- Healthcare Services

- Cell and Gene Therapy Contract Research Organizations Market

Cell and Gene Therapy Contract Research Organizations Market Size, Share, and Growth Forecast 2026 - 2033

Cell and Gene Therapy Contract Research Organizations Market by Development Stage (Drug Discovery, Preclinical), Service (Project and Clinical Trial Management, Regulatory Strategy), Indication (Oncology, CNS Disorders), and Regional Analysis, 2026 - 2033

Cell and Gene Therapy Contract Research Organizations Market Size and Trends Analysis

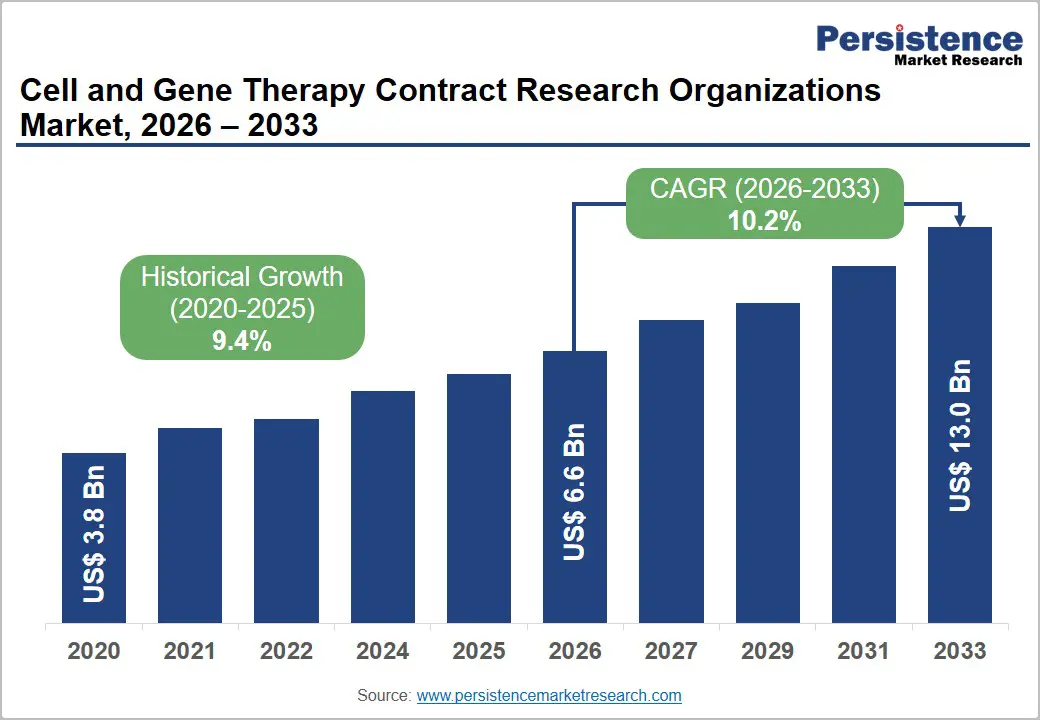

The global cell and gene therapy contract research organizations market size is likely to be valued at US$6.6 billion in 2026 and is estimated to reach US$13.0 billion by 2033, growing at a CAGR of 10.2% during the forecast period from 2026 to 2033, driven by the rising number of cell and gene therapy clinical trials and increasing outsourcing by biotechnology companies seeking access specialized scientific and regulatory expertise.

Key Industry Highlights:

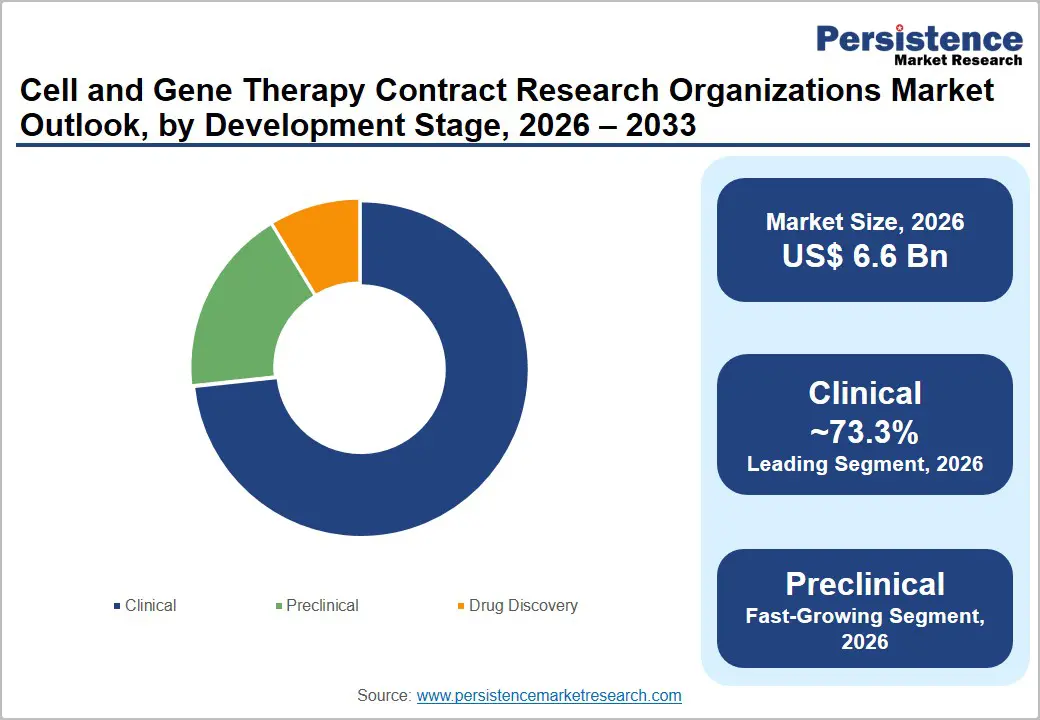

- Leading Development Stage: Clinical, approximately 73.3% share in 2026, as it requires extensive outsourcing for complex trial management, patient monitoring, and regulatory compliance.

- Dominant Service: Clinical monitoring, nearly 42.6% share in 2026, as cell and gene therapy trials require continuous patient safety oversight and long-term follow-up.

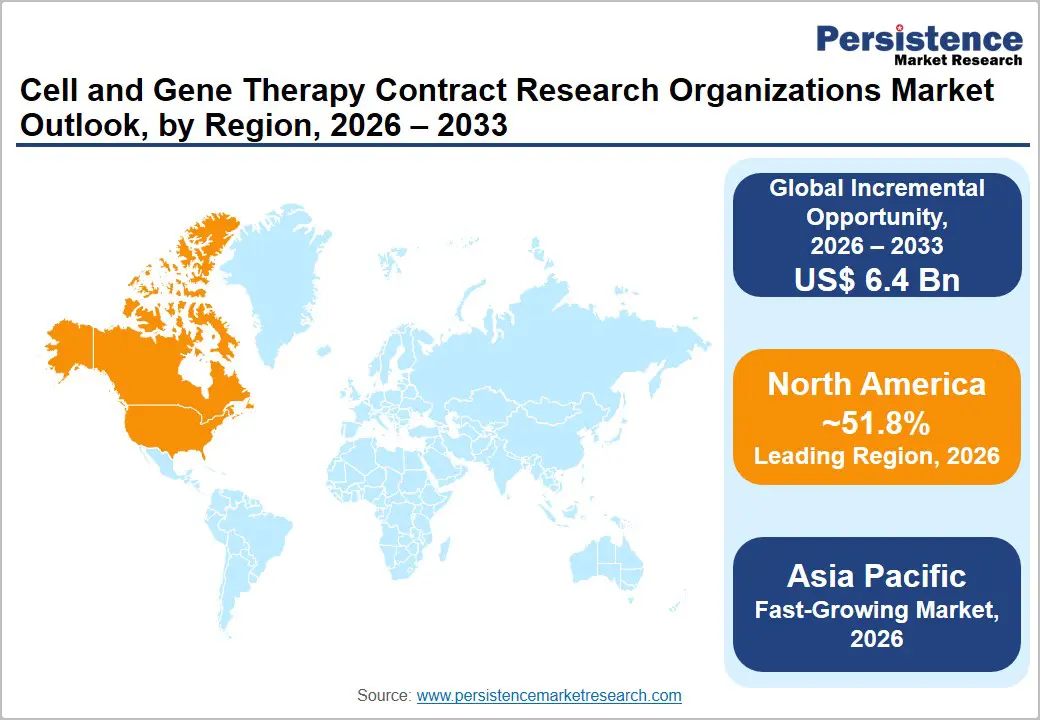

- Leading Region: North America, with about a 51.8% share in 2026, owing to its strong concentration of cell and gene therapy developers.

- Fast-growing Region: Asia Pacific, backed by rising biotechnology investments and improving regulatory frameworks.

- Recent Approval: In July 2025, Genethon received regulatory approvals from the U.K.'s MHRA and the European Medicines Agency (EMA) to initiate pivotal Phase III clinical trials for GNT0004, its gene therapy candidate for Duchenne muscular dystrophy. The approvals mark a significant advancement in late-stage gene therapy development and create additional opportunities for specialized CROs supporting multinational clinical trials.

DRO Analysis

Driver - Increasing Prevalence of Cancer and Genetic Disease

The clinical case for Cell and Gene Therapies (CGT) rests on a patient population that has no curative alternative under conventional drug treatment. According to the World Health Organization (WHO), globally, there were an estimated 20 million new cancer cases and 9.7 million deaths in 2022 alone. In 2050, more than 35 million new cancer cases are predicted, which will be a 77% surge from the 20 million cases in 2022. It underscores a pressing demand for advanced treatments that target late-stage tumors through immunotherapy.

The genetic disease burden adds a second, distinct patient pool. According to WHO, as cited in an August 2025 report, approximately 7.74 million people globally were living with sickle cell disease in 2021. Sickle cell disease is a single-gene disorder that is now treatable with Food and Drug Administration (FDA)-approved gene therapies such as Casgevy. As both cancer incidence and the catalog of identifiable single-gene disorders continue to rise, the population of patients eligible for CGT treatment expands in parallel. Every patient treated requires a Contract Research Organization (CRO) or Contract Development and Manufacturing Organization (CDMO) to manufacture, test, and monitor that therapy.

Capital Concentration in Manufacturing Infrastructure

While venture funding for early-stage CGT biotech companies has tightened considerably in recent years, capital has shifted decisively toward manufacturing infrastructure, thereby benefiting CDMOs and CROs. According to PharmaSource's 2025 industry tracking report, which monitored 732 CDMO announcements throughout the year, total disclosed investment in CDMO capacity reached US$24.86 billion in 2025, with September alone accounting for US$7.17 billion. It was the highest single month of the year. Cell and gene therapy was a named priority in that spending.

The same report confirmed that specialized cell and gene therapy facilities opened at Made Scientific in New Jersey, ProBio in New Jersey, and multiple sites across Europe, as CGT manufacturing moves from academic labs to industrial scale. Also, Lonza launched a dedicated Cell and Gene Technologies Division, and AGC Biologics extended its global CGT-capable network. This shows a structural shift. Large pharmaceutical and institutional capital are now funding manufacturing capacity, rather than waiting for biotech sponsors to raise their own funds first. This is sustaining CRO and CDMO demand even through a slow biotech venture funding cycle.

Restraint - Low-Throughput Testing Methods May Create a Manufacturing Bottleneck

Quantifying the quality and potency of Adeno-Associated Virus (AAV) vectors remains a key technical bottleneck. Multiple analytical methods, including electron microscopy, analytical ultracentrifugation, and mass spectrometry, must currently be run in parallel as no single method offers both the sensitivity and throughput required at a commercial level. A 2025 peer-reviewed review published in Frontiers in Molecular Medicine confirmed that current methods of analytical process development face hurdles in terms of lengthy turnaround time for analysis and low throughput.

There is a definite requirement for benchmarking the variability of potency and genome titer assays across the market. This testing constraint has direct downstream consequences. A separate peer-reviewed analysis on AAV manufacturing scale-up confirmed that long development and manufacturing timelines add high overhead costs and increase the complexity of bringing AAV-based therapies to market. As more CGT sponsors move from clinical-level to commercial-level production, this analytics gap becomes a binding constraint on how quickly CROs and CDMOs can release batches for use.

Opportunity - Decade-Long Patient Monitoring Requirements to Create New Services

The U.S. Food and Drug Administration (FDA) treats gene therapies differently from conventional drugs as their effects can be permanent. According to an October 2025 analysis published by Hogan Lovells covering the FDA's new draft guidance, the agency now recommends a range of follow-up periods based on the specific type of gene therapy, extending from up to five years for AAV vectors to fifteen years for integrating vectors. This requirement has proven challenging in practice for companies that cease operating within that timeframe.

The FDA's October 2025 draft guidance, titled Postapproval Methods to Capture Safety and Efficacy Data for Cell and Gene Therapy Products, now formally recommends that sponsors provide a plan for follow-up, including funding, in the event the sponsor ceases to operate the study before completion. This creates a long-duration and recurring revenue category for CROs capable of building and maintaining multi-year patient registries that outlive the original sponsoring biotech company.

End-to-End Manufacturing Consolidation to Reduce Delays between Discovery and Production

CGT sponsors have historically had to coordinate across multiple separate vendors, creating delays and knowledge loss at every handoff. Large CROs are now consolidating these functions into single and integrated organizations. Charles River Laboratories has built this model through its CDMO division. According to the company, its global CDMO network has supported the development of 24 FDA-approved cell and gene therapies and conducted more than 1,000 studies in the field over the past year. It follows an integrated approach that combines research and development with Chemistry, Manufacturing, and Controls (CMC) as well as biologics testing to maximize knowledge transfer, reduce bottlenecks, and boost drug development.

In September 2025, Charles River Laboratories announced a formal alliance with the Parker Institute for Cancer Immunotherapy. This gave its CDMO Centers of Excellence direct access to support Phase I clinical trial manufacturing for institutions such as Children's Hospital Los Angeles. As CGT sponsors prioritize speed-to-clinic over vendor diversification, this single-provider, discovery-to-commercialization model is becoming a deciding factor in CDMO selection.

Category-wise Analysis

Development Stage Insights

The clinical segment is predicted to lead with a share of approximately 73.3% in 2026, as it requires the highest level of outsourcing and technical expertise. Unlike conventional drugs, cell and gene therapies involve complex trial protocols, personalized treatments, long-term patient monitoring, and strict handling of genetically modified products. Most biotechnology companies developing these therapies are small or mid-sized and lack the infrastructure to manage global clinical trials on their own. Hence, they depend heavily on CROs for trial design, site management, patient recruitment, data management, biomarker testing, and regulatory submissions.

The preclinical segment is estimated to be the fastest-growing over the forecast period, as it determines whether a cell or gene therapy is safe enough to enter human testing. At this stage, developers must evaluate biodistribution, toxicity, immune responses, vector persistence, genome editing accuracy, and off-target effects. These studies are far more specialized than those required for traditional medicines and often require advanced laboratory platforms that many therapy developers do not possess internally.

Service Insights

The clinical monitoring segment is anticipated to dominate with a share of nearly 42.6% in 2026, as cell and gene therapy trials require much closer oversight than conventional clinical studies. These therapies often involve critically ill patients, individualized treatments, specialized manufacturing logistics, and potential long-term safety risks. CROs continuously verify patient safety, protocol compliance, investigational product handling, adverse event reporting, and data accuracy throughout the study.

The regulatory strategy segment is expected to remain in the second position in 2026, as cell and gene therapies are developed under evolving regulatory frameworks that differ significantly from those for traditional medicines. Companies need expert guidance on regulatory pathways, Investigational New Drug (IND) submissions, chemistry, manufacturing and controls (CMC), accelerated approval programs, orphan drug incentives, and long-term follow-up requirements. Several emerging biotechnology companies lack in-house regulatory teams, making CRO support increasingly valuable.

Regional Insights

North America Cell and Gene Therapy Contract Research Organizations Market Trends

North America is predicted to dominate in 2026 with a global share of approximately 51.8%, as it has the world's largest concentration of cell and gene therapy developers, academic research centers, and specialized CROs. The region also benefits from a well-established regulatory framework, superior venture capital funding, and a well-established outsourcing culture. Most biotechnology companies in the U.S. outsource complex activities such as clinical trial management, regulatory consulting, biomarker analysis, and long-term patient follow-up instead of building these capabilities internally.

U.S. Cell and Gene Therapy Contract Research Organizations Market Trends

A regional share of nearly 67.2% is expected to be held by the U.S. in 2026, as it remains the global center for advanced therapy innovation. Most pioneering work in CAR-T therapy, CRISPR-based gene editing, AAV gene therapy, and regenerative medicine originates from U.S.-based biotechnology companies, universities, and research hospitals. This creates continuous demand for specialized CRO services across preclinical, clinical, regulatory, and post-approval stages. Regulatory support is another key growth driver. The FDA provides programs such as the Regenerative Medicine Advanced Therapy (RMAT) designation to boost the development of promising therapies.

Asia Pacific Cell and Gene Therapy Contract Research Organizations Market Trends

Asia Pacific is anticipated to be the fastest-growing region with a global share of nearly 28.1% in 2026, as governments are investing heavily in biotechnology, precision medicine, and advanced manufacturing. Countries across the region have introduced policies to strengthen domestic cell and gene therapy research, improve clinical trial infrastructure, and attract global pharmaceutical investment. Low development costs and fast patient recruitment also encourage multinational companies to conduct studies in the region.

China Cell and Gene Therapy Contract Research Organizations Market Trends

China is expected to lead with a regional share of around 39.5% in 2026, as the government has prioritized biotechnology through long-term industrial policies and increased investments in innovative medicines. China-based biotechnology companies are developing a large number of CAR-T therapies, gene therapies, and genome-editing products, further creating significant demand for CRO expertise in clinical operations, regulatory support, and laboratory testing.

India Cell and Gene Therapy Contract Research Organizations Market Trends

In 2026, India is projected to account for a share of approximately 26.3% in 2026, as it combines a large scientific workforce with competitive research costs and increasing government support for biotechnology. India-based CROs have built superior capabilities in clinical data management, bioanalytical testing, pharmacovigilance, and regulatory documentation, allowing them to expand into advanced therapy research. Government initiatives are also supporting the market. The Department of Biotechnology (DBT) and the Indian Council of Medical Research (ICMR) have issued national guidelines for stem cell research and continue to support regenerative medicine projects through funding and research collaborations.

Europe Cell and Gene Therapy Contract Research Organizations Market Trends

Europe will likely see decent growth over the forecast period with a global share of nearly 13.4% in 2026, as it has a well-established scientific base, supportive regulatory pathways, and extensive collaboration between academia, hospitals, and biotechnology companies. Several countries in the region have well-developed research networks for rare diseases and regenerative medicine, which are prominent application areas for cell and gene therapies. Europe also emphasizes long-term safety monitoring and real-world evidence collection after approval, creating ongoing opportunities for CROs involved in clinical monitoring, pharmacovigilance, and regulatory compliance.

Germany Cell and Gene Therapy Contract Research Organizations Market Trends

Germany will likely register a substantial regional share of approximately 33.5% in 2026, owing to its advanced biotechnology sector, world-class universities, and high concentration of pharmaceutical manufacturers. Organizations such as the Paul Ehrlich Institute actively regulate and support advanced therapy development, while leading academic centers conduct research in gene editing, stem cell therapy, and cancer immunotherapy. Germany also benefits from close collaboration between research institutes and industry.

U.K. Cell and Gene Therapy Contract Research Organizations Market Trends

The U.K. is expected to account for around 27.3% of the regional share in 2026, as it combines superior life sciences research with supportive government initiatives for advanced therapies. The country hosts leading universities, biotechnology companies, and specialized organizations that focus on translating laboratory discoveries into commercial treatments. A key growth driver is the Cell and Gene Therapy Catapult, which supports therapy developers through process development, manufacturing innovation, and commercialization.

Competitive Landscape

The global cell and gene therapy contract research organizations market is moderately fragmented, with competition shared between large full-service CROs, specialized advanced therapy CROs, and regional niche providers. No single company dominates, as sponsors select partners based on expertise in specific modalities such as CAR-T, gene editing, viral vectors, or rare disease trials rather than total company size. This has created a landscape where established CROs such as IQVIA, ICON, Labcorp, Medpace, Syneos Health, and Thermo Fisher compete alongside specialist providers, including Allucent, QPS, Precision for Medicine, and Altasciences.

Competition is centered on end-to-end capabilities instead of standalone clinical trial management. Biotech companies prefer CROs that can support study design, biomarker development, regulatory strategy, patient recruitment, decentralized trials, genomic analytics, and long-term follow-up under a single contract. Hence, several CROs have expanded through acquisitions and strategic partnerships rather than building capabilities organically.

Key Industry Developments

- In June 2026, Merck KGaA announced a definitive agreement to acquire Bio-Techne for approximately US$11.3 billion. Merck stated that the acquisition would strengthen its Life Science business by expanding capabilities in cell and gene therapy research tools, biologics, and precision diagnostics, strengthening its position in advanced therapy development.

- In January 2026, Eli Lilly entered a collaboration worth up to US$1.12 billion with Seamless Therapeutics to develop gene-editing therapies for hearing loss. The agreement gives Lilly access to Seamless' programmable recombinase technology, expanding investment in next-generation genetic medicines and increasing demand for specialized preclinical and clinical development partners.

- In November 2025, Bharat Biotech launched Nucelion Therapeutics, a wholly owned subsidiary focused on cell and gene therapy contract research, development, and manufacturing (CRDMO) services. The company established a GMP-compliant facility in Genome Valley, Hyderabad, offering plasmid DNA production, viral and non-viral vector manufacturing, cell therapy production, and aseptic fill-finish services for global developers.

Companies Covered in Cell and Gene Therapy Contract Research Organizations Market

- Altasciences

- Allucent

- Labcorp

- Linical

- Medpace

- Thermo Fisher Scientific Inc.

- Precision Medicine Group, LLC.

- QPS Holdings

- Syneos Health

- ICON plc

- Others

Frequently Asked Questions

The global cell and gene therapy contract research organizations market is projected to be valued at US$6.6 billion in 2026.

The cell and gene therapy contract research organizations market is expected to reach US$13.0 billion by 2033.

Key market trends include the adoption of AI in clinical trial management and the expansion of integrated CRO-CDMO service models.

Clinical is expected to be the leading development stage with a share of nearly 73.3% in 2026, as the rising number of cell and gene therapy candidates entering human trials is pushing demand for specialized CRO expertise.