- Pharmaceuticals

- Hypercalcemia Treatment Market

Hypercalcemia Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Hypercalcemia Treatment Market by Treatment (Bisphosphonates, Calcitonin, Glucocorticoids, Denosumab, Calcimimetics), Distribution Channel (Hospitals, Clinics, Independent Pharmacy & Drug Stores), and Regional Analysis from 2026 to 2033.

Hypercalcemia Treatment Market Share and Trends Analysis

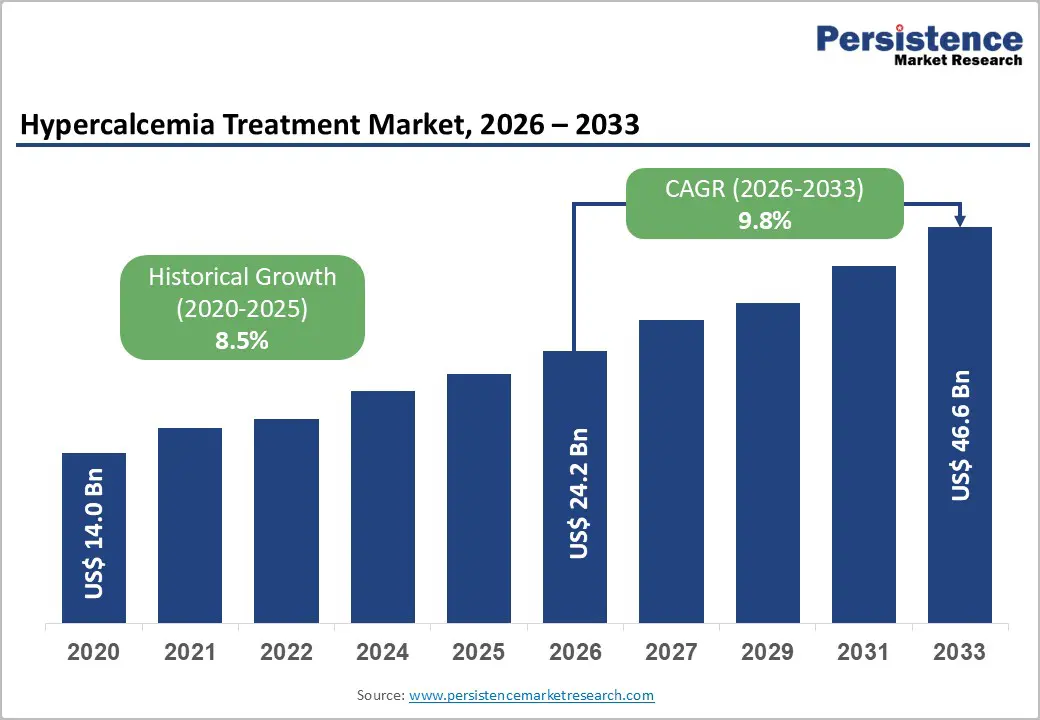

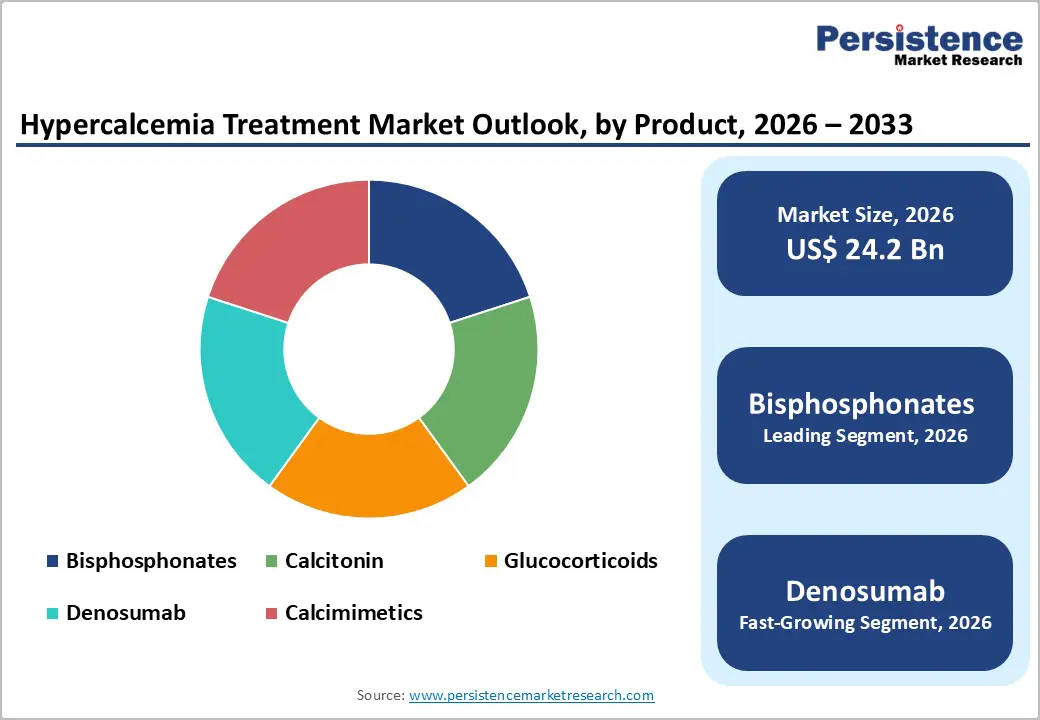

The global hypercalcemia treatment market is estimated to grow from US$ 24.2 Bn in 2026 to US$ 46.6 Bn by 2033. The market is projected to record a CAGR of 9.8% during the forecast period from 2026 to 2033.

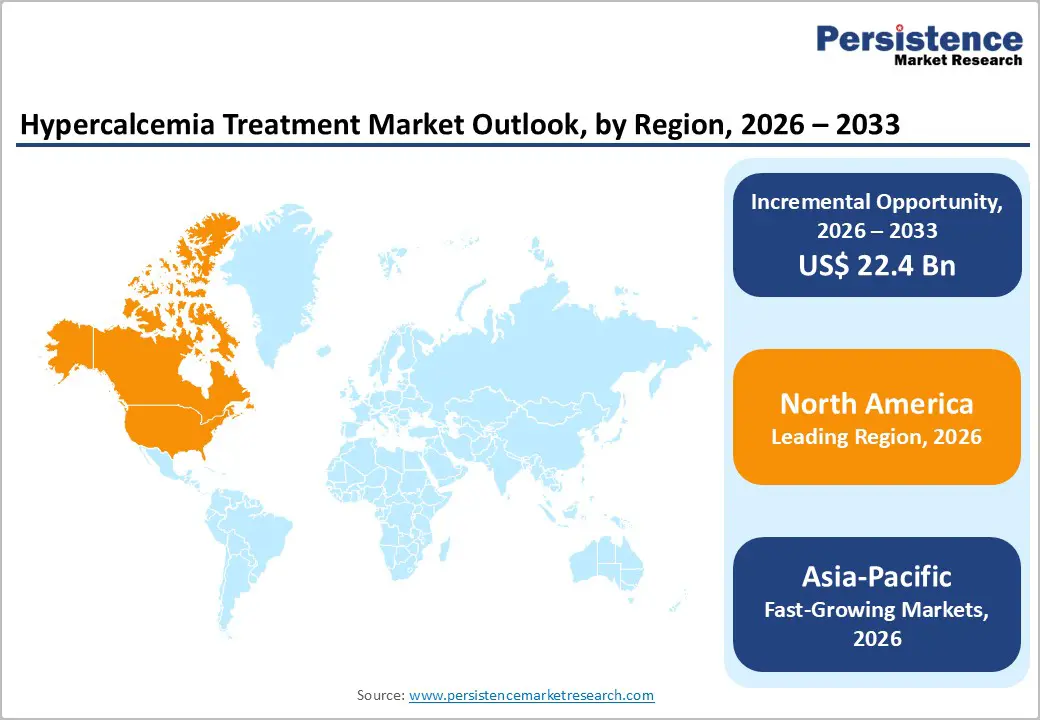

The global hypercalcemia treatment market is growing steadily, driven by rising cancer prevalence, increased awareness of metabolic disorders, and demand for effective calcium-lowering therapies. North America dominates due to advanced oncology care, strong reimbursement frameworks, and early adoption of novel drugs, while Asia-Pacific shows rapid growth supported by improving diagnostics, expanding hospital infrastructure, and rising healthcare investments.

Key Industry Highlights

- Dominant Segment: Bisphosphonates account for 62.4% share of the hypercalcemia treatment market in 2025, driven by their strong efficacy in lowering serum calcium levels, widespread use in malignancy-associated hypercalcemia, proven safety profile, and broad availability across hospital and oncology settings.

- Dominant Region: North America leads the hypercalcemia treatment market with 40.3% share in 2025, supported by advanced oncology infrastructure, high cancer incidence, strong reimbursement policies, and early adoption of novel agents. Asia-Pacific is the fastest-growing region, driven by expanding healthcare infrastructure, rising cancer burden, and improved diagnostic access.

- Market Drivers: Rising prevalence of cancer-related hypercalcemia, growing awareness of metabolic disorders, increased hospitalization rates, advancements in oncology care, and availability of effective intravenous and oral therapies are driving market growth.

- Market Opportunity: Key opportunities include development of targeted biologics, long-acting formulations, expansion of outpatient treatment options, improved management of chronic hypercalcemia, and growth across emerging markets with increasing oncology care investments.

| Key Insights | Details |

|---|---|

| Hypercalcemia Treatment Market Size (2026E) | US$ 24.2 Bn |

| Market Value Forecast (2033F) | US$ 46.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.5% |

Market Dynamics

Driver: Growing Burden of Metabolic and Endocrine Disorders

Hypercalcemia prevalence is directly tied to metabolic/endocrine disease burden, including primary hyperparathyroidism and malignancy-associated metabolic dysregulation. Epidemiological data indicate that hypercalcemia affects about 1%–2% of the general population, with approximately 90% of cases caused by primary hyperparathyroidism or malignancy due to dysregulated calcium homeostasis. This highlights the intersection of endocrine disorders (e.g., PTH hypersecretion) with elevated calcium levels. Patients with advanced malignancies and endocrine abnormalities experience complex metabolic dysregulation, reinforcing ongoing therapeutic demand.

In cancer populations, hypercalcemia represents a significant metabolic complication. U.S. data show hypercalcemia of malignancy occurring in about 2% of all cancer patients, with tens of thousands affected annually, underscoring the clinical burden across tumor types such as breast, lung, and hematologic cancers. As cancer incidence and metabolic disease burden rise with aging populations globally, clinical management of hypercalcemia becomes more important, sustaining demand for effective treatments that address both metabolic and endocrine drivers of elevated serum calcium.

Restraints: High Cost of Advanced and Biologic Therapies

Advanced and biologic therapies represent a significant cost burden within many specialty therapeutic areas, including potential future hypercalcemia treatments that employ targeted biologics or monoclonal agents. Reliable data show that biologic drugs can range from several thousand to over USD 100,000 per patient per year, depending on indication and molecule complexity. This steep price structure arises from costly research, development, and manufacturing processes inherent to biologics.

Beyond patient-level costs, biologics represent a substantial share of healthcare expenditure overall: biologic therapies account for roughly 38–40% of all pharmaceutical spending in the U.S. and European Union, despite representing a small fraction of total prescriptions. High costs can restrict access and result in tighter reimbursement criteria, delaying patient access to advanced therapies targeting complex pathophysiological mechanisms such as those driving severe or refractory hypercalcemia. This economic constraint limits adoption and can slow market expansion until more affordable alternatives (e.g., biosimilars) gain traction.

Opportunity: Development of Novel Targeted and Biologic Therapies

The broader biologic therapeutics landscape is rapidly expanding, representing a major opportunity for novel targeted approaches that could improve hypercalcemia management, particularly in malignancy-associated or refractory cases. These trends reflect increased application of targeted antibodies, receptor modulators, and precision biologics across metabolic and oncologic indications.

At the public health level, inclusion of key biologic therapies and biosimilars on the WHO Essential Medicines List demonstrates a strategic shift toward broader global access and price reductions, with biosimilar versions offering similar efficacy at approximately 65% lower cost compared to originator biologics. This trend signals expanding opportunities to introduce biologically targeted interventions in markets previously limited by cost, supporting diversification of treatment options for complex conditions like hypercalcemia.

Category-wise Analysis

By Product, Bisphosphonates Dominates the Hypercalcemia Treatment Market

Bisphosphonates occupies 62.4% share of the global market in 2025, because they directly inhibit osteoclast-mediated bone resorption, the pathophysiologic process releasing calcium into the bloodstream. Intravenous bisphosphonates such as pamidronate and zoledronic acid are frequently used and are effective in normalizing serum calcium in 60–90% of treated patients, making them a clinical standard for oncology-related hypercalcemia management. This efficacy is well documented in hospital treatment data showing that 40.4% of hospitalized hypercalcemia patients received pamidronate and 28.7% received zoledronic acid during care, reflecting their widespread use in real-world practice.

Moreover, their established role in clinical guidelines reinforces market dominance: bisphosphonates are recommended as a core component of therapy after initial hydration and calciuresis, with robust evidence supporting their use across diverse patient populations. Their effectiveness, coupled with familiarity among clinicians and availability in intravenous form for acute management, continues to position bisphosphonates at the forefront of hypercalcemia treatment modalities globally.

By Distribution Channel, Hospitals dominates due to emergency care needs, intravenous therapies, monitoring, and multidisciplinary management

Hospitals dominate the hypercalcemia treatment market as the primary end-user setting because severe or symptomatic hypercalcemia often constitutes a medical emergency requiring intensive monitoring and rapid intervention. Patients with high serum calcium levels typically present with dehydration, neurologic symptoms, cardiac arrhythmias, or renal dysfunction, and require immediate care including intravenous fluids, electrolyte management, and rapid-acting therapies that can only be safely provided in a hospital setting. Hypercalcemia of malignancy, for example, is associated with high morbidity and mortality, and treatment often involves intravenous bisphosphonates administered under close clinical supervision.

Furthermore, hospitals offer comprehensive diagnostic capabilities and multidisciplinary care essential for complex cases, including endocrinology, oncology, nephrology, and critical care teams. Real-world treatment patterns indicate that the majority of hypercalcemia therapies especially intravenous bisphosphonates and calcitonin are administered during hospital stays, underscoring hospitals’ central role in managing acute episodes and complicated underlying conditions. As a result, hospitals account for the largest share of treatment delivery due to their ability to handle both acute emergencies and ongoing monitoring of patients requiring specialized therapeutic interventions.

Regional Insights

North America Hypercalcemia Treatment Market Trends

North America leads the hypercalcemia treatment market largely due to its advanced healthcare infrastructure and high prevalence of conditions that cause elevated serum calcium, especially malignancy-associated cases. The region accounts for 40.3% of global market revenue, reflecting strong diagnostic capabilities, widespread use of effective treatments like bisphosphonates, and broad awareness among providers and patients.([turn0search1]; [turn0search5]) In the U.S., hypercalcemia of malignancy affects an estimated 2%–2.8% of cancer patients, resulting in tens of thousands of cases annually that require clinical intervention.([turn0search18]) Additionally, robust reimbursement systems and significant investments in R&D by both public health bodies and pharmaceutical companies further support adoption of advanced therapies and maintain North America’s leadership in this market.

Europe Hypercalcemia Treatment Market Trends

Europe holds a substantial share of the global hypercalcemia treatment market, supported by strong public healthcare systems across Germany, France, the U.K., and other Western European countries with structured treatment protocols and broad drug access. The region is responsible important in global market, underpinned by well-established healthcare policies, national insurance schemes, and high patient awareness of endocrine and oncology care.([turn0search5]) Europe also bears a significant burden of cancer, with over 4.47 million new cancer cases reported in 2022, which drives the need for metabolic condition management including hypercalcemia.([turn0search3]) This high incidence of cancer and chronic disorders underscores the sustained demand for effective calcium-lowering treatments, making Europe a key regional contributor to market growth.

Asia-Pacific Hypercalcemia Treatment Market Trends

Asia Pacific is emerging as the fastest-growing region in the hypercalcemia treatment market owing to expanding healthcare infrastructure, increasing disease diagnosis rates, and rising awareness of metabolic and oncologic disorders. The region’s market is projected to grow at a higher rate compared to North America and Europe, with an estimated CAGR above other regions, supported by expanding tertiary care facilities and broader access to treatment in countries like China, India, and Japan. Governments across Asia Pacific are investing in healthcare reforms and programs that improve early diagnosis and intervention, contributing to increased treatment uptake. Furthermore, growing healthcare expenditure, as seen in China where health spending reached approximately 7.05% of GDP and improvements in affordability and drug availability accelerate market expansion across the region.

Market Competitive Landscape

The hypercalcemia treatment market features established pharmaceutical players offering bisphosphonates, calcitonin, and supportive therapies. Competition is driven by strong clinical efficacy, hospital-based adoption, and regulatory approvals. Companies focus on lifecycle management, expanded oncology indications, biosimilar development, and strategic collaborations to strengthen hospital presence and global reach.

Key Industry Developments:

- In July 2025, XTANDI® in combination with leuprolide significantly improved survival outcomes in men with non-metastatic hormone-sensitive prostate cancer with high-risk biochemical recurrence. Clinical trial results showed delayed disease progression and reduced risk of metastasis, supporting the use of this combination therapy in earlier-stage, high-risk prostate cancer management.

- In May 2025, Astellas and Pfizer announced that XTANDI™ (enzalutamide) demonstrated long-term overall survival benefits in patients with metastatic hormone-sensitive prostate cancer. Clinical study results showed sustained survival improvement when XTANDI was used in combination with standard therapy, reinforcing its role as an effective first-line treatment option in advanced prostate cancer management.

Companies Covered in Hypercalcemia Treatment Market

- Amgen Inc.

- Pfizer Inc.

- Mylan N. V.

- Sunovion

- Apotex Corporation

- Novartis AG

- Bayer AG

- Hoffmann La Roche

- Atnahs Pharma

- Cipla Inc.

- Sun Pharmaceuticals Industries Ltd

- Dr. Reddy’s Laboratories

- Aurobindo Pharma Limited

- Others

Frequently Asked Questions

The global hypercalcemia treatment market is projected to be valued at US$ 24.2 Bn in 2026.

Rising cancer prevalence, metabolic disorders, improved diagnosis, hospital admissions, and demand for effective calcium-lowering therapies drive growth.

The global hypercalcemia treatment market is poised to witness a CAGR of 9.8% between 2026 and 2033.

Development of targeted biologics, outpatient therapies, biosimilars, emerging market expansion, and improved chronic hypercalcemia management.

Amgen Inc., Pfizer Inc., Mylan N. V., Sunovion, Apotex Corporation, Novartis AG.