- Healthcare Services

- Healthcare Patent Analytics Market

Healthcare Patent Analytics Market Size, Share, and Growth Forecast 2026 - 2033

Healthcare Patent Analytics Market by Component (Software, Services), Deployment Type (Cloud-Based, On-Premises), Patent Type (Drug Patents, Medical Device Patents, Biotechnology Patents, Diagnostic Patents, Others), End-user (Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Contract Research Organizations, Academic & Research Institutes, Healthcare IT Companies, Others), and Regional Analysis, 2026 - 2033

Healthcare Patent Analytics Market Share and Trends Analysis

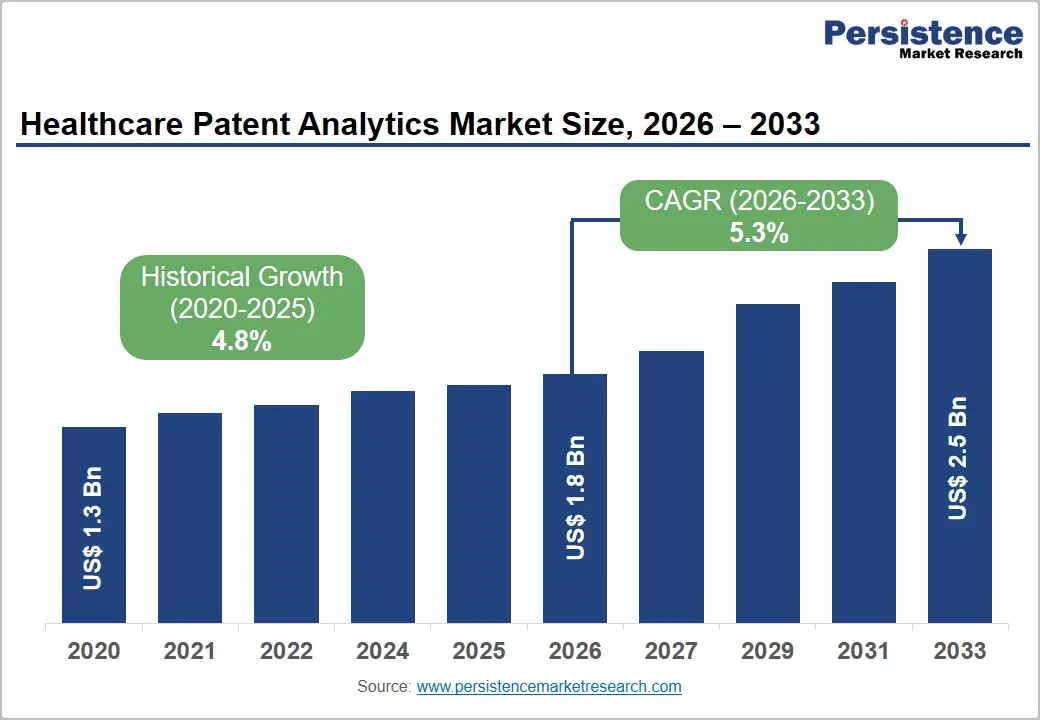

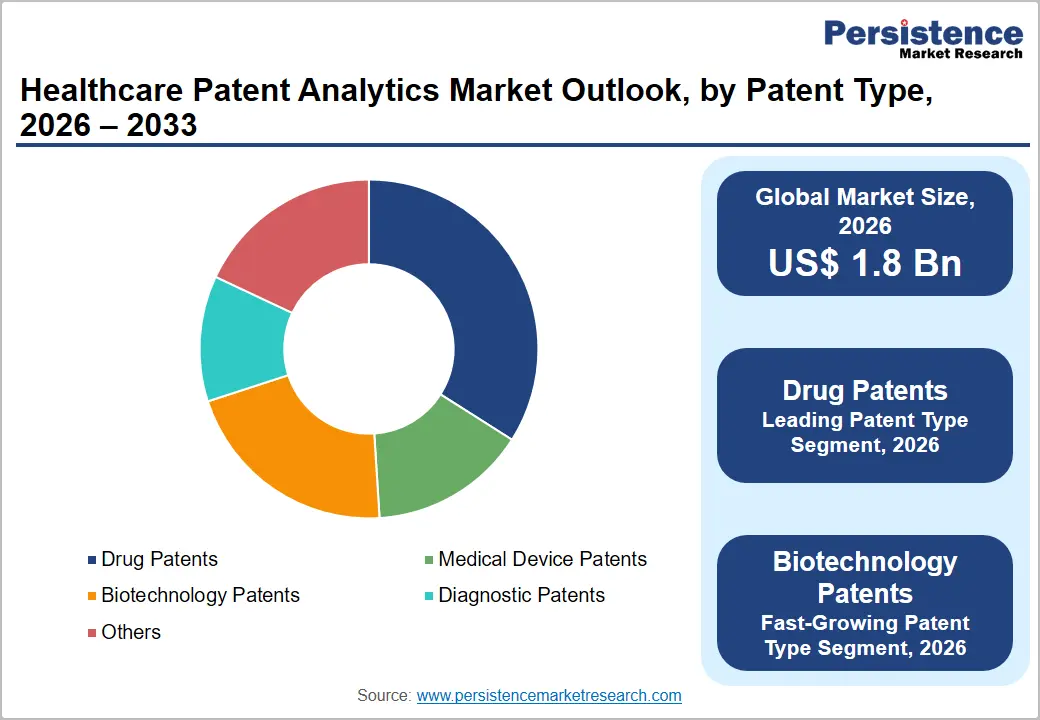

The global healthcare patent analytics market size is expected to be valued at US$ 1.8 billion in 2026 and projected to reach US$ 2.5 billion, growing at a CAGR of 5.3% between 2026 and 2033. It is witnessing steady growth due to increasing pharmaceutical and biotechnology innovation, rising global patent filings, and growing demand for intellectual property intelligence solutions.

Healthcare companies are increasingly adopting AI- and machine learning-powered analytics platforms to streamline patent searches, portfolio management, competitive benchmarking, and freedom-to-operate analysis. The market is also benefiting from expanding investments in biologics, precision medicine, medical devices, and digital health technologies. Cloud-based patent analytics solutions are gaining popularity due to scalability and real-time insights

Key Industry Highlights

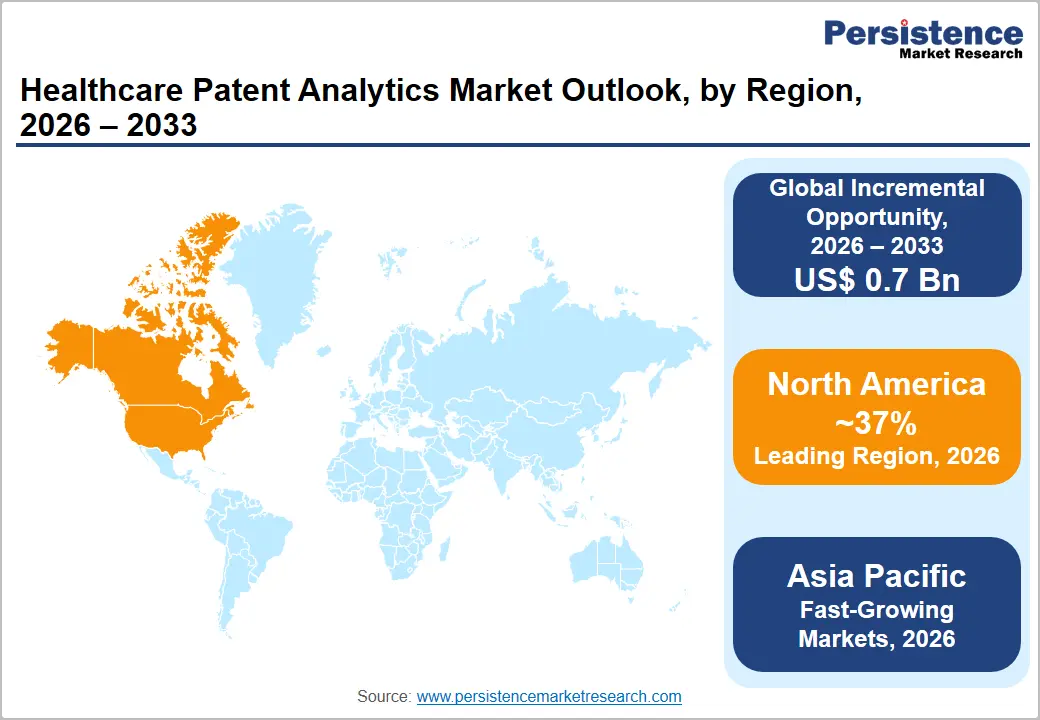

- Leading Region: North America is likely to register approximately 37% of the global healthcare patent analytics market share in 2026, driven by the world's highest biopharma R&D concentration, USPTO's robust patent filing infrastructure, and deep AI-powered analytics adoption by major pharmaceutical companies and CROs.

- Fast-Growing Market: Asia Pacific is the highest-growth market, propelled by CNIPA's 1.59 million patent applications in 2022, India's 3,000+ generic pharmaceutical manufacturers, Japan's advanced biopharma sector, and rapidly expanding cloud-based analytics adoption across Southeast Asian pharmaceutical hubs.

- Dominant Patent Type Segment: Drug patents command ~34% of the patent type segment in 2025, driven by extraordinary financial stakes, blockbuster drug patents protecting US$ 5–10 billion in annual sales, and continuous FDA Orange Book and Purple Book monitoring requirements across global pharmaceutical portfolios.

- Fast-Growing End-user Segment: Biotechnology Patents are the fastest-growing patent type, driven by CRISPR, mRNA, CAR-T, and gene therapy patent explosions, expanding biosimilar pipeline navigation needs, and FDA's approval of 40+ biosimilar products requiring intensive patent clearance analytics.

- Key Opportunity: SaaS-delivered cloud analytics platforms, enabled by India's PLI pharmaceutical scheme (INR 15,000 crore) and Southeast Asia's growing biopharma sector, offer vendors scalable, low-barrier entry into high-growth emerging markets with expanding IP management needs.

Market Dynamics

Drivers - Surging Healthcare Patent Filings and IP Intelligence Demand

The accelerating volume of global healthcare patent filings is creating an indispensable demand for advanced analytics platforms. WIPO's World Intellectual Property Indicators 2023 report documented that biopharmaceutical and medical technology sectors collectively account for approximately 20% of all global patent applications.

The U.S. Patent and Trademark Office (USPTO) received over 650,000 patent applications in fiscal year 2023, with healthcare and life sciences representing the most densely filed technology classes. As pharmaceutical companies navigate patent cliffs with branded drugs worth over US$ 200 billion in annual sales facing generic competition through 2030 per Evaluate Pharma the need to monitor competitive IP landscapes, identify freedom-to-operate risks, and uncover licensing opportunities makes healthcare patent analytics a mission-critical investment.

AI and Machine Learning Integration Transforming Patent Intelligence

The integration of artificial intelligence, natural language processing (NLP), and machine learning into patent analytics platforms is fundamentally elevating the value proposition of healthcare patent intelligence. Platforms such as PatSnap and Orbit Intelligence now deploy AI-driven semantic search, automated prior art retrieval, and predictive validity scoring capabilities that dramatically reduce the time and cost of patent analysis.

A 2023 World Economic Forum (WEF) white paper on AI in intellectual property estimated that AI-powered patent search tools reduce analysis cycle times by up to 70% compared to manual review. For pharmaceutical and biotechnology companies managing patent portfolios of thousands of assets, this efficiency gain translates directly into competitive advantage and reduced legal expenditure, accelerating the adoption of AI-enhanced patent analytics platforms across the healthcare sector.

Market Restraints - High Implementation Costs and Integration Complexity

Advanced healthcare patent analytics platforms particularly enterprise-grade solutions with AI capabilities carry substantial licensing, implementation, and integration costs that can restrict adoption among smaller pharmaceutical companies, CROs, and academic institutions. Annual software licensing fees for tier-one platforms from Clarivate Plc and LexisNexis can range from tens of thousands to several hundred thousand U.S. dollars, and integration with existing IP management and R&D data systems requires significant IT investment. Smaller organizations with constrained IP budgets may opt for manual analysis or basic database subscriptions, limiting their total addressable market contribution.

Data Quality, Standardization, and Jurisdictional Fragmentation

The global patent data landscape remains fragmented across over 150 national and regional patent offices, each with distinct data formats, classification systems, and disclosure requirements. The European Patent Office (EPO) and USPTO maintain relatively structured databases, but patent data from emerging markets including China's National Intellectual Property Administration (CNIPA) presents language, translation accuracy, and metadata standardization challenges. Inconsistent data quality undermines the reliability of analytics outputs, requiring significant human expert validation and reducing user confidence in automated patent intelligence recommendations, particularly in high-stakes pharmaceutical freedom-to-operate analyses.

Opportunities - Biotechnology Patent Explosion and Biosimilar Landscape Navigation

The rapid expansion of biotechnology patent filings driven by mRNA therapeutics, gene editing, cell therapy, and monoclonal antibody innovation is creating significant incremental demand for specialized biotechnology patent analytics. The WIPO Technology Trends: Assistive Technology and related biotechnology reports document sustained double-digit growth in CRISPR, CAR-T, and gene therapy patent filings since 2015.

Simultaneously, the global biosimilar pipeline is expanding rapidly: the FDA's Biosimilar Action Plan has approved over 40 biosimilar products in the U.S. as of 2024, with patent expiry landscapes requiring intensive analytics to identify entry windows. Companies offering purpose-built biotechnology patent mapping, sequence patent analytics, and biosimilar clearance study tools are exceptionally well-positioned to capture this structural growth opportunity through the forecast period.

Cloud Deployment and SaaS Model Expansion into Emerging Markets

The shift toward cloud-based, SaaS-delivered patent analytics platforms is dramatically lowering the entry barrier for healthcare organizations in emerging markets, particularly in India, China, Brazil, and Southeast Asia where growing pharmaceutical manufacturing sectors are generating increasing IP management needs. India's Production Linked Incentive (PLI) scheme for pharmaceuticals, which allocated INR 15,000 crore (approximately US$ 1.8 billion) to the sector is driving domestic pharmaceutical R&D investment and consequent IP analytics adoption.

Cloud-based deployment eliminates costly on-premises infrastructure requirements, making platforms accessible to mid-sized generic pharmaceutical companies and CROs in cost-sensitive markets. Vendors offering tiered, usage-based SaaS pricing models tailored for emerging market organizations are positioned to capture a growing share of this underpenetrated segment.

Category-wise Analysis

Component Insights

Software is the dominant component segment in the healthcare patent analytics market, accounting for approximately 62% of total revenue in 2026. Software platforms encompassing patent search engines, portfolio management tools, competitive intelligence dashboards, and AI-driven analytics suites constitute the core value delivery mechanism of the market.

Leading platforms such as Clarivate's Derwent Innovation, PatSnap, and Questel's Orbit Intelligence command significant recurring subscription revenues from pharmaceutical, biotechnology, and medical device clients globally. The scalability of cloud-based software, combined with continuous AI and NLP capability upgrades, makes software the primary investment focus for healthcare organizations seeking real-time patent intelligence and competitive landscaping capabilities.

Deployment Type Insights

Cloud-based deployment is leading type segment, representing approximately 67% of the healthcare patent analytics market in 2026. The cloud model's dominance reflects pharmaceutical and biotechnology organizations' increasing preference for accessible, scalable, and regularly updated patent intelligence platforms that do not require internal IT infrastructure investment.

Cloud delivery enables real-time database updates critical in fast-moving therapeutic areas and supports global team collaboration across distributed R&D and IP functions. The National Institute of Standards and Technology (NIST) cloud computing framework highlights data accessibility, elasticity, and reduced total cost of ownership as the primary enterprise cloud adoption drivers, which directly align with the operational requirements of healthcare patent analytics users across multinational pharmaceutical companies and CROs.

Patent Type Insights

Drug patents constitute the leading patent type segment, commanding approximately 34% of total market revenue in 2026. This dominance reflects the pharmaceutical sector's unparalleled patent intensity small molecule drugs, formulations, dosage forms, and manufacturing processes each generate distinct patent families requiring comprehensive monitoring and analysis.

The financial stakes of drug patent management are extraordinary: a single blockbuster drug patent can protect revenues exceeding US$ 5–10 billion annually. The FDA's Orange Book and Purple Book list thousands of active drug and biologic patents, each requiring continuous monitoring for patent term extensions, certifications, and litigation activity making drug patent analytics the highest-value and highest-volume segment in the healthcare patent analytics market.

End-user Insights

Pharmaceutical Companies represent the dominant end-user segment, accounting for approximately 38% of total market revenue in 2026. Large pharmaceutical companies maintain extensive patent portfolios spanning drug compounds, formulations, synthesis processes, and clinical methods each requiring active monitoring, competitive benchmarking, and expiry management. The patent cliff exposure of the global pharmaceutical industry with over US$ 200 billion in branded drug sales at risk of generic entry through 2030 per Evaluate Pharma creates an urgent and sustained demand for patent analytics solutions that identify competitive threats, map freedom-to-operate landscapes, and support life-cycle management strategies including secondary patents, authorized generics, and formulation innovations.

Regional Insights

North America Healthcare Patent Analytics Market Trends and Insights

North America is likely to lead the global healthcare patent analytics market with approximately 37% market share in 2026, driven by the world's highest concentration of pharmaceutical and biotechnology R&D investment, the USPTO's robust patent filing infrastructure, and a mature intellectual property legal ecosystem. Strong adoption of AI-powered analytics platforms by large pharma and biotech firms headquartered in the U.S. sustains the region's leadership position through the forecast period.

U.S. Healthcare Patent Analytics Market Size

The United States is likely to account for approximately 84% of North America's healthcare patent analytics revenue in 2026, underpinned by over 6,000 pharmaceutical and biotechnology companies operating nationally per the Pharmaceutical Research and Manufacturers of America (PhRMA). Deep integration of patent analytics within Big Pharma IP and R&D functions drives consistently high per-organization platform spend.

Europe Healthcare Patent Analytics Market Trends and Insights

Europe is the second-largest regional market, characterized by strong pharmaceutical R&D activity in Germany, the United Kingdom, France, and Switzerland, and the harmonized patent framework provided by the European Patent Office (EPO). The introduction of the Unitary Patent system across 17 EU member states in June 2023 is increasing patent filing volume and complexity, directly amplifying demand for multi-jurisdictional patent analytics solutions across the continent.

Germany Healthcare Patent Analytics Market Size

Germany represents approximately 22% of the European healthcare patent analytics market in 2026, anchored by pharmaceutical and medical technology leaders including Bayer AG, Boehringer Ingelheim, and Siemens Healthineers. Germany's position as Europe's largest pharmaceutical market and its dense medtech innovation ecosystem drive sustained demand for IP analytics platforms and freedom-to-operate analysis services.

U.K. Healthcare Patent Analytics Market Size

The United Kingdom accounts for approximately 18% of European market revenue, supported by its globally competitive life sciences sector anchored by AstraZeneca, GSK, and Wellcome Sanger Institute. The UK Intellectual Property Office (IPO)'s progressive digital infrastructure and the country's post-Brexit independent patent framework under MHRA are sustaining strong demand for specialized patent intelligence solutions.

France Healthcare Patent Analytics Market Size

France contributes approximately 13% of European healthcare patent analytics revenue in 2026. The country's pharmaceutical sector led by Sanofi S.A. and supported by the French National Institute of Health and Medical Research (INSERM) generates significant patent activity in immunology, rare diseases, and vaccines. Government-backed biocluster initiatives are expanding early-stage biotech patent filing activity, supporting platform adoption.

Asia Pacific Healthcare Patent Analytics Market Trends and Insights

Asia Pacific is the fastest-growing regional market, driven by surging pharmaceutical R&D investment in China, India, Japan, and South Korea. China's National Intellectual Property Administration (CNIPA) received over 1.59 million patent applications in 2022 the world's largest volume with life sciences patent filings growing rapidly, creating substantial demand for Chinese-language patent analytics and cross-jurisdictional intelligence capabilities.

India Healthcare Patent Analytics Market Size

India accounts for approximately 14% of Asia Pacific's healthcare patent analytics market in 2026. The country's position as the world's largest generic pharmaceutical manufacturer with over 3,000 active pharmaceutical manufacturers per the Pharmaceuticals Export Promotion Council of India (Pharmexcil) creates strong demand for patent expiry monitoring, freedom-to-operate analysis, and biosimilar patent clearance tools.

Competitive Landscape

The global healthcare patent analytics market is highly competitive, characterized by the presence of established intellectual property analytics providers, AI-driven software developers, and specialized patent consulting firms. Companies are focusing on integrating artificial intelligence, machine learning, and big data analytics to enhance patent search accuracy, portfolio management, and competitive intelligence capabilities. Strategic collaborations, cloud-based platform expansion, and acquisition activities are increasingly shaping market competition. Leading participants are strengthening their healthcare and biotechnology patent databases to support innovation in pharmaceuticals and medical devices.

Key Developments:

- In October 2025, it showcased major upgrades to its Pharma.AI platform during its “Towards Pharmaceutical Superintelligence” webinar. The company enhanced PandaOmics with new large language model (LLM)-based scoring capabilities for confidence, druggability, and commercial tractability.

- In May 2026, Thomson Reuters partnered with Sterne Kessler to launch the “Patent Claim Eligibility Analyzer,” an AI-powered patent analysis tool integrated within CoCounsel Legal. The solution was developed to streamline Section 101 patent-eligibility analysis by rapidly reviewing patent claims, identifying relevant legal precedents, and providing precedent-backed explanations within minutes rather than days.

Companies Covered in Healthcare Patent Analytics Market

- Clarivate Plc

- LexisNexis

- Questel

- IFI Claims Patent Services

- Gridlogics Technologies Pvt. Ltd.

- PatSnap

- Anaqua Inc.

- CPA Global

- Derwent

- Orbit Intelligence

- IPlytics GmbH

- InnovationQ Plus

- Minesoft Ltd.

Frequently Asked Questions

The global healthcare patent analytics market is estimated to be valued at US$ 1.8 billion in 2026, projected to reach US$ 2.5 billion at a CAGR of 5.3% by 2033. The market's US$ 700 million absolute dollar opportunity is driven by expanding pharmaceutical patent portfolios, AI integration in patent platforms, and growing IP intelligence needs across biotech and CRO sectors.

Growing investments in biologics, precision medicine, gene therapy, and medical devices are creating the need for advanced patent landscape analysis and portfolio management solutions.

North America leads with approximately 37% global market share in 2026. The United States, accounting for ~84% of North America's revenue, is driven by over 6,000 pharmaceutical and biotechnology companies per PhRMA, the USPTO's robust filing infrastructure, and deep enterprise adoption of AI-powered patent intelligence platforms by Big Pharma and CRO organizations.

Increasing pharmaceutical and biotechnology R&D activities, coupled with the rising complexity of biologics, gene therapies, and personalized medicine patents, are driving demand for advanced analytics platforms.

The leading companies include Clarivate Plc, LexisNexis, Questel, PatSnap, Anaqua Inc., CPA Global, IFI Claims Patent Services, IPlytics GmbH, Gridlogics Technologies Pvt. Ltd., InnovationQ Plus, Minesoft Ltd., and Orbit Intelligence.