- Home Care & Utilities

- Floriculture Market

Floriculture Market Size, Share, and Growth Forecast, 2026 - 2033

Floriculture Market by Product Type (Cut Flowers, Potted Plants, Bedding Plants), Flower Type (Roses, Lilies, Others), Floral Fashion Type (Fresh Accessories, Live Appliqué, Botanical Jewelry), Application (Decorative, Industrial, Others), and Regional Analysis 2026 - 2033

Floriculture Market Size and Trends Analysis

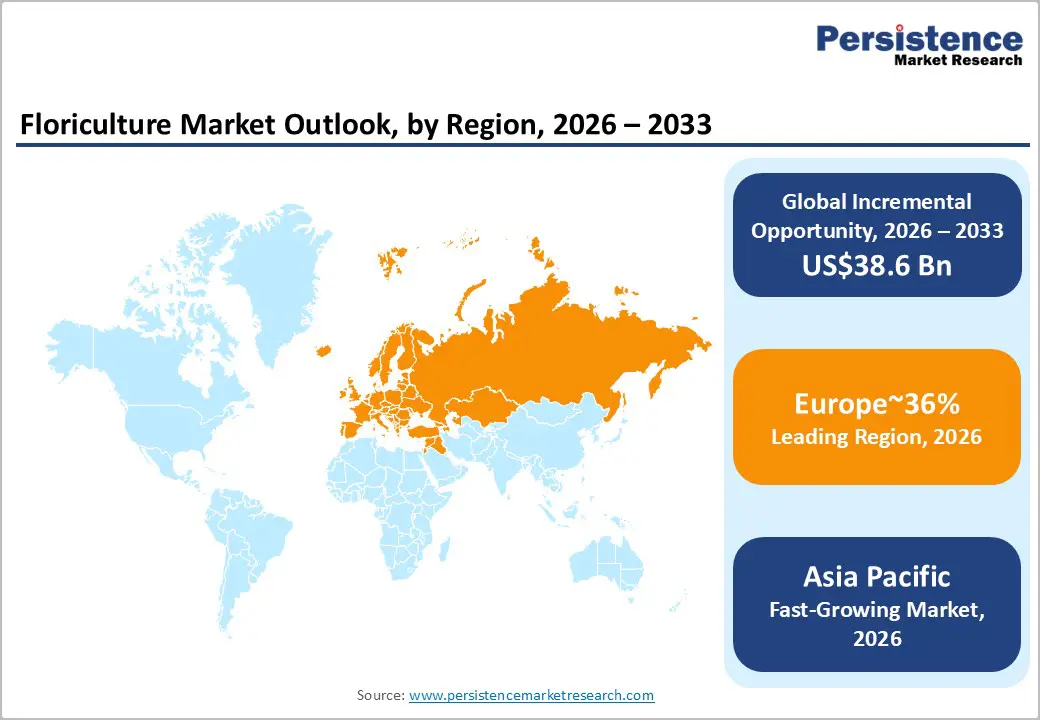

The global floriculture market size is likely to be valued at US$65.9 billion in 2026 and is expected to reach US$104.5 billion by 2033, growing at a CAGR of 6.8% during the forecast period from 2026 to 2033, driven by the rising demand for ornamental plants in residential and commercial spaces, supported by urbanization and gifting traditions.

The floriculture market includes the cultivation and trade of cut flowers, potted plants, and related products for decorative, industrial, and other purposes. Key drivers of growth include rising urbanization, which fuels the demand for indoor plants, and the expansion of e-commerce, which facilitates direct-to-consumer sales. Improvements in greenhouse technology and biotechnology enhance production efficiency, while strong export activity from major regions such as Europe supports higher trade volumes.

Key Industry Highlights:

- Leading Region: Europe due to its dominant role in trade, auction-based distribution, and advanced cultivation ecosystems, accounting for 36% share of the global market, technology integration, and ecosystem advantages.

- Fastest-growing Region: Asia Pacific due to rapid urbanization, rising disposable incomes, and adoption across floriculture sectors. Key countries are expected to drive adoption through manufacturing scale, gifting demand, and infrastructure initiatives.

- Leading Flower Type: Roses to account for approximately 32% share through industrial adoption, throughput, quality, and high-value applications.

- Leading Floral Fashion Type: Fresh accessories to dominate for simplicity, cost, adoption, and functional use across key sectors, holding approximately 45% share.

| Key Insights | Details |

|---|---|

|

Floriculture Market Size (2026E) |

US$65.9 Bn |

|

Market Value Forecast (2033F) |

US$104.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Urbanization and Rising Disposable Incomes

The ongoing urbanization trend is significantly driving the market by increasing access to ornamental plants and flowers in densely populated cities. As urban consumers seek aesthetic improvements for residential, commercial, and public spaces, demand for flowers consistently rises across retail, hospitality, and corporate sectors. This is further amplified by rising disposable incomes, which encourage the purchase of premium and seasonal floral varieties, especially those with advanced packaging and extended shelf life. Retail distribution has adapted through modern floristry outlets, e-commerce platforms, and subscription models, optimizing reach and minimizing post-harvest losses. Urban landscaping initiatives and municipal beautification projects also embed flowers into infrastructure, driving demand from public sector budgets.

Technology plays a crucial role, with climate-controlled storage, automated sorting systems, and precision irrigation ensuring year-round availability while maintaining quality. Consumers’ preference for exotic and rare flowers reconfigures cultivation, sourcing, and cold-chain management strategies. Regulatory frameworks governing pesticide use and quality standards influence production and distribution costs. Digital marketing and greenhouse automation further support firms in maintaining profitability. The combined effects of urbanization, rising incomes, and technological integration not only expand the market but also increase its complexity, fostering both growth and supply chain sophistication in the floriculture sector.

Biophilic Design & Mental Wellness

The post-pandemic focus on mental wellness is driving increased demand for biophilic design within the global market. Urban residential and commercial spaces are integrating potted plants, foliage, and green installations to improve occupant well-being, air quality, and aesthetics. Corporate offices and hospitality chains are allocating budgets for green infrastructure, embedding floriculture procurement into their operational and capital expenditure frameworks. This shift is spurring the adoption of premium, low-maintenance plants that align with long-term design standards and minimize replacement costs.e

Technology-enabled solutions, such as automated irrigation, smart lighting, and climate-controlled displays, enhance plant survival and quality, boosting value-chain efficiency. Regulatory oversight on plant importation, pesticide use, and indoor air quality further shapes sourcing and production strategies. The convergence of lifestyle-driven demand and institutional investment strengthens floriculture’s role in urban planning and wellness-focused design.

This demand for biophilic elements also drives product diversification across species and sizes, creating high-margin segments and complex supply chains. E-commerce platforms and wholesale distributors are standardizing logistics, reducing losses, and improving profitability. Corporate green spaces elevate recurring procurement cycles, influencing production and greenhouse capacity planning. Integration of floriculture into wellness and sustainability initiatives enhances brand value, creating predictable revenue streams for growers and suppliers. This trend propels the market expansion while driving technological, logistical, and regulatory advancements.

Barrier Analysis - Cold Chain Logistics and Carbon Footprint Costs

The market faces significant structural challenges due to its reliance on cold chain logistics, particularly for intercontinental trade between South America, Africa, Europe, and North America. Air freight, the primary mode of transportation for perishable flowers, exposes the industry to fuel price volatility and operational inefficiencies. Rising aviation fuel costs and stringent carbon emission regulations, such as the EU's carbon border tax, add to supply-chain expenses, increasing per-unit logistics costs and compressing margins for growers, exporters, and distributors. These factors also influence pricing strategies across retail and institutional channels.

Temperature-sensitive products require specialized handling, packaging, and climate-controlled storage, complicating operational workflows. To maintain product quality and regulatory compliance, procurement, inventory management, and route optimization are critical. The need for carbon footprint compliance is pushing growers and distributors to reconsider sourcing and transportation models, exploring nearshoring, alternative transport options, and energy-efficient cold chain solutions. Regulatory scrutiny intensifies documentation and reporting obligations, affecting operational timelines and financial planning. The combination of logistics dependency, climate sensitivity, and environmental policies creates persistent barriers to margin stability, constraining market expansion and requiring systemic adjustments in supply-chain operations.

Climate Change and Yield Volatility

The market faces increasing challenges due to climate-induced supply variability, with extreme weather events in key production regions such as Colombia and Kenya disrupting flower availability. Unseasonal rains and heatwaves alter cultivation schedules, leading to erratic flowering cycles and reduced predictability for exporters. These environmental shifts also increase pest prevalence, disease, and post-harvest losses, affecting efficiency throughout the supply chain. Growers are turning to controlled-environment agriculture, such as advanced greenhouses and automated monitoring, to stabilize production.

While these solutions improve reliability, they significantly raise capital and operational costs, making it harder for smaller producers to compete. The combination of climate volatility, pest pressures, and technology adoption alters supply chain risk profiles, impacting procurement, inventory, and regional sourcing strategies. Yield instability also influences market pricing, with short-term cost fluctuations for wholesalers and retailers. Investment in greenhouse infrastructure reallocates resources toward energy, climate control, and monitoring technology, raising the overall cost structure. Regulatory frameworks on water use and sustainability add further compliance costs. Together, climate change and yield volatility create structural barriers, embedding production risk and high capital requirements into the global floriculture ecosystem.

Opportunity Analysis - Genetics and Breeding Innovation

Advancements in genetics and breeding present a structurally significant growth opportunity within the market, driven by the need for resilient and high-value plant varieties. Advancements in genetics and breeding present a key growth opportunity in the market, driven by the demand for resilient, high-value plant varieties. CRISPR and advanced breeding techniques enable the creation of drought-resistant, pest-tolerant, and longer-lasting flowers, addressing supply-chain vulnerabilities caused by climate volatility. These innovations focus on enhancing vase life, color diversity, and aesthetic appeal, while navigating regulatory and consumer concerns about genetic modification. By integrating these technologies into breeding programs, year-round availability is supported, reducing post-harvest losses and stabilizing margins across wholesale and retail segments.

Technology adoption in propagation systems, precision irrigation, and automated monitoring further optimizes genetic performance and cultivation efficiency. Regulatory frameworks shape the commercialization of novel varieties, influencing patenting, import/export approval, and labeling, thus guiding strategic investments. Breeding innovation drives product differentiation, allowing suppliers to charge premium prices for exclusive varieties. Enhanced genetic resilience reduces reliance on costly inputs such as pesticides, fertilizers, and energy-intensive greenhouse operations. Collaboration between research institutions, nurseries, and tech providers accelerates the scalability of resilient cultivars, expanding the market for specialty flowers and reinforcing global competitiveness. Overall, genetics and breeding offer significant opportunities, positioning technological innovation as a core driver of growth in floriculture.

Smart Farming and Precision Agriculture

The adoption of smart farming and precision agriculture technologies is transforming the global market. IoT-enabled sensors, AI-driven irrigation systems, and climate-monitoring platforms help growers optimize water usage, nutrient delivery, and microclimate control, improving yield predictability and reducing post-harvest losses. In developing markets, including India and Vietnam, these technologies modernize traditional practices, allowing smaller producers to achieve efficiencies once reserved for large-scale operations. Real-time data analytics and automated greenhouse management enhance pest control, energy optimization, and flowering cycle scheduling, ensuring higher quality and consistency.

Regulatory frameworks governing water use, sustainability, and energy efficiency also drive technology adoption, embedding compliance advantages into operations. This combination of digital tools and mechanized cultivation reshapes cost structures, margins, and scalability, positioning precision agriculture as a key growth driver. It also promotes higher-margin products by improving quality, uniformity, and vase life, enabling premium pricing in domestic and export markets. Technology-driven efficiency reduces reliance on labor-intensive practices, easing seasonal workforce challenges and lowering operational costs. Partnerships between tech providers, nurseries, and agricultural agencies accelerate deployment, ensuring wide-scale integration. In total, IoT and AI-enabled cultivation enhance productivity, reliability, and profitability, cementing smart farming as a long-term opportunity in floriculture.

Category-wise Analysis

Flower Type Insights

Roses are projected to lead, accounting for approximately 32% share in 2026, underpinned by their entrenched role as a symbol of romance, gifting, and luxury across Western and Asian consumer segments. Adoption remains anchored by consistent demand, superior supply-chain integration, and global familiarity, with wholesalers and retailers prioritizing operational efficiency, freshness preservation, and standardized transport in high-volume environments.

Ongoing innovation in cold-chain logistics, automated sorting, and climate-controlled storage continues to reinforce replacement cycles and product availability. Major players such as Dümmen Orange, Florensis, and Syngenta Flowers leverage comprehensive rose portfolios to maintain market lock-in and enterprise workflow integration. This combination of mature infrastructure, optimized logistics, and predictable consumer demand sustains the segment’s dominance within structured global floriculture operations.

Lilies and tropical varieties are expected to be the fastest-growing segment in the market, driven by emerging consumer preference for bold, architectural floral arrangements and premium ornamental aesthetics. Growth is catalyzed by the introduction of pollen-free hybrids, longer-lasting oriental lilies, and exotic tropical species that enhance visual appeal and reduce allergenic concerns.

Accelerating adoption is supported by greenhouse automation, precision irrigation, and post-harvest conditioning technologies, lowering operational friction for growers entering premium segments. Leading floriculture firms such as Dümmen Orange, Syngenta Flowers, and Florensis are expanding hybrid and exotic portfolios to capture early-cycle demand and embed switching advantages.

Floral Fashion Type Insights

Fresh accessories are projected to lead the floral fashion market, accounting for approximately 45% share in 2026, underpinned by their entrenched role in weddings, proms, and formal events across Europe and Asia. Adoption remains anchored by consistent cultural relevance, high aesthetic appeal, and recurring utilization, with designers and event planners prioritizing quality, durability, and standardized production for high-volume occasions.

Ongoing evolution in floral preservation techniques, moisture-retentive packaging, and automated assembly continues to reinforce product availability and seasonal reliability. Leading brands such as Interflora, Teleflora, and Fleurop maintain extensive fresh accessory portfolios, integrating corsages, boutonnieres, and hair florals into event workflows. This combination of cultural embeddedness, operational consistency, and portfolio depth sustains the segment’s dominance within structured high-value floral fashion deployments.

Botanical jewelry is expected to be the fastest-growing segment in the floral fashion market, driven by emerging demand for sustainable, living art pieces in couture and bridal applications. Growth is catalyzed by biotechnology-enabled durability, use of succulent cuttings, orchids, and other live flora, which enhance longevity and aesthetic innovation.

Accelerating adoption is supported by precision cultivation, moisture-controlled mounting techniques, and digital marketing channels that reduce friction for first-time consumers. Key players such as Atelier Flora, FloraFolk, and Verdant Creations are expanding collections of wearable living plants to capture early-cycle demand and embed experiential appeal. As craftsmanship, technology integration, and social media influence mature, this segment is expected to outpace overall market growth over the forecast period.

Regional Insights

Europe Floriculture Market Trends

Europe is expected to remain the leading regional market in global floriculture, accounting for approximately 36% share in 2026, supported by its structurally dominant position in trade, auction-based distribution, and advanced cultivation ecosystems. The Netherlands anchors the regional supply chain, functioning as the primary re-export hub with sophisticated auction infrastructure, enabling transparency, liquidity, and high-volume throughput. Technological integration, including biotech-driven sustainable hybrids, precision greenhouse systems, and climate-controlled storage, continues to reinforce supply reliability and margin stability. Consolidated vendor landscapes, exemplified by Flamingo and Royal FloraHolland, support enterprise-scale operations and long-term export commitments, while eco-compliance and EU Green Deal alignment embed sustainability into operational workflows.

The Netherlands is expected to continue shaping Europe’s floriculture momentum, anchoring regional trade through auctions, biotech partnerships, and export optimization. Investments in facility expansions and precision cultivation technologies enable higher yields, longer vase life, and eco-friendly product lines, reinforcing competitive positioning. Regulatory harmonization under the EU Green Deal strengthens the adoption of sustainable farming practices, while pesticide residue limits incentivize cleaner production methods that influence upstream supply chains in Germany, the U.K., France, and Spain. The Netherlands-based initiatives, such as HilverdaFlorist’s eco-rose programs, are projected to drive incremental export growth, establishing the country as both a technology and trade nucleus. Consequently, Europe’s forward-looking market outlook is anchored in integrated innovation, supply-chain sophistication, and regulatory-aligned expansion across leading continental hubs.

North America Floriculture Market Trends

North America is expected to remain a mature and structurally stable market in global floriculture, with demand primarily anchored in replacement cycles, compliance-driven upgrades, and enterprise optimization strategies rather than greenfield capacity expansion. E-commerce and subscription-based delivery models further reinforce recurring demand, while wellness-driven adoption of potted plants stabilizes revenue streams. The market is characterized by a fragmented vendor landscape, where local growers differentiate through freshness and sustainability credentials, competing alongside imports from Colombia and Ecuador.

The U.S. is expected to anchor North America’s market momentum, shaping regional dynamics through high import volumes, domestic innovation, and sustainability-oriented adoption. California’s advanced breeding programs, particularly in disease-resistant lilies, are projected to reduce post-harvest losses and enhance margin stability for domestic growers. Retailers increasingly emphasize traceability, eco-certification, and quality differentiation, influencing procurement strategies and vendor partnerships. Investment flows toward greenhouse expansions, automation technologies, and hydroponic infrastructure are set to reinforce productivity while supporting premiumization.

Asia Pacific Floriculture Market Trends

Asia Pacific is anticipated to be the fastest-growing region, as rapid urbanization, expanding middle-class populations, and rising disposable incomes accelerate consumption and industrial scaling. Growth is driven by technology-enabled cultivation, including biotech hybrids, precision greenhouse systems, and advanced post-harvest handling, which enhance flower quality, shelf life, and export readiness. Manufacturing and cost advantages across low-cost labor nations such as Vietnam and India support scalable production for both domestic and international markets. Cultural gifting traditions, combined with festivals and ceremonial consumption, embed recurring demand, while investment in greenhouse expansion and controlled-environment agriculture enhances productivity and resilience, positioning Asia Pacific as a scale-driven, high-growth floriculture hub.

India is expected to anchor Asia Pacific’s regional momentum, shaping market expansion through domestic consumption, export orientation, and digital supply-chain integration. Rapid urbanization and westernized gifting trends are organizing previously fragmented markets, particularly via ONDC-enabled platforms that streamline procurement and distribution. Consequently, India’s structural role is set to reinforce Asia Pacific’s high-growth trajectory, combining domestic consumption, export competitiveness, and technology-led industrial scaling across the region.

Competitive Landscape

The global floriculture market is moderately fragmented, with leadership concentrated among global suppliers such as Dümmen Orange, Syngenta Flowers, and Royal FloraHolland, which dominate genetics, breeding, and high-value distribution channels, while a large base of small-to-medium growers manages cultivation and local supply. Top players also set technology standards through investments in biotech hybrids, climate-controlled cultivation, and automated post-harvest systems, reinforcing their structural position within both domestic and export markets.

Competitive positioning among leading firms is defined by horizontal differentiation across flower categories and vertical integration from genetics to logistics, as exemplified by Dümmen Orange’s hybrid breeding programs and Royal FloraHolland’s auction platforms. The sector is increasingly defined by technology-enabled service models, premium hybrid adoption, and expansion of eco-compliant cultivars, indicating forward-looking consolidation of workflow influence while preserving structural fragmentation in small-scale farming and local retail segments.

Key Industry Highlights:

- In January 2026, Selecta One partnered with Tapp Paper Dataloggers to integrate paper-based data loggers into its global logistics, reducing electrical and plastic waste by 90% by eliminating lithium batteries and plastic housings for temperature monitoring.

- In September 2025, Prayagraj (India) launched six polyhouses and two net houses under the Horticulture Development Mission to grow export-quality roses, ensuring optimal growing conditions for high-value exports to Russia and the Middle East.

- In August 2025, Ball Horticultural earned “gold” status as a US Best Managed Company for the fifth consecutive year, highlighting its strong financial performance and strategic excellence as a leading global partner.

Companies Covered in Floriculture Market

- Dümmen Orange

- Syngenta Flowers

- Royal FloraHolland

- Selecta Cut Flowers

- Forest Produce Ltd.

- Danziger Group

- Oserian Group

- Marginpar BV

- Esmeralda Farms

- Finlays

- Beekenkamp

- Florensis

- Flamingo Horticulture

- Arcangeli Giovanni

- Karen Roses

- Multiflora

Frequently Asked Questions

The global floriculture market is projected to be valued at US$65.9 billion in 2026 and is expected to reach US$104.5 billion by 2033, driven by rising demand for ornamental plants in residential and commercial spaces, urbanization, and the expansion of e-commerce channels.

The integration of plants into interiors for improved well-being, air quality, and aesthetics has shifted from a trend to a structural demand. Corporate, hospitality, and residential sectors now allocate budgets for green infrastructure, making floriculture procurement a regular part of operations and wellness-focused design.

The floriculture market is forecast to grow at a CAGR of 6.8% from 2026 to 2033, reflecting steady expansion from both traditional gifting occasions and newer applications in corporate wellness and interior landscaping.

Europe is expected to lead the market with a 36% share in 2026, driven by the Netherlands' global trade hub and advanced auction infrastructure. Asia Pacific is the fastest-growing region, fueled by urbanization, a growing middle class, and modernizing supply chains in India and China.

The floriculture market is moderately fragmented, with leadership concentrated among global genetics and breeding specialists such as Dümmen Orange and Syngenta Flowers. Royal FloraHolland dominates as the primary auction and distribution platform. Key growers and exporters include Oserian Group, Marginpar BV, and Flamingo Horticulture, which compete through scale, quality, and integration with global cold-chain logistics.