- Industrial Goods & Service

- Foundation Repair Services Market

Foundation Repair Services Market Size, Share, and Growth Forecast, 2026 - 2033

Foundation Repair Services Market by Service type (Settlement Repair, Wall Repair, Chimney Repair, Floor Slab Repair, Others), End-user (Residential, Commercial), and Regional Analysis for 2026 - 2033

Foundation Repair Services Market Size and Trends Analysis

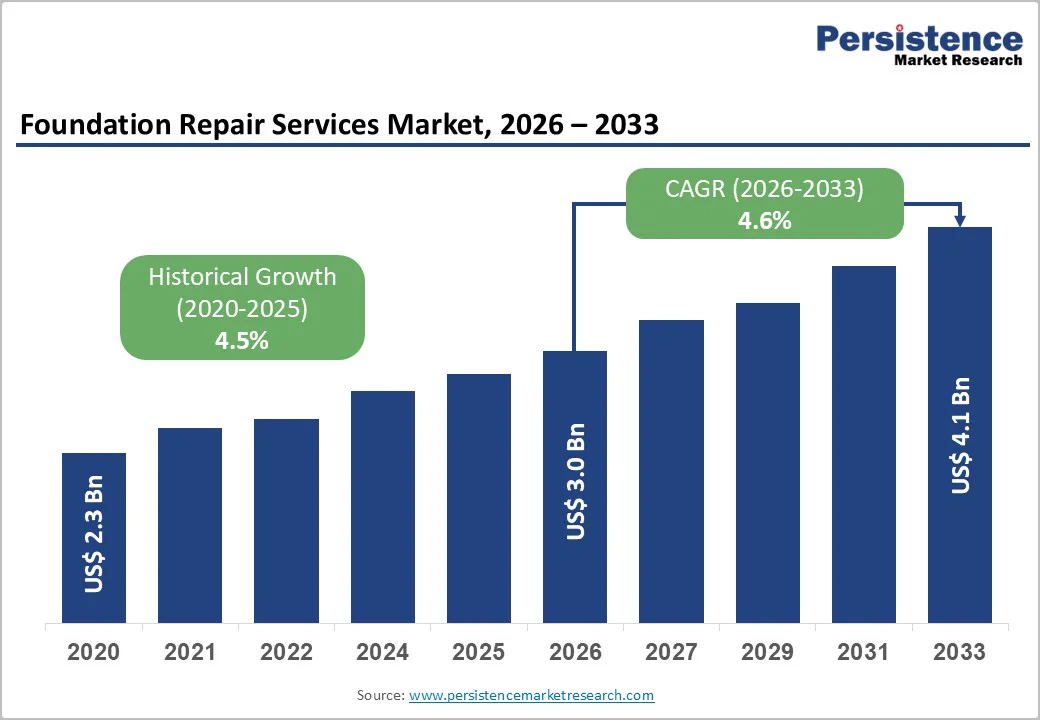

The global foundation repair services market size is likely to be valued at US$3.0 billion in 2026 and is expected to reach US$4.1 billion by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 to 2033, driven by the continuous infrastructure aging, soil degradation, and greater awareness of structural risk management.

Climate-driven soil changes, such as erosion, clay swelling, flooding, and drought cycles, can greatly accelerate foundation settlement and structural movement. Rapid urbanization in emerging economies, increasing rates of homeownership, and a rise in redevelopment and renovation projects are boosting demand in both residential and commercial sectors.

Key Industry Highlights:

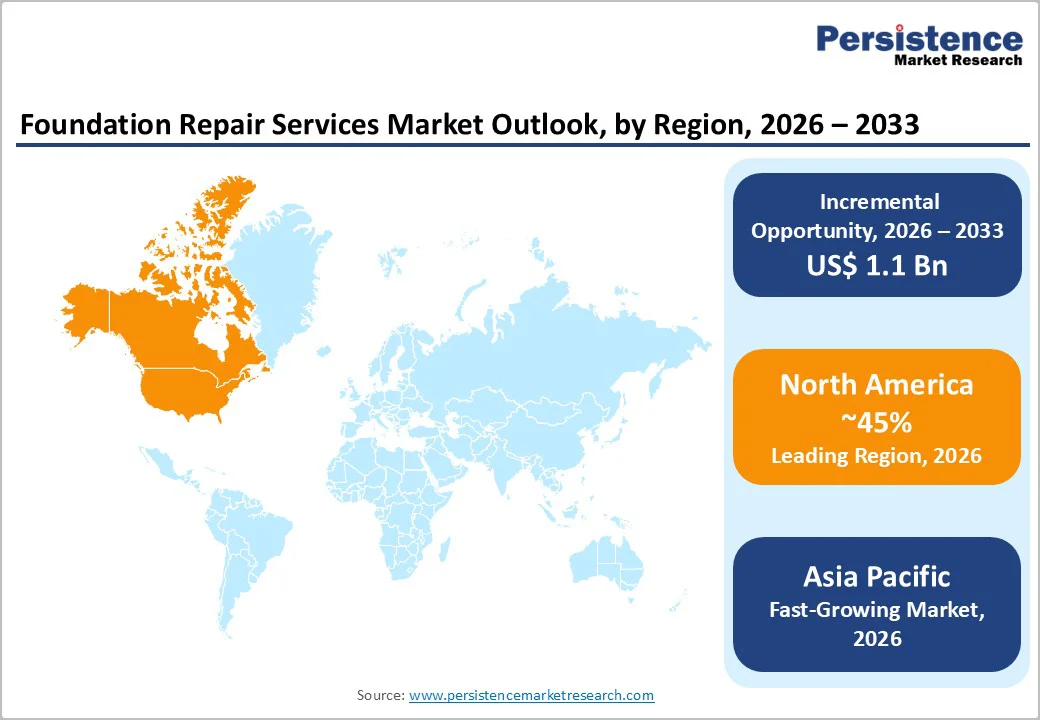

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by expansive soil-related repairs in the U.S., faster growth in Canada, climate-induced soil shifts, seismic-zone compliance requirements, and a consolidated competitive landscape.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rapid urbanization, widespread soil instability across high-rise developments, evolving regulatory enforcement, and competitive local contractor ecosystems.

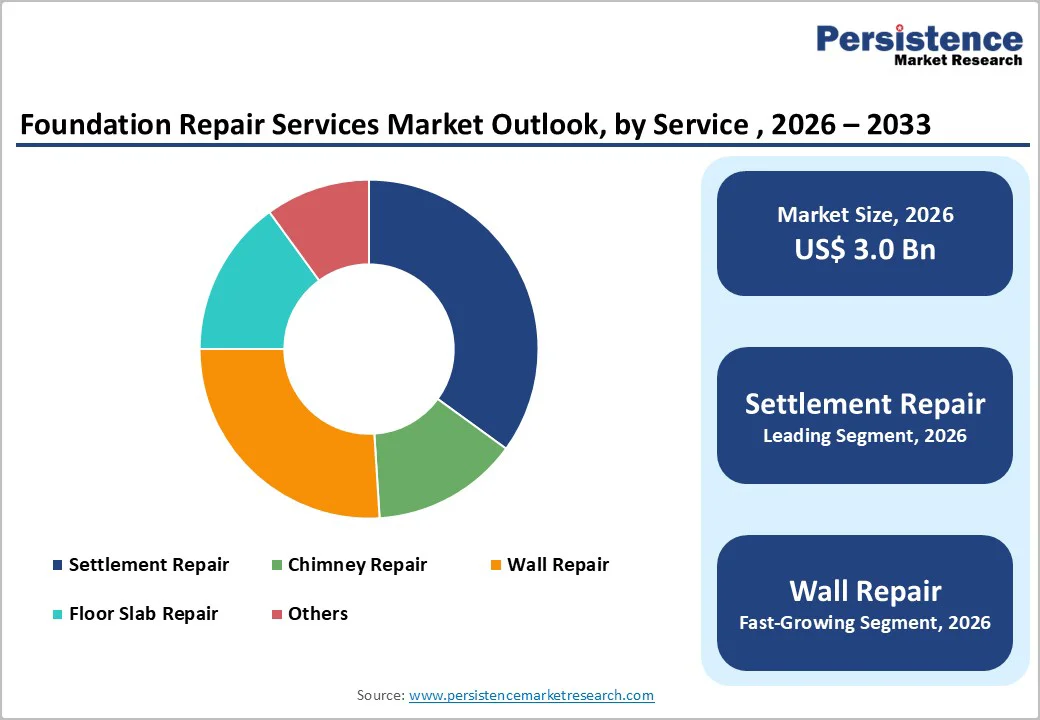

- Leading Service Type: The settlement repair segment is projected to represent the leading product type in 2026, accounting for 36% of the market share, driven by widespread ground-movement issues across aging residential and commercial structures.

- Leading End-user: The residential segment is anticipated to lead, accounting for over 63% of the revenue share in 2026, supported by rising homeowner investments in structural safety, preventive inspections, and property value protection.

| Key Insights | Details |

|---|---|

|

Foundation Repair Services Market Size (2026E) |

US$3.0 Bn |

|

Market Value Forecast (2033F) |

US$4.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Aging Infrastructure and Urbanization-Driven Foundation Stress

A large proportion of global residential and commercial buildings, particularly those constructed before the 1980s, are now experiencing structural fatigue, soil settlement, and material degradation. Over time, foundations are affected by wear, shifting subsoils, moisture intrusion, and inadequate original engineering standards that no longer meet modern load requirements. In North America and Europe, foundation cracking, uneven settling, and wall displacement have become increasingly common, prompting higher demand for underpinning, helical piers, wall stabilization, and slab repair. This structural aging is further intensified by extreme weather patterns such as freeze-thaw cycles, prolonged droughts, and flooding, all of which accelerate soil movement around older foundations.

Rapid city development in Asia Pacific, Latin America, and parts of Africa increases pressure on land with variable soil quality, often leading to foundation stresses in new and existing structures. High-rise construction on reclaimed land, expansive clay zones, and densely packed urban corridors heighten the likelihood of settlement-related issues. Rapid urbanization is also accelerating infrastructure upgrades, including roads, utilities, and transit systems, which disturb the surrounding soil and can impact the stability of nearby foundations. The expansion of metropolitan areas is driving large-scale renovation and redevelopment projects, where foundation inspections and remediation are critical to maintaining structural integrity and safety.

High Repair Costs and Budgetary Constraints

Foundation issues often require specialized labor, engineering assessments, and advanced repair technologies such as helical piers, polyurethane injections, or structural wall reinforcements. These procedures can be costly due to the complexity of diagnosing subsurface conditions and the precision needed to prevent further structural damage. In many regions, repair expenses escalate owing to fluctuating material costs, stringent permitting requirements, and the need for certified technicians, making it difficult for homeowners and small businesses to undertake timely repairs.

Budgetary constraints also affect demand, particularly in developing economies and lower-income urban areas, where discretionary spending on structural maintenance is limited. Even in mature markets, insurance coverage for foundation repairs is often restricted, placing a heavy financial burden on property owners. Local governments, commercial facility managers, and households frequently prioritize visible renovations over structural corrections, contributing to deferred maintenance. Economic downturns, rising interest rates, and inflation reduce capital allocation for non-emergency foundation work.

Technological Innovations in Diagnostics and Materials

Modern tools dramatically improve accuracy, efficiency, and early detection of structural issues. Advanced systems such as ground-penetrating radar (GPR), LiDAR scanning, infrared thermography, moisture-mapping sensors, and AI-enabled crack monitoring allow technicians to identify subsurface voids, soil shifts, and structural weaknesses with far greater precision than traditional visual inspections. These tools shorten assessment timelines, reduce exploratory demolition, and enhance customer trust through data-backed evaluations.

Material advancements also open strong growth pathways, with next-generation repair solutions offering greater strength, speed, and sustainability. High-performance composites, carbon-fiber wall reinforcements, self-healing concrete additives, and eco-friendly polyurethane foams enable more durable repairs with reduced installation time. Helical piers engineered with corrosion-resistant alloys and advanced load-distribution designs enhance performance in challenging soils, supporting long-term stability for both residential and commercial buildings. The construction sector is increasingly embracing sustainable materials and resilient infrastructure, enabling service providers to deliver advanced, technology-driven repair solutions that enhance reliability while reducing long-term maintenance costs.

Category-wise Analysis

Service Type Insights

The settlement repairs segment is expected to lead the foundation repair services market, accounting for approximately 36% of the total revenue in 2026, driven by widespread soil movement and aging building stock worldwide. Older residential and commercial structures, particularly those built before stricter code reforms of the 1980s, are more vulnerable to differential settlement caused by expansive clays, drought cycles, and inadequate historical footing designs. This has strengthened the demand for underpinning, helical piers, and pier-and-beam stabilization systems that restore load distribution and structural integrity.

The wall repair segment is likely to represent the fastest-growing service type in 2026, driven by rising awareness of structural performance issues associated with foundation walls, bowing, and cracking across residential and commercial buildings. Recent reports highlight wall repair services gaining ground as contractors increasingly use advanced reinforcement techniques, including carbon fiber and steel anchoring systems, to address moisture-induced wall failures and lateral pressure challenges common in urban and aging structures. For example, several North American foundation service providers are emphasizing wall repair capabilities to meet heightened demand in markets with older homes and high moisture exposure, signaling strong growth momentum for this segment.

End-user Insights

Residential is projected to lead the market, capturing around 63% of the total revenue share in 2026, driven by demand from homeowners investing in structural safety, longevity, and property value preservation. The residential segment represents the largest share of foundation repair projects, as homeowners routinely rely on professional services to address problems such as uneven floors, wall cracking, and moisture infiltration. This trend is exemplified by Olshan Foundation Repair, one of the industry’s longest-established companies, which predominantly serves the residential market through a comprehensive portfolio of slab, pier, and wall stabilization solutions tailored to homeowner needs.

The commercial end-use segment is expected to be the fastest-growing in 2026, supported by rising investments in office complexes, retail facilities, industrial sites, and infrastructure assets that require reliable foundation maintenance to prevent operational downtime. Due to their larger scale, heavier load requirements, and structural complexity, commercial projects often demand advanced repair technologies, resulting in higher service adoption compared to traditional residential applications. Companies such as Ram Jack Systems and The Dwyer Company illustrate this trend by delivering customized solutions for large-scale commercial and mixed-use developments, demonstrating how leading providers are expanding capabilities while continuing to serve the dominant residential market.

Regional Insights

North America Foundation Repair Services Market Trends

North America is expected to lead the market, capturing approximately 45% share in 2026, supported by an aging building stock, varied soil profiles, and robust regulatory frameworks that encourage routine structural inspections and corrective maintenance. The region represents a significant portion of global demand, with the U.S. accounting for the largest share due to its extensive residential and commercial real estate footprint and widespread soil challenges, including shrink–swell clays and freeze–thaw cycles that compromise foundation stability. This trend is reflected by companies such as Olshan Foundation Repair, which reports consistently strong service demand across states, including Texas, Oklahoma, and Colorado.

Emerging trends in North America revolve around technological adoption, preventive monitoring, and energy-efficient repair methods that reduce long-term costs for property owners. Companies are integrating digital inspections, advanced polymer injections, and structural sensors to diagnose foundation displacement more accurately. A strong example is Foundation Supportworks, which uses proprietary geotechnical software and helical foundation systems to optimize repair outcomes for residential and commercial buildings.

Europe Foundation Repair Services Market Trends

Europe is likely to be a significant market for foundation repair services in 2026, due to aging building stock, soil instability, and heritage preservation challenges, which drive demand for structural maintenance and stabilization solutions. Seasonal moisture variations and soil shrink-swell conditions in Western Europe increasingly expose foundations to stress, while historic masonry structures often need non-invasive underpinning and wall reinforcements. For example, Groundworks has integrated AI-enabled moisture mapping into its inspection process, enabling early detection of structural weaknesses.

Emerging trends in Europe include the adoption of advanced diagnostics and green repair materials, as service providers seek to differentiate offerings and comply with stringent environmental and construction standards. European contractors are increasingly integrating technologies such as ground-penetrating radar (GPR), 3D scanning, and moisture monitoring to improve the accuracy of foundation assessments, enabling more targeted interventions with minimal disruption to historic façades. For example, Germany’s foundation repair sector has reported higher uptake of carbon fiber wall reinforcement systems in older masonry structures.

Asia Pacific Foundation Repair Services Market Trends

The Asia Pacific region is expected to be the fastest-growing market, supported by rapid urbanization, intensive construction activity, and pronounced soil and seismic challenges across key economies. The region hosts a large and expanding base of residential and commercial structures that require ongoing stabilization services. China accounts for a substantial share of repair demand, as high-rise construction and land subsidence issues continue to drive service adoption. Japan and several Southeast Asian countries face frequent earthquakes and typhoons, increasing the need for advanced wall reinforcement, slab leveling, and underpinning solutions designed for highly dynamic soil conditions.

Key trends in the Asia Pacific region include the growing adoption of advanced diagnostic and reinforcement technologies, increased emphasis on preventive maintenance services, and collaborative partnerships between global and local contractors to expand service coverage. Service providers are increasingly leveraging digital inspection tools, soil mapping technologies, and advanced polymer injection techniques to enhance precision and reduce repair timelines, aligning with rising expectations from property owners and developers. For instance, contractors in major metropolitan areas are deploying AI-assisted assessment platforms and drone-based imaging to enable early detection of foundation issues, improving service efficiency in complex urban environments.

Competitive Landscape

The global foundation repair services market is moderately fragmented, comprising multinational firms, regional operators, and specialized local contractors that collectively shape competitive dynamics. Leading players, including Supportworks, Inc., The Dwyer Company, Basic Foundation Repair, Connecticut Basement Systems, and Groundworks, focus on expanding service portfolios, geographic coverage, and technological capabilities to address residential and commercial demand, especially in areas with aging infrastructure and challenging soil conditions.

Market frontrunners invest in advanced diagnostics such as AI-driven assessment tools, eco-friendly repair materials, and modular underpinning systems to enhance precision and customer outcomes. They also integrate technologies such as augmented reality inspections and predictive maintenance while forming strategic alliances with construction, insurance, and real estate partners, strengthening competitive positioning and accelerating the adoption of foundation repair solutions globally.

Key Industry Developments:

- In June 2025, Landmark Foundation Group (LFG) launched a strategic growth platform to help independent foundation repair and waterproofing companies scale their operations while preserving local leadership, culture, and brand legacy. Led by CEO Jason Courtney, LFG delivers tailored strategic, operational, and financial resources that strengthen partner capabilities and drive sustainable expansion.

- In January 2025, CenterOak Partners LLC launched Solid Ground Solutions as a strategic platform to consolidate regional foundation repair businesses across the Central U.S., strengthening operational efficiency and expanding service capacity under established brands. The firm appointed Seth Tomasch as CEO, leveraging his more than 20 years of leadership experience in sponsor-backed portfolio companies to drive platform growth and execution.

Companies Covered in Foundation Repair Services Market

- Foundation Repair Services, Inc.

- BASIC FOUNDATION REPAIR

- Eric’s Concrete & Masonry Services Ltd.

- Connecticut Basement Systems

- Supportworks, Inc.

- Dwyer Companies

- Groundworks

- SOS Foundation Repair

Frequently Asked Questions

The global foundation repair services market is projected to reach US$3.0 billion in 2026.

Aging infrastructure, soil instability, and rapid urbanization increase the need for residential and commercial foundation maintenance and repair.

The foundation repair services market is expected to grow at a CAGR of 4.6% from 2026 to 2033.

Technological innovations, advanced repair materials, preventive maintenance, and expansion in emerging regions.

Foundation Repair Services, Inc., Basic Foundation Repair, Eric’s Concrete & Masonry Services Ltd., and Connecticut Basement Systems are the leading players.