- Healthcare Services

- Geriatric Care Services Market

Geriatric Care Services Market Size, Share and Growth Forecast, 2026 - 2033

Geriatric Care Services Market by Service Type (Home Care Services, Adult Day Care Services, Residential Care Services), Disease (Alzheimer's, Cardiovascular Diseases, Parkinson’s Disease, Stroke, Arthritis, General Frailty, Others), Payment Source (Government Programs, Private Insurance, Out-of-Pocket Payments), and Regional Analysis for 2026 - 2033

Geriatric Care Services Market Share and Trends Analysis

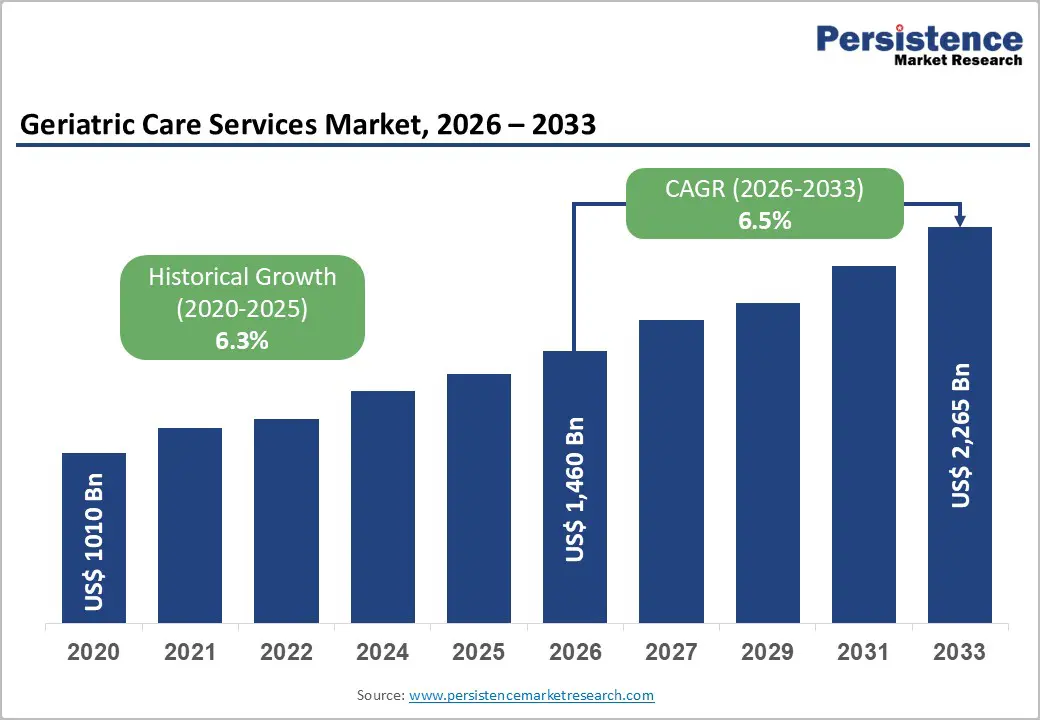

The global geriatric care services market size is likely to be valued at US$ 1,460 billion in 2026 and is projected to reach US$ 2,265 billion by 2033, growing at a CAGR of 6.5% during the forecast period 2026 - 2033.

The market expansion reflects rapid population aging, rising prevalence of chronic diseases among elderly populations, and increasing demand for long-term and home-based healthcare services. According to global demographic projections, individuals aged 65 years and older are expected to represent a significantly larger share of the total population by 2030, increasing demand for geriatric healthcare services, assisted living, and elderly home care solutions.

Additionally, healthcare systems are prioritizing cost-effective long-term care models, driving the adoption of home care services, adult day care programs, and institutional care facilities. Continuous integration of digital health technologies, remote monitoring, and coordinated geriatric care management systems is further strengthening the global elderly care services market outlook.

Key Industry Highlights

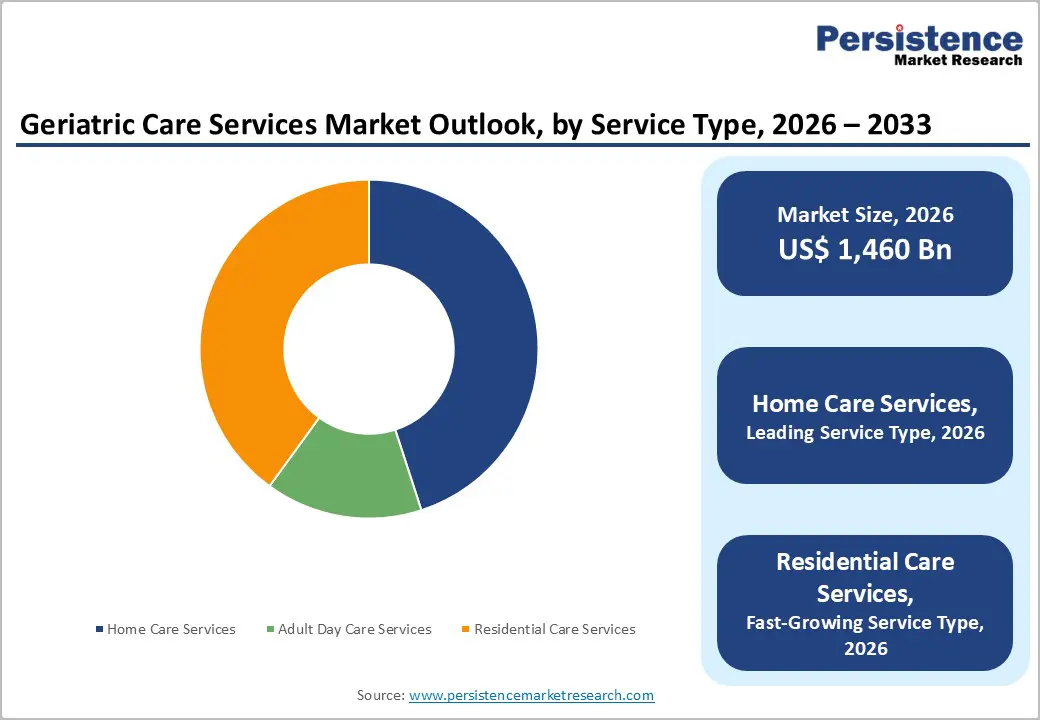

- Dominant Service Type: Home care services are set to command around 45% of revenue share in 2026, while adult day care services are likely to grow the fastest at 7.2% CAGR, driven by aging-in-place preferences.

- Leading Disease Segment: Cardiovascular disease-related care services are expected to lead with 38% share in 2026, while Alzheimer’s disease care services are projected to grow fastest at 7.8% CAGR due to rising dementia prevalence.

- Payment Source Leadership: Government programs are estimated to account for 50% of revenue in 2026, while private insurance is likely to expand fastest at 6.9% CAGR by 2033, supported by rising long-term care awareness.

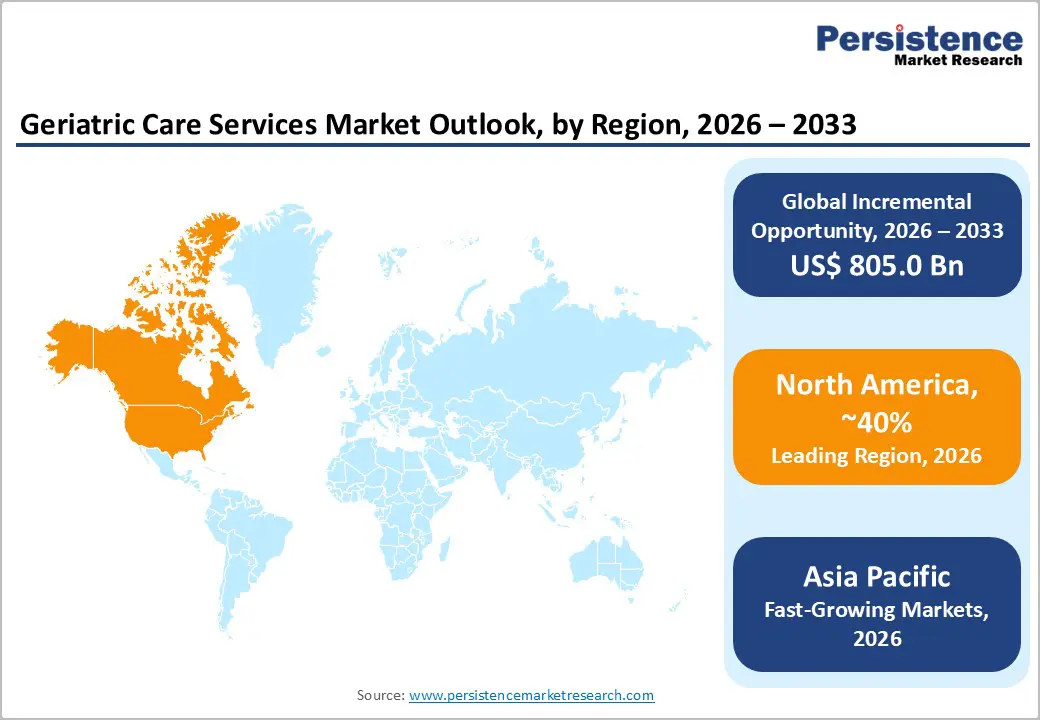

- Regional Leadership: North America is poised to lead with 40% revenue share in 2026, while Asia Pacific is expected to grow fastest at 7.5% due to population aging and infrastructure expansion.

- Competitive Environment: Market growth is shaped by mergers, acquisitions, digital health adoption, and geographic expansion, with providers focusing on home care, telehealth, and specialized dementia services.

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Expansion of the Global Aging Population

The global elderly population is expanding rapidly, driving significant demand for a wide spectrum of geriatric care services, including home healthcare, assisted living, and long-term clinical support programs. According to WHO and United Nations projections, the number of individuals aged 60 years and above is expected to rise from approximately 1 billion in 2020 to 2.1 billion by 2050, with developed economies such as the U.S., Japan, and Germany already exceeding 20% of their population aged 65+. This demographic shift is elevating the need for scalable care infrastructure and specialized senior services globally.

In response, governments are actively adapting healthcare systems: Vietnam’s Ministry of Health advanced its National Elderly Care Strategy in 2025, allocating resources to expand community-based care networks, long-term care centers, and caregiver training programs. Further, Hanoi launched the Elderly Healthcare Complex Project in early 2026, integrating clinical support, wellness services, and home care coordination to address aging demands. These verified public-sector moves emphasize that population aging is not only a long-term projection but an immediate strategic priority, directly boosting investment, service expansion, and sector capacity building across regions.

Rising Burden of Chronic and Age-Related Diseases

The prevalence of chronic and age-related diseases among older adults remains a core driver of demand for professional geriatric care services, as long-term clinical supervision and rehabilitation become essential components of comprehensive care. Data from the CDC shows that approximately 80% of older adults live with at least one chronic condition, and nearly 70% have two or more, including Alzheimer’s disease, cardiovascular disorders, arthritis, and stroke-related disabilities, which require ongoing monitoring and multidisciplinary care. These complex health needs are expanding the role of geriatric service providers beyond episodic treatment to continuous disease management and preventive support.

The governments are responding with enhanced care access initiatives. In 2026, China launched expanded home-based elderly care subsidies, distributing more than 1.7 billion yuan in vouchers for disabled seniors to access professional care services, acknowledging the care burden associated with chronic conditions. Vietnam’s “Elderly Healthcare - For a Healthy Vietnam in 2026” program also engaged seniors through nationwide health screenings, telehealth guidance, and education on chronic disease management. These official programs demonstrate that rising chronic disease prevalence is not just a health trend but a systemic driver accelerating demand for integrated geriatric care models, digital health solutions, and expanded caregiver capacity.

Barrier Analysis - High Cost of Long-Term Care Services

The high cost of long-term geriatric care is continuing to create significant barriers to market growth, particularly for middle- and low-income households with limited financial flexibility. Current surveys indicate that median annual expenses for long-term nursing home care are approximately US$114,975 for semi-private rooms and exceed US$74,000 for assisted living facilities, reflecting continuous inflation in staffing, medical supplies, and facility operations. These rising costs are forcing families to depend more heavily on informal caregiving networks, which are often underprepared to manage complex medical and daily care needs. Households with partial insurance coverage or government subsidies are still encountering financial pressures that limit their ability to access professional services, creating gaps in care continuity and quality.

As the population of elderly individuals grows, the combination of high costs and limited coverage is slowing the adoption of formal elderly care services, including home care, assisted living, and rehabilitation programs. Healthcare providers and private operators are responding by exploring scalable models for cost management, such as technology-enabled home care platforms and community-based support programs, which will be essential to meet rising demand. Over the next decade, these financial constraints are shaping investment priorities, influencing service delivery strategies, and compelling policymakers to enhance public funding and insurance schemes to ensure sustainable access to high-quality geriatric care.

Workforce Shortages in the Elderly Care Sector

The global geriatric care sector is currently facing persistent workforce shortages, which are affecting service quality, operational capacity, and the expansion of care programs. According to the U.S. Department of Health and Human Services (HHS), updated staffing standards issued in December 2025 highlight ongoing personnel deficits in rural and tribal nursing facilities, demonstrating that even advanced healthcare systems are struggling to maintain adequate staffing levels. These shortages are creating operational challenges for institutional facilities, home care providers, and community-based elderly care programs, limiting their ability to meet rising demand and ensure consistent patient outcomes.

Shortages of trained nurses, certified nursing aides, and geriatric specialists remain widespread across both developed and developing regions. In response, governments are implementing workforce development programs; for example, in March 2026, India launched a national initiative to upskill 150,000 caregivers, focusing on competencies in elderly care and health support services.

Despite these initiatives, high turnover, caregiver burnout, and limited access to specialized training are continuing to restrict service capacity. These workforce gaps are delaying the expansion of institutional facilities and home care programs, which will continue to constrain overall market growth as the global population ages rapidly.

Opportunity Analysis - Expansion of Home-Based Elderly Care Services

The increasing preference for aging in place is creating significant opportunities for home-based care services within the geriatric care market. Elderly patients now prefer medical supervision, rehabilitation, and daily assistance at home rather than in institutional settings, which enhances comfort and preserves independence. In India’s Union Budget 2026-27, the government announced plans to train 150,000 caregivers under the National Skills Qualifications Framework to strengthen home-based and long-term care capacity. Healthcare providers are responding by expanding home nursing services, telehealth, and coordinated care teams to meet this shift.

In Europe, pilot initiatives such as the deployment of smart assistive robots to support daily routines, medication reminders, and emergency detection in private homes are being funded through public grants to address workforce gaps and enhance home care outcomes. These moves are coupled with increasing telehealth support that connects seniors to remote clinical supervision and follow-ups.

As aging-in-place models gain traction, home healthcare providers have opportunities to scale integrated solutions that reduce hospital admissions, improve continuity of care, and enhance quality of life for elderly individuals living at home.

Integration of Digital Health and Remote Monitoring Technologies

Technological innovation is reshaping the elderly care ecosystem, with digital health and remote monitoring solutions offering new avenues for market expansion. Wearable devices and telehealth platforms are increasingly mainstream in chronic disease management, enabling continuous monitoring of vital signs, medication adherence, and mobility without requiring travel. Governments and public payers are strengthening tele-monitoring services with supportive reimbursement frameworks, which is driving adoption of remote care solutions in chronic and elderly care settings.

In parallel, healthcare organizations are trialing age-friendly digital care models and AI-assisted systems that support cognitive engagement, medication reminders, and real-time health tracking. For example, a pilot program in New York provided “AI companion” devices to seniors through the New York State Office for the Aging, enabling virtual interaction, daily reminders, and social engagement via TV-based interfaces.

Combined with broader health system commitments, such as multi-million visit telehealth programs and evolving hybrid remote/in-person care models, these innovations are creating substantial opportunities for providers, insurers, and technology firms to integrate digital health into scalable eldercare services.

Category-wise Analysis

Service Type Insights

Home care services are expected to lead the geriatric care market with an estimated 45% revenue share in 2026, driven by global demand for aging-in-place solutions. Seniors increasingly opt for care at home for personalized medical supervision, rehabilitation therapy, and daily assistance, avoiding institutional relocation. Legislative initiatives and integrated care pathways, combined with remote monitoring adoption, are supporting this trend.

In 2025-2026, the U.S. “Hospital at Home” program extension through 2030 demonstrates a shift toward delivering acute and chronic care at home, easing hospital burden and improving care continuity. Providers are scaling home care offerings, incorporating digital tools, and improving clinical outcomes outside traditional facilities.

Adult day care services are projected to grow at 7.2% CAGR from 2026 to 2033, fueled by rising demand for community-based elderly programs offering daytime supervision, medical support, social engagement, and rehabilitation. These centers help families maintain work schedules while supporting seniors’ physical and cognitive health. Recent 2026 reporting highlighted the expansion of Programs of All-Inclusive Care for the Elderly (PACE) in the U.S., providing comprehensive services including transportation, meals, and clinical oversight. Urbanization, dual-income households, and supportive policies are further accelerating adoption, positioning adult day care as a key driver of market growth.

Disease Insights

Cardiovascular diseases represent the largest disease segment, with 38% of demand in 2026, due to high prevalence among elderly populations. Chronic heart conditions require long-term monitoring, medication management, and rehabilitation across hospitals, clinics, and home care. In 2025-2026, the global adoption of remote monitoring and predictive analytics for cardiac patients has enabled early intervention, reducing complications and hospital readmissions. Integration of digital health tools with preventive care initiatives is reinforcing the leading role of cardiovascular-focused geriatric care, ensuring sustained demand and investment in specialized programs.

Alzheimer’s disease is the fastest-growing segment, with an estimated 7.8% CAGR between 2026 and 2033, due to rising dementia prevalence worldwide. Patients require structured memory care, continuous supervision, and dedicated programs, prompting expansion of specialized facilities and caregiver training. In 2025, the World Health Organization highlighted telemedicine and telehealth models as effective for dementia care, improving supervision, social engagement, and caregiver support. These technology-enabled approaches are driving adoption, creating opportunities for providers to innovate and scale Alzheimer’s care services globally.

Regional Insights

North America Geriatric Care Services Market Trends

North America continues to hold the largest share of the global geriatric care services market, capturing approximately 40% of total revenue in 2026 due to advanced healthcare systems, widespread elderly care infrastructure, and strong public funding mechanisms. The United States remains the primary revenue generator as a growing elderly population fuels demand for home healthcare, assisted living, long-term care, and holistic care management services. Federal programs such as Medicare and Medicaid provide critical financial support, covering skilled nursing, rehabilitation, and home health services, enhancing care accessibility for seniors across income groups.

The additional government actions reinforced this leadership position; for example, the New York City Department for the Aging received a US$ 6.2 million funding boost to expand caregiver support programs, covering training, therapy, and case management for informal and family caregivers. This initiative reflects growing recognition of caregiver support as fundamental to the region’s elderly care ecosystem. Continued private investment in digital health platforms, telehealth solutions, and senior care community expansions further strengthens North America’s competitive edge in global geriatric care services, while encouraging innovation in remote patient monitoring and personalized care delivery.

Europe Geriatric Care Services Market Trends

Europe remains the second-largest regional market for geriatric care services, representing around 28% of global revenue in 2026, supported by comprehensive government-funded healthcare systems and aging population dynamics. Countries such as Germany, the United Kingdom, France, and Spain are increasing investments in institutional care, community healthcare networks, and home care solutions. Public long-term care insurance schemes in Germany and coordinated national healthcare programs in other European countries provide robust financial backing, enabling broader access to elderly care.

Recent developments underscore Europe’s ongoing policy engagement with eldercare needs. In early 2026, the Labour Party in the United Kingdom announced plans to appoint a national dementia tsar and undertake structural reforms to improve adult social care frameworks, aiming to enhance service quality and care access for dementia and frailty cases. This move reflects heightened government focus on strengthening care pathways and safeguarding vulnerable seniors. Coupled with investments in digital health integration, workforce training, and community care innovation, these policy developments reinforce Europe’s capacity to manage aging populations while sustaining high standards and operational efficiency in geriatric care delivery.

Asia Pacific Geriatric Care Services Market Trends

The Asia Pacific region is poised to experience the fastest growth in the geriatric care services market, with an estimated CAGR of around 7.5% from 2026 to 2033, driven by rapidly aging populations and expanding healthcare infrastructure. Countries such as China, Japan, India, and Southeast Asian economies are intensifying efforts to strengthen elderly care systems, including institutional care, community health programs, and home-based services. Japan’s high proportion of citizens aged 65 and older continues to push demand for diverse care solutions, while China is expanding community support networks to meet the needs of its growing senior demographic.

In 2025, China’s Ministry of Civil Affairs announced major enhancements to aged care meal assistance services and home- and community-based care networks, including plans to establish tens of thousands of affordable care beds and in-home services. These measures are part of a broader national strategy to strengthen care access and wellbeing for seniors. Combined with increasing private sector participation, insurance coverage expansion, and adoption of digital health monitoring tools, Asia Pacific’s elderly care sector is rapidly evolving and becoming a pivotal growth hub within the global market, attracting international investment and innovation.

Competitive Landscape

The global geriatric care services market exhibits a moderately consolidated structure, with leading players such as Brookdale Senior Living, Korian, LHC Group, and Nihon Care Services collectively controlling a significant portion of revenue. These established providers leverage extensive healthcare networks, regulatory compliance expertise, and integrated care delivery models. They also invest heavily in workforce training, telehealth platforms, and digital health technologies to maintain service quality, clinical outcomes, and operational efficiency across institutional, home, and community care segments.

Regional and niche competitors, including Revera Inc and Sodexo Senior Care Services , focus on specialized care offerings, memory care units, and localized service networks. Barriers such as labor shortages, regulatory compliance, and high operational costs limit entry for smaller players. However, digitalization, telehealth adoption, and remote monitoring technologies are enabling new service providers and health-technology companies to enter the market via innovative care delivery solutions. Market consolidation is expected to increase gradually as leading providers expand through acquisitions, partnerships, and technology integration to enhance geographic coverage, service diversity, and patient-centric care.

Key Industry Developments

- In February 2026, Barcelona launched 600 ARI robots with a €3.8 million EU grant to assist elderly residents with medication reminders, companionship, and telecommunication. The pilot also plans future emergency detection and environmental monitoring.

- In August 2025, UnitedHealth completed its US$ 3.3 billion acquisition of Amedisys, expanding home health and hospice services under OptumHealth. DOJ-required divestitures ensured regulatory compliance while strengthening in-home care offerings.

- In May 2025, Sunrise added premium boutique communities in California through a partnership with Griffin Living. The expansion enhances high-end assisted living and memory care with wellness and sensory therapy programs.

Companies Covered in Geriatric Care Services Market

- Brookdale Senior Living Inc.

- Amedisys Inc.

- Genesis Healthcare Inc.

- Sunrise Senior Living

- Kindred Healthcare

- Home Instead Inc.

- Extendicare Inc.

- Orpea Group

- DomusVi Group

- Colisée Group

- Sodexo Care Services

- Care UK

- Barchester Healthcare

- Benesse Style Care

Frequently Asked Questions

The global market is projected to reach approximately US$ 1,460 billion in 2026.

Rapid population aging, rising prevalence of chronic and age-related diseases, and increasing preference for home-based care drive market growth.

The market is expected to grow at a CAGR of 6.5% from 2026 to 2033.

Expansion of home care services, integration of digital health technologies, and emerging markets with aging populations present significant opportunities.

Key players include Brookdale Senior Living Inc., Amedisys Inc., Sunrise Senior Living, Kindred Healthcare, Extendicare Inc., and Home Instead Inc.