- Medical Devices

- Gauze Pad Market

Gauze Pad Market Size, Share, and Growth Forecast, 2026 - 2033

Gauze Pad Market by Sterility (Sterile Gauze Pads, Non-Sterile Gauze Pads), Application (Wound Care, Burn Care, Post-Surgical Care, Others), End-User (Hospitals, Clinics, Home Care Settings, Others), and Regional Analysis for 2026 - 2033

Gauze Pad Market Share and Trends Analysis

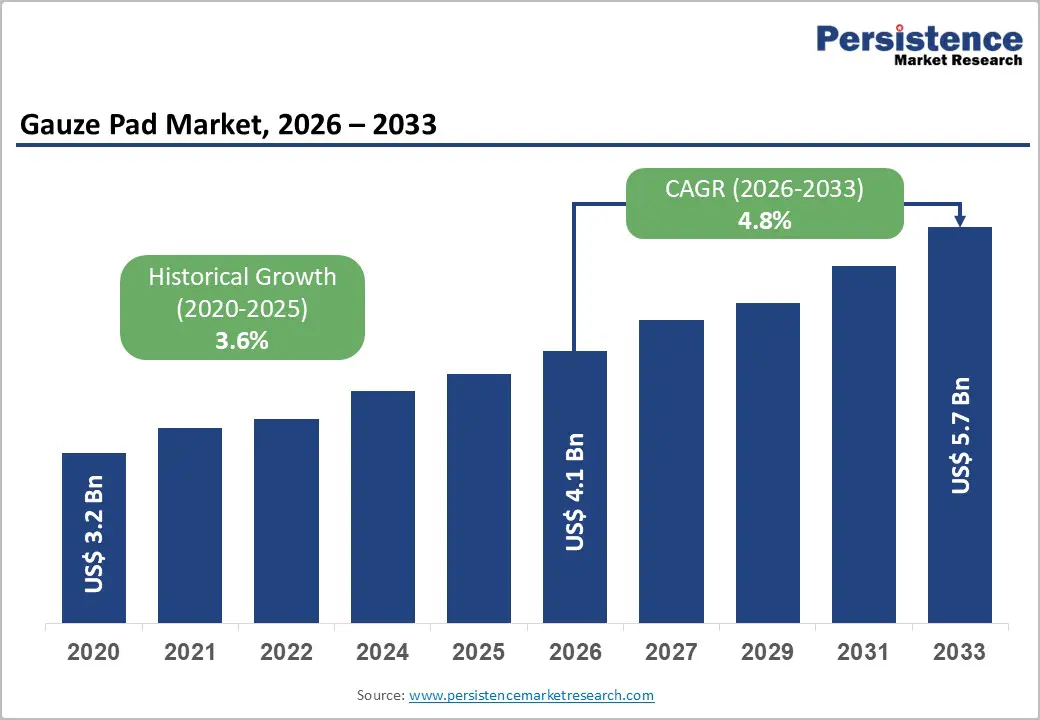

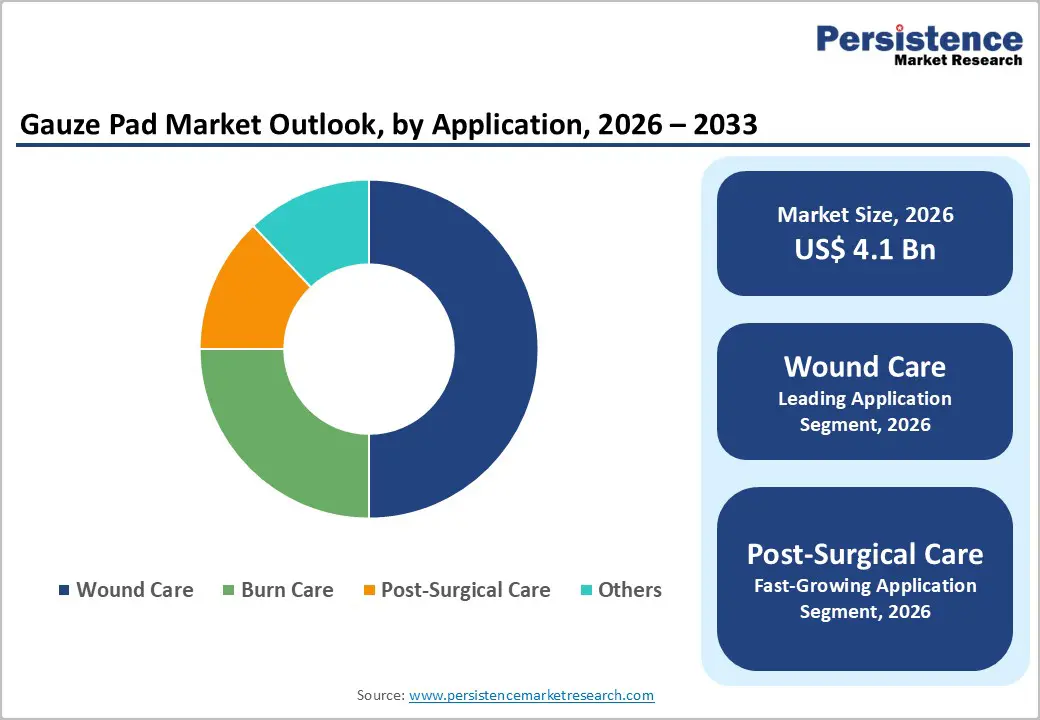

The global gauze pad market size is likely to be valued at US$ 4.1 billion in 2026, and is projected to reach US$ 5.7 billion by 2033, growing at a CAGR of 4.8% during the forecast period 2026−2033. The market demonstrates stable expansion driven by sustained clinical demand and healthcare system modernization.

Rising incidence of surgical procedures and trauma cases increases the volume of wound management interventions, directly expanding gauze pad consumption across acute and post-acute settings. Population aging, as documented by the World Health Organization (WHO), increases the prevalence of chronic wounds, including pressure injuries and diabetic ulcers, which require repeated dressing changes and infection control measures. Improved clinical awareness and standardized treatment protocols strengthen product adoption. Infection prevention frameworks promoted by the U.S. Centers for Disease Control and Prevention (CDC) reinforce the use of sterile dressings in surgical and inpatient environments. Increased outpatient procedures shift demand toward cost-efficient, disposable wound care materials suitable for ambulatory settings.

Key Industry Highlights

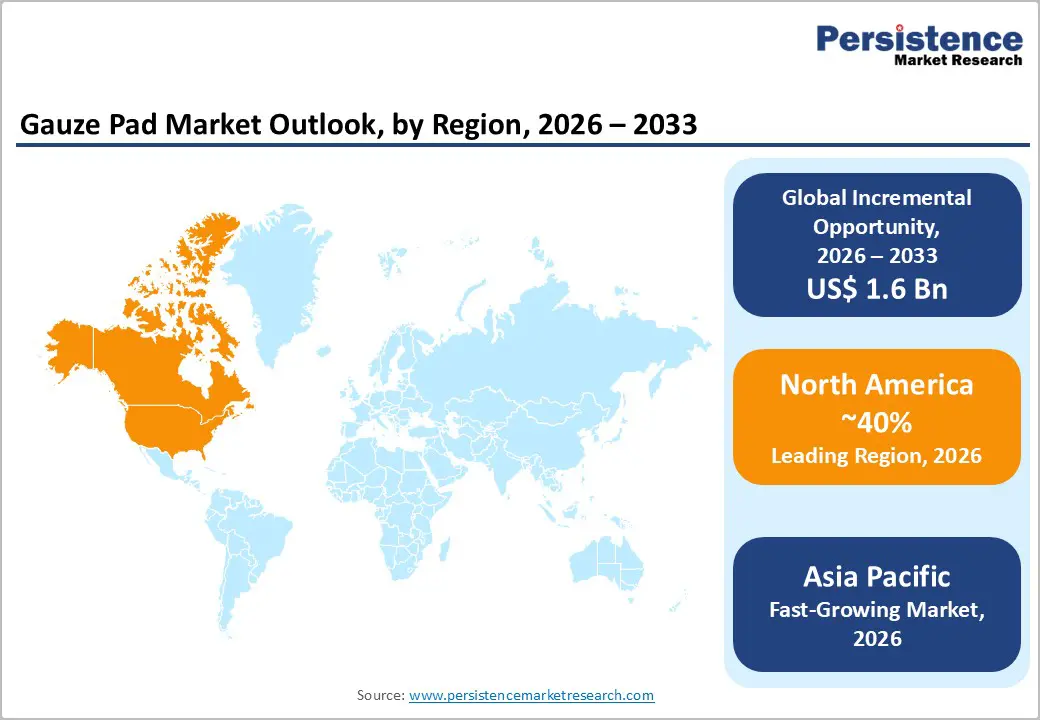

- Dominant Region: North America is projected to hold about 40% market share in 2026, driven by high surgical volumes and strict infection standards.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, supported by healthcare expansion and rising surgical volumes.

- Leading Application: Wound care extracts are expected to secure nearly 50% revenue share in 2026, reflecting the high incidence of acute and chronic wounds and strong retail availability.

- Fastest-growing Application: Post-surgical care is projected to be the fastest-growing segment from 2026 to 2033, driven by rising ambulatory surgeries and outpatient recovery demand.

| Key Insights | Details |

|---|---|

|

Gauze Pad Market Size (2026E) |

US$ 4.1 Bn |

|

Market Value Forecast (2033F) |

US$ 5.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Soaring Surgical Volume and Chronic Wound Burden

High volumes of surgical procedures directly influence demand for wound care solutions due to the sheer number of tissue-disrupting interventions requiring effective postoperative management. In modern health systems, surgical care represents a significant share of clinical activity, with the U.S. CDC reporting around 51.4 million inpatient procedures performed in U.S. hospitals in the most recent public health data available. Each surgical incision creates a wound that must be protected against contamination and fluid build-up, mandating sterile dressings to support tissue healing and prevent complications such as surgical site infections. The operational scale of surgeries fuels consistent consumption of essential dressings for wound coverage, exudate control, and infection prevention across inpatient, outpatient and ambulatory settings.

Chronic wounds impose sustained clinical and economic pressure on health services, driven by demographic and disease-related trends. U.S. health data indicate that chronic wounds affect over 5.7 million individuals, creating an ongoing need for reliable wound management interventions. These wounds, which include diabetic foot ulcers, pressure ulcers and venous leg ulcers, are characterized by prolonged healing times and elevated risk of secondary infection, requiring frequent dressing changes and extended clinical oversight. The high prevalence of chronic wounds among aging populations and people with chronic conditions creates a long-term demand for dressings that support moisture balance and protect vulnerable tissue, thereby encouraging sustained integration of wound care products into care pathways.

Healthcare Infrastructure Expansion and Standardized Infection Control

Expansion of physical and digital healthcare delivery capacity at hospitals, clinics, and community health centers strengthens the system's ability to manage higher patient volumes with improved clinical outcomes. Investment by the U.S. Department of Health and Human Services in public health infrastructure and capacity supports state, tribal, local, and territorial health departments in building systems that enhance service delivery, improve data interoperability, train clinical and support staff, and deploy surveillance platforms that detect risks early and reduce treatment delays. Funding directed at the modernization of facilities and the procurement of essential clinical resources supports stronger adherence to safety and hygiene protocols in care environments. Enhanced infrastructure enables quicker turnaround for patient care and standardized workflows that require consistent access to sterile dressings and supplies used in wound management across surgical, emergency, and long-term care settings.

High prevalence of healthcare-associated infections underscores the importance of standardized infection control protocols in clinical settings. According to the U.S. CDC, about 1 in 31 hospitalized patients in the United States experiences at least 1 healthcare-associated infection at any given time, reflecting persistent exposure risk in care facilities. Infection control programs guided by federal standards push hospitals and healthcare providers to adopt rigorous hygiene protocols, sterilization practices, and monitoring systems that reduce transmission of pathogens within facilities. Emphasis on preventing hospital-acquired infections drives the procurement and consistent use of sterile materials in patient care routines, creating sustained demand for products that support hygiene and safety practices.

Pricing Pressure and Commodity Product Characteristics

Intense price competition stems from the classification of basic wound dressings as standardized medical consumables within hospital procurement frameworks. Purchasing departments treat these items as interchangeable supplies with limited clinical differentiation, placing them in high-volume, low-margin categories subject to competitive bidding. Group purchasing organizations and public health systems emphasize cost-containment targets, leading to contracts awarded primarily on the basis of lowest price. Such commercial conditions constrain supplier negotiation power and limit pricing flexibility, particularly in large institutional tenders, where multi-year agreements lock in fixed rates. The absence of patented technology or complex manufacturing processes limits the ability to justify premium positioning, reinforcing a commodity perception across distribution channels.

Commodity characteristics further intensify margin compression by increasing supplier density and reducing switching costs for buyers. Healthcare providers can transition between manufacturers with limited operational disruption, strengthening purchaser leverage during contract renewal cycles. Production inputs such as cotton and sterilization services follow global price fluctuations, yet reimbursement frameworks and tender ceilings restrict the pass-through of rising costs to end users. This imbalance places sustained pressure on operating margins and working capital cycles. Private label expansion by distributors and hospital networks increases downward price benchmarks, compelling branded manufacturers to align with market clearing prices.

Competition from Advanced Wound Dressings

The rising adoption of advanced wound dressings poses a structural constraint on the gauze pad market. Products such as foam, hydrocolloid, alginate, and antimicrobial dressings are engineered to maintain optimal moisture balance, manage exudate more effectively, and support faster tissue regeneration. Clinical protocols in hospitals and specialty wound care centers increasingly prioritize evidence-based outcomes, shorter healing times, and fewer dressing changes. Advanced formats deliver extended wear time and improved patient comfort, which aligns with cost-efficiency objectives in value-based healthcare systems. Procurement teams evaluate total treatment costs rather than unit prices, shifting purchasing preferences toward solutions that reduce nursing time, minimize infection risk, and limit readmission rates.

The restraint is further reinforced by regulatory standards and reimbursement frameworks that favor clinically differentiated products with documented performance data. Advanced wound care manufacturers invest in research, clinical validation, and material science innovation, strengthening product positioning in high-acuity settings such as surgical recovery, diabetic ulcer treatment, and burn management. Training programs for clinicians increasingly emphasize moist wound-healing principles, encouraging a shift away from traditional dry dressings. Patient awareness regarding scarring, pain reduction, and infection control also influences demand patterns toward premium alternatives.

Expansion of Home Healthcare and Community-Based Treatment Models

The growing preference for delivering clinical and supportive care outside traditional settings is driving strategic shifts in healthcare service delivery. Data from the U.S. Centers for Medicare & Medicaid Services (CMS) and CDC highlight that home health care and related long-term services constitute a significant and rising portion of personal healthcare spending and capacity planning in the United States, reflecting public policy emphasis on care in community settings rather than institutional care. Home health care is classified by major U.S. health expenditure trackers as part of personal healthcare spending, underlining government recognition of its role in the broader continuum of care. Patients with chronic conditions, post-acute care needs, and those preferring to age in place higher value on at-home services, making community-based treatment models a focus area for public health programs seeking to reduce hospital readmissions, enhance patient outcomes, and manage costs within constrained budgets.

Service delivery closer to patient residences directly influences resource planning for medical supply requirements, enabling providers and payers to tailor product portfolios toward frequent dressing changes, infection control, and routine wound management outside inpatient facilities. Wider implementation of care plans outside hospitals reduces pressure on acute care capacity, supports transition care models, and aligns with numerous government health policy initiatives that advocate for decentralized health services. This diffusion of care pathways into patients’ homes increases the recurring use of consumables for routine daily care activities and chronic wound monitoring in non-acute environments, reflecting an operational shift that places greater emphasis on convenience, continuity of care, and cost efficiency within publicly funded healthcare frameworks.

Product Innovation in Advanced Wound Management Integration

Innovative wound management solutions that integrate advanced technologies into traditional wound-contact products are emerging as a strategic avenue for creating differentiation and clinical value. Rising incidences of chronic conditions such as diabetes contribute to a large and complex wound burden. U.S. federal public health data indicate that over 38 million people in the country are living with diabetes, a key risk factor for hard-to-heal wounds requiring more sophisticated care than standard dressings can provide, according to the CDC in 2025. Investment in smart, sensor-enabled, antimicrobial and bioactive materials allows continuous assessment of wound status, earlier detection of complications, and reduced infection risk.

Advanced wound management integration aligns with shifting care paradigms toward outpatient and home settings, where real-time monitoring and ease of use remain critical performance parameters. Technologies that automate moisture management, deliver targeted antimicrobial action, or connect with telehealth platforms meet the standards set by public health authorities for proactive chronic disease management and reduce reliance on frequent clinic visits. Enhanced product performance in these domains can translate into lower total cost of care, a priority underscored by federal programs emphasizing value-based reimbursement models.

Category-wise Analysis

Sterility Insights

The sterile segment is anticipated to claim around 65% of the gauze pad market revenue share in 2026, reflecting strong institutional reliance on infection-controlled wound management practices. Hospitals and surgical centers require sterile dressings for operative procedures and inpatient recovery protocols. Regulatory mandates on surgical site infection prevention reinforce procurement of validated sterile products. Clinical staff preference aligns with ready-to-use, individually packaged sterile formats that reduce contamination risk. Accessibility through centralized hospital supply chains supports consistent utilization. Continuous innovation in packaging integrity and sterilization assurance strengthens acceptance across acute care environments.

Non-sterile gauze pads are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by expanding home care adoption and cost-sensitive outpatient settings. Primary care clinics and community health centers use non-sterile formats for secondary dressing layers and general wound cleaning. Lower unit cost enhances affordability in emerging healthcare systems. Retail distribution and digital commerce expansion improve accessibility for home caregivers. Innovation in bulk packaging and improved fiber softness increases usability in non-critical applications.

Application Insights

Wound care extracts are poised to dominate with a forecasted market share of over 50% in 2026, powered by sustained incidence of acute injuries and chronic ulcers. Consumer trust in traditional gauze-based dressing methods reinforces baseline demand. Broad retail penetration across pharmacies ensures availability. Preventive healthcare awareness encourages early wound management, increasing dressing frequency. Digital commerce platforms facilitate repeat purchasing behavior for chronic wound patients. High prevalence of diabetic foot ulcers, pressure injuries in long-term care facilities, and workplace-related lacerations sustains routine utilization across age groups. Community pharmacies in urban and semi-urban areas maintain continuous inventory to meet daily demand.

Post-surgical care is expected to be the fastest-growing segment from 2026 to 2033, driven by rising ambulatory surgeries and structured discharge protocols. Healthcare systems prioritize early discharge with standardized recovery kits. Provider referrals influence patient adherence to sterile dressing usage. The expansion of minimally invasive procedures increases outpatient recovery volumes, supporting scalable consumption growth. Day-care cataract surgeries, laparoscopic cholecystectomies, cosmetic dermatology procedures, and orthopedic arthroscopies generate a consistent need for post-operative dressings outside inpatient settings. Discharge packets supplied by hospitals often include pre-counted sterile pads to ensure continuity of care during the first recovery week. Telehealth follow-up consultations encourage routine dressing replacement and reinforce compliance.

Regional Insights

North America Gauze Pad Market Trends

North America is expected to lead with an estimated 40% of the gauze pad market share in 2026, supported by high procedural intensity across acute and ambulatory care networks. The United States accounts for the majority of regional consumption due to elevated volumes of inpatient admissions, outpatient surgeries, and chronic wound management cases requiring standardized dressing protocols. Federal infection prevention guidelines and accreditation requirements reinforce routine use of sterile, individually packaged dressings in operating rooms and recovery units. Group Purchasing Organizations negotiate large-scale procurement contracts that centralize sourcing, stabilize pricing structures, and ensure uninterrupted supply across integrated delivery networks. Advanced reimbursement frameworks under Medicare and private insurers sustain predictable utilization patterns for post-operative and chronic wound care supplies.

Market dominance is further strengthened by established manufacturing capacity and vertically integrated distribution systems that reduce logistical disruptions and lead times. Large medical supply distributors operate automated warehousing platforms that replenish hospital inventories through data-driven demand forecasting models. Strong regulatory oversight by the U.S. Food and Drug Administration (FDA) promotes adherence to validated sterilization and packaging standards, increasing institutional preference for certified suppliers. Growth in outpatient surgery centers and home healthcare services expands consumption beyond inpatient settings, reinforcing steady baseline demand. Expansion of value-based care models incentivizes providers to adopt standardized wound management kits designed to minimize complications and readmissions.

Europe Gauze Pad Market Trends

Europe represents a mature yet strategically resilient landscape for gauze pad consumption, supported by universal healthcare coverage models and standardized clinical pathways across public hospital systems. High surgical intervention rates in Germany, France, Italy, and Spain sustain structured demand for sterile wound dressings in both inpatient and ambulatory settings. Strong regulatory alignment under European Union (EU) Medical Device Regulation (MDR) frameworks enforces rigorous quality and traceability standards, encouraging procurement from certified manufacturers with validated sterilization processes. Aging population demographics and elevated prevalence of chronic wounds such as venous leg ulcers and pressure injuries generate consistent long-term dressing utilization. Public reimbursement structures incentivize evidence-based wound management protocols, reducing variability in clinical practice.

Market stability is reinforced by well-developed pharmaceutical wholesale networks and cross-border medical supply distribution channels. Sustainability priorities influence purchasing decisions, driving demand for biodegradable cotton materials and reduced-plastic packaging formats in line with environmental compliance targets. Hospital tenders emphasize product performance metrics including absorbency standards, sterility assurance levels, and packaging integrity under transport conditions. Growth in home nursing services across Nordic and Western European countries supports repeat purchasing patterns for chronic wound patients receiving community-based care. Digital prescription systems and integrated electronic health records improve supply planning accuracy within hospital procurement departments.

Asia Pacific Gauze Pad Market Trends

Asia Pacific is forecasted to be the fastest-growing market for gauze pad between 2026 and 2033, stimulated by accelerated healthcare capacity expansion and rising procedural volumes across secondary and tertiary care institutions. Rapid construction of multi-specialty hospitals, expansion of government-funded insurance schemes, and higher penetration of private healthcare providers are increasing access to surgical and wound management services. Large patient pools affected by diabetes, traumatic injuries, and road accidents are generating sustained demand for cost-efficient dressing materials. Public health investments in rural health missions and district hospitals are formalizing procurement systems that previously relied on fragmented sourcing. Domestic manufacturing clusters in China and India support high-volume, low-cost production, enabling competitive pricing without compromising supply continuity.

Growth momentum is further driven by distribution modernization and digital retail penetration. Pharmacy chains and e-commerce medical supply platforms are expanding reach beyond metropolitan areas, enabling home caregivers to access standardized wound care materials. Regulatory harmonization initiatives and quality certification requirements are improving product consistency, increasing trust among institutional buyers. Medical tourism inflows for elective and reconstructive procedures are adding incremental demand across private hospitals. Infrastructure upgrades in community health centers are encouraging structured wound management practices rather than informal treatment methods.

Competitive Landscape

The global gauze pad market structure remains moderately fragmented, characterized by participation from multinational medical supply corporations alongside regional textile-based manufacturers with localized distribution capabilities. Despite fragmentation, leading participants including 3M, Cardinal Health, Medtronic, Smith+Nephew, PAUL HARTMANN, B. Braun, and Kenvue Brands collectively account for a substantial revenue concentration. Competitive strength among these organizations is reinforced through vertically integrated manufacturing, validated sterilization infrastructure, and established global distribution partnerships. Large-scale procurement contracts with hospital networks and group purchasing organizations enable volume stability and pricing leverage. Operational scale allows investment in automation, quality assurance systems, and advanced packaging technologies that meet stringent clinical standards across developed healthcare systems.

Strategic positioning centers on regulatory compliance, supply continuity, and portfolio breadth rather than product differentiation alone. Leading corporations leverage diversified medical consumables portfolios to bundle wound care products with complementary surgical and post-operative supplies, strengthening institutional relationships. Compliance with international medical device regulations and adherence to sterilization validation protocols create entry barriers for smaller producers lacking certification infrastructure. Digital supply chain management systems, real-time inventory tracking, and predictive demand planning enhance fulfillment reliability during peak procedural cycles. Brand credibility within hospital procurement departments influences tender outcomes, especially where infection control benchmarks and audit transparency are critical evaluation criteria.

Key Industry Developments

- In January 2026, Beiersdorf AG expanded its wound care portfolio with the introduction of Second Skin Protection invisible spray and liquid plaster formats under the Hansaplast, Elastoplast, and CURITAS brands to address consumer avoidance of conventional adhesive dressings and strengthen healthcare growth.

- In December 2025, MPM Medical introduced new HCPCS-compliant collagen at-home wound care kits and a proprietary wound care portal designed to expand patient access, improve compliance with post-operative care protocols, and simplify insurance verification and home delivery processes.

Companies Covered in Gauze Pad Market

- 3M

- Cardinal Health.

- Medtronic

- Smith+Nephew.

- PAUL HARTMANN AG

- B. Braun SE

- Kenvue Brands LLC

- Dynarex Corporation.

- Texpol

- Winner Medical Co., Ltd.

Frequently Asked Questions

The global gauze pad market is projected to reach US$ 4.1 billion in 2026.

Rapid rise in surgical volumes, increasing prevalence of chronic wounds, expanding home healthcare adoption, and stringent infection control standards are driving the market.

The market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Integration of advanced wound management features, expansion into emerging healthcare systems, growth in home-based care channels, and development of eco-friendly dressing materials represent key market opportunities.

Some of the key market players include 3M, Cardinal Health, Medtronic, Smith+Nephew, PAUL HARTMANN AG, and B. Braun SE.