- Specialty & Fine Chemicals

- Flame-Retardant Foams and Insulation Market

Flame-Retardant Foams and Insulation Market Size, Share, and Growth Forecast, 2026 – 2033

Flame-Retardant Foams and Insulation Market by Product Grade (Standard/Commercial, Acoustic, Others) Application Form (Rigid Boards, Flexible Foams, Spray Polyurethane Foams), End-user (Construction, Others), and Regional Analysis 2026 – 2033

Flame-Retardant Foams and Insulation Market Size and Trends Analysis

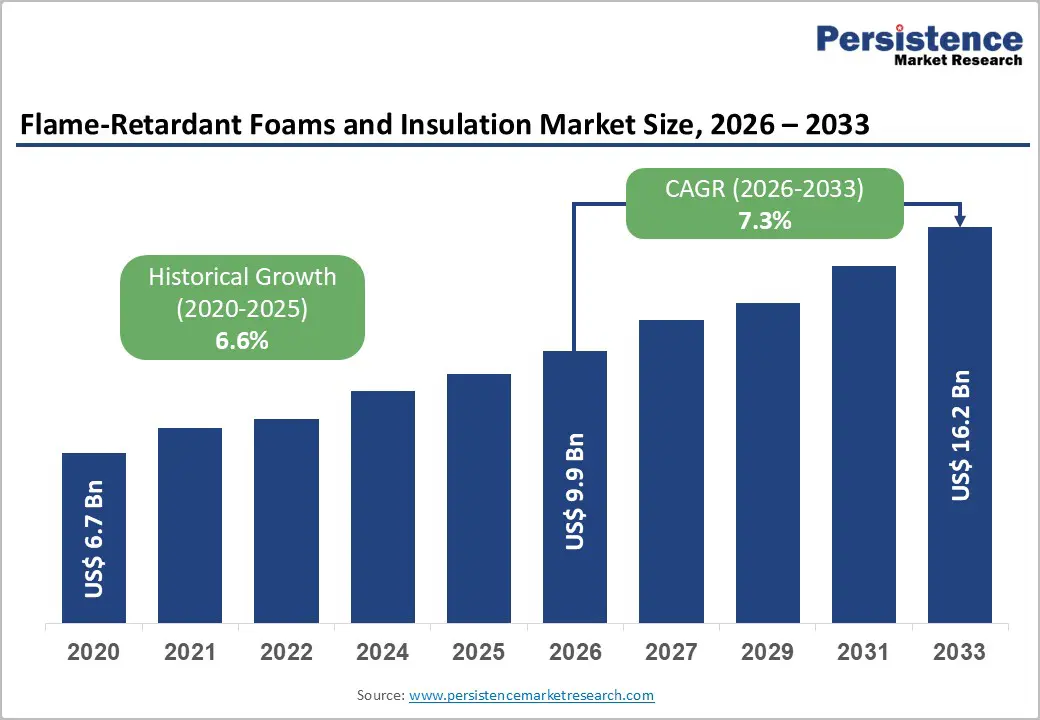

The global flame-retardant foams and insulation market size is likely to be valued at US$9.9 billion in 2026 and is expected to reach US$16.2 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033, driven by the rising global frequency of high-rise urban development and the rapid electrification of the automotive sector, both of which necessitate advanced passive fire protection systems. Key growth catalysts include the mandatory integration of non-combustible insulation in high-density residential projects and the critical need for thermal runaway prevention in Electric Vehicle (EV) battery packs. Stringent fire safety regulations in construction and rising demand from the EV sector drive this expansion. As the industry shifts toward halogen-free and bio-based formulations, manufacturers are increasingly prioritizing sustainability alongside safety performance to meet evolving regulatory benchmarks.

Key Industry Highlights:

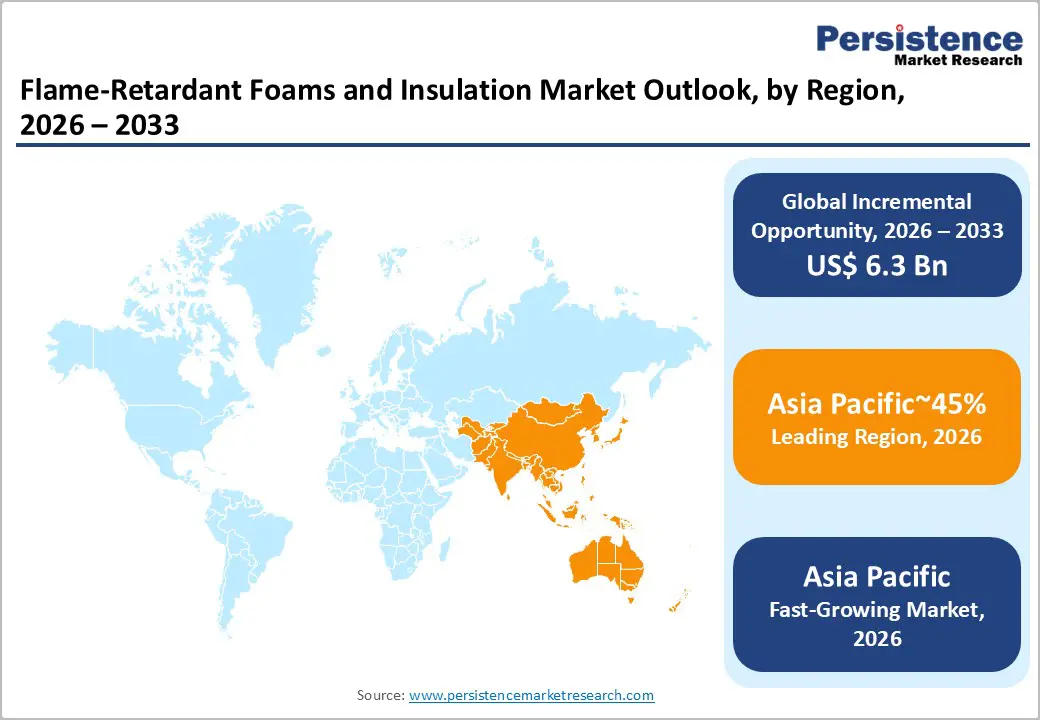

- Leading Region: Asia Pacific is projected to lead due to large-scale manufacturing, low-cost production, rapid urbanization, and integrated chemical parks, accounting for approximately 45% share in 2026, supported by technology adoption and ecosystem advantages across construction, industrial, and electronics sectors.

- Fastest-Growing Region: Asia Pacific is anticipated to grow fastest due to infrastructure expansion, urbanization programs, EV deployment, and residential/commercial retrofit adoption across sectors.

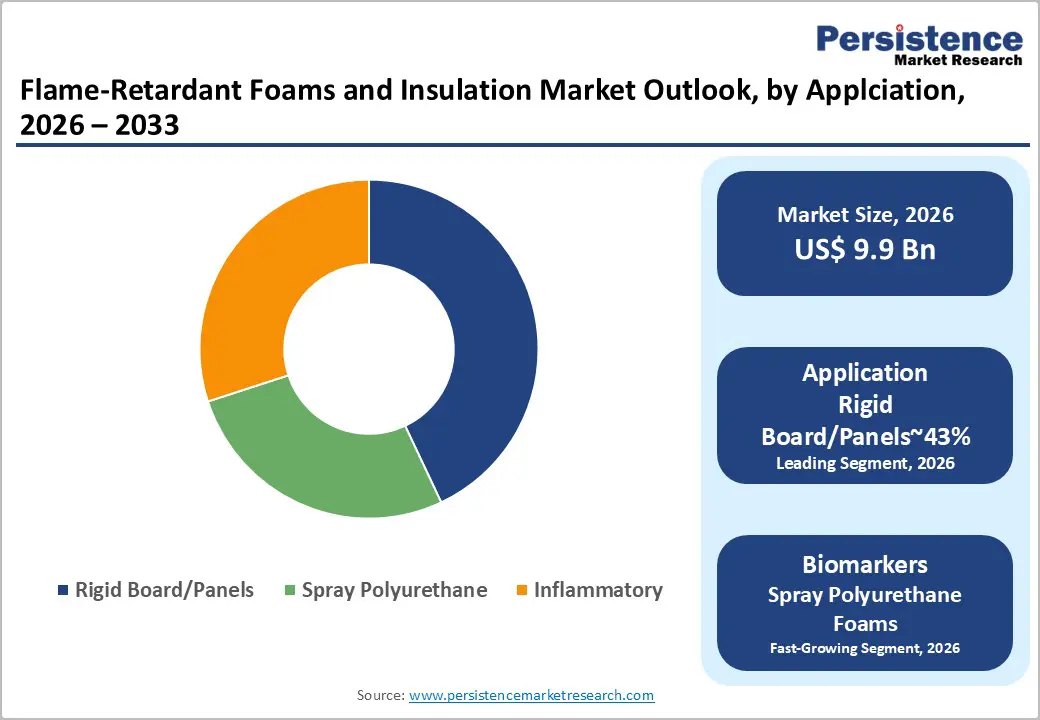

- Leading Product Grade: Standard/Commercial foams are expected to lead, accounting for approximately 69% share through industrial adoption in 2026, high throughput, consistent quality, and use in high-value applications such as cold-chain logistics, residential, and commercial construction.

- Leading Application Form: Rigid Boards/Panels are projected to dominate for simplicity, cost-efficiency, adoption, and functional use across key sectors, holding approximately 43% share in 2026, underpinned by structural integrity, high R-values, and wide acceptance in construction and pre-engineered building projects.

| Key Insights | Details |

|---|---|

| Flame-Retardant Foams and Insulation Market Size (2026E) | US$9.9 Bn |

| Market Value Forecast (2033F) | US$16.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Expansion of Flame-Retardant Insulation Demand Driven by EV and Energy Storage Growth

The accelerating adoption of electric vehicles and energy storage systems is structurally elevating demand for flame-retardant foams within the electrical and electronics sector. Thermal management challenges in lithium-ion battery packs, particularly the risk of thermal runaway, necessitate high-performance fire-resistant solutions that prevent cascading failures. Advanced FR foams meeting UL 94 V-0 ratings are increasingly integrated into battery enclosures and module barriers, simultaneously reducing weight compared to conventional metallic alternatives. These materials enhance vehicle efficiency, extend operational range, and align with stringent fire-safety mandates imposed by regulatory bodies and Tier-1 automotive manufacturers. Innovation in polymer formulation and processing techniques further improves thermal insulation while maintaining structural stability under high-temperature scenarios, reinforcing adoption across evolving EV platforms.

Simultaneously, the broader energy storage ecosystem, encompassing grid-scale and residential applications, is driving material requirements that combine thermal, electrical, and mechanical performance. Fire-retardant foams provide critical protective layers for densely packed cells, mitigating propagation risks in high-capacity systems. Regulatory compliance and performance expectations are intensifying pressure on manufacturers to deploy lightweight, thermally stable, and chemically resilient insulation solutions. As EV penetration and energy storage deployments expand globally, the integration of high-grade flame-retardant foams becomes a foundational enabler for safe, efficient, and scalable electrification infrastructure.

Surge in Flame-Retardant Foam Adoption Driven by Urbanization and Construction Expansion

Rapid urbanization and large-scale construction activity are intensifying demand for flame-retardant foams in residential, commercial, and industrial buildings. Rising urban populations necessitate expanded housing, transportation, and commercial infrastructure, directly increasing insulation requirements across walls, roofs, and facades. Rigid boards are emerging as the dominant application due to their structural stability, thermal efficiency, and ability to reduce energy consumption in buildings. Regulatory frameworks and building codes increasingly mandate fire-resistant materials, reinforcing adoption across high-density urban developments. Advances in foam formulation and panel fabrication enhance durability, fire resistance, and installation efficiency, aligning with evolving architectural and sustainability standards.

Asia Pacific is particularly prominent due to extensive construction investments, concentrated urban growth, and high regulatory emphasis on energy-efficient buildings. The regional expansion reinforces demand for high-performance FR foams capable of meeting both safety and thermal performance requirements. As large-scale infrastructure projects proliferate, integrated solutions combining flame retardancy, insulation, and structural support are increasingly preferred. These dynamics collectively elevate rigid boards as a central solution, promoting safer, energy-efficient construction across emerging and mature urban markets.

Barrier Analysis – Raw Material Cost Pressures and Price Volatility Constraining FR Foam Adoption

The flame-retardant foam market faces persistent cost pressures driven by the high prices of specialty chemical precursors and additive systems. Production depends on materials such as Methylene Diphenyl Diisocyanate, Toluene Diisocyanate, and phosphorus- or nitrogen-based retardants, whose prices are closely linked to crude oil fluctuations and petrochemical supply chain disruptions. These input cost dynamics directly elevate the final price of rigid boards, flexible foams, and spray-applied insulation, creating structural constraints on margin stability across the value chain. Manufacturing processes must balance high-performance fire retardancy with cost efficiency, while price-sensitive segments risk adoption of lower-grade or non-certified substitutes, particularly in emerging or lightly regulated markets.

Volatility in feedstock availability and pricing introduces operational unpredictability, affecting procurement strategies and production planning. Integrated flame-retardant formulations, although essential for regulatory compliance and performance, further amplify cost intensity relative to standard foam grades. This environment intensifies competitive pressure, encouraging selective adoption in applications where performance and safety outweigh price sensitivity. As procurement and material costs remain uncertain, market participants must navigate structural challenges that inherently limit penetration, particularly in price-constrained construction and industrial segments.

Regulatory and Environmental Constraints from Halogenated Flame Retardants

The flame-retardant foam market is increasingly constrained by environmental and health regulations targeting halogenated retardants. Substances such as decabromodiphenyl ether are restricted under frameworks such as EU REACH and U.S. TSCA due to persistence, bioaccumulation, and toxicity concerns. Compliance requires substantial redesign of formulations, testing, and certification to achieve equivalent fire resistance with halogen-free alternatives. This regulatory shift elevates disposal costs, complicates lifecycle management, and limits adoption in specific polyurethane foam applications where legacy halogenated systems remain standard. The phasing out of nearly a third of halogenated materials introduces structural headwinds, slowing innovation cycles and reducing the effective growth rate of affected segments.

Manufacturers face intensified R&D demands to maintain performance parity while meeting stricter environmental compliance. Small and mid-sized enterprises encounter particularly high entry barriers due to capital intensity associated with formulation redesign, product recertification, and testing compliance. The combined impact of regulatory scrutiny, higher operational costs, and substitution challenges constrains product penetration in key end-use applications. As global policy frameworks tighten, the market must increasingly pivot toward halogen-free chemistries, embedding sustainability considerations into material selection and production practices.

Opportunity Analysis – Sustainable and Bio-Based Flame-Retardant Foams

Rising demand for green building certifications such as LEED and BREEAM is driving innovation in sustainable flame-retardant foams. Bio-based polyols derived from soy, castor, and other renewable sources are increasingly replacing conventional petroleum-based formulations, while eco-friendly additives such as expandable graphite and aluminum trihydrate enhance fire resistance. These materials offer reduced embodied carbon, improved recyclability, and alignment with corporate ESG mandates, creating structural incentives for adoption across commercial and residential construction projects. Manufacturers are focusing on integrating high fire-rating performance with environmental sustainability to meet evolving regulatory and market expectations.

The growth of sustainable insulation reflects broader industry trends prioritizing energy efficiency and circular material use. Incorporation of bio-based retardants and renewable polyols reduces lifecycle environmental impact while maintaining thermal and mechanical performance. As green building initiatives expand globally, the adoption of eco-friendly FR foams enables developers and architects to meet compliance targets and certification requirements. These dynamics establish sustainable formulations as a high-value segment, creating structural market opportunities for materials that simultaneously satisfy fire safety, environmental, and performance standards.

Expansion of Acoustic High-Performance Flame-Retardant Foams

Acoustic flame-retardant foams are increasingly adopted to meet stringent noise-control requirements in data centers, telecommunications hubs, and electronic facilities. These materials combine sound absorption with thermal and fire-resistant performance, addressing the dual regulatory pressures of fire safety and acoustic compliance. Rising demand for high-density electronic infrastructure, including 5G deployment and server farms, reinforces the need for specialized foam solutions capable of mitigating reverberation, vibration, and airborne noise without compromising safety. Development of these acoustic variants reflects broader market trends emphasizing multifunctional performance across critical environments.

The convergence of fire-resistance and acoustic functionality supports premium product positioning within the insulation market. Partnerships between electronics integrators, data center operators, and foam manufacturers enable tailored solutions that command higher pricing due to performance differentiation. Enhanced material formulations allow integration into walls, ceilings, and equipment housings while maintaining compliance with fire codes and acoustic standards. As noise regulation enforcement intensifies, adoption of acoustic high-performance FR foams is structurally expanding, creating a defined market segment aligned with advanced electronics infrastructure requirements and performance-driven procurement strategies.

Category–wise Analysis

Product Grade Insights

Standard/Commercial is expected to lead, accounting for approximately 69% share in 2026, underpinned by its entrenched role across residential, commercial, and cold-chain construction applications. Adoption remains anchored by cost efficiency, scalability, and thermal performance, with providers prioritizing standardized production and workflow integration to meet high-volume project demands. Polyurethane (PU) and Polyisocyanurate (PIR) variants dominate due to superior thermal resistance-to-thickness ratios, enabling deployment in space-constrained urban construction, HVAC systems, and appliance insulation. Ongoing platform evolution, including bio-circular feedstocks and AI-optimized formulations, reinforces utilization intensity and compliance with green building certifications. Leading brands such as Owens Corning, Saint-Gobain, and Huntsman Corp maintain portfolio ecosystems that integrate additive chemistry and high-volume production capabilities.

Acoustic foams are expected to be the fastest-growing, driven by emerging safety and performance requirements in high-risk applications such as EV battery enclosures, tunnels, and aircraft interiors. Growth is being catalyzed by advanced low-smoke, zero-halogen (LSZH) formulations that resist melting or dripping, improving fire safety, visibility, and air quality during emergencies. Accelerating adoption is supported by dual-purpose acoustic-thermal hybridization, enabling sound attenuation in data centers and open-plan offices, while AI-assisted optimization improves material density and fire performance. BASF’s Basotect® and Kingspan Kooltherm® platforms capture early-cycle demand by embedding thermal runaway protection and structural fire integrity into projects.

Application Form Insights

Rigid Boards/Panels are expected to lead the Flame-Retardant Foams and Insulation market, accounting for approximately 43% share, underpinned by their entrenched role across construction, pre-engineered buildings, and cold-storage applications. Adoption remains anchored by superior thermal resistance, structural integrity, and ease of mechanical installation, with providers prioritizing standardized production and workflow integration for large-scale projects. Polyisocyanurate (PIR) and polyurethane (PU) variants dominate due to high R-values, durability, and compatibility with wall and roofing assemblies, supporting retrofit and new-build deployments globally. Ongoing platform evolution, including low-embodied-carbon feedstocks and factory-applied fire-resistant facers, continues to reinforce utilization intensity. Leading brands such as Kingspan, Metl-Span, Owens Corning, and Johns Manville maintain comprehensive rigid board portfolios, integrating advanced thermal performance and fire safety features.

Spray Polyurethane Foam (SPF) is expected to be the fastest-growing segment, driven by emerging energy-efficiency and air-sealing requirements in residential, commercial, and retrofit projects. Growth is being catalyzed by on-site application capabilities that provide seamless coverage, fill irregular gaps, and reduce labor time, enhancing adoption across complex geometries and older buildings. Accelerating deployment is supported by ultra-low VOC, high-yield formulations and HFO blowing agents, which improve environmental performance while maintaining fire resistance. Huntsman Building Solutions’ Icynene line and robotic spray systems exemplify industrial innovation, capturing early-cycle demand.

Regional Insights

Asia Pacific Flame-Retardant Foams and Insulation Market Trends

Asia-Pacific is expected to dominate the flame-retardant foams and insulation market, as well as representing the fastest growing region, accounting for approximately 45% share in 2026, underpinned by its entrenched role across high-volume construction, industrial manufacturing, and electronics sectors. Adoption remains anchored by low-cost production, extensive chemical parks, and rapid urbanization in China, India, and ASEAN nations, with providers prioritizing integrated supply chains and scale economics to support high-demand infrastructure projects. China leverages large-scale manufacturing for standard-grade foams, Japan focuses on precision and ultra-thin high-R-value applications, while India drives growth through residential and commercial construction programs. Ongoing platform evolution, including bio-based polyols and halogen-free electronics-grade foams, continues to reinforce regional utilization. Leading brands such as Wanhua Chemical Group, BASF SE, Kingspan Jindal, and Saint-Gobain dominate APAC portfolios, integrating material innovation, thermal performance, and fire safety.

India is expected to be the fastest-growing regional market in the Flame-Retardant Foams and Insulation market, driven by emerging urbanization, infrastructure expansion, and energy-efficiency retrofits. Growth is being catalyzed by large-scale programs such as the Pradhan Mantri Awas Yojana (PMAY) and Smart Cities Mission, which stimulate demand for high-performance rigid panels and spray-applied foams. Accelerating adoption is supported by EV deployment, where melamine and high-performance foams are integrated into battery compartments to enhance thermal safety. Localized production hubs, joint ventures, and industrial partnerships reduce supply chain friction, enabling rapid scale-up of standardized and specialty foams. As construction activity, high-rise developments, and electronics manufacturing continue to expand, demand for flame-retardant insulation solutions in India is expected to grow significantly.

North America Flame-Retardant Foams and Insulation Market Trends

North America is expected to represent the mature growth of the market region, underpinned by its entrenched role in advanced regulatory frameworks, industrial innovation, and high-performance construction applications. Adoption remains anchored by stringent safety codes, including the International Building Code (IBC) and state-level mandates such as California’s Technical Bulletin 117-2013, with providers prioritizing certified, high-density foams for automotive, aerospace, and residential energy-efficiency projects. Ongoing platform evolution, including next-generation spray polyurethane foams and EV battery thermal management solutions, reinforces utilization intensity while supporting energy-bill reduction and fire-safety objectives. Leading brands such as Owens Corning, Huntsman Corp, BASF SE, and Johns Manville integrate material innovation, high R-value performance, and industrial-grade flame retardancy into their portfolios.

The U.S. is expected to be the fastest-growing regional market, driven by expanding EV adoption, residential retrofit programs, and high-performance spray-foam demand. Growth is being catalyzed by increasing safety and energy-efficiency requirements in automotive, aerospace, and residential construction, where high-density foams deliver critical fire protection and thermal insulation. Accelerating deployment is supported by R&D innovations in spray-applied foams and hybrid acoustic-thermal solutions, enabling efficient coverage and labor savings in complex geometries. Industrial leaders, including Huntsman Corp and Owens Corning, are scaling advanced product lines that combine energy efficiency with UL-rated fire resistance.

Europe Flame-Retardant Foams and Insulation Market Trends

Europe is expected to maintain stable market growth, underpinned by its entrenched role in regulatory harmonization, environmental sustainability, and energy-efficient construction. Adoption remains anchored by strict fire-safety mandates, including bans on combustible cladding and mandatory A1/A2-rated non-combustible insulation, with providers prioritizing certified, high-performance boards and panels for commercial and residential retrofits. Ongoing platform evolution, including bio-based PU foams, chemical recycling, and circular economy initiatives, reinforces utilization while aligning with net-zero and EPBD recast targets. Leading brands such as BASF SE, Kingspan Group, Saint-Gobain, Armacell, and Rockwool A/S integrate sustainable materials, acoustic performance, and fire safety into their product ecosystems.

The U.K. is expected to be the fastest-growing regional market, driven by rising retrofit demand, energy-efficiency mandates, and urban high-rise expansion. Growth is being catalyzed by KfW-style subsidies, large-scale residential retrofit programs, and adoption of acoustic and low-emission foams, which improve thermal performance while reducing energy consumption. Accelerating deployment is supported by halogen-free, bio-based PU and elastomeric foams that satisfy evolving REACH and CPR compliance standards. Leading industrial players, including Kingspan Group and Armacell, are scaling low-embodied-carbon (LEC) products and circular-economy solutions to meet early-cycle retrofit demand.

Competitive Landscape

The global flame-retardant foams and insulation market is moderately fragmented, with leadership concentrated among global suppliers such as BASF SE, Kingspan Group, Saint-Gobain, Armacell, and Rockwool A/S. These leading players influence market structure through technological innovation, standard-setting in fire-resistance and acoustic performance, and the establishment of reliable supply chains that shape procurement strategies across construction, automotive, and electronics sectors. Competitive positioning varies, with firms differentiating through vertical integration of chemical feedstocks, specialized high-performance foams, and niche applications such as EV battery thermal management or retrofit acoustic solutions. Industry behavior reflects ongoing platform evolution, including the adoption of bio-based polyols, halogen-free formulations, and circular economy practices, alongside consolidation of regional production hubs and service-led distribution models.

Key Industry Developments:

- In February 2026, Kingspan Group inaugurated its first large-scale "Lower Embodied Carbon" (LEC) insulation plant in North America. This facility significantly reduces the carbon footprint of rigid boards, allowing the company to capture the "Green Building" certification market, which currently carries a price premium.

- In February 2026, Kingspan Group reported a record €751.9 million (US$881.18 million) investment in 2025, including new, large-scale, low-carbon insulation plants in North America.

Companies Covered in Flame-Retardant Foams and Insulation Market

- BASF SE

- Dow Inc.

- Huntsman Corporation

- Covestro AG

- Kingspan Group

- Armacell International S.A.

- Saint-Gobain S.A.

- Owens Corning

- Johns Manville

- Recticel NV/SA

- Knauf Insulation

- Zotefoams plc

- Zhejiang Wansheng Co., Ltd

- Lanxess

- Soprema

- ICL Group

Frequently Asked Questions

The global flame-retardant foams and insulation market is projected to be valued at US$9.9 billion in 2026 and is expected to reach US$16.2 billion by 2033, driven by demand from high-rise construction, electric vehicle battery safety, and energy storage systems requiring high-performance thermal and fire-resistant solutions.

Spray Polyurethane Foam (SPF) adoption is accelerating due to its ability to create seamless air and moisture barriers, fill irregular gaps, and reduce labor time on-site, making it ideal for energy-efficiency retrofits, complex geometries, and older buildings that cannot accommodate pre-cut rigid boards.

The market is forecast to grow at a CAGR of 7.3% from 2026 to 2033, supported by stringent fire safety regulations, EV battery thermal management requirements, and the transition to halogen-free, bio-based foam formulations.

Asia Pacific is the fastest-growing regional market, driven by urbanization, large-scale infrastructure programs such as PMAY and Smart Cities Mission, and increasing integration of high-performance foams in residential, commercial, and EV applications.

The market is moderately fragmented, with key players including BASF SE, Huntsman Corporation, Dow Inc., Covestro AG, Kingspan Group, Armacell International S.A., Saint-Gobain S.A., Owens Corning, Johns Manville, Recticel NV/SA, Knauf Insulation, Zotefoams plc, Zhejiang Wansheng Co., Ltd, Lanxess, Soprema, and ICL Group. These leaders compete through technological innovation, specialized high-performance foams, and integrated supply chains across construction, automotive, and electronics sectors.