly in California, New York, and Texas, fuels demand for EV-specific navigation features, while Canada mirrors similar technology-driven growth patterns.

Europe In-Dash Navigation System Market Trends

European markets are witnessing steady growth due to rising demand for premium, connected, and safety-oriented vehicle technologies. Germany leads the region as the largest automotive market and home to major navigation technology providers such as Bosch and Continental, leveraging strong engineering capabilities to drive innovation. The German in-dash navigation market is growing at a CAGR of 6.1%, supported by connected vehicle adoption and strong OEM presence. Navigation systems are increasingly integrated with safety and infotainment platforms, enhancing driving experience and supporting autonomous vehicle development.

Countries such as the UK, France, and Spain remain important contributors, with navigation features now common even in mid-range vehicles. The European Union’s Green Deal and emission regulations are driving demand for EV-focused navigation systems that support charging optimization and low-emission zone routing. The UK market is expanding at 7.1% CAGR, driven by smart navigation demand and congestion management. Overall, EV growth across Europe is positioning navigation systems as essential tools for sustainable mobility.

Asia Pacific In-Dash Navigation System Market Trends

Asia Pacific is the fastest-growing region in the global in-dash navigation system market, expanding at a CAGR of 15.50% through 2033. Growth is driven by rapid urbanization, rising vehicle ownership, and increasing automotive production across China, India, and Southeast Asia. The region accounts for nearly 65% of global automotive output, prompting manufacturers to integrate navigation systems as standard features to attract a growing middle-class consumer base.

China leads the region, dominating EV manufacturing and advancing smart mobility initiatives, which boosts demand for AI-powered navigation and real-time traffic optimization. Government-backed smart transportation programs further support adoption. India’s automotive market is growing rapidly, with vehicle sales rising 10% annually and navigation demand increasing at a CAGR of 12.5%. Japan maintains leadership in navigation innovation through companies like Denso and Pioneer. Meanwhile, Southeast Asian countries such as Vietnam, Thailand, and Indonesia are emerging growth markets, driven by congestion management and urban mobility needs.

Competitive Landscape

The global in-dash navigation system market shows a moderately consolidated structure, with technological leadership concentrated among the major global players. Leading companies including Garmin, TomTom, Continental AG, Robert Bosch GmbH, and Denso Corporation collectively hold around 55% of the global market share. Their dominance is supported by long-standing automotive OEM partnerships, advanced navigation algorithms, and integrated hardware-software platforms. Companies such as Harman International, Alpine Electronics, Pioneer Corporation, and Clarion Co. Ltd. pursue differentiated strategies focused on premium infotainment integration, aftermarket solutions, and regional expansion.

Competition is intensifying as emerging Chinese automotive technology firms and EV-focused startups enter the market with cost-effective and EV-optimized navigation solutions. Key competitive factors include AI-driven traffic prediction, cloud-based mapping, advanced voice control, and seamless ADAS integration. Mergers and acquisitions are increasing as companies seek to strengthen capabilities and expand geographic presence. Growth strategies increasingly focus on EV routing, autonomous driving integration, and 5G-enabled connectivity.

Key Developments:

- In March 2025: Continental AG developed an advanced navigation platform offering lane-level guidance and real-time autonomous route adjustments, supporting Level 3–4 autonomous functionality. The solution targets premium vehicles in Europe and North America by mid-2026, enhancing safety and automated driving capabilities.

- In November 2024: TomTom launched an enhanced EV navigation platform using machine learning to predict charging availability, optimize stops, and improve battery range estimation under diverse driving and environmental conditions, boosting convenience and reliability for EV drivers.

- In August 2024: Robert Bosch GmbH deployed 5G-enabled navigation platforms enabling ultra-low latency cloud services, real-time traffic prediction, and autonomous vehicle communication, positioning Bosch as a leader in next-generation connected vehicle technologies.

Companies Covered in In-Dash Navigation System Market

- Garmin Ltd.

- TomTom NV

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Alpine Electronics, Inc.

- Clarion Co. Ltd.

- Harman International

- Pioneer Corporation

- Mitsubishi Electric Corporation

- Luxoft Holding Inc

- Delphi Automotive

- HERE Technologies

- Panasonic Corporation

- JVCKENWOOD Corporation

Frequently Asked Questions

The global market is expected to reach US$ 41.8 Billion by 2033, growing at a 10.5% CAGR from 2026.

Key drivers include EV-specific navigation, ADAS and connected vehicle integration, and voice-controlled navigation innovations.

OEM embedded systems lead with ~52% share, while passenger cars dominate vehicle segments with 45% market share.

North America leads with ~35% market share, while Asia Pacific is the fastest-growing region at 15.5% CAGR.

Major opportunities lie in EV charging optimization and autonomous vehicle integration with AR-enabled navigation features.

Top players include Garmin, TomTom, Continental, Bosch, and Denso, with emerging competition from HERE Technologies and Chinese providers.