- Beauty & Personal Care

- Gemstone Cosmetic Powder Market

Gemstone Cosmetic Powder Market Size, Share, and Growth Forecast, 2026 – 2033

Gemstone Cosmetic Powder Market by Product Type (Diamond Powder, Quartz Powder, Pearl Powder, Amber Powder, Ruby Powder), Application (Skincare, Haircare, Makeup, Personal Care), and Regional Analysis for 2026 – 2033

Gemstone Cosmetic Powder Market Size and Trends Analysis

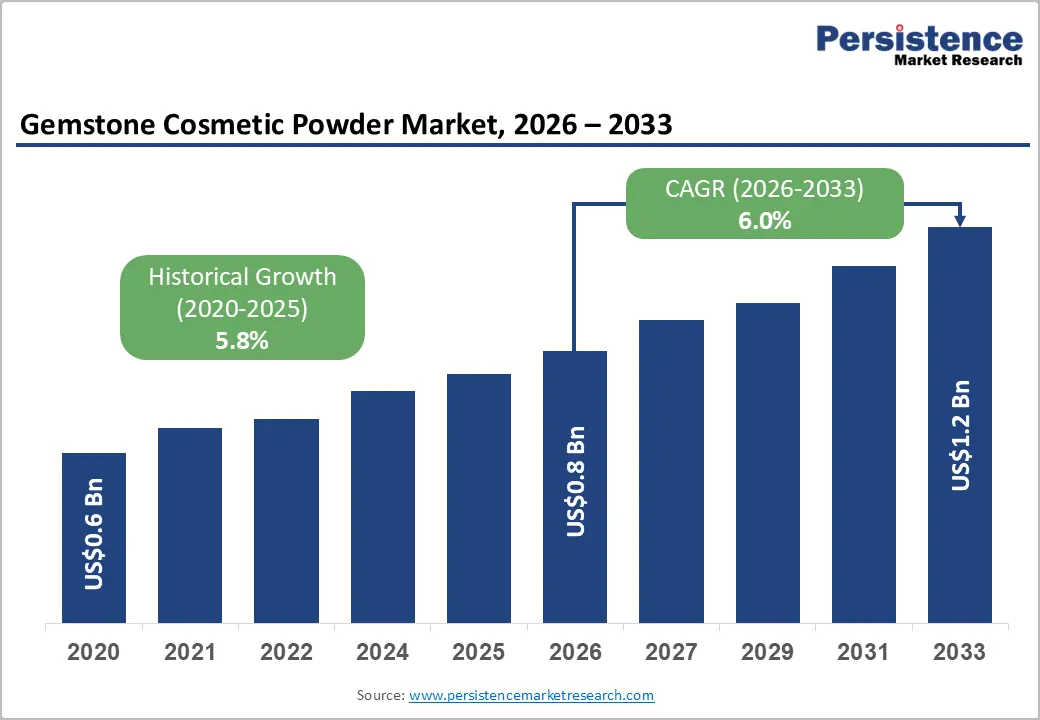

The global gemstone cosmetic powder market size is likely to be valued at US$0.8 billion in 2026 and is expected to reach US$1.2 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by rising consumer preference for natural, mineral-based, and premium cosmetic ingredients. Increasing incorporation of gemstone powders such as pearl, quartz, and diamond in skincare and makeup formulations is fueling demand, particularly for products offering radiance, anti-aging, and skin-enhancing benefits. The Asia Pacific region dominates the market, supported by cost-efficient manufacturing, abundant raw material availability, and strong growth in clean beauty adoption. Expanding regulatory approvals and certifications for natural and mineral cosmetics, coupled with innovation in multifunctional beauty products, are accelerating product launches and brand penetration.

Key Industry Highlights:

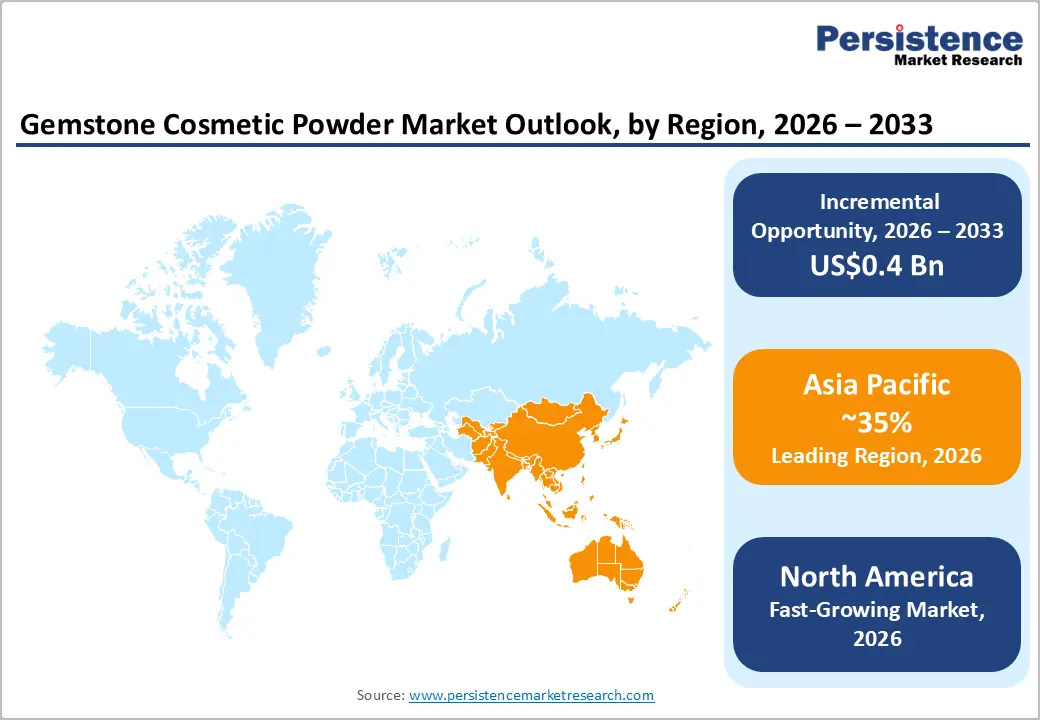

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong manufacturing capabilities, rapid urbanization, regulatory support for natural cosmetics, and rising regional demand for premium mineral-based beauty products.

- Fastest-growing Region: North America is likely to be the fastest-growing region, supported by rising clean beauty adoption, strong premium cosmetics demand, advanced R&D capabilities, high consumer awareness of mineral-based ingredients, and robust e-commerce penetration.

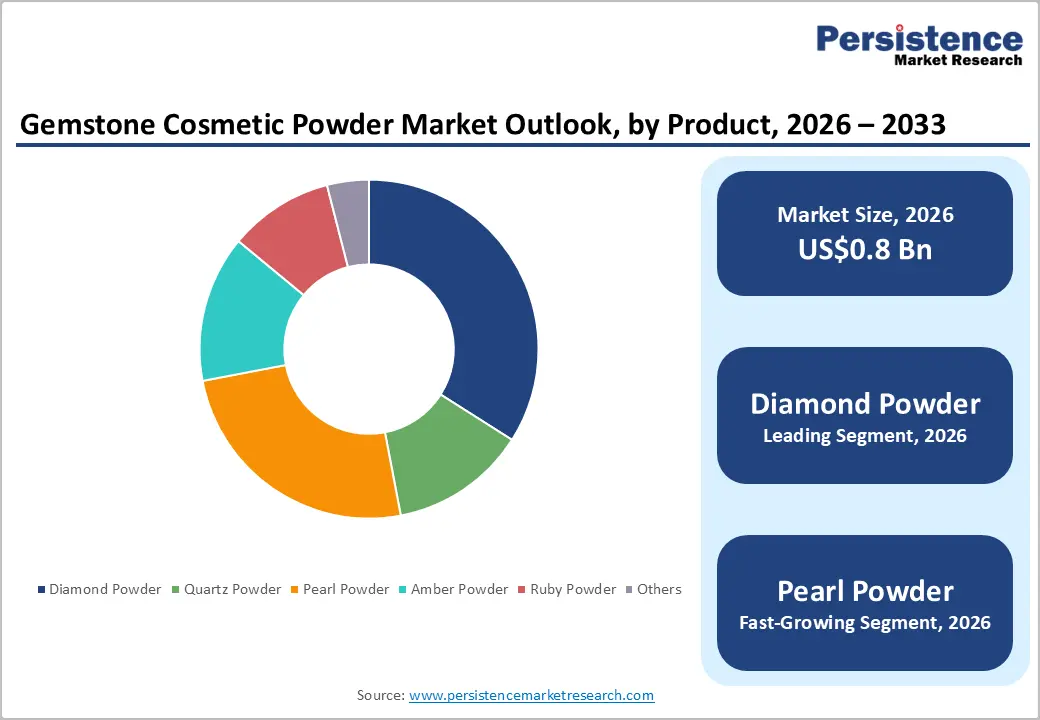

- Leading Product Type: Diamond powder is projected to represent the leading product type in 2026, accounting for 28% of the revenue share, driven by strong demand in premium skincare and exfoliation products. Growth remains robust but is slower than pearl-based formulations.

- Leading Application: Skincare is anticipated to be the leading application type, accounting for over 35% of the revenue share in 2026, supported by strong consumer focus on anti-aging and skin health. Growth remains stable but is surpassed by makeup applications.

| Key Insights | Details |

|---|---|

| Gemstone Cosmetic Powder Market Size (2026E) | US$0.8 Bn |

| Market Value Forecast (2033F) | US$ 1.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Natural and Organic Cosmetics

Buyers increasingly prioritize ingredient transparency, skin safety, and long-term wellness benefits. Heightened awareness of the potential side effects of synthetic chemicals such as parabens, phthalates, and artificial colorants has accelerated the demand for mineral-based alternatives perceived as gentler and skin-compatible. Gemstone powders, including pearl, quartz, and diamond, align well with clean beauty expectations due to their natural origin, minimal processing, and multifunctional properties such as exfoliation, radiance enhancement, and skin conditioning. This trend is particularly strong among millennial and Gen Z consumers, who actively seek eco-conscious and cruelty-free formulations.

Regulatory support for natural and organic cosmetic formulations strengthens this demand dynamic, encouraging manufacturers to replace synthetic fillers with mineral and gemstone-based ingredients. Certification frameworks and clean-label standards are pushing brands to reformulate products, increasing the adoption of gemstone cosmetic powders across skincare, makeup, and personal care categories. The influence of social media, beauty influencers, and dermatology-led marketing has also amplified consumer trust in mineral-rich cosmetics, positioning gemstone powders as both functional and aspirational ingredients. Rising disposable incomes and urban lifestyles are driving spending on premium beauty products that combine aesthetics with wellness benefits.

Limited Availability and Inconsistent Quality of Natural Gemstone Sources

Gemstone powders rely on geographically concentrated mining and extraction activities, making their supply highly sensitive to environmental regulations, policy changes, and geopolitical disruptions. Variations in mineral composition, purity levels, and crystal structure across different mining locations can result in inconsistencies in color, particle size, and functional performance of gemstone powders. These variations complicate standardization for cosmetic manufacturers, particularly those targeting premium skincare and makeup segments that demand uniform texture, appearance, and efficacy. Fluctuations in gemstone supply caused by mining restrictions, seasonal disruptions, or sustainability regulations can lead to raw material shortages, increasing procurement risks and price volatility for cosmetic brands.

Quality inconsistency also increases production complexity and compliance costs across the gemstone cosmetic powder value chain. Manufacturers must invest in advanced purification, micronization, and quality-testing processes to meet cosmetic-grade standards, which raises overall production expenses and extends time-to-market. For brands operating under strict regulatory frameworks, inconsistent gemstone quality may result in batch rejections or reformulation requirements, affecting scalability and product launch timelines. Ethical sourcing and environmental concerns surrounding gemstone mining restrict supplier options, narrowing access to reliable sources. Smaller and emerging brands are particularly impacted, as they often lack the financial capacity to secure long-term supply contracts or invest in quality control infrastructure.

Expansion of Premium and Luxury Skincare and Makeup Segments

High-end beauty consumers increasingly seek exclusive, high-performance, and naturally-derived ingredients. Gemstone powders such as pearl, diamond, ruby, and quartz are widely perceived as symbols of luxury and sophistication, making them well-suited for prestige beauty formulations. Premium brands leverage these ingredients to enhance product differentiation, aesthetic appeal, and perceived efficacy, particularly in anti-aging creams, illuminating powders, serums, and high-end makeup products. Rising disposable incomes, especially among urban consumers and affluent middle classes, are driving increased spending on luxury cosmetics that offer both visual enhancement and skincare benefits.

Luxury beauty brands are also focusing on innovation and exclusivity, creating limited-edition and bespoke formulations that incorporate gemstone cosmetic powders. This strategy enables companies to command higher margins while strengthening brand identity and consumer loyalty. The convergence of clean beauty and luxury trends has accelerated demand for mineral-based, ethically sourced gemstone ingredients in high-end cosmetics. The growing influence of social media, celebrity endorsements, and beauty influencers has significantly heightened consumer awareness of gemstone-infused luxury cosmetics, particularly across makeup segments such as highlighters, foundations, and finishing powders. As premium skincare and makeup continue to gain momentum in Asia Pacific and North America, gemstone cosmetic powders are increasingly positioned as aspirational ingredients, supporting sustained growth throughout the luxury cosmetics value chain.

Category-wise Analysis

Product Type Insights

Diamond powder is expected to lead the gemstone cosmetic powder market, accounting for approximately 28% of revenue in 2026, driven by its strong association with luxury, performance, and premium skincare positioning. Its fine exfoliating nature and ability to enhance skin radiance make it a preferred ingredient in high-end formulations, particularly facial powders, serums, and anti-aging creams. The ingredient’s high purity perception and visual appeal also resonate strongly with consumers seeking advanced skincare solutions that combine efficacy with indulgence. For example, luxury skincare brands often highlight diamond powder in illuminating face powders to emphasize refinement and superior finish, strengthening consumer trust and brand prestige.

Pearl powder is likely to represent the fastest-growing segment, supported by rising demand for natural radiance, anti-aging, and skin-brightening solutions. Consumers increasingly associate pearl powder with gentle nourishment, antioxidant properties, and cultural beauty traditions, particularly within Asian skincare routines. Its versatility across creams, masks, foundations, and finishing powders supports rapid adoption across both skincare and makeup categories. Brands are leveraging pearl powder to align with clean beauty narratives and consumer preference for naturally derived luxury ingredients. For example, premium Asian beauty brands incorporate pearl powder into brightening creams to emphasize luminosity and skin clarity.

Application Insights

Skincare is projected to lead the market, capturing around 35% of the revenue share in 2026, supported by strong consumer focus on skin health, anti-aging, and ingredient efficacy. Gemstone powders are widely incorporated into creams, serums, masks, and exfoliators to enhance texture, luminosity, and overall skin appearance. The growing preference for premium skincare routines has encouraged brands to integrate gemstone ingredients as functional yet aspirational components. Skincare consumers tend to value long-term benefits, making gemstone powders particularly attractive due to their mineral-based positioning and perceived skin-enhancing properties. For example, luxury skincare brands often include gemstone powders in facial creams to highlight rejuvenation and refinement, strengthening brand differentiation.

Makeup is likely to be the fastest-growing application, driven by the rising demand for glow-enhancing, mineral-based, and premium color cosmetics. Gemstone powders are increasingly used in foundations, highlighters, blushes, and finishing powders to deliver luminosity, smooth texture, and visual appeal. Social media trends and influencer-led beauty routines have accelerated consumer interest in radiant, flawless makeup looks, directly benefiting gemstone-infused formulations. Brands are using gemstone powders to elevate makeup products beyond color, positioning them as skin-friendly and luxurious. For example, the growing use of pearl or diamond-infused highlighters in premium makeup collections to emphasize shine and elegance.

Regional Insights

North America Gemstone Cosmetic Powder Market Trends

North America is likely to be the fastest-growing region in 2026, driven by strong momentum as consumer preferences shift toward premium, natural, and clean beauty products. With rising disposable incomes and heightened awareness of ingredient transparency, mineral-rich formulations have gained traction, particularly among millennials and Gen Z consumers who favor products with perceived skin benefits and minimal synthetic additives. Social media and influencer culture have amplified interest in gemstone-enhanced makeup and skincare, driving demand for glow-imparting powders and highlighters. E-commerce platforms and direct-to-consumer models are accelerating market reach, enabling niche and indie brands to scale rapidly.

There is also increasing uptake of multifunctional products that blend skincare and makeup benefits, such as illuminating setting powders and anti-aging primers. For example, Jane Iredale has incorporated pearl and mineral powders into its makeup collections, emphasizing both aesthetic glow and skin-friendly formulations. Other players are investing in R&D to enhance micronization technology and improve ingredient performance in makeup and skincare applications. Strategic partnerships with gemstone suppliers and dermatological endorsements help build credibility, fostering consumer trust in product efficacy and safety.

Europe Gemstone Cosmetic Powder Market Trends

Europe is likely to be a significant market for gemstone cosmetic powder in 2026, due to strong consumer demand for clean, natural, and ethically sourced beauty products, with a growing emphasis on sustainability and ingredient transparency. European consumers increasingly scrutinize product labels, preferring formulations free from synthetic additives such as parabens, sulfates, and talc, which aligns well with mineral-based gemstone powders that offer gentle, skin-friendly alternatives. Regulatory frameworks such as REACH and the EU Cosmetics Regulation reinforce safety and clean beauty standards, encouraging brands to innovate with mineral-rich ingredients and eco-conscious practices such as recyclable packaging and cruelty-free certification.

European brands are also leveraging heritage and craftsmanship to enhance market appeal, particularly in premium segments where tradition and quality are highly valued. For example, Charlotte Tilbury has strengthened its presence in European gemstone makeup by incorporating mineral and pearl-like pigments into highlighters and setting powders that emphasize radiant, natural finishes while aligning with modern clean beauty trends. This strategic use of gemstone-inspired elements helps bridge the gap between luxury and functionality, making such products popular in both everyday beauty routines and special occasion collections.

Asia Pacific Gemstone Cosmetic Powder Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by deep cultural affinity for natural beauty rituals, rapid adoption of clean and mineral based cosmetics, and increasing purchasing power among beauty consumers. Traditional beauty practices in countries have long valued natural ingredients such as pearl and crystal powders, which are now being integrated into contemporary skincare and makeup products with claims of radiance, anti aging, and skin enhancing benefits. The influence of K beauty and J beauty trends has been particularly strong, as brands frequently combine gemstone powders with innovative formulations that appeal to both functional performance and aspirational aesthetics.

Within this evolving trend landscape, both global and regional brands are capitalizing on market growth opportunities through targeted product innovation and localized marketing strategies. For instance, Shiseido has integrated gemstone-inspired elements with advanced Japanese beauty technology in select skincare products and powder foundations, appealing to consumers who value a blend of tradition-inspired benefits and modern performance. By fusing heritage-driven ingredients with cutting-edge formulation science, such brands reinforce their regional presence while addressing rising consumer demand for premium, natural, and multifunctional cosmetic solutions.

Competitive Landscape

The global gemstone cosmetic powder market exhibits a moderately fragmented structure, driven by the coexistence of established beauty giants and niche mineral based brands that focus on gemstone infused formulations, product innovation, and premium positioning. Market players differentiate themselves through a blend of clean beauty credentials, ethical sourcing, gemstone purity, and performance claims, which resonate with growing consumer demand for natural and luxury cosmetics. While some companies leverage broad distribution networks and R&D capabilities to build scale, a number of specialized brands emphasize niche positioning and storytelling to capture dedicated audiences.

With key leaders including L’Oréal S.A., Estée Lauder Companies Inc., Shiseido Company Limited, Jane Iredale, RMS Beauty, Youngblood Mineral Cosmetics, Alima Pure, ILIA Beauty, Lune+Aster, and Tarte Cosmetics commanding significant attention through extensive portfolios and reach, competition remains vibrant and evolving. These players compete through strategic product innovation, brand collaborations, and diversified distribution strategies that span retail, specialty stores, and e-commerce platforms, enabling them to capture shifting consumer preferences across regions and applications. Established conglomerates often integrate gemstone cosmetic powders into broader luxury and skincare portfolios, using their strong marketing and scientific capabilities to validate benefits and expand reach.

Key Industry Developments:

- In April 2025, gemstone-infused skincare continued its shift from a niche concept to a mainstream luxury ritual, driven by brands such as KNESKO. The woman-founded company blends clinical skincare science with holistic gemstone energy, infusing products with crystals like amethyst, rose quartz, and obsidian aligned to chakras. By positioning gemstone skincare as both performance-driven and emotionally resonant, KNESKO emphasizes intentional self-care, mindfulness, and a holistic approach to beauty that connects inner well-being with outer results.

- In February 2024, UNI-POWDER concluded its “Infinite Beauty Innovation on Powder” product launch in Guangzhou, spotlighting advancements in cosmetic powder technology. The event highlighted four key innovation areas: chip-grade high-purity silica, natural alternative materials, green encapsulation technologies, and efficiency-focused slurry solutions. Notably, the chip-grade high-purity silica, produced through a proprietary process, achieves semiconductor-level purity with reduced metallic impurities and precise particle size and sphericity, delivering a silky texture and enhanced performance in both loose and pressed powder formulations.

Companies Covered in Gemstone Cosmetic Powder Market

- Jane Iredale

- RMS Beauty

- Youngblood Mineral Cosmetics

- Alima Pure

- ILIA Beauty

- Lune+Aster

- Hourglass Cosmetics

- Becca Cosmetics

- Tarte Cosmetics

Frequently Asked Questions

The global gemstone cosmetic powder market is projected to reach US$0.8 billion in 2026.

The rising demand for natural, mineral-based, and premium beauty products that combine skincare benefits with aesthetic appeal

The gemstone cosmetic powder market is expected to grow at a CAGR of 6.0% from 2026 to 2033.

The key market opportunities lie in the growing demand for premium, multifunctional, and sustainably sourced gemstone-based cosmetics.

Jane Iredale, RMS Beauty, Youngblood Mineral Cosmetics, Alima Pure, and ILIA Beauty are the leading players.