- Medical Devices

- Hydrocephalus Shunts Market

Hydrocephalus Shunts Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Hydrocephalus Shunts Market by Product (Valves, and Catheters), by Procedure (Ventriculoperitoneal (VP) Shunts, Ventriculoatrial (VA) Shunts, Lumboperitoneal (LP) Shunts, and Ventriculopleural Shunts) by End User (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033

Hydrocephalus Shunts Market Share and Trends Analysis

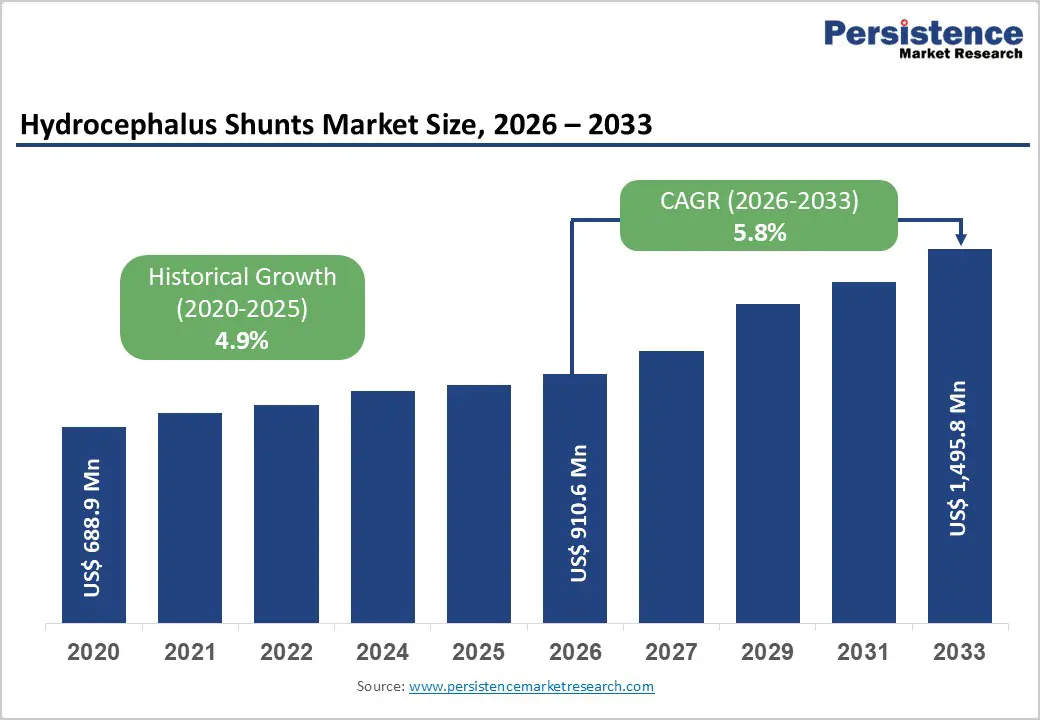

The global hydrocephalus shunts market size is estimated to grow from US$ 910.6 million in 2026 to US$ 1,495.8 million by 2033. The market is projected to grow at a CAGR of 5.8% from 2026 to 2033.

Global demand for hydrocephalus shunts is rising steadily, driven by the increasing incidence of congenital and acquired hydrocephalus, the growing prevalence of normal pressure hydrocephalus (NPH) in the aging population, and continuous improvements in neurosurgical care delivery. Rising rates of preterm births, neonatal intraventricular hemorrhage, traumatic brain injuries, brain tumors, and central nervous system infections are contributing to sustained demand for cerebrospinal fluid (CSF) diversion procedures.

Increasing awareness of early diagnosis and long-term management of hydrocephalus, combined with improved access to neurosurgical interventions, is accelerating procedural volumes globally. Expansion of tertiary hospitals, specialty neurology and neurosurgery centers, ambulatory surgery facilities, and structured follow-up care programs is further supporting market growth. Technological innovation in programmable, anti-siphon, and MRI-compatible valves is improving pressure regulation accuracy, reducing complications, and enhancing patient outcomes. In parallel, the growing focus on reducing revision rates, preventing shunt-related infections, and improving long-term quality of life is reinforcing adoption across pediatric and adult patient populations.

Key Industry Highlights:

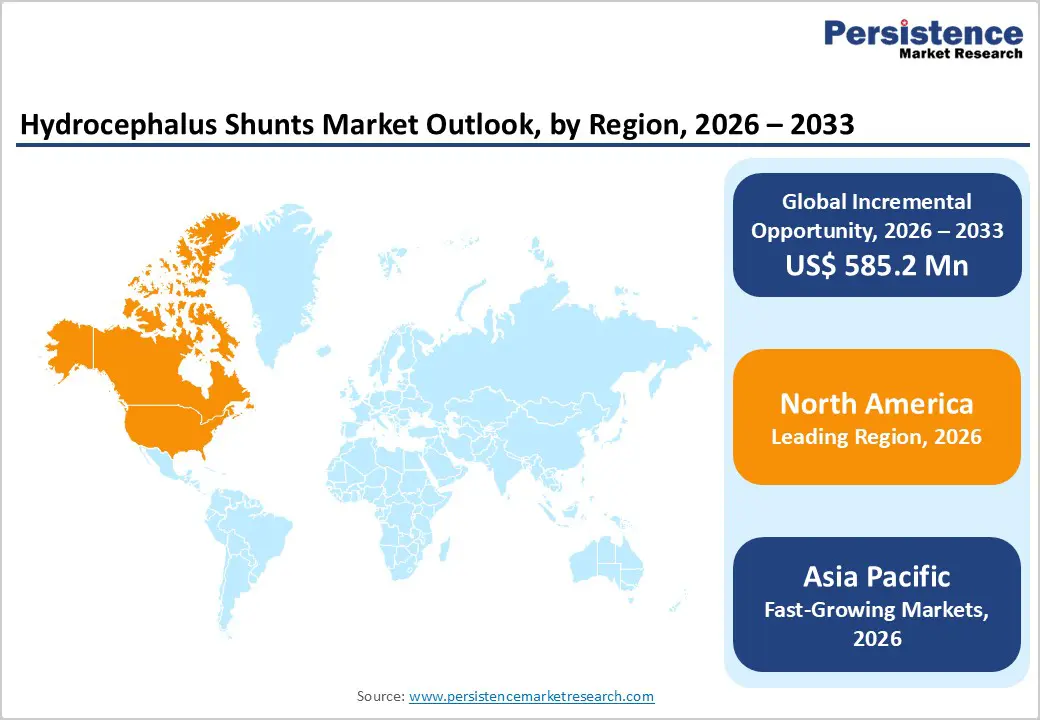

- Leading Region: North America holds the largest market share at 48.7%, supported by advanced neurosurgical infrastructure, high diagnostic rates for hydrocephalus, strong reimbursement frameworks, and early adoption of programmable and pressure-regulating shunt systems.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to a large pediatric population, rising incidence of neurological disorders, rapid hospital expansion, and increasing investments in neurosurgical capabilities.

- Leading Product Segment: Valves dominate the market due to their critical role in CSF flow regulation, higher average selling prices, and widespread adoption of programmable and anti-siphon designs.

- Fastest-Growing Product Segment: Catheters are witnessing rapid growth as demand rises for antimicrobial-impregnated and biocompatible materials aimed at reducing shunt infections and revision surgeries.

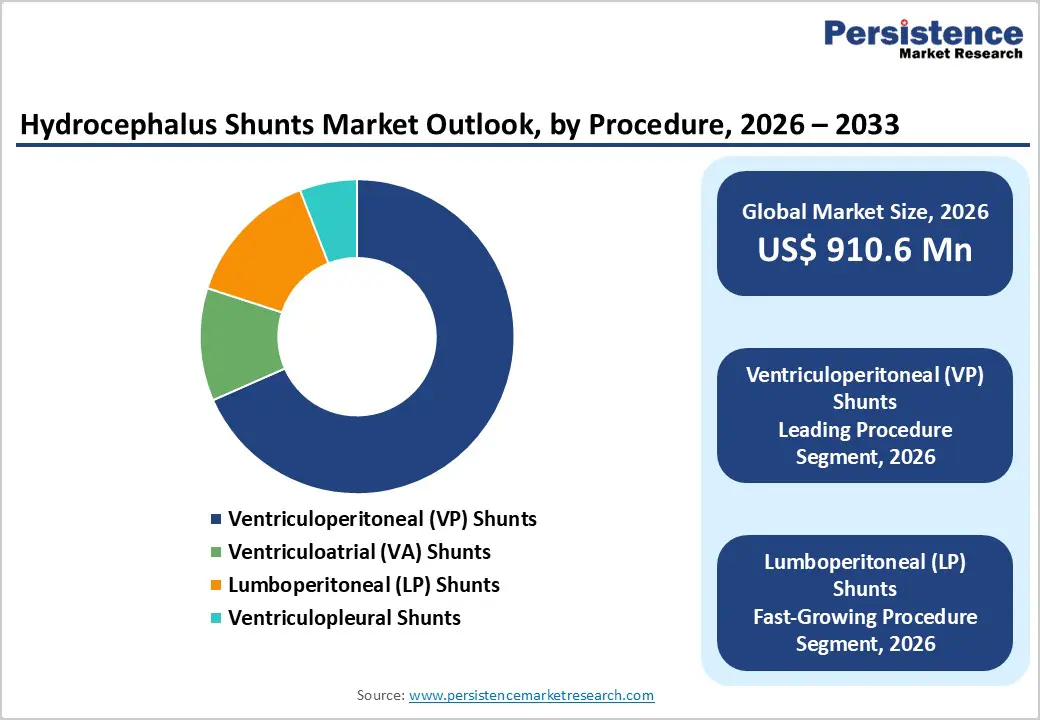

- Leading Procedure Segment: Ventriculoperitoneal (VP) Shunts remain the largest procedure segment due to broad clinical applicability across pediatric, adult, and NPH patients.

- Fastest-Growing Procedure Segment: Hospitals are expanding rapidly as increasing neurosurgical volumes and complex case management drive higher procedural concentration.

| Key Insights | Details |

|---|---|

| Hydrocephalus Shunts Market Size (2026E) | US$ 910.6 Mn |

| Market Value Forecast (2033F) | US$ 1,495.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Dynamics

Driver - Rising Disease Burden and Advancements in Shunt Technology Driving Market Growth

The rising incidence of pediatric hydrocephalus and normal pressure hydrocephalus (NPH) among the elderly is a primary factor driving sustained demand for hydrocephalus shunt systems globally. Increasing rates of preterm births and neonatal intraventricular hemorrhage continue to contribute significantly to congenital and early-onset hydrocephalus cases, particularly in developing and middle-income regions. In parallel, improved clinical awareness and diagnostic capabilities have led to higher identification rates of NPH in aging populations, especially in developed healthcare systems. As hydrocephalus remains a chronic condition requiring long-term cerebrospinal fluid (CSF) diversion, the growing patient pool directly translates into consistent shunt implantation volumes and repeat procedures over a patient’s lifetime.

Additionally, continuous technological advancements in shunt systems are strengthening clinical adoption and replacement demand. Increasing use of programmable, anti-siphon, and MRI-compatible valves is improving pressure regulation accuracy and reducing risks associated with over- or under-drainage. These innovations allow non-invasive pressure adjustments, lowering the need for revision surgeries and enhancing long-term patient outcomes. Improved valve durability, infection-resistant materials, and enhanced safety profiles are encouraging clinicians to transition away from conventional fixed-pressure systems. Together, rising disease prevalence and technology-driven improvements are reinforcing procedural confidence and supporting steady expansion of the hydrocephalus shunts market.

Restraints - Shunt Reliability Challenges and Infection-Related Complications Restraining Market Adoption

High shunt failure and revision rates remain a major restraint in the global hydrocephalus shunts market, significantly impacting long-term clinical outcomes and healthcare costs. Mechanical malfunctions such as valve failure, catheter obstruction, disconnection, and material degradation frequently necessitate revision surgeries over a patient’s lifetime. Over-drainage and under-drainage complications can lead to serious neurological consequences, including subdural hematomas and slit ventricle syndrome, further increasing the need for corrective procedures. The cumulative burden of repeat surgeries places substantial financial strain on healthcare systems and patients, while also influencing clinician preference toward alternative treatment approaches in selected cases.

Moreover, the risk of shunt-related infections and post-operative complications continues to constrain broader market adoption, particularly in pediatric populations. Shunt infections can result in prolonged hospital stays, repeated interventions, and increased morbidity, posing significant challenges in neonatal and infant care. These risks are further amplified in resource-limited settings where access to sterile surgical environments, advanced diagnostic tools, and long-term follow-up care is limited. Persistent concerns around infection control and complication management reduce clinical confidence in permanent shunt implantation and underscore the need for safer, more durable, and infection-resistant shunt technologies.

Opportunity - Infection-Resistant Innovation and Expanding Neurosurgical Capacity Creating New Growth Opportunities

Growing demand for antimicrobial and infection-resistant shunt systems is creating significant opportunities in the global hydrocephalus shunts market. Persistent concerns around shunt-related infections, particularly in pediatric and neonatal patients, are driving clinicians toward antimicrobial-impregnated catheters and advanced valve surface coatings designed to inhibit bacterial colonization. These technologies help reduce post-operative infection rates, lower the frequency of revision surgeries, and improve long-term patient outcomes. As healthcare systems place greater emphasis on infection prevention and cost containment, adoption of premium shunt systems with proven antimicrobial efficacy is increasing, especially in high-volume neurosurgical centers.

Furthermore, the global expansion of neurosurgical infrastructure is supporting higher diagnosis and treatment rates for hydrocephalus across both developed and emerging markets. Growth in tertiary care hospitals, wider availability of advanced neuroimaging modalities, and increasing numbers of trained neurosurgeons are improving early detection and surgical access. Government investments in healthcare capacity, coupled with private sector expansion of specialty neurological centers, are narrowing treatment gaps in regions such as Asia Pacific, Latin America, and the Middle East. Improved infrastructure is enabling broader adoption of advanced shunt technologies and supporting long-term market expansion.

Category-wise Analysis

By Product, Valves Dominate Globally Due to Critical Role in CSF Regulation

The valves segment is projected to dominate the global hydrocephalus shunts market in 2026, accounting for a revenue share of 61.7%. Segment leadership is driven by the essential function of valves in regulating intracranial pressure and controlling CSF drainage, making them the most value-intensive component of shunt systems. Increasing adoption of programmable valves allows clinicians to adjust pressure settings non-invasively, reducing the need for revision surgeries. Anti-siphon and gravity-assisted valve technologies are further improving outcomes by minimizing over-drainage complications. High replacement rates during shunt revisions, combined with growing preference for MRI-compatible and precision-controlled designs, continue to support revenue dominance. Ongoing innovation focused on durability, pressure accuracy, and infection risk reduction reinforces sustained adoption across pediatric and adult patient populations.

By Procedure, Ventriculoperitoneal (VP) Shunts Lead Due to Broad Clinical Adoption

The ventriculoperitoneal (VP) shunts segment is projected to dominate the global hydrocephalus shunts market in 2026, accounting for a revenue share of 60.0%. This dominance is attributed to VP shunts being the standard-of-care procedure for managing both congenital and acquired hydrocephalus. VP shunts offer flexibility across age groups, long-term effectiveness, and comparatively lower complication rates than alternative diversion pathways. Rising diagnosis of pediatric hydrocephalus, increasing survival rates of preterm infants, and growing recognition of NPH in older adults are driving sustained procedural volumes. VP shunts are widely preferred due to established surgical familiarity, favorable outcomes, and compatibility with advanced valve technologies. Expansion of long-term patient monitoring programs and structured post-operative follow-up is further strengthening segment leadership.

By End-user, Hospitals Dominate Due to High Surgical Volume and Specialized Care

The hospitals segment is projected to dominate the global hydrocephalus shunts market in 2026, accounting for a revenue share of 48.0%. Hospitals serve as the primary centers for hydrocephalus diagnosis, surgical intervention, and post-operative management, particularly for complex pediatric and adult cases. Availability of specialized neurosurgeons, advanced imaging facilities, intensive care units, and multidisciplinary clinical teams supports higher procedural concentration in hospital settings. Hospitals are also early adopters of programmable and advanced shunt systems aimed at reducing revision rates and long-term complications. Rising neurosurgical volumes, increasing trauma cases, and growing emphasis on comprehensive inpatient care continue to reinforce hospital dominance. Integration of standardized treatment protocols and long-term patient follow-up programs further sustains leadership.

Regional Insights

North America Hydrocephalus Shunts Market Trends

The North America hydrocephalus shunts market is expected to dominate globally with a value share of 48.7% in 2026, led primarily by the U.S. The region benefits from a highly developed healthcare system, widespread access to advanced neuroimaging, and strong clinical awareness of both pediatric hydrocephalus and normal pressure hydrocephalus in elderly populations. High diagnosis rates, favorable reimbursement policies, and early adoption of programmable and anti-siphon shunt technologies support sustained market leadership.

The presence of leading manufacturers, well-established hospital networks, and specialized neurosurgical centers further strengthens adoption. Increasing focus on reducing shunt failure rates and minimizing revision surgeries is driving demand for technologically advanced valve systems. Growth in outpatient follow-up care, long-term monitoring programs, and structured hydrocephalus management pathways continues to enhance procedural efficiency. Regulatory clarity and consistent FDA approvals enable rapid commercialization of next-generation shunt technologies, reinforcing North America’s dominant position.

Europe Hydrocephalus Shunts Market Trends

The Europe hydrocephalus shunts market is expected to grow steadily, supported by an aging population, increasing recognition of normal pressure hydrocephalus, and strong emphasis on evidence-based neurosurgical practices. Countries such as Germany, the U.K., France, Italy, and the Nordic region are key contributors due to well-established public healthcare systems and high access to specialized neurosurgical services. Rising prevalence of age-related neurological disorders and improved diagnostic capabilities are driving consistent procedural demand.

European healthcare systems prioritize long-term patient outcomes and cost-effective treatment pathways, encouraging adoption of programmable and durable shunt systems that reduce revision frequency. Expanding outpatient monitoring, integrated care pathways, and structured follow-up programs are improving long-term management of hydrocephalus patients. Harmonized regulatory frameworks and broader reimbursement coverage for advanced neurosurgical devices further support stable market expansion across the region.

Asia Pacific Hydrocephalus Shunts Market Trends

The Asia Pacific hydrocephalus shunts market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by expanding healthcare infrastructure, a large pediatric population, and rising incidence of neurological conditions. Countries including China, India, Japan, South Korea, and Southeast Asian nations are witnessing increasing diagnosis of congenital hydrocephalus, traumatic brain injuries, and post-infectious hydrocephalus. Rapid expansion of tertiary hospitals, growing availability of trained neurosurgeons, and rising healthcare expenditure are improving access to surgical treatment.

Increasing awareness of early intervention and long-term disease management is accelerating adoption of shunt systems. Local manufacturing, pricing improvements, and partnerships with global device companies are enhancing product availability. Government initiatives aimed at strengthening neurosurgical capacity and improving maternal and neonatal care are further supporting sustained regional growth.

Competitive Landscape

The global hydrocephalus shunts market is highly competitive, with strong participation from companies such as Medtronic, Aesculap, Inc., Spiegelberg GmbH & Co. KG., Integra LifeSciences, and B. Braun SE. These players benefit from established global distribution networks, diversified neurosurgical product portfolios, and continuous innovation in valve and catheter technologies. Competitive focus centers on improving pressure regulation accuracy, reducing infection risk, and enhancing long-term patient outcomes.

Manufacturers are prioritizing development of programmable, MRI-compatible, and anti-siphon shunt systems to minimize complications and revision rates. Strategic initiatives include portfolio expansion, clinical evidence generation, surgeon training programs, and penetration into emerging markets. Increasing neurosurgical volumes and growing demand for durable, long-term hydrocephalus management solutions continue to intensify competition across hospital and specialty care settings.

Key Industry Developments:

- In September 2025, Madison Scientific (MadSci) secured an additional USD 3 million in seed funding, supplementing its earlier USD 7 million raise and bringing the company’s oversubscribed seed round to a total of USD 10 million; the round was co-led by WARF Ventures along with two other investors and included participation from Heinz Ventures, mHUB Ventures, Endeavor Health Ventures, Princeton Alumni Angels, Stateline Angels, Central Illinois Angels, Impact Foundation, Isthmus Project, MedTech Angels, and other strategic investors.

- In February 2025, a Pittsburgh-based research team received a USD 2.3 million grant from the National Institutes of Health (NIH) under the Blueprint MedTech program to accelerate the development and clinical translation of a minimally invasive fetal shunt, led by Stephen Emery, professor of obstetrics, gynecology, and reproductive sciences at the University of Pittsburgh School of Medicine and director of the Center for Innovative Fetal Intervention at UPMC Magee-Womens Hospital, in collaboration with Youngjae Chun, professor of industrial engineering at the University of Pittsburgh’s Swanson School of Engineering.

- In August 2024, CereVasc received Breakthrough Device Designation from the U.S. Food and Drug Administration (FDA) for its eShunt system for the treatment of normal pressure hydrocephalus (NPH), supported by data from pilot clinical studies; additionally, the company was granted Investigational Device Exemption (IDE) approval for its STRIDE pivotal study evaluating the eShunt in NPH patients.

Companies Covered in Hydrocephalus Shunts Market

- Medtronic

- Aesculap, Inc.

- Spiegelberg GmbH & Co. KG.

- Integra LifeSciences

- B. Braun SE

- Sophysa

- CHRISTOPH MIETHKE GMBH & CO. KG

- Hpbio

- G. Surgiwear Ltd

- Bicakcilar

- Desu Medical

- Natus Medical Incorporated

- Sophysa

- Others

Frequently Asked Questions

The global hydrocephalus shunts market is projected to be valued at US$ 910.6 Mn in 2026.

Rising incidence of pediatric and normal pressure hydrocephalus, growing neurosurgical procedure volumes, and continued adoption of programmable and infection-resistant shunt technologies are the primary demand drivers.

The global hydrocephalus shunts market is poised to witness a CAGR of 5.8% between 2026 and 2033.

Expansion of antimicrobial and adjustable shunt systems, increasing LP shunt adoption in adult patients, and untapped demand in emerging markets with improving neurosurgical access present key growth opportunities.

Medtronic, Aesculap, Inc., Spiegelberg GmbH & Co. KG., Integra LifeSciences, B. Braun SE are some of the key players in the hydrocephalus shunts market.