- Automation & Robotics

- FTIR Gas Analyzer Market

FTIR Gas Analyzer Market Size, Share, and Growth Forecast, 2026 - 2033

FTIR Gas Analyzer Market by Analyzer Type (Portable, Fixed), Concentration Level (High Concentration Range, Low Concentration Level), End-User (Oil & Gas, Chemical, Automotive, Pharmaceutical, Food & Beverage, Others), and Regional Analysis for 2026 - 2033

FTIR Gas Analyzer Market Share and Trends Analysis

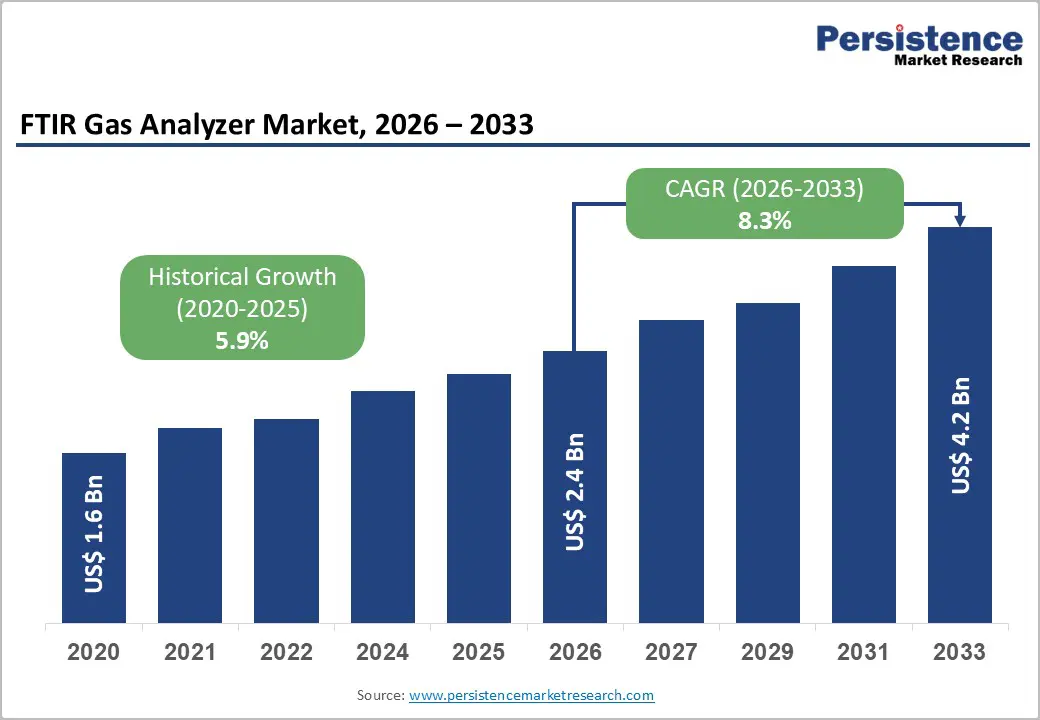

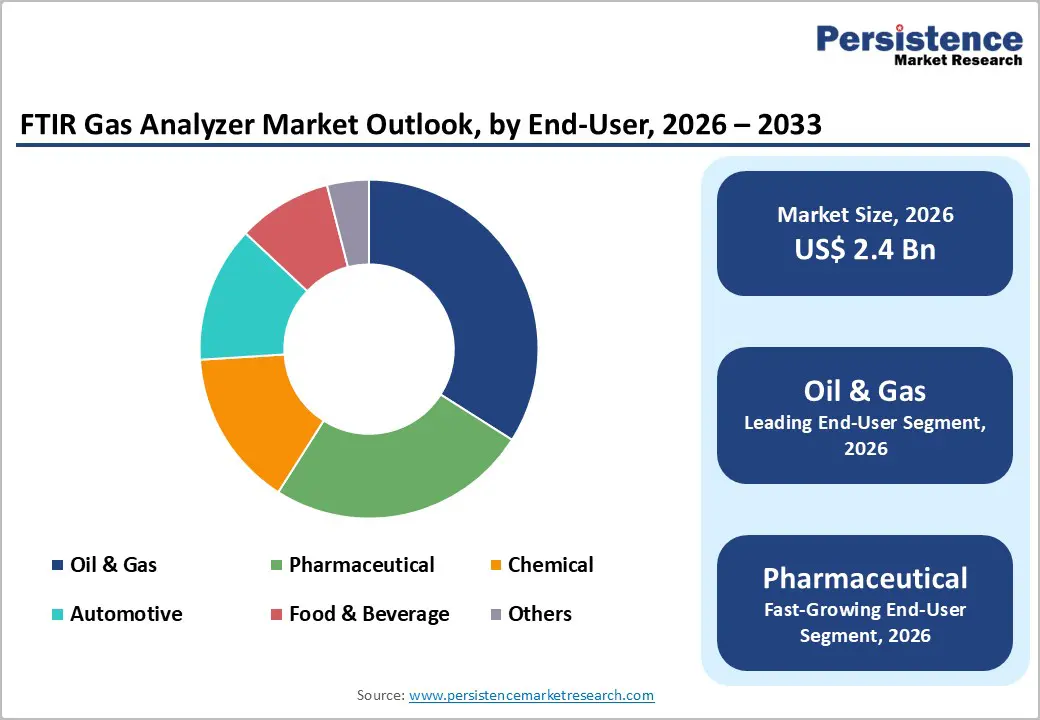

The global FTIR gas analyzer market size is likely to be valued at US$ 2.4 billion in 2026, and is projected to reach US$ 4.2 billion by 2033, growing at a CAGR of 8.3% during the forecast period 2026−2033. Sustained regulatory enforcement on industrial emissions, rising environmental monitoring requirements, and integration of advanced spectroscopy technologies are expected to drive consistent market expansion. Governments are strengthening air quality surveillance frameworks to address pollution driven by urbanization and to meet climate commitments, creating measurable demand for high-precision multi-gas detection systems. Industrial sectors are adopting continuous emissions monitoring systems to ensure compliance with environmental standards, directly increasing the procurement of Fourier Transform Infrared (FTIR) analyzers for real-time analysis.

Healthcare infrastructure expansion and rising awareness of respiratory exposure risks are supporting broader clinical and laboratory gas analytics applications. Technological convergence with automation platforms, industrial Internet of Things (IIoT), and cloud-based diagnostics enhances operational efficiency and lifecycle traceability, encouraging the replacement of legacy gas detection technologies.

Key Industry Highlights

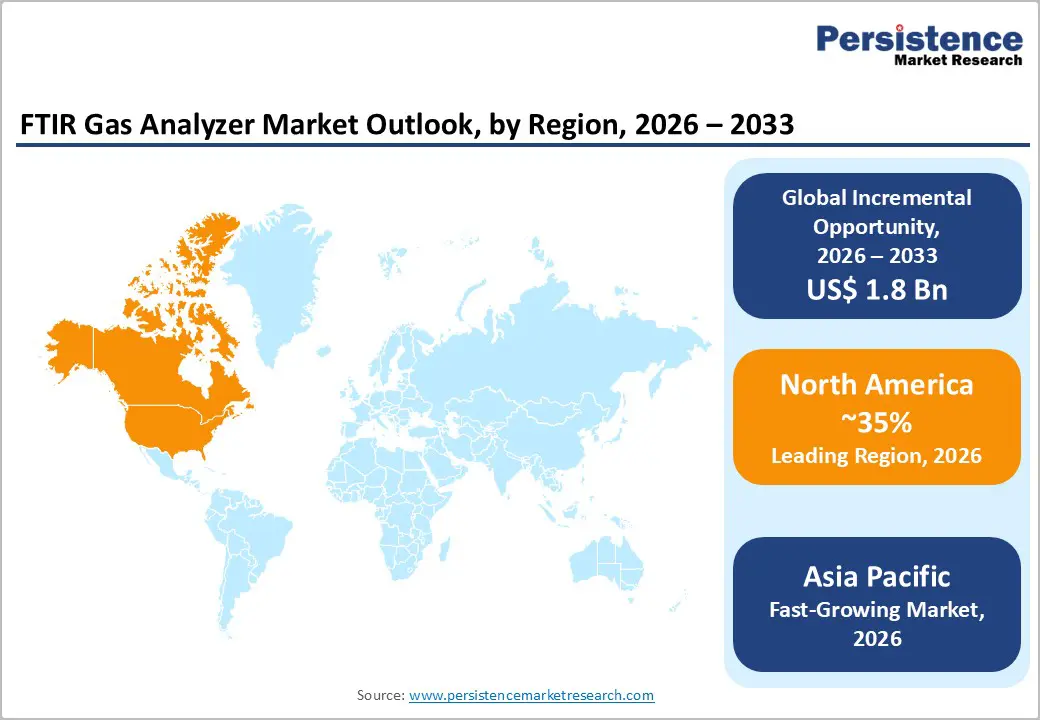

- Dominant Region: North America is projected to hold about 35% market share in 2026, driven by strict emissions regulations and real-time multi-gas monitoring.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by industrial growth and real-time gas monitoring.

- Leading End-User: The oil & gas segment is projected to hold roughly 34% revenue share in 2026, led by emissions monitoring, process optimization, and leak detection needs.

- Fastest-growing End-User: The pharmaceutical segment is expected to be the fastest-growing between 2026 and 2033, driven by quality standards, sterile environments, and compact real-time gas analyzers.

| Key Insights | Details |

|---|---|

|

FTIR Gas Analyzer Market Size (2026E) |

US$ 2.4 Bn |

|

Market Value Forecast (2033F) |

US$ 4.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Stringent Environmental Compliance Frameworks and Emissions Monitoring Mandates

Government emissions reporting requirements and compliance regimes underpin regulatory efforts to measure, disclose, and control pollutant releases across industry sectors. In the United States, the Greenhouse Gas Reporting Program requires approximately 8,000 large facilities to submit detailed annual emissions data for key greenhouse gases, including carbon dioxide and methane, with the data publicly published to support transparency in environmental performance. Regulatory frameworks such as Section 40?CFR Part 75 requires continuous monitoring and reporting of emissions data for power plants under the Clean Air Act, ensuring that pollutants such as CO2, NOX, and SO2 are measured and evaluated at regular intervals.

Regulatory agencies rely on validated emissions data to enforce standards, assess environmental risk, and inform policy formulation. Monitoring obligations under Titl-V permits and compliance assurance monitoring rules require systematic collection and reporting of emissions to demonstrate adherence to emission limits and permit terms. Noncompliance can trigger administrative actions, fines, or operational restrictions, creating a strong incentive for facilities to deploy reliable measurement technologies. The extensive scope of reporting programs and detailed monitoring specifications requires that facilities implement continuous or periodic measurement systems capable of accurately quantifying gas concentrations.

Industrial Digitization and Process Optimization Initiatives

Industrial digitization efforts reform traditional manufacturing and energy operations into interconnected, data-driven ecosystems that deliver measurable efficiency gains and tighter process control. Networks of smart sensors, cloud data platforms, and advanced analytics enable operators to monitor variables such as emissions, combustion ratios, and production throughput in real time, reducing production variability and unplanned stoppages through predictive insights. These capabilities align directly with the United States government’s IoT Advisory Board findings that IoT integration drives transparency, operational performance, and real-time analytics across industrial domains, forming a data backbone for automated decision-making and process refinement.

Process optimization initiatives rooted in digitization address core industry priorities for efficiency and quality enhancement by aligning operational data with automated control systems. The IIoT framework fosters seamless data flow between field instrumentation and enterprise analytics, accelerating detection of inefficiencies and enabling dynamic adjustments that yield throughput improvements. Integration of digital technologies also supports compliance reporting and safety monitoring by delivering high-fidelity datasets essential for regulatory audits and environmental benchmarking. Government frameworks and standardization efforts underscore the strategic value of IoT-enabled systems in improving competitiveness, safety, and sustainability, reinforcing the rationale for investments in digital process technologies that enhance performance visibility and operational agility.

Technical Complexity and Skilled Workforce Requirements

FTIR instruments require precise optical alignment, spectral calibration and advanced data interpretation, demanding a depth of analytical and instrumental expertise not usually found among general technical staff. Complexities arise from the need to resolve overlapping absorption bands and compensate for environmental interferences such as humidity and temperature during measurements, which can compromise accuracy if not properly managed. Operators must understand the physics of interferometry and Fourier transform mathematics along with chemistry fundamentals to extract valid readings from raw spectral data, a skill set that is typically acquired through specialized training and hands-on experience rather than general technical education.

Training pathways for analytical techniques such as FTIR require significant investment in education or company-sponsored upskilling, particularly since undergraduate or general technical curricula often do not cover complex spectroscopic methods in depth. This creates a bottleneck, forcing organizations to either recruit highly trained personnel at a premium cost or invest in training programs with extended lead times to build internal capability. The gap between demand for skilled analytical professionals and supply limits rapid deployment of advanced analytical systems, and drives operational risk for organizations that lack sufficient in-house proficiency to manage calibration, maintenance and regulatory reporting linked to emissions or quality monitoring.

Supply Chain Volatility in Precision Optical Components

The restricted availability and logistical fragility of high-precision optical components stem from deep structural dependencies within the upstream materials ecosystem. Polished lenses, beam splitters, reflective coatings and other sub-micron optical assemblies require extremely pure substrates such as fused silica and rare earth oxide coatings sourced from a few global suppliers with concentrated production footprints. These materials and intermediate products are often categorized as critical minerals by governments due to their essential role in advanced manufacturing and national security applications, and official U.S. lists highlight the risk of supply chain disruptions arising from over-reliance on limited foreign sources of processed critical minerals and their derivative products, such as advanced optics.

Concentration of supply also elevates exposure to localized shocks, whether from regulatory changes, natural disasters or diplomatic disputes affecting raw material exporters. Official government commentary on processed critical minerals underscores the vulnerability of supply chains for derivative manufacturing sectors reliant on those inputs. In this environment, procurement teams must allocate disproportionate resources to risk mitigation, such as dual sourcing and stockpiling, which drives up operating expenses and complicates production planning. Late deliveries of optical substrates ripple through assembly schedules, delaying product launch timelines and constraining revenue realization, making these supply chain challenges a material restraint on growth-oriented capital expenditure cycles.

Integration with IoT, Cloud & Digital Platforms

Cloud connectivity and IoT devices radically improve the operational value of advanced sensor systems by enabling continuous, real-time data streams that can be accessed, analyzed and acted on remotely. According to the U.S. National Institute of Standards and Technology (NIST), the Internet of Things Advisory Board noted that IoT implementations generate large volumes of real-time environmental data that can be processed and turned into actionable insights, supporting near-instant decision-making in areas such as compliance reporting, process controls, and hazard detection. The ability to feed live measurements into cloud platforms and analytics engines reduces reliance on periodic manual checks, eliminates delays in issue identification, and enhances transparency across organizational functions.

Enterprise-level communications infrastructure further amplifies the strategic advantage of connected monitoring. Government advisory perspectives emphasize that integrated sensing networks reduce operational risk by facilitating remote oversight and predictive insights across distributed facilities, enabling earlier intervention and maintenance planning before critical failures occur. Automated alerting and centralized dashboards allow environmental and safety teams to prioritize responses according to risk levels and regulatory thresholds, improving safety outcomes and lowering the costs

Technological Convergence with Portable and Remote Diagnostics Platforms

Integration of advanced analytical systems with portable, remote diagnostics platforms offers transformative value given the intensifying regulatory and operational demands for real-time emissions and air quality data. Field teams and environmental agencies are under increasing pressure from frameworks such as the U.S. Environmental Protection Agency (EPA)’s ambient monitoring and emissions reporting mandates to deliver accurate, timely measurements that inform compliance reporting and public health assessments. For example, as of 2025 the EPA’s Emissions & Generation Resource Integrated Database (eGRID) provides comprehensive emissions data for nearly all U.S. power plants, linking environmental performance with generation statistics and supporting state and federal monitoring programs.

Convergence with connected mobile diagnostics and remote data transmission enables operators to move beyond static, laboratory-bound measurement workflows and into scalable field-deployed monitoring frameworks. Deployment of IoT-enabled sensors and cloud-based data integration enables continuous capture and harmonization of volatile gas data streams from multiple locations, reducing the lag between detection and actionable intelligence and minimizing field labor costs compared to periodic manual sampling. Remote diagnostics also supports networked monitoring architectures that align with EPA’s emphasis on optimizing air quality surveillance networks through periodic assessments and adoption of new technologies.

Category-wise Analysis

Analyzer Type Insights

Fixed analyzers is poised to lead with a forecasted 62% of the FTIR gas analyzer market revenue share in 2026, owing to regulatory mandates for continuous emissions monitoring and integration within industrial exhaust systems. Industrial facilities require permanent installation for stack monitoring, process control, and environmental reporting. Regulatory compliance audits prioritize continuous measurement over intermittent sampling. Infrastructure investments in refineries, power plants, and chemical manufacturing units reinforce procurement of fixed systems. Integration with centralized control rooms improves traceability, data logging, and audit readiness. Provider preference for stable, long-term monitoring solutions strengthens the dominance of fixed installations.

Portable analyzers are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by demand for on-site diagnostics, environmental inspections, and emergency leak detection. Field engineers prioritize mobility and rapid deployment across distributed assets. Industrial safety programs integrate portable spectroscopy tools within maintenance workflows. Miniaturization innovations improve battery efficiency and spectral resolution. Accessibility across remote infrastructure and inspection-based service models accelerates adoption in energy transition projects and infrastructure audits.

End-User Insights

The oil & gas segment is expected to hold a dominant position, accounting for an anticipated 34% of the FTIR gas analyzer market share in 2026, driven by upstream and downstream emissions monitoring requirements, refinery process optimization, and leak detection programs. Hydrocarbon processing generates complex gas mixtures requiring multi-component analysis, creating a demand for precise and reliable measurement technologies. Providers within integrated energy companies increasingly standardize spectroscopy-based monitoring solutions to ensure consistency across operations. Digitalization initiatives, including real-time data analytics and remote monitoring platforms, enhance operational transparency, support predictive maintenance, and strengthen compliance assurance with environmental and safety regulations, improving overall process efficiency.

The pharmaceutical segment is forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by stringent quality control standards, sterile production environments, and gas purity verification requirements. Technology-enabled laboratory automation enables laboratories to adopt high-resolution spectroscopy for real-time monitoring of critical parameters. The accessibility of compact analyzers within research and development laboratories facilitates routine testing and method development. Multi-gas simultaneous detection improves operational productivity and reduces analysis time, enabling cost-effective processes. Integration with digital record-keeping and quality management systems further supports regulatory compliance and process optimization in pharmaceutical manufacturing.

Regional Insights

North America FTIR Gas Analyzer Market Trends

North America is expected to dominate with an estimated 35% of the FTIR gas analyzer market value in 2026, reflecting robust adoption across industrial, environmental, and research applications. Dominance is supported by stringent regulatory frameworks requiring continuous monitoring and reporting of emissions across the energy, petrochemical, and chemical sectors. Industrial operators increasingly rely on multi-component, real-time gas analysis to optimize refinery processes, prevent leaks, and maintain compliance with federal and state environmental standards. Integration of spectroscopy-based analyzers with digital monitoring systems enables predictive maintenance and operational efficiency improvements, allowing stakeholders to reduce downtime and mitigate regulatory risk while supporting high-accuracy emission and safety reporting.

High technological infrastructure and advanced automation capabilities reinforce market leadership. Laboratory and research facilities use compact, high-resolution analyzers for quality control and safety verification, leading to widespread adoption in industrial workflows. Government initiatives incentivizing environmental monitoring and low-emission operations encourage the deployment of portable and remote measurement platforms, enhancing coverage beyond fixed monitoring stations. Service ecosystems, including calibration, remote diagnostics, and technical support, improve reliability and reduce operational cost, making adoption more attractive for large-scale operators. Strategic collaborations between technology providers and industry participants drive continuous improvement in sensor performance, data integration, and analytical accuracy.

Europe FTIR Gas Analyzer Market Trends

Europe maintains a mature regulatory framework guided by European Union (EU) environmental directives and carbon reduction targets. Industrial clusters in Germany, France, and the Netherlands drive the adoption of FTIR gas analyzers across chemical, energy, and pharmaceutical operations, where multi-component gas detection and real-time emissions monitoring are critical. Integration with digital monitoring platforms supports predictive maintenance, operational transparency, and compliance reporting. Research and development initiatives focus on enhancing instrument accuracy, miniaturization, and portability, enabling laboratories and production facilities to perform rapid quality verification and emissions assessments. Public and private programs promoting sustainable industrial practices further encourage the deployment of advanced spectroscopy-based solutions across diverse manufacturing processes.

Operational efficiency, safety assurance, and regulatory compliance underpin market adoption. IoT-enabled platforms and cloud-connected analyzers provide centralized oversight across distributed facilities, reducing manual sampling requirements and improving data integrity. Laboratories leverage compact, high-resolution instruments to streamline routine gas verification, improving productivity and minimizing downtime. Strategic partnerships between technology providers and industrial operators support the continuous improvement of analytical capabilities, knowledge transfer, and workforce training. Expanding infrastructure for low-emission production and sustainability initiatives reinforces demand for high-accuracy gas analysis systems, ensuring consistent adoption and stable growth.

Asia Pacific FTIR Gas Analyzer Market Trends

Asia Pacific is forecasted to be the fastest-growing market for the FTIR gas analyzer market between 2026 and 2033, stimulated by rapid industrial expansion, rising demand for environmental monitoring, and increasing adoption of advanced process control technologies. Growth is driven by large-scale chemical, pharmaceutical, and energy production facilities requiring precise, real-time measurement of multi-component gas streams. Regulatory authorities are implementing stricter emission standards and incentivizing the adoption of continuous monitoring technologies to mitigate industrial air pollution. Deployment of high-resolution, portable analyzers in field operations allows manufacturers to meet compliance targets efficiently while maintaining operational performance. Expansion of energy infrastructure, including renewable sources, further fuels demand for real-time gas analysis to optimize process efficiency and ensure compliance with safety standards across distributed production networks.

Integration of spectroscopy-based analyzers with digital platforms and IoT-enabled monitoring systems is accelerating adoption. Remote diagnostics and cloud-based data aggregation support centralized oversight of geographically dispersed operations, reducing dependence on manual sampling and on-site analysis. Compact, high-accuracy instruments allow laboratories and production sites to perform routine verification and quality assurance with minimal downtime, improving productivity and cost efficiency. Strategic investments in automation, training, and service networks enable faster scaling and technology transfer across manufacturing and research facilities.

Competitive Landscape

The global FTIR gas analyzer market structure exhibits moderate consolidation, with a mix of leading analytical instrumentation companies and specialized spectroscopy providers shaping competitive dynamics. Market positioning focuses on technological differentiation, where product innovation, detection accuracy, and multi-component analysis capabilities distinguish providers. Key players such as Alfa Romeo Automobiles S.p.A., Audi AG, ABT Sportsline GmbH, BREMBO S.p.A., BRABUS GmbH, and ALPINA Burkard Bovensiepen GmbH + Co. KG leverage their global operational networks and engineering expertise to integrate advanced gas analysis solutions into production workflows, emission monitoring programs, and research applications, maintaining competitive advantage in a moderately consolidated landscape.

Barriers to entry remain significant due to precision engineering requirements and extensive regulatory validation processes. Designing instruments capable of high-resolution, multi-gas detection necessitates advanced sensor technology, robust optics, and rigorous software integration. New entrants must navigate certification requirements for industrial and laboratory applications, which include safety compliance, emission reporting standards, and environmental monitoring approvals. Established players mitigate these barriers through continuous R&D investment, proprietary technologies, and partnerships with industrial clients for tailored implementations.

Key Industry Developments

- In February 2026, ABB introduced its first fully integrated carbon capture measurement solution combining advanced gas analyzers into a turnkey package to deliver real?time CO? impurity monitoring and support industrial decarbonization efforts across hard?to?abate sectors.

- In June 2025, researchers from Wuhan University demonstrated an FTIR method capable of rapidly analyzing seven light alkanes in wellhead gases during drilling operations. The technique delivers results in about 15 seconds, enabling real-time gas logging at the wellhead and improving detection of thin hydrocarbon layers compared with slower methods such as gas chromatography.

Companies Covered in FTIR Gas Analyzer Market

- Alfa Romeo Automobiles S.p.A.

- Audi AG

- ABT Sportsline GmbH

- BREMBO S.p.A.

- BRABUS GmbH

- ALPINA Burkard Bovensiepen GmbH + Co. KG

- TVR Automotive Limited

- Volkswagen of America, Inc.

- Carroll Shelby International, Inc.

- MAT Foundry Group Ltd.

- Surface Transforms PLC

Frequently Asked Questions

The global FTIR gas analyzer market is projected to reach US$ 2.4 billion in 2026.

Rising industrial emissions monitoring requirements, stringent environmental regulations, and demand for real-time multi-gas analysis are driving the market.

The market is poised to witness a CAGR of 8.3% from 2026 to 2033.

Integration with portable, IoT-enabled, and remote diagnostics platforms for real-time monitoring presents key market opportunities.

Some of the key market players include Alfa Romeo Automobiles S.p.A., Audi AG, ABT Sportsline GmbH, BREMBO S.p.A., and BRABUS GmbH.